Asbestos Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

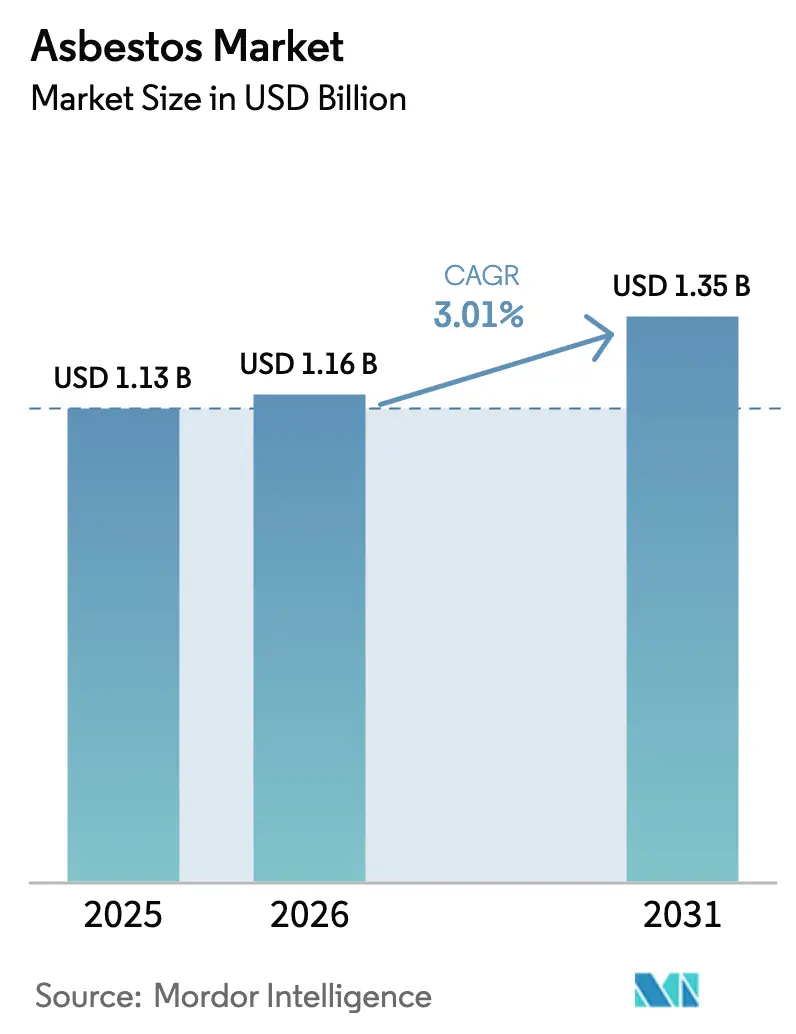

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asbestos Market Analysis by Mordor Intelligence

The asbestos market size is expected to grow from USD 1.13 billion in 2025 to USD 1.16 billion in 2026 and is forecast to reach USD 1.35 billion by 2031 at 3.01% CAGR over 2026-2031. Cost competitiveness in cement sheets and pipes, infrastructure booms in emerging economies, and weak regulatory enforcement continue to counterbalance escalating health concerns and outright bans. Asia-Pacific anchors demand through low-cost housing projects, while Russia, Kazakhstan, Brazil, and China keep global supply concentrated. Regulatory arbitrage shapes trade flows as producers target jurisdictions with permissive rules. Simultaneously, litigation expenses and the rapid commercialization of safer substitutes pressure margins and accelerate technology migrations.

Key Report Takeaways

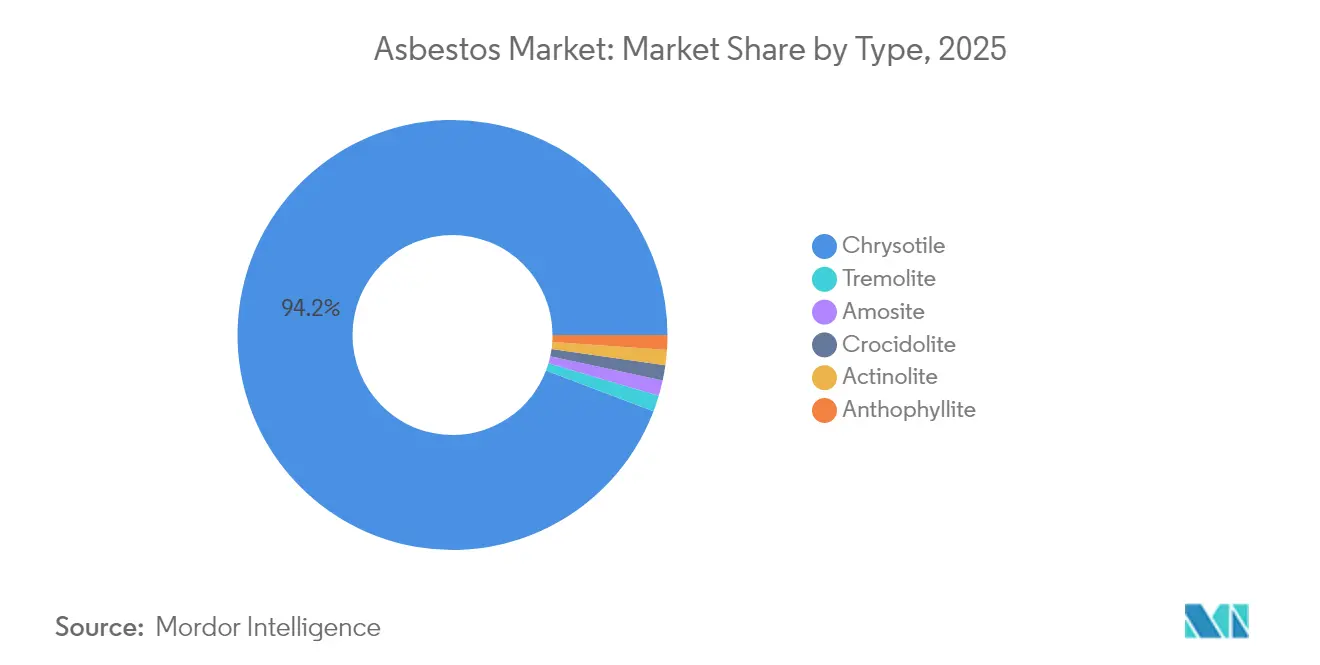

- By type, chrysotile held 94.23% of asbestos market share in 2025, yet tremolite recorded the highest forecast CAGR at 3.16% through 2031.

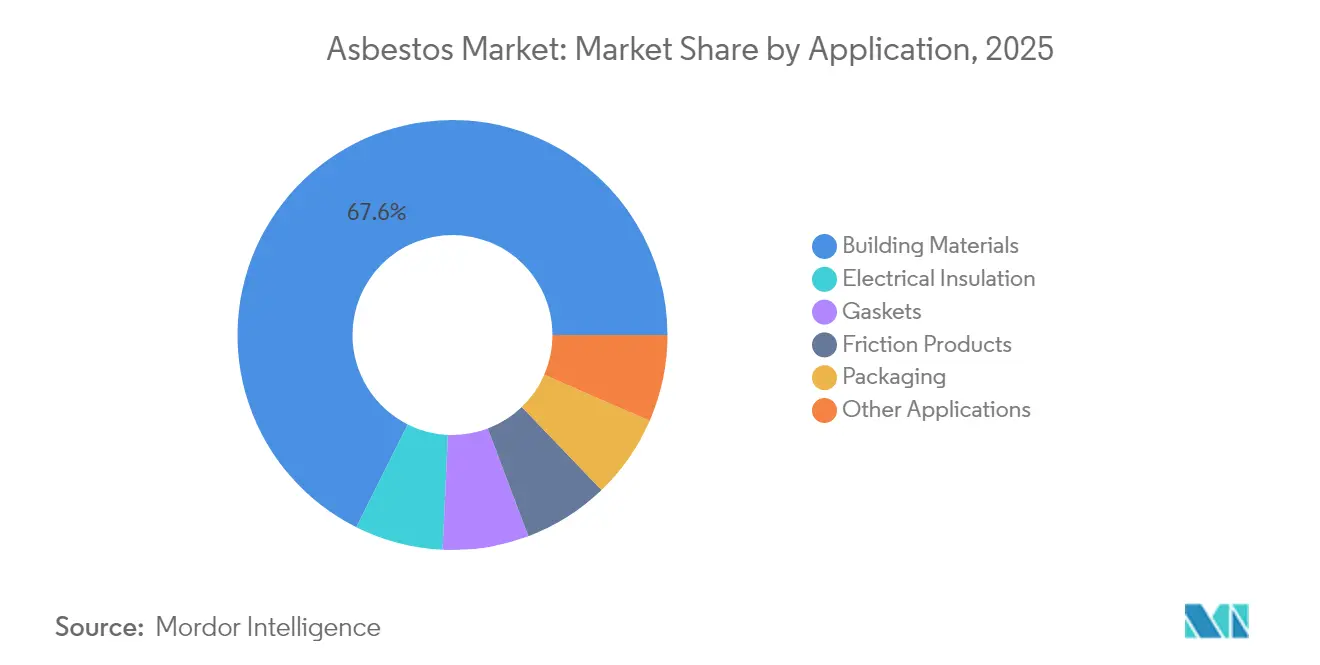

- By application, building materials accounted for 67.62% share of the asbestos market size in 2025, while electrical insulation is advancing at a 3.26% CAGR through 2031.

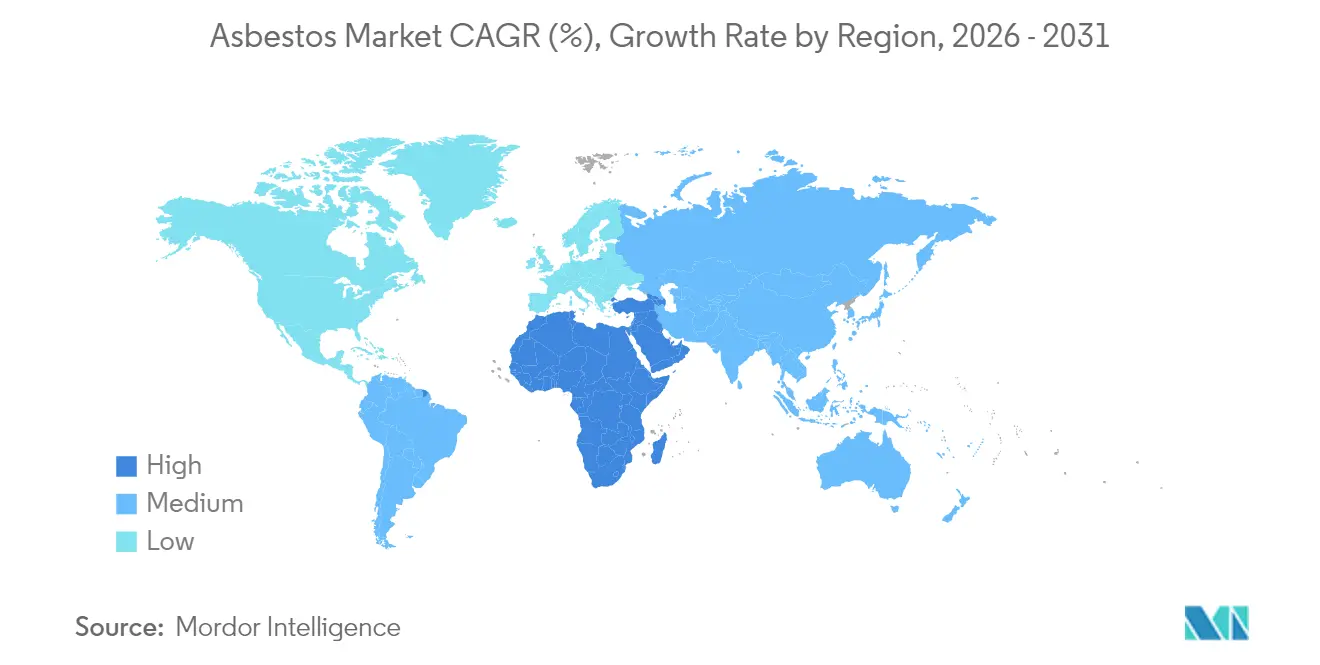

- By geography, Asia-Pacific commanded 70.62% revenue in 2025; the Middle East and Africa region is projected to expand at a 3.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asbestos Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Infrastructure Growth in APAC and Africa Sustaining Low-Cost Asbestos Cement Demand | +1.2% | APAC core, spill-over to Africa | Medium term (2-4 years) |

| Rising Retrofit and Repair Activity in Legacy Asbestos-Built Stock (Roofing, Pipes) | +0.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Cost Advantage of Chrysotile Over Synthetic Substitutes for Chlor-Alkali Diaphragms | +0.6% | Global industrial centers | Short term (≤ 2 years) |

| Weak Enforcement of Asbestos Bans in High-Growth Emerging Economies | +0.9% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Niche Demand from Specialised Gaskets in Chemical and Oil Processing | +0.4% | Global industrial hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid infrastructure growth in APAC and Africa sustaining low-cost asbestos cement demand

Large-scale housing and transport programs across India, China, Nigeria, and Ethiopia continue to favor asbestos cement because of its price advantage and ready supply. India imported 361,164 tonnes in 2019-2020, mainly from Russia, to feed roof and pipe projects that dominate affordable housing. Chinese construction firms expanding into Ethiopia and Angola often specify asbestos cement sheets for rural schools and warehouses, reinforcing demand corridors that link Asian producers with African builders. Nigeria’s construction sector historically consumed more than 1 million tons across multiple projects, indicating an entrenched user base that still values the material’s durability. WHO warns that asbestos-related diseases cause 125,000 annual deaths worldwide, yet governments prioritizing cost control continue to approve imports. This infrastructure-led demand underpins the asbestos market even as global bans intensify.

Rising retrofit and repair activity in legacy asbestos-built stock

Millions of roofs, water mains, and wallboards installed before bans now require upkeep, prompting steady demand for encapsulation coatings, removal services, and replacement panels. Specialized contractors invest in negative-pressure enclosures, HEPA filtration, and certified disposal, which pushes startup costs to USD 150,000 and beyond according to industry surveys. The United States consumed 110 tons of chrysotile from stockpiles in 2024, entirely for maintenance in chlor-alkali plants that still rely on asbestos diaphragms. Latvia’s 2024 pilot removal scheme exhausted its budget months early, underscoring the latent workload in older housing stock. These retrofit activities extend the asbestos market life cycle while fostering the parallel growth of alternative materials that can slot into existing fittings without design changes.

Cost advantage of chrysotile over synthetic substitutes for chlor-alkali diaphragms

For decades, asbestos diaphragms delivered reliable performance at lower operating voltages in brine electrolysis units. European Commission reviews between 1975 and 2004 confirmed no technically equivalent replacement in legacy cells, keeping three plants in Germany and Poland reliant on roughly 300 tons of chrysotile[1]European Commission, “Review of Chrysotile Derogations,” europa.eu . That cost gap is narrowing as membrane suppliers such as De Nora commercialize polymer solutions that reduce energy use and cut hazardous waste. The United States EPA nonetheless issued a 2024 rule that phases out chrysotile, compelling gradual plant conversions by 2037 and signaling to emerging markets that the economics of status-quo technology are deteriorating. Until full compliance takes effect, price-sensitive operators in Asia, Africa, and Latin America continue to purchase chrysotile fiber, sustaining a niche but profitable flow for miners.

Weak enforcement of asbestos bans in high-growth emerging economies

India banned mining in 1993, yet it remains the world’s largest asbestos importer and hosts an industry valued at USD 2 billion that employs about 300,000 people across more than 100 factories. Nigeria reports no official asbestos mortality statistics, reflecting data gaps that impede policy enforcement. Public awareness is low; surveys in Indian industrial corridors show residents seldom recognize asbestos as carcinogenic despite widespread exposure. Such regulatory vacuums allow low-priced sheets and pipes to remain the default choice in rural construction, keeping the asbestos market entrenched even as global opinion shifts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of National Bans (E.G., EPA 2024 US Chrysotile Phase-Out) | -1.8% | Global, led by developed markets | Short term (≤ 2 years) |

| Escalating Litigation and Insurance Costs for Producers and Downstream Users | -1.1% | North America and EU, spreading globally | Medium term (2-4 years) |

| Rapid Commercialisation of Non-Asbestos Fibre-Cement and Brake Friction Materials | -0.7% | Global, faster adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acceleration of national bans (e.g., EPA 2024 US chrysotile phase-out)

The United States outlawed chrysotile imports in March 2024 and set phased conversion deadlines that extend through 2037 for specialty uses. Mexico’s Congress advanced a blanket prohibition in January 2024, widening the no-use zone across North America. More than 60 countries now enforce full bans, and multilateral bodies such as WHO continue to promote substitution initiatives. The chlor-alkali sector alone faces USD 2.8 billion to USD 3.4 billion in conversion costs under the updated rule set. As each major economy implements restrictions, suppliers lose market access, compressing global consumption and redirecting fiber toward fewer permissive destinations.

Escalating litigation and insurance costs for producers and downstream users

Insurance carriers paid out USD 1.8 billion in asbestos claims in 2022, a 9% jump that strains reserves and raises premiums for manufacturers and contractors. Global corporate liabilities reached USD 73 billion, prompting restructurings such as Berkshire Hathaway affiliates filing for Chapter 11 protection in early 2025. 3M booked USD 523 million to cover respirator-linked claims, illustrating how peripheral players also shoulder substantial exposure. Social inflation trends in the United States added 7 percentage points to liability growth during 2023, amplifying settlement values and jury awards. These financial burdens push firms to exit asbestos segments, accelerate substitution research, or off-load portfolios to specialist legacy-management vehicles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chrysotile dominance faces regulatory pressure

Chrysotile captured 94.23% of asbestos market share in 2025 because builders, automakers, and chlor-alkali operators favor its flexible fibers and relative availability. Russia accounted for 48% of global mine output in 2025, followed by Kazakhstan, Brazil, and China, yet sanctions and logistics issues trimmed Russian exports from 65% to 48% since 2020. Tremolite exhibited a 3.16% CAGR through 2031, the fastest within the asbestos market, due to specialized metallurgical and heat-shield applications where substitutes remain costly. EPA’s 2024 ban removed chrysotile access to the lucrative United States, signaling that amphibole types could inherit a residual share only in jurisdictions without bans. As more countries align with WHO recommendations, type demand will splinter into narrow geographic niches, making supply more volatile.

Many producers already segment inventory by destination. Russian mines channel premium chrysotile grades to India and China, whereas mid-grade fiber moves to Africa and Latin America where construction standards are lower. In contrast, amphibole demand is now almost entirely research-driven, with universities and material science firms ordering micro quantities for controlled experiments in filtration and high-temperature ceramics. Such shifts illustrate a bifurcated asbestos market that simultaneously contracts in volume yet persists in high-precision pockets.

By Application: Building materials leadership under siege

Buiding materials represented 67.62% of 2025 consumption because of their affordability in low-income housing. India alone erected more than 100,000 rural dwellings with asbestos cement roofs during the last fiscal year, underpinning the building materials share. Electrical insulation posted a 3.26% CAGR to 2031, reflecting demand in heavy-duty transformers and furnace cables where thermal shock resistance and dielectric strength trump health concerns. Friction products such as brake pads declined in North America and Europe but stayed stable in Africa and parts of Asia where vehicle safety regulations are less stringent. Packaging, once a sizable niche, dwindled as food and pharma rules tightened.

Alternative fiber-cement boards now outprice asbestos panels by only USD 0.15 per square meter in some Southeast Asian markets, eroding the legacy cost advantage. The EPA-mandated shift to membrane cells in chlor-alkali facilities will also dent diaphragm fiber orders. Gasket makers increasingly adopt compressed non-asbestos sheets, citing better sealability and reduced fugitive emissions. Consequently, the asbestos market is losing its largest application pillars even as smaller industrial niches persist.

Geography Analysis

Asia-Pacific generated 70.62% of asbestos market revenue in 2025, led by India’s position as the world’s top importer at 44% of global volume. The region employed about 300,000 workers across more than 100 plants, creating economic inertia that resists health-based reforms. China remained both a major consumer and producer, and public health projections forecast 15,000 annual asbestos disease deaths by 2035, underscoring the social costs of continued use. Indonesia, Vietnam, and the Philippines also retain permissive rules, funneling fiber from Russian and Kazakhstan mines into roofing and piping lines. These factors cement Asia-Pacific’s dominance in the asbestos market even as international advocacy builds against it.

North America underwent structural change after the United States banned chrysotile in 2024. Domestic consumption fell to 110 tons sourced entirely from legacy stockpiles, and chlor-alkali plants must complete membrane conversions by 2037. Canada, once a significant producer, now exports almost all mined asbestos to Asia but faces external pressure to shutter operations. Mexico’s draft ban would seal off the final regional outlet, consolidating a continental moratorium that influences global trade lanes. Litigation remains the region’s defining legacy burden, with billions in outstanding claims that squeeze balance sheets across the construction, industrial gas, and consumer goods sectors.

Europe maintains a zero-tolerance policy on new asbestos use, having implemented bans across member states in the 1990s. Legacy remediation now dominates activity, including the removal of insulating boards from schools and public buildings. The European Commission still grants narrow derogations for low-voltage chlor-alkali cells where safe dismantling is technically complex, but those exceptions are shrinking. National programs such as Latvia’s 2024 pilot demonstrate that remediation demand often outstrips fiscal capacity, suggesting a long tail of asbestos service activity. These experiences feed innovation in alternative fiber-cement boards and membrane technologies that exporting firms now sell to Asia, Africa, and Latin America.

Competitive Landscape

The asbestos market is moderately consolidated around a handful of miners. Russia’s PJSC Uralasbest produced 21% of global chrysotile and supplied 41% of Russian output in 2025, exporting roughly 80% of its grade 4-6 fiber[2]Uralasbest, “Company Fact Sheet,” uralasbest.ru . Kostanay Minerals JSC in Kazakhstan lifted its market presence to 26% of global exports after capital upgrades improved ore recovery. SAMA Mineração de Amianto Ltda. in Brazil owns the world’s largest active open-pit asbestos mine and accounted for 15% of world supply, with 90% shipped to Asia and MEA. Ningbo Xinyan Friction Materials Co., Ltd. illustrates downstream integration, balancing asbestos and non-asbestos product lines to hedge regulatory risk and exporting 80-90% of output to 30 countries.

Competitive strategy emphasizes cost leadership and market proximity. Russian and Kazakh firms market FOB prices 15-20% below Brazilian fiber because of shorter shipping routes to India, consolidating share despite sanctions. Producers invest in beneficiation to deliver higher tensile strength fibers for specialized gaskets, preserving margins in contracting volumes. At the same time, leading players are launching legacy management funds or purchasing liability insurance to reassure lenders and customers. Velan Inc., for example, retired its asbestos liabilities before accepting a takeover bid, signaling that clean balance sheets are a prerequisite for corporate transactions in this space. The competitive gap widens between miners that pivot toward substitute technology partnerships and those that remain locked in commodity extraction.

Asbestos Industry Leaders

PJSC Uralasbest

JSC Orenburg Minerals

Kostanay Minerals JSC

SAMA Mineração de Amianto Ltda.

BHARAT ASBESTOS & RUBBER CO.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: EPA finalized a ban on the import, processing, manufacture, distribution, and use of chrysotile asbestos under TSCA—targeting chlor-alkali diaphragm use, consumer friction products, gaskets, brake blocks, and more.

- May 2022: Visaka Industries Ltd announced the expansion of its Asbestos Cement division (ACD) at the Raebareli unit in Uttar Pradesh. The company commissioned a new production line with a capacity of 1.00 lakh MTPA for commercial production.

Global Asbestos Market Report Scope

Asbestos is a naturally occurring fibrous silicate mineral that is differentiated into six different types, each of which is composed of long and thin fibrous crystals. The asbestos market is segmented by type, application, and geography (Asia-Pacific, North America, Europe, South America, the Middle East, and Africa). By type, the market is segmented into chrysotile, amosite, crocidolite, anthophyllite, tremolite, and actinolite. By application, the market is segmented into building materials, electrical insulation, friction products, packaging, gaskets, and other applications. The report also covers market sizes and forecasts in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Chrysotile |

| Amosite |

| Crocidolite |

| Tremolite |

| Actinolite |

| Anthophyllite |

| Building Materials |

| Electrical Insulation |

| Friction Products |

| Packaging |

| Gaskets |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Chrysotile | |

| Amosite | ||

| Crocidolite | ||

| Tremolite | ||

| Actinolite | ||

| Anthophyllite | ||

| By Application | Building Materials | |

| Electrical Insulation | ||

| Friction Products | ||

| Packaging | ||

| Gaskets | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the asbestos market?

The asbestos market size reached USD 1.16 billion in 2026 and is forecast to grow to USD 1.35 billion by 2031.

Which region dominates global demand?

Asia-Pacific controls 70.62% of demand, fueled by India’s position as the top importer and ongoing infrastructure expansion.

Which asbestos type is most prevalent?

Chrysotile accounts for 94.23% of global consumption, although its dominance is under regulatory pressure.

How will the U.S. EPA ban affect global trade?

The 2024 chrysotile ban removes a major market, forces chlor-alkali plants to convert by 2037, and redirects supply toward Asia, Africa, and Latin America.

What is driving demand growth despite health risks?

Cost advantages in cement products, weak enforcement in emerging markets, and limited substitutes in certain industrial applications sustain consumption.

Page last updated on: