Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

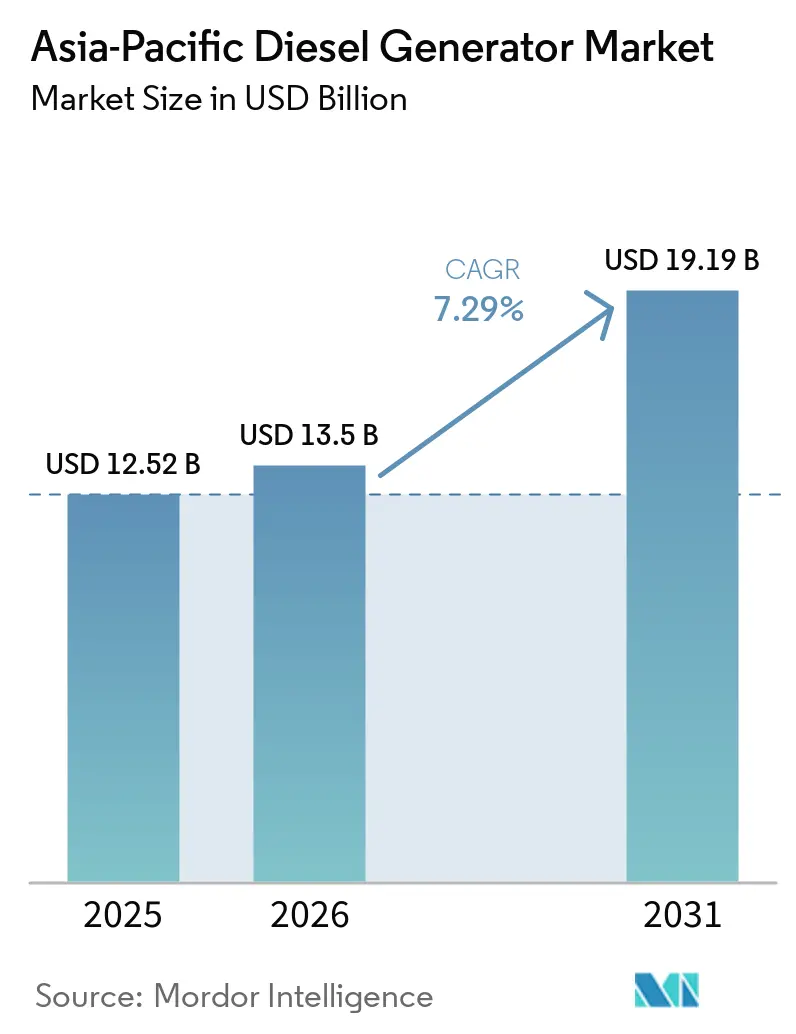

| Base Year Market Size (2025) | USD 12.52 Billion |

| Market Size (2026) | USD 13.5 Billion |

| Market Size (2031) | USD 19.19 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Diesel Generator Market Analysis by Mordor Intelligence

The Asia-Pacific Diesel Generator Market size is projected to expand from USD 12.52 billion in 2025 and USD 13.5 billion in 2026 to USD 19.19 billion by 2031, registering a CAGR of 7.29% between 2026 to 2031.

Industrial electrification outpacing grid upgrades, sovereign-AI policies that force hyperscalers to localize compute, and emission-norm-driven fleet renewal are combining to pull diesel sets from a standby niche into a mission-critical role across data centers, manufacturing corridors, and remote mine sites. OEMs are shifting pitch books from upfront cost to total cost of ownership as predictive-maintenance contracts and hybrid-ready controllers help buyers tame fuel volatility and compliance costs. India, Vietnam, Indonesia, and the Philippines dominate new installations because their grids operate with reserve margins below 12%, forcing industrial buyers to finance gensets as baseload insurance. Meanwhile, large-capacity arrays above 2 MW are rising fastest as hyperscale data halls demand N+1 redundancy and 72-hour fuel autonomy to preserve Tier IV uptime standards.[1]Cushman & Wakefield, “Asia Pacific Data Center Market Update,” cushmanwakefield.com

Key Report Takeaways

- By capacity, the 375-750 kVA bracket led with 45.1% of the Asia-Pacific diesel generator market share in 2025, while the above-2,000 kVA bracket is projected to register an 8.7% CAGR through 2031.

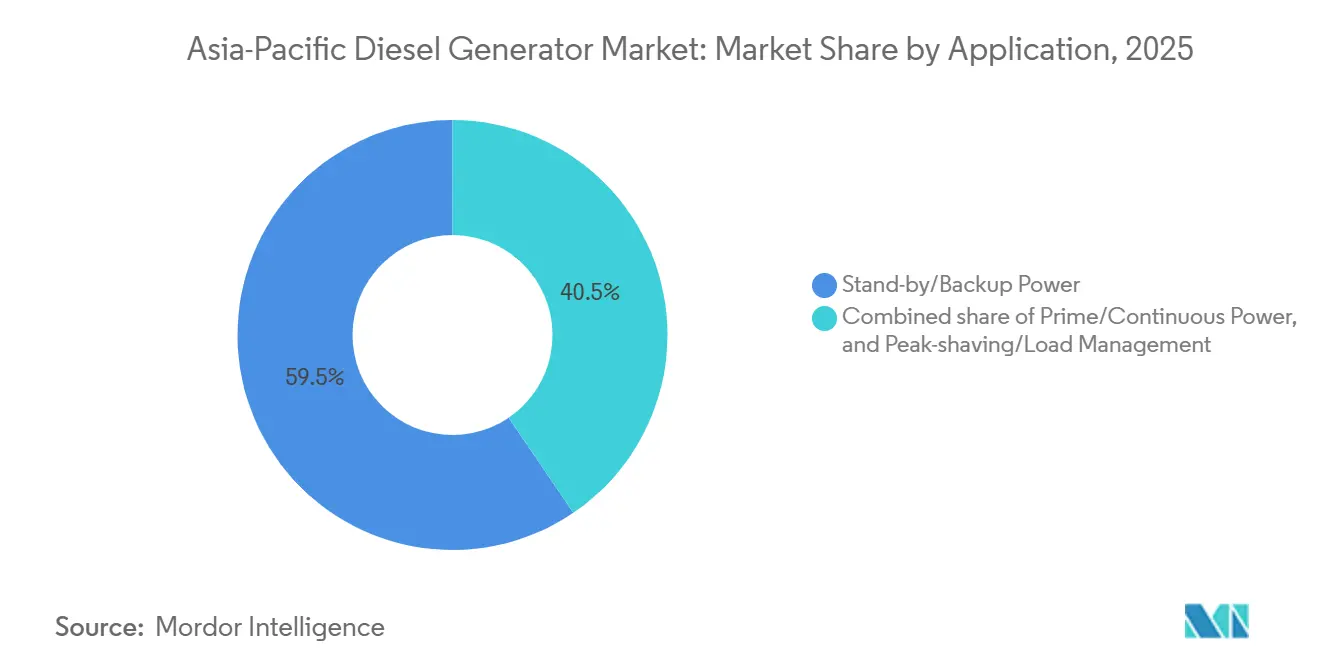

- By application, standby/backup power commanded 59.5% share of the Asia-Pacific diesel generator market size in 2025, and prime/continuous power is expected to expand at an 8.2% CAGR between 2026 and 2031.

- By end user, industrial sites held 44.4% share of the Asia-Pacific diesel generator market size in 2025, whereas the commercial segment is expected to advance at a 7.9% CAGR to 2031.

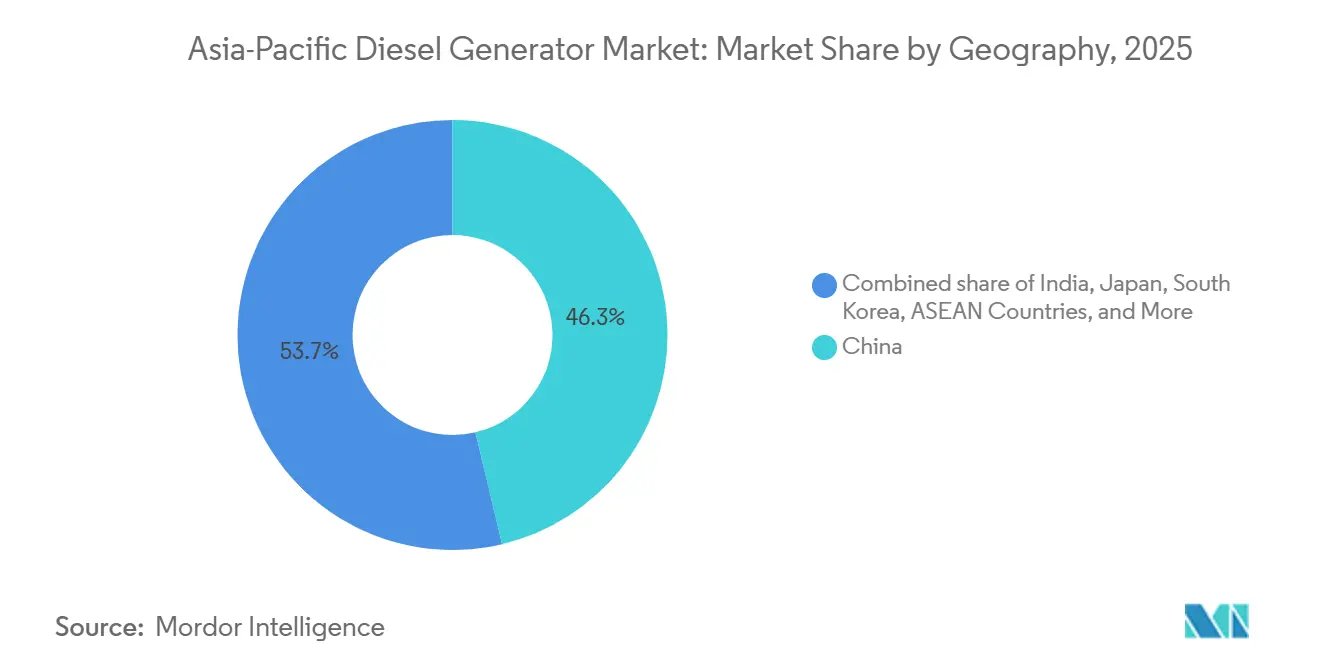

- By geography, China retained 46.3% of the Asia-Pacific diesel generator market share in 2025, yet India is expected to be the fastest 8.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialization & urbanization | +1.2% | India, Vietnam, Indonesia, Bangladesh | Medium term (2-4 years) |

| Data-center build-out boom | +1.5% | India, Malaysia, Singapore, China tier-1 cities | Short term (≤ 2 years) |

| Grid-reliability gaps & outage frequency | +0.9% | India, Indonesia, Philippines, Myanmar | Long term (≥ 4 years) |

| Hybrid micro-grids on island tourism hubs | +0.6% | Indonesia, Philippines, Thailand | Medium term (2-4 years) |

| Emission-norm driven replacement cycle | +1.1% | India, China, Japan | Short term (≤ 2 years) |

| Predictive-maintenance digital twins | +0.7% | Japan, South Korea, Australia, regional roll-outs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialization & Urbanization

India’s Production-Linked Incentive outlays of USD 30 billion across 14 sectors by 2025 deepened power-demand spikes in Tamil Nadu and Uttar Pradesh, where summer deficits touched 15%.[2]Press Information Bureau, “PLI Scheme Updates,” pib.gov.in Similar strains emerged in Vietnam’s Bac Ninh and Hai Phong electronics belts after USD 20 billion of FDI arrived in 2024, yet transmission upgrades trail demand by up to three years.[3]World Bank, “Vietnam Country Overview,” worldbank.org Buyers, therefore, budget for 750-2,000 kVA prime-rated sets, moving gensets from facilities overhead to core capex and extending replacement cycles to ten years. Fuel efficiency and Stage IV compliance have become board-level KPIs because continuous duty now dominates procurement briefs.

Data-Center Build-Out Boom

A 19,371 MW IT-load pipeline across Asia-Pacific in 2025 requires 1.2-1.5× redundancies, translating into 23,000-29,000 MW of diesel backup demand if all projects proceed. Adani’s pledged 5 GW AI campus in India alone implies 7,500 MW in gensets by 2035. Data-sovereignty statutes, such as Indonesia’s in-country hosting rule, accelerate localized build-outs in weak-grid markets, ensuring multi-megawatt gensets stay relevant even as renewable penetration rises.

Grid-Reliability Gaps & Outage Frequency

India’s T&D losses averaged 19% in 2024, while ASEAN’s reliability index trails OECD peers by 30-40%.[4]International Energy Agency, “Asia Pacific Energy Outlook,” iea.org Outage durations of 8-12 hours per month in Indonesian industrial zones push customers toward prime-power configurations, effectively doubling diesel runtime relative to pure standby roles. ASEAN utilities need USD 800 billion for grid upgrades by 2045, yet have secured only USD 47 billion by 2025, making private generation a long-term hedge.

Hybrid Micro-Grids on Island Tourism Hubs

A Komodo National Park resort cut diesel use 40% in 2025 by pairing 500 kW solar and 1 MWh batteries with 750 kVA sets. OEMs now bundle hybrid-ready controllers to win bids for Indonesia, Philippine, and Thailand, where logistics premiums push delivered diesel above USD 1.25 per liter, and sustainability standards tighten for ecotourism brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter emission regulations favoring gas & renewables | -0.8% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Volatile diesel prices | -0.5% | India, Indonesia, Philippines, broader global markets | Short term (≤ 2 years) |

| Corporate renewable PPAs cutting runtime | -0.4% | India, China, Singapore | Medium term (2-4 years) |

| Shortage of Tier-4 skilled technicians | -0.3% | ASEAN, India, aging workforce in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Emission Regulations Favoring Gas & Renewables

China’s National VI and India’s CPCB Stage IV add 15-20% to diesel genset capex, eroding the cost gap versus gas turbines and solar-plus-storage hybrids. Singapore’s carbon tax of SGD 25 per ton in 2024 rises to as high as SGD 80 by 2030, accelerating shifts to low-carbon backup.

Volatile Diesel Prices

Singapore spot diesel traded between USD 80-120 per barrel in 2024-2025, and Indonesia’s subsidy rollback lifted pump prices 30% in 2024. Operators now demand fuel-efficiency guarantees and hybrid capability, raising OEM engineering complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Large Units Gain as Data Centers Scale

The 375-750 kVA class captured 45.1% of the Asia-Pacific diesel generator market share in 2025. Telecom towers, mid-rise offices, and light factories prize its footprint and price. However, above-2,000 kVA units are forecast to post an 8.7% CAGR, making them the fastest contributor to the Asia-Pacific diesel generator market size growth. Hyperscalers parallel 2-3 MW blocks to reach 20 MW arrays, while Indonesian and Australian mines deploy multi-MW islands for off-grid hauling operations.

Below-75 kVA sets face solar-plus-battery substitution in urban homes, yet remain essential in remote clinics. The 75-375 kVA band benefits from India’s 5G rollout; 200,000 new macro towers in 2024-2025, each specified 30-50 kVA backup. ISO 8528 certification is now non-negotiable above 500 kVA as buyers demand transient load handling and harmonic control.

By Application: Prime Power Gains as Off-Grid Sites Multiply

Standby duty held 59.5% of the Asia-Pacific diesel generator market share in 2025, locked in by data-center uptime codes and hospital life-safety rules. Yet prime/continuous duty is expanding at an 8.2% CAGR through 2031, already topping 40% of the incremental Asia-Pacific diesel generator market size. Indonesian mines, Australian LNG sites, and Indian textile parks run diesels 6,000-8,000 hours yearly, demanding robust engines like Cummins QSK95 rated 3 MW prime.

Peak-shaving, though niche, grows where time-of-use tariffs exceed USD 0.20 per kWh. Japan’s 2024 Fire Service Act mandates 72-hour runtime for elder-care centers, nudging even standby orders toward prime-rated sets.

By End User: Commercial Segment Accelerates on Green-Building Mandates

Industrial buyers held 44.4% share in 2025 as auto, electronics, and chemical expansions required on-site baseload coverage. Commercial premises are on track for a 7.9% CAGR to 2031, driven by LEED and GRIHA rules that oblige malls, offices, and hotels to maintain independent backup. India’s 10 billion ft² certified stock in 2025 embedded 500-1,500 kVA per building. Data centers, counted in commercial, dwarf other verticals, explaining why commercial contributions to the Asia-Pacific diesel generator market size keep widening.

Residential uptake is flat, where rooftop solar and community batteries now match diesel on lifecycle cost. However, high-rise condos in Manila and Jakarta still specify 30-100 kVA sets to comply with elevator-safety codes during outages.

Geography Analysis

China anchored 46.3% of the Asia-Pacific diesel generator market share in 2025, yet policy-driven renewables and grid upgrades moderate its forward curve. India is pacing the region with an 8.5% CAGR through 2031 as USD 30 billion of PLI subsidies concentrate load in corridors whose grids lag by three years. Cummins’ USD 1 billion 2024 investment validates the shift.

Japan’s replacement cycle quickened under its 2024 72-hour mandate, moving care-facility owners from 50-75 kVA to 100-150 kVA enclosed models. South Korea’s semiconductor push requires ultra-clean 2-4 MW sets with <2% THD to protect lithography lines; Yanmar and Mitsubishi lead this high-margin niche.

ASEAN’s island geography cements diesel as the default backup. Indonesia and the Philippines endure 8-12-hour monthly outages, sustaining prime-rated orders, while Vietnam’s FDI corridors import gensets to bridge a 4-GW grid deficit. Australia and New Zealand’s remote mines round out demand for rugged 1-5 MW packages, often containerized for desert conditions.

Competitive Landscape

Asia-Pacific Diesel Generator Market is semi-consolidated. Cummins’ India super-hub focuses on Stage IV engines and IoT services to cut lifecycle cost. Generac entered via a 2024 Singapore rental pact that supplies 100-500 kVA fleets for events and short-term construction, eroding smaller local lessors’ share.

Mahindra Powerol’s 2024 Stage IV range and Kirloskar’s new Pune plant show regional firms closing the technology gap. Weichai surpassed 100,000 National VI engines by 2024, granting domestic Chinese brands early-mover credibility. Hybrid-ready controllers and digital twins have become table stakes; laggards lacking R&D breadth risk margin compression as compliance costs climb.

Asia-Pacific Diesel Generator Industry Leaders

Cummins Inc

Mitsubishi Heavy Industries Engine & Turbocharger

Yanmar Holdings co. Ltd

Caterpillar Inc

Mahindra Powerol Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: March 2026: Generac Holdings, Inc. announced the launch of its SD1250 and SD1500 diesel generators, designed to provide reliable and efficient power for high-demand applications. These generators, powered by the Perkins 5012 46-liter engine, address a key need in the industrial market by offering enhanced fuel efficiency, lower emissions, and a compact design.

- September 2025: Valvoline Cummins India launched the country’s first full-synthetic CK4 oil for next-generation commercial diesel engines. Offering enhanced wear protection and compatibility with BSVI systems, it supports longer generator-engine life cycles across Asia-Pacific, improving operational reliability in challenging climates.

- September 2025: NRL Recycling acquired Tycod Autotech for INR 240 million, entering precision auto-component manufacturing. While not generator-specific, this development strengthens Asia-Pacific supply chains for diesel-generator engine parts and supports future localized production ecosystems.

- September 2025: Cummins and Komatsu signed an MOU to co‑develop hybrid powertrains for heavy mining haul trucks, integrating Wabtec drive systems. Although mining‑focused, the initiative signals future diesel‑hybrid advancements that may influence Asia‑Pacific generator markets through improved fuel efficiency, lower emissions, and decarbonization technologies.

Asia-Pacific Diesel Generator Market Report Scope

The diesel generator market encompasses the global industry engaged in the production, distribution, installation, and maintenance of diesel-powered generator sets (gensets) designed to generate electricity for backup, standby, prime, or continuous power purposes.

The Asia-Pacific Diesel Generator Market report is segmented by capacity, end-user, and application. By capacity, the market is segmented into below 75 kVA, 75 to 350 kVA, 375 to 750 kVA, 750 kVA to 2,000 kVA, and above 2,000 kVA. By application, the market is segmented by standby/backup power, prime/continuous power, and peak-shaving/load management. By end-user, the market is segmented into residential, commercial, and industrial. The report also covers the market size and forecasts for the Asia-Pacific Diesel Generator Market across the major regions or countries (China, India, Japan, South Korea, ASEAN Countries, Australia and New Zealand, and the rest of Asia-Pacific). The report offers the market size and forecasts in revenue (USD billion) for all the above segments.

By Capacity (kVA)

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Stand-by/Backup Power |

| Prime/Continuous Power |

| Peak-shaving/Load Management |

By End User

| Residential |

| Commercial |

| Industrial |

By Geography

| China |

| India |

| Japan |

| South Korea |

| ASEAN Countries |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Capacity (kVA) | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Stand-by/Backup Power |

| Prime/Continuous Power | |

| Peak-shaving/Load Management | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific diesel generator market by 2031?

The market is forecast to reach USD 19.19 billion by 2031, expanding at a 7.29% CAGR during 2026-2031.

Which capacity range holds the largest share today?

Sets rated 375-750 kVA led with 45.1% of regional revenue in 2025 thanks to telecom towers and mid-rise commercial buildings.

Why are data centers important for future diesel-genset demand?

Hyperscale data halls need N+1 redundancy, so every megawatt of IT load demands roughly 1.2-1.5 MW of diesel backup capacity.

Which country will grow fastest through 2031?

India is expected to post the quickest 8.5% CAGR as PLI-fueled manufacturing corridors outpace grid reinforcement.

How are stricter emission norms affecting genset buyers?

Stage IV and National VI rules add 15-20% to capex, pushing owners toward newer, more efficient engines or hybrid micro-grids that reduce runtime.

Page last updated on: