Armored Vehicle Fire Suppression Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

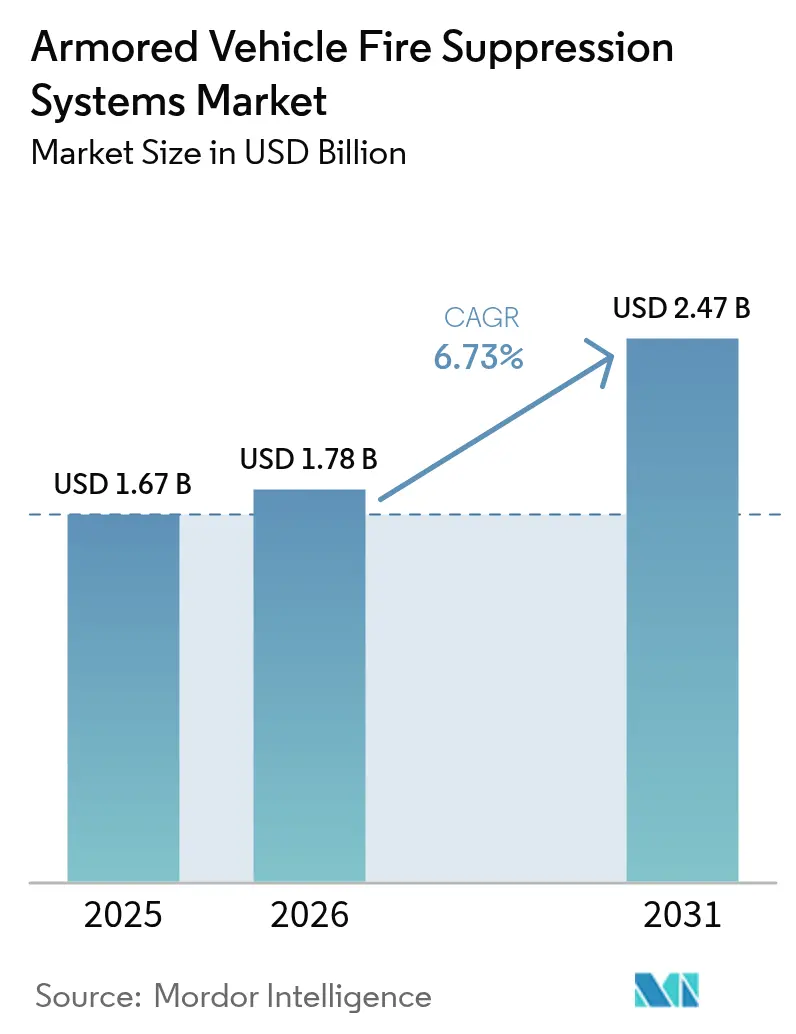

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Armored Vehicle Fire Suppression Systems Market Analysis by Mordor Intelligence

The armored vehicle fire suppression systems market size was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.78 billion in 2026 to reach USD 2.47 billion by 2031, at a CAGR of 6.73% during the forecast period (2026-2031). Rising defense modernization budgets, a global ban on Halon, and the push to replace PFAS-containing foams are expanding procurement pipelines across major vehicle upgrade and new-build programs.[1]Source: U.S. Government Accountability Office, “Defense Infrastructure: DOD Faces Challenges in Eliminating PFAS,” gao.gov Demand also benefits from sensor miniaturization that delivers sub-10-millisecond autonomous discharge, ensuring compliance with stringent MIL-STD-810H false-alarm requirements. Rapid electrification of combat platforms, exemplified by battery-powered infantry fighting vehicles under evaluation in Europe and South Korea, reshapes agent chemistry specifications and spurs innovation in predictive thermal management. North America anchors spending, but Asia-Pacific’s double-digit defense outlays make it the fastest-growing regional opportunity for suppliers able to deliver PFAS-free, AI-enabled solutions. Competitive dynamics center on integration know-how rather than price, with leading vendors coupling fire suppression with active protection suites to present unified survivability architectures.

Key Report Takeaways

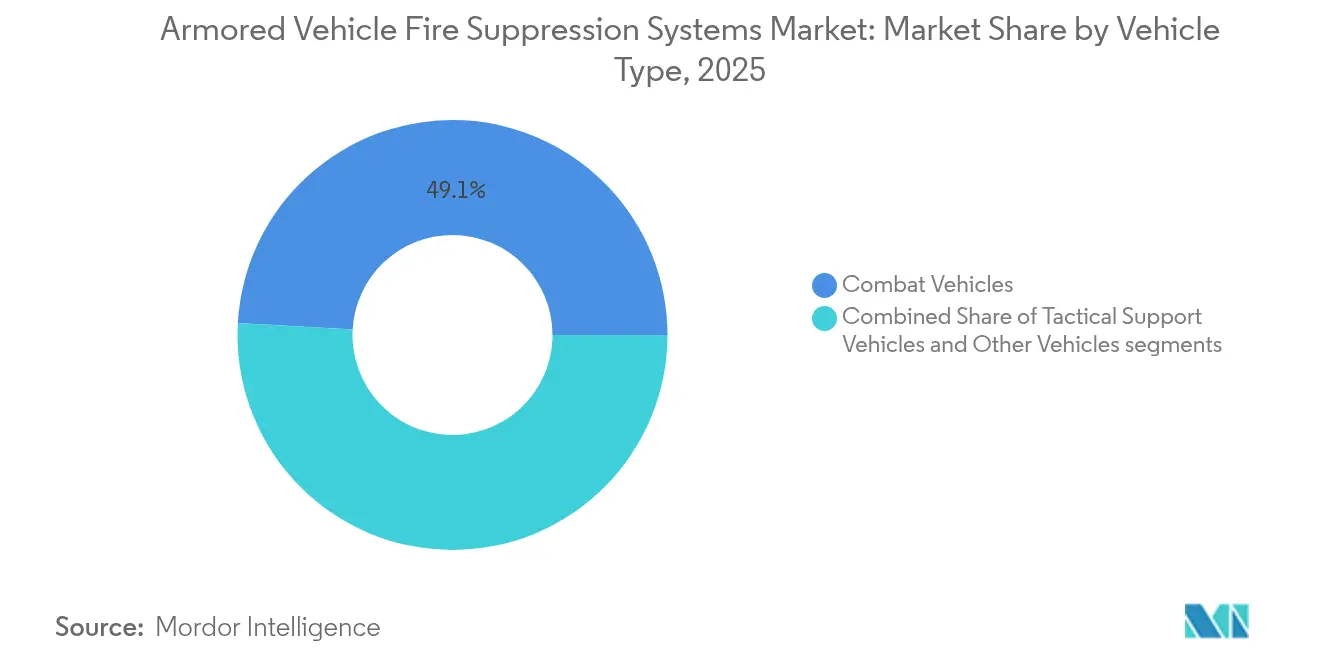

- By vehicle type, combat vehicles led with 49.12% revenue share in 2025, while tactical support vehicles are projected to post a 7.34% CAGR to 2031.

- By system type, automatic/autonomous solutions held 66.55% of the armored vehicle fire suppression systems market share in 2025; hybrid configurations are expected to expand at a 9.02% CAGR.

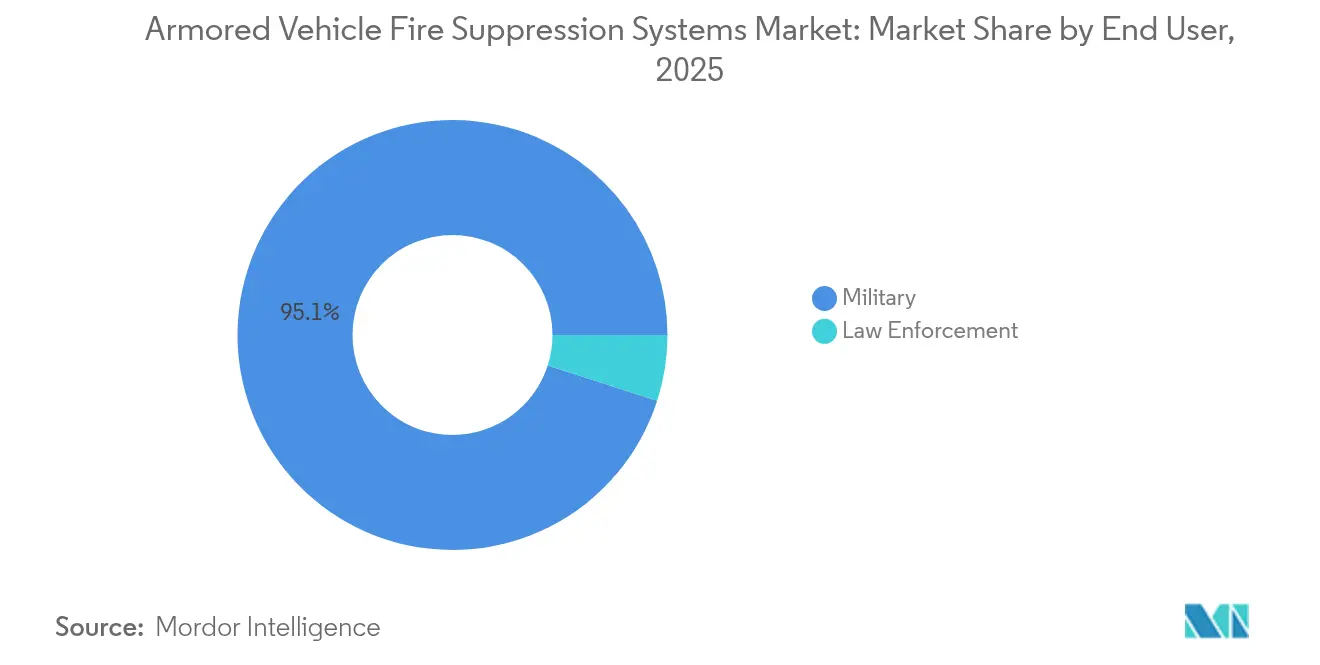

- By end user, military programs commanded 95.05% of demand in 2025, whereas law-enforcement fleets exhibit the highest 8.14% CAGR outlook through 2031.

- By component, cylinders and agents accounted for 39.22% of the armored vehicle fire suppression systems market size in 2025; detectors and sensors will rise fastest at a 7.51% CAGR.

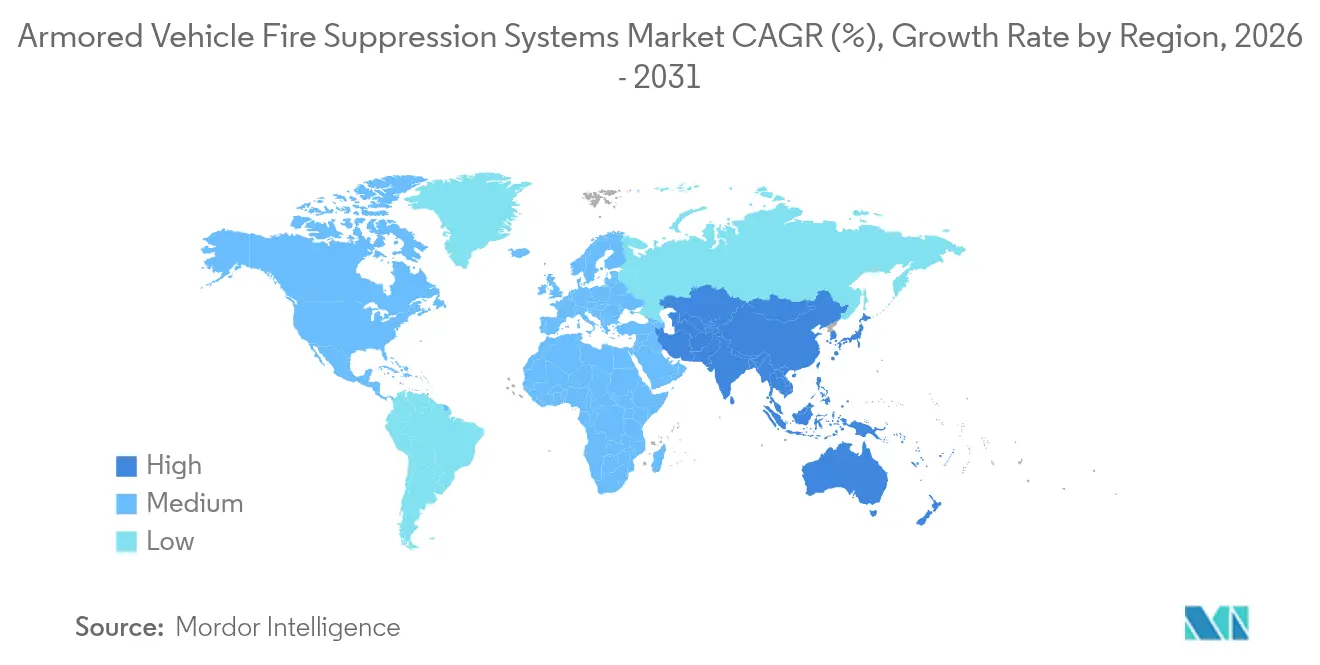

- By geography, North America contributed 47.25% of 2025 revenue, but Asia-Pacific is poised to grow at an 8.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Armored Vehicle Fire Suppression Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift-to-electric combat platforms | +1.2% | Global (early adoption NA and EU) | Medium term (2-4 years) |

| Stricter MIL-STD-810H safety mandates | +0.9% | North America and NATO allies | Short term (≤ 2 years) |

| Lightweight non-Halon agents | +0.8% | Global | Medium term (2-4 years) |

| Auto-detect AI sensor fusion | +1.1% | North America and EU | Long term (≥ 4 years) |

| Active protection system (APS) integration | +0.7% | Europe and APAC | Long term (≥ 4 years) |

| Increased global defense spending and modernization programs | +1.4% | Global, with highest impact in Europe, APAC, and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift-to-Electric Combat Platforms

Lithium-ion propulsion elevates fire-load density in armored hulls, creating thermal runaway scenarios that reach 400°C and defeat legacy Halon-based solutions. Platforms under Germany’s KF41 Lynx and South Korea’s Redback-K programs specify suppression agents that remain effective inside sealed battery casings while coordinating with 80 kW cooling packs derived from RTX’s fighter-jet thermal systems. Chinese GB 38031-2020 mandates a 5-minute propagation delay, signaling that the benchmark military fleets will emulate. To comply, OEMs layer Kapton-based insulation, predictive cell-isolation algorithms, and distributed nozzle arrays that flood battery bays before cascading failure begins.[2]Source: DuPont, “The Biggest Threat to Electric Vehicles and the Materials Solution,” dupont.com

Stricter MIL-STD-810H Safety Mandates

The newest MIL-STD-810H tests require suppression hardware to endure −54°C arctic deployments, 71°C desert heat, and heavy-caliber shock while sustaining electromagnetic compatibility with vehicle radios. Contractors answer with dual-spectrum optical sensors that combine mid-wave IR and UV bands, trimming false activations below 0.1% and cutting crew workload. Compliance demands extensive lab cycles that lengthen development by 120 days, tipping the advantage to firms with in-house chambers. Algorithms trained on field telemetry now distinguish solar glint from true ignition, enabling machines to suppress fires even when vision blocks are obscured by dust or smoke.

Lightweight Non-Halon Agents (FK-5-1-12)

Novec 1230 offers zero ozone depletion and a 0.014 global warming potential, allowing total flooding in occupied spaces without toxic by-products. Flow-field studies show that the agent discharges evenly through narrow crew-compartment manifolds, eliminating the risk of cold-spot reignition. Militaries demand extinguishment within 30 seconds at minimal volume, a criterion the agent meets while trimming bottle mass to offset additional APS radars. Higher cost prompts buyers to favor multiyear contracts that secure price breaks and guarantee batch consistency.

Auto-Detect AI Sensor Fusion

AI-enabled arrays merge IR, thermal, and acoustic signatures to flag ignition within 10 milliseconds and classify event type with 99.7% confidence. Northrop Grumman’s ATHENA pod, selected for the US Army’s improved threat-detection kit, delivers 360° coverage while filtering clutter from APS radar sweeps.[3]Source: Joint Forces, “ATHENA Selected by US Army,” joint-forces.com Machine-learning models retrain on board, driving down false alarms over service life and letting crews focus on maneuver instead of manual firefighting drills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks for PFAS-free agents | -0.6% | Global (NA and EU acute) | Short term (≤ 2 years) |

| High retrofit cost for legacy fleets | -0.4% | Global | Medium term (2-4 years) |

| Weight-penalty vs. active armor trade-off | -0.3% | Europe and APAC | Long term (≥ 4 years) |

| IP ownership concentration | -0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks for PFAS-Free Agents

Only three fluorine-free foams meet US Defense Department standards, yet 2 million gallons must be fielded before October 2025, forcing the Pentagon to seek a one-year extension. Validation of each new batch stretches 120 days, leaving tactical vehicle rollouts waiting on lab queues. European forces face identical hurdles, risking divergent agent usage that undermines NATO logistic commonality.

High Retrofit Cost for Legacy Fleets

Switching from Halon to FK-5-1-12 can exceed 20% of a vehicle’s original procurement cost because piping diameters, storage pressures, and detection wiring all change. US DEVCOM trials of potassium bicarbonate alternatives illustrate the complexity of validating new flow dynamics inside steel hulls originally optimized for gaseous Halon. Nations with constrained budgets often delay upgrades, widening survivability gaps between modernized and legacy platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Combat Platforms Drive Market Leadership

The armored vehicle fire suppression systems market size for combat vehicles amounted to nearly half of global revenue at 49.12% in 2025. Large-scale programs such as Italy’s EUR 16 billion (USD 18.87 billion) Armoured Combat System and Germany’s Leopard 2A8 procurement embed fully automatic, dual-zone extinguishers that simultaneously protect crew and engine bays. Spain, Romania, and Latvia have followed with tracked IFV buys that specify Novec-based flooding agents compatible with NATO standards.

Tactical support vehicles furnish the fastest 7.34% CAGR, mirroring doctrine shifts in Ukraine that expose logistics convoys to direct fire. The US Army’s M1E3 Abrams program emphasizes common survivability kits for tank-retrieval and ammunition-resupply variants, ensuring part interchangeability and easing training demands. Specialized recovery rigs and bridge layers also maintain demand, albeit at modest volumes, because their hydraulic equipment creates distinct ignition sources that require bespoke nozzle positioning.

By System Type: Automation Dominance with Hybrid Growth

Automatic and autonomous installations captured 66.55% of 2025 revenue, reflecting doctrinal reliance on sub-150-millisecond discharge that safeguards crews when immediate manual action is impossible. These systems combine dual-spectrum optics with pressure-rise sensors to cross-validate events before releasing agent, trimming costly inadvertent discharges.

Manual designs persist in low-intensity roles or nations prioritizing initial acquisition price over lifecycle risk. Yet hybrid configurations, blending automatic default with crew override, deliver the highest 9.02% CAGR. Operators appreciate the option to halt suppression in fuel-fume scenarios where venting remedies the hazard, avoiding agent wastage and downtime.

By End User: Military Dominance with Law-Enforcement Growth

Military programs generated 95.05% of the 2025 demand as global defense spending hit USD 2.48 trillion. NBC hardening, electromagnetic shielding, and integration with battle-management networks put military specifications beyond typical civilian reach, locking in vendor specialization.

Law-enforcement agencies record an 8.14% CAGR, propelled by urban riot vehicles and border patrol armaments. Brazil’s procurement of Roshel Senator trucks, fitted with NATO-grade suppression, exemplifies the civil uptake of battlefield technologies and underscores the manufacturer’s ability to scale designs to non-military legal frameworks.

By Component: Agent Systems Lead with Sensor Innovation

Cylinders and agents represented 39.22% of component revenue because consumables require periodic replenishment, generating annuity-like sales. The armored vehicle fire suppression systems market sees FK-5-1-12 dominate Western inventories while soy-based foams gain pilot adoption as prices fall and capacity scales.

Detectors and sensors post the strongest 7.51% CAGR. The move to sensor fusion triples semiconductor content per vehicle and elevates cybersecurity requirements, driving contracts that bundle firmware support with hardware supply. Nozzles, valves, and plumbing also benefit from new corrosion-resistant alloys suited to salt-spray naval variants, but growth remains tied to overall vehicle build rates.

Geography Analysis

North America retained a 47.25% share in 2025, anchored by the US Department of Defense’s USD 2.1 billion PFAS-replacement initiative that directly funds agent production and retrofit kits. The FY 2025 defense budget of USD 920 billion holds spending steady, letting primes plan production lots five years out. Canada’s Arctic Mobility Enhancement program adds niche demand for low-temperature formulations able to flow at −40 °C in amphibious hulls. Mexico’s interoperability alignment with US standards further widens the continental installed base.

Europe accelerates procurement under NATO readiness goals, with 22 member states hiking defense budgets by at least 10% in real terms for 2025. Italy’s massive Lynx and Panther orders, Germany’s Leopard 2A8 buy, and Spain’s Leopard 2E overhaul all specify APS-linked suppression networks, establishing shared supply chains and stringent cyber-hardening baselines. Thales’ FMBTech consortium of 26 firms uses EU funding to coordinate valve geometry, sensor firmware, and agent logistics across borders, smoothing export licensing.

Asia-Pacific delivers the highest 8.07% CAGR. Japan’s record USD 59 billion 2025 defense budget finances Patria AMV XP local production featuring modular suppression that drops into Type 16 mobile gun and Type 96 APC hulls. China’s 2027 readiness goal pushes indigenous agent R&D to circumvent Western embargoes, while South Korea’s Redback-K embeds smart-bottle telemetry that alerts crews to pressure loss in real time. Southeast Asian modernization—from the Philippines’ USD 35 billion plan to Indonesia’s medium-tank acquisition—extends demand to tropical climates where high humidity influences agent longevity.

Competitive Landscape

Suppliers operate in a moderately fragmented arena where players like KIDDE-DEUGRA leverage RTX’s aerospace thermodynamics to offer cross-domain solutions, bundling common detection cores across ground, air, and naval fleets. Explospot Systems targets ammunition-cook-off risks with proprietary compound powder that suppresses blast overpressure alongside flame, addressing kinetic penetrator scenarios.

Technology differentiation outweighs price competition. Vendors winning large NATO or Indo-Pacific tenders typically prove seamless data-bus integration with APS radars and vehicle health management software, thus reducing cabling weight and installation hours. PFAS-free manufacturing competence emerged as a discriminator once Western agencies mandated fluorine-free agents, causing backlogs for firms still requiring recipes.

Patent filings gravitate toward predictive suppression, such as heat-sensitive conductors embedded within battery arrays that trigger isolation the instant resistance changes exceed preset thresholds. White-space exists in cloud-linked analytics that correlate vehicle telemetry with ambient weather, enabling fleet managers to schedule preventive maintenance when sensor drift indicates nozzle blockage or bottle pressure loss.

Armored Vehicle Fire Suppression Systems Industry Leaders

KIDDE-DEUGRA Brandschutzsysteme GmbH (RTX Corporation)

Firetrace International

Nero Industries Co.

Emerson Electric Co.

Marotta Controls, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The International Armored Group opened a BGN 20 million (USD 12.07 million) Bulgarian plant producing Guardian Xtreme MRAPs with NATO-standard suppression suites.

- May 2024: During the DSA 2024 Exhibition in Malaysia, FNSS displayed its latest innovation, the PARS III 6x6 vehicle. This vehicle highlights the TEBER-II 30/40 Remote-Controlled Turret (RCT) and the SANCAK 30 mm Remote-controlled Turret. Notably, the PARS III 6x6 comes with standard automatic fire suppression systems.

Global Armored Vehicle Fire Suppression Systems Market Report Scope

Armored vehicle fire suppression systems are installed onboard military vehicles to control the eruption and spread of fire caused by a variety of factors, including hostile weapon fire, engine malfunction, etc. These systems are designed to suppress the spread of fire before it can damage critical systems while also protecting the passenger cabin from external fire.

The armored vehicle fire suppression systems market is segmented by vehicle type and geography. By vehicle type, the market is segmented into combat vehicles, troop transport vehicles, and other vehicle types. Other vehicles include armored cars and trucks. The report also covers the market sizes and forecasts for the armored vehicle fire suppression systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Combat Vehicles | Main Battle Tanks (MBTs) |

| Infantry Fighting Vehicles (IFVs) | |

| Armored Personnel Carriers (APCs) | |

| Tactical Support Vehicles | |

| Other Vehicles |

| Automatic/Autonomous |

| Manual |

| Hybrid |

| Military |

| Law Enforcement |

| Detectors and Sensors |

| Control Units and Panels |

| Cylinders and Agents |

| Nozzles, Valves, and Plumbing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Vehicle Type | Combat Vehicles | Main Battle Tanks (MBTs) | |

| Infantry Fighting Vehicles (IFVs) | |||

| Armored Personnel Carriers (APCs) | |||

| Tactical Support Vehicles | |||

| Other Vehicles | |||

| By System Type | Automatic/Autonomous | ||

| Manual | |||

| Hybrid | |||

| By End User | Military | ||

| Law Enforcement | |||

| By Component | Detectors and Sensors | ||

| Control Units and Panels | |||

| Cylinders and Agents | |||

| Nozzles, Valves, and Plumbing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the armored vehicle fire suppression systems market?

The market is valued at USD 1.78 billion in 2026 and is projected to grow to USD 2.47 billion by 2031, advancing at a 6.73% CAGR. .

Which segment holds the largest armored vehicle fire suppression systems market share?

Combat vehicles account for 49.12% of revenue, making them the dominant vehicle segment.

Why are PFAS-free agents important for future procurements?

Western militaries must eliminate PFAS foams by October 2026, so compliant agents unlock new contracts and avoid environmental liabilities.

Which region is expanding fastest?

Asia-Pacific leads with an 8.07% CAGR, fueled by Japan’s and China’s modernization budgets.

How quickly must modern automatic systems respond to a fire?

State-of-the-art autonomous units detect and discharge within 120-150 milliseconds, meeting NATO survivability benchmarks.

What technological trend could redefine the market in the long term?

Integration of AI-based predictive suppression with active protection systems promises to prevent ignition before flames emerge, creating a proactive survivability layer.

Page last updated on: