Argentina Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

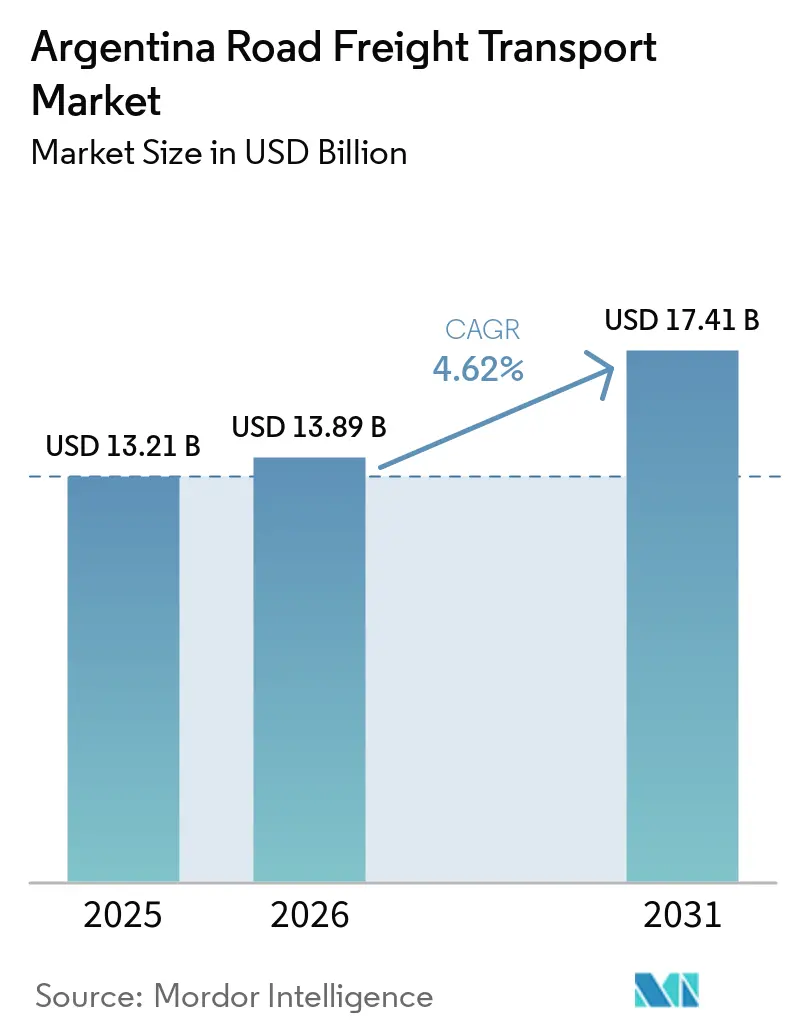

| Base Year Market Size (2025) | USD 13.21 Billion |

| Market Size (2026) | USD 13.89 Billion |

| Market Size (2031) | USD 17.41 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Road Freight Transport Market Analysis by Mordor Intelligence

The Argentina road freight transport market size was valued at USD 13.21 billion in 2025 and is estimated to grow from USD 13.89 billion in 2026 to reach USD 17.41 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

The moderate expansion pace reflects how infrastructure upgrades, cold-chain investments, and customs digitalization jointly reshape freight flows while creating divergent outcomes for small operators versus large fleets. Capacity additions under the federal Plan Vial 2030 are already trimming average transit times on key trunk routes, improving asset utilization for carriers that run modern equipment. Digital freight-matching platforms, now widespread in urban corridors, help small and medium enterprises (SMEs) cut empty kilometers and win loads that were once accessible only through brokers. At the same time, provincial weight-limit enforcement, foreign-exchange (FX) volatility, and an aging driver pool continue to raise operating costs, leaving margin pressure acute in commodity bulk lanes that cannot easily absorb surcharges.

Key Report Takeaways

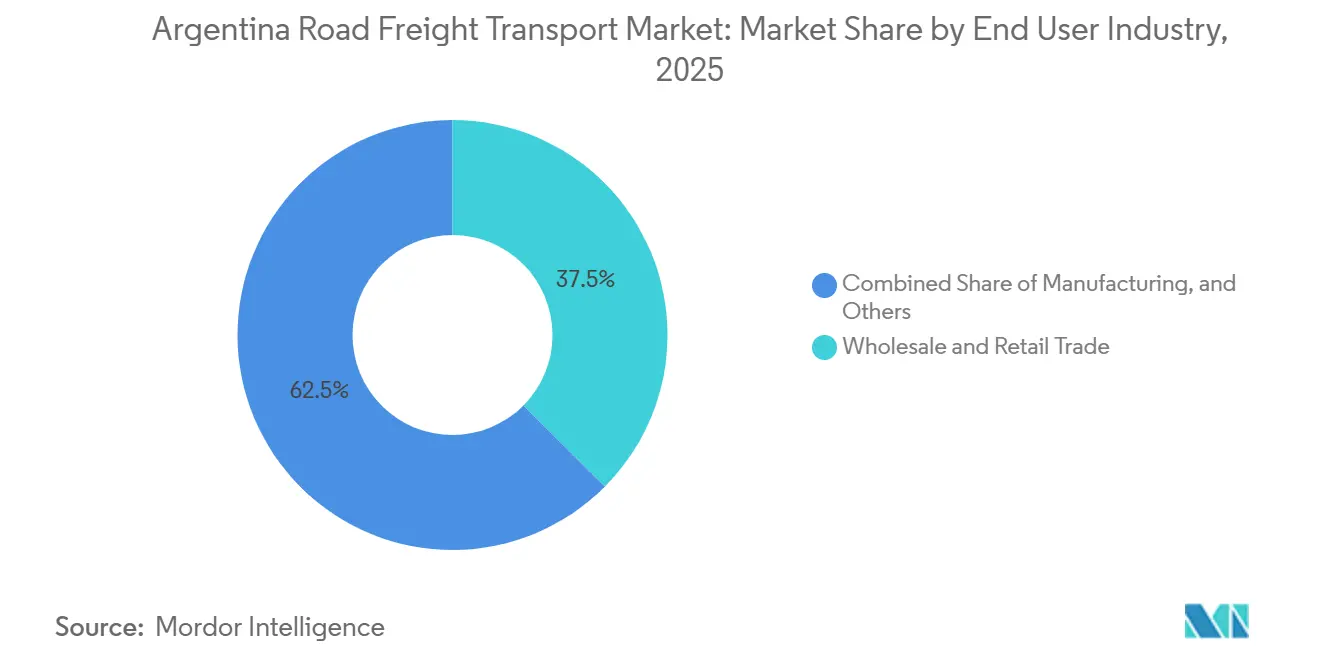

- By end-user industry, wholesale and retail trade led with 37.46% of the Argentina road freight transport market share in 2025, while manufacturing is projected to expand at a 6.11% CAGR through 2031.

- By destination, domestic haulage held 62.89% of the Argentina road freight transport market size in 2025 and international movements are advancing at a 5.45% CAGR to 2031.

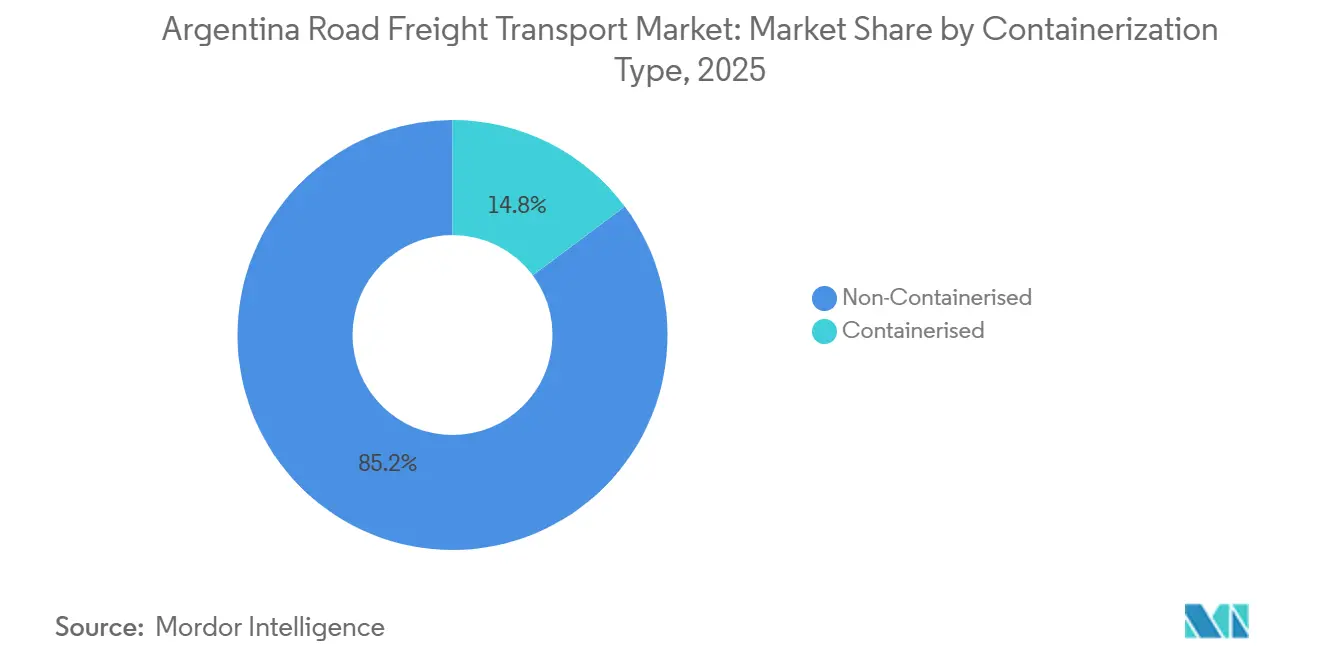

- By containerization, non-containerized freight accounted for 85.20% of the Argentina road freight transport market size in 2025, yet containerized volumes are forecast to grow at a 6.80% CAGR through 2031.

- By temperature control, non-temperature-controlled represented 94.33% of the Argentina road freight transport market size in 2025, meanwhile temperature-controlled is accelerating at an 8.83% CAGR.

- By truckload specification, full truckload captured 78.08% of 2025 revenue; less-than-truckload services are expanding at a 6.69% CAGR on the back of digital load-consolidation tools.

- By distance, long haul accounted for 70.91% of the Argentina road freight transport market size in 2025, meanwhile, short haul is accelerating at a 6.02% CAGR.

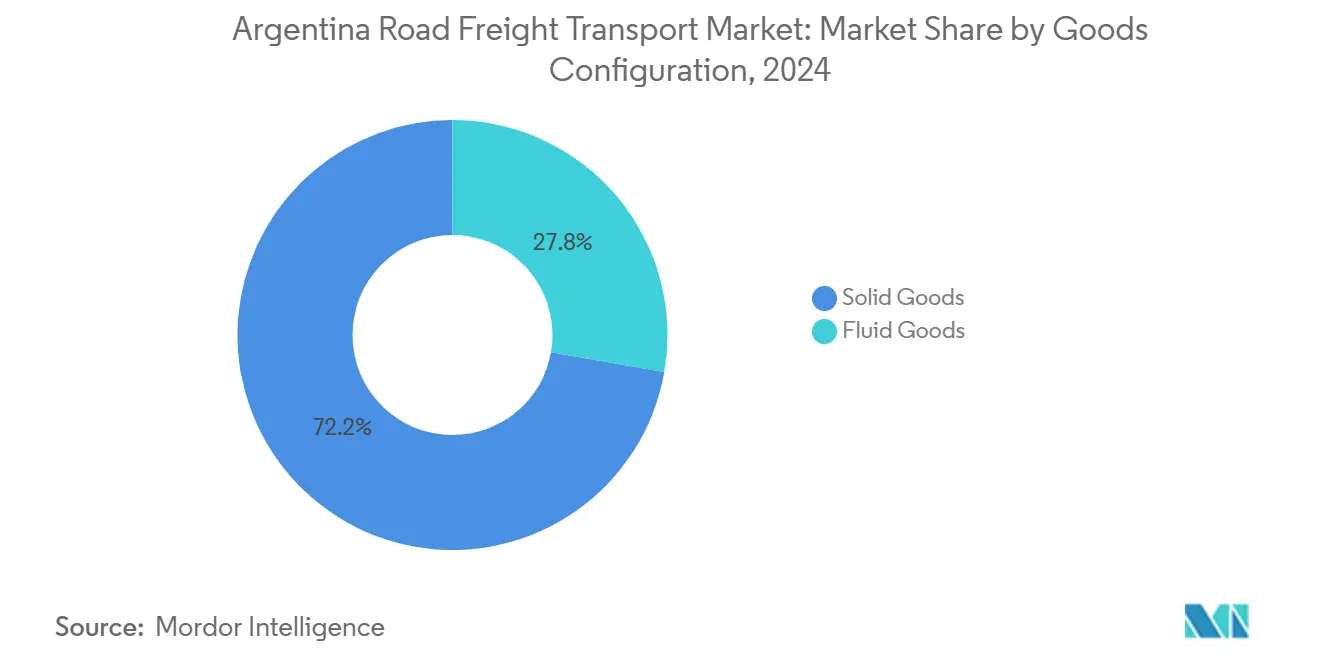

- By goods, solid goods accounted for 72.24% of the Argentina road freight transport market size in 2025, meanwhile, fluid goods is accelerating at a 6.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Plan Vial 2030 highway-dualling program accelerates trunk-road capacity | +0.9% | National trunk routes, Buenos Aires-Rosario-Córdoba corridor | Long term (≥ 4 years) |

| Cold-chain boom from soaring chilled-beef and vaccine exports | +0.7% | Buenos Aires, Entre Ríos, Santa Fe | Medium term (2-4 years) |

| Mercosur single-window e-customs reduces border dwell time | +0.6% | Brazil, Chile, Paraguay crossings | Short term (≤ 2 years) |

| Rapid uptake of digital freight-matching platforms among SMEs | +0.5% | Major urban centers | Short term (≤ 2 years) |

| Pilot deployments of battery-electric rigid trucks in urban emission zones | +0.3% | Buenos Aires metro, Rosario | Medium term (2-4 years) |

| Bio-B100 fuel tax-credit scheme lowers line-haul operating costs | +0.4% | Agricultural provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Plan Vial 2030 Highway-Dualling Program Accelerates Trunk-Road Capacity

Argentina’s multi-year initiative is upgrading 5,000 kilometers of trunk highways to dual carriageway status, already cutting transit times by up to 30% along the Buenos Aires-Rosario-Cordoba axis. Faster journeys translate into higher daily kilometers per truck, allowing large fleets with modern tractors to spread fixed costs over more revenue miles. Enhanced pavement quality trims fuel consumption and tire wear for all carriers, although the competitive edge accrues to operators that can guarantee delivery windows demanded by just-in-time manufacturers. Private-sector maintenance concessions bundled into the build-operate contracts shift lifecycle risk away from the treasury and open vertical-integration opportunities for freight and logistics firms willing to co-invest in toll-road operations.

Cold-Chain Boom from Soaring Chilled-Beef and Vaccine Exports

Chilled-beef shipments topped 950,000 tons in 2024, while Argentina’s vaccine plants now supply biologics across 23 provinces, pushing demand for trailers capable of holding cargo at 0-2 °C end-to-end. Refrigerated units cost about 40% more than dry vans, yet specialized fleets recoup the premium within two years thanks to rate uplifts that hover near 50%. Strict SENASA and good distribution Practice rules restrict new entrants, effectively protecting incumbents that already comply. Geographic clustering of meat plants in Buenos Aires and Entre Rios enables route density, while vaccine deliveries to remote northern provinces fetch surcharges that offset partial-load backhauls[1].USDA FOREIGN AGRICULTURAL SERVICE, “Livestock and Products Semi-annual Report,” usda.gov

Mercosur Single-Window E-Customs Reduces Border Dwell-Time

Fully functional since late 2024 at the busiest Brazil-Argentina crossings, the single-window portal compresses 14 paper documents into one electronic record, slicing clearance time to as little as two hours for compliant fleets. Productivity gains of 15-20% per tractor allow operators to redeploy capacity and raise turnover without adding vehicles. E-customs capability is rapidly becoming a prerequisite in shipper tenders, effectively penalizing carriers that delay investing in electronic data interchange systems.

Rapid Uptake of Digital Freight-Matching Platforms Among SMEs

Roughly 35% of small and mid-sized carriers in Buenos Aires, Cordoba, and Rosario now source loads via online marketplaces, cutting empty kilometers from 40% to about 25% and shrinking order-to-pickup lead times to mere hours. Platform commissions of 8-12% do squeeze margins, yet higher utilization offsets the fee. Spot freight dominates current volumes, though several platforms are piloting contract modules that could bring predictable revenue streams to qualified carriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX volatility and import-licence caps disrupt truck-parts supply | -1.1% | Nationwide, acute need for imported fleets | Short term (≤ 2 years) |

| Chronic driver shortage amid an aging workforce and licence bottlenecks | -0.9% | National, severe in remote provinces | Long term (≥ 4 years) |

| Rising cargo-theft hotspots inflate insurance premiums | -0.6% | Buenos Aires-Rosario corridor, northern provinces | Medium term (2-4 years) |

| Border-post IT outages cause unpredictable transit delays | -0.4% | Secondary international crossings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cargo-Theft Hotspots Inflate Insurance Premiums

Organized cargo theft jumped 35% in 2024 along the Buenos Aires-Rosario corridor, targeting electronics, pharmaceuticals, and agro-inputs. Insurers raised rates by up to 25% on the worst lanes, and some require armed escorts that add USD 200-400 per trip. Smaller carriers, with little leverage at renewal time, bear the brunt.

Border-Post IT Outages Cause Unpredictable Transit Delays

While primary crossings boast 95% system uptime, second-tier posts still suffer weekly outages that can balloon clearance time from two hours to two days. Operators now build buffer hours into schedules and diversify routes, but the lost utilization undercuts the gains from e-customs digitalization[2].ARGENTINE TRUCKERS CONFEDERATION, “Driver Workforce Analysis,” camioneros.org.ar

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing Reactivation Drives Acceleration

Manufacturing freight rose to a 6.11% CAGR, narrowing the gap with the wholesale and retail trade’s 37.46% 2025 share of the Argentina road freight transport market size. Investment incentives under the RIGI regime have triggered multi-year plant expansions, increasing inbound raw-material moves and outbound finished-goods traffic. Mining and energy projects generate specialized heavy-haul requirements, especially for equipment headed to Vaca Muerta and the lithium triangle. Agriculture continues to create seasonal peaks that reshuffle capacity, while private residential building in Greater Buenos Aires keeps construction-material flows resilient.

The Argentina road freight transport industry also benefits from diversification: cold-chain fleets capture pharmaceutical volumes, general-cargo carriers pivot between agribusiness and consumer goods, and niche specialists focus on oversized cargo. Operators with multi-vertical portfolios smooth revenue seasonality, whereas mono-commodity haulers remain vulnerable to crop cycles.

By Truckload Specification: Digital Platforms Enable LTL Surge

Full truckload owned 78.08% of the Argentina road freight transport market size in 2025, yet less-than-truckload expanded at 6.69% CAGR as platforms aggregated partial shipments. LTL networks thrive on e-commerce parcelization and on manufacturers’ move toward smaller, just-in-time orders. Modern cross-docks and route-optimization software underpin profitability despite complex handling. Meanwhile, full truckload remains indispensable for bulk grains, petro-products, and project cargo that demand dedicated capacity. Competitive pressure pushes FTL operators to adopt dynamic pricing tools and to sign annual contracts that lock in volume security.

Asset utilization is the differentiator: LTL rigs often log two urban turns per day, whereas FTL tractors that secure balanced backhauls hit utilization targets only when digital spot platforms quickly match return loads. Hence both segments increasingly rely on the Argentina road freight transport market’s growing digital infrastructure for efficiency.

By Destination: Cross-Border Digitalization Narrows Growth Gap

Domestic services accounted for 62.89% of the Argentina road freight transport market size in 2025, but international services to Brazil, Chile and Paraguay are growing faster at a CAGR of 5.45%, thanks to single-window customs that shorten crossings by several hours. International hauls fetch 15-20% higher yields per kilometer, provided carriers invest in bilingual dispatch, customs documentation expertise, and fleet specifications accepted on both sides of the border. Peso depreciation further boosts export competitiveness, maintaining two-way load factors despite asymmetrical trade volumes.

Domestic freight dynamics still hinge on Buenos Aires, which concentrates 45% of loads. Secondary provinces suffer higher logistics costs, incentivizing intermodal rail revival projects and the spread of inland container depots that shorten truck legs. These initiatives aim to rebalance capacity within the Argentina road freight transport market without undermining long-distance haulers’ business models[3].MINISTRY OF PUBLIC WORKS, “National Highway Statistics,” argentina.gob.ar

By Containerization: Port Upgrades Accelerate Shift

Non-containerized cargo still holds an 85.2% of the Argentina road freight transport market share in 2025, yet containerized volumes climb at a 6.80% CAGR as upgrades at Buenos Aires, Rosario, and Bahía Blanca ports raise crane moves per hour and cut truck wait times. Standardized boxes reduce pilferage and damage for high-value goods, making shippers willing to absorb a 10-15% rate premium. Meanwhile, agricultural bulk and petroleum products remain in tipper or tanker formats, limiting container share gains but ensuring diversification within the Argentina road freight transport market.

For carriers, mixed fleets become vital. Those able to swap between skeletal chassis and bulk trailers protect utilization through crop seasons and slack periods alike. Data-driven dispatch that forecasts container imbalances further elevates margins.

By Distance: Urban Densification Propels Short-Haul Growth

Long-haul lanes still command 70.91% of revenue, a testament to Argentina’s geographic sprawl. Yet short-haul traffic post a 6.02% CAGR, powered by urban consolidation centers, same-day e-commerce promises, and manufacturers decentralizing inventories. Short-haul trucks now run multiple daily loops, generating revenue densities rivaling long-haul figures despite lower per-kilometer tariffs. Urban congestion, however, forces the adoption of smaller rigs that navigate narrow streets and off-peak delivery windows that beat traffic.

Fuel cost exposure rises with distance, so long-haul carriers are quickest to leverage biodiesel credits and highway mpg gains from Plan Vial 2030. Utilization hinges on securing backhauls from interior provinces to coastal consumption hubs within the Argentina road freight transport market.

By Goods Configuration: Biodiesel Expansion Lifts Fluid Growth

Solid goods command 72.24% of shipments in the Argentina road freight transport market share in 2025, yet fluid commodities, especially biodiesel feedstock, chemicals, and petroleum products, grow at a 6.15% CAGR. Specialized tankers enjoy rate premiums and lower competition because of high capital thresholds and stringent certification. Concentration of biodiesel plants in Santa Fe and Cordoba provinces guarantees predictable lanes, while chemical output near Buenos Aires supports balanced round trips.

Solid-cargo carriers face commoditized pricing but hedge through niche services: refrigerated pallets, over-dimensional, or high-security electronics moves. Diversification is increasingly essential to navigate margin swings within the Argentina road freight transport market.

By Temperature Control: Pharmaceutical and Protein Exports Drive Expansion

Non-temperature-controlled freight accounted for 94.33% of the Argentina road freight transport market in 2025, while temperature-controlled shipments are projected to grow at an 8.83% CAGR. Beef exporters and vaccine manufacturers insist on verifiable 0-2 °C integrity, making IoT telemetry and redundant cooling systems standard. Rate uplifts of 40-50% cover the extra diesel or electricity cost for reefers and qualify carriers for long-term contracts that anchor fleet-financing models.

Ambient freight remains the backbone of the Argentina road freight transport market, but commoditization pushes general carriers to adopt telematics, safety certifications, and digital customer portals to stand out.

Geography Analysis

The Buenos Aires-Rosario-Cordoba industrial triangle generates roughly 60% of national truck traffic, creating network density that supports high backhaul ratios and keeps rate volatility relatively low. Harvest surges in the Pampas flood ports from March to June, lifting spot prices and stressing equipment supply. Northwestern provinces surge on mining cargo bound for lithium and copper projects perched at altitudes above 4,000 meters, demanding specialized prime movers, retarders, and driver acclimatization protocols. Patagonia’s sparse but high-value loads, include wool, live cattle, and wind-farm components, invite select carriers equipped for extreme climates.

Border provinces profit from the Mercosur customs upgrade. At Paso de los Libres, fleets now clear into Brazil in two hours; yet further north, IT outages remain common, prompting carriers to pre-book slots at redundancy-capable crossings. Coastal terminals enjoy dredging and crane upgrades that lift container turn times, while inland provinces wrestle with weight-limit enforcement on secondary roads that sap productivity.

Regulatory fragmentation persists: 23 provinces interpret axle-load rules differently, compelling dispatchers to map routes that balance distance against fine risk. Larger fleets exploit local subsidiaries to navigate permits; smaller firms face paperwork overload, widening the competitive gap in the Argentina road freight transport market.

Competitive Landscape

The top 10 carriers together hold roughly 28% of total revenue, confirming a low concentration playing field. National names such as Andreani, TASA Logistica, and Via Cargo continue to scale technology investments in telematics, cross-dock automation, and customer-facing portals. Multinational integrators DSV, Yusen, and Geodis expand via targeted acquisitions that secure cross-border expertise and storage footprints[4]ANDREANI LOGÍSTICA, “Corporate Newsroom,” andreani.co.

Family-owned regional haulers still dominate provincial markets, leveraging personal relationships and intimate lane knowledge. Yet rising insurance premiums and driver wage inflation pressure thin margins, nudging small fleets toward collaboration platforms or outright sale. Cold-chain specialists guard their moats by locking up scarce GDP-certified warehouse capacity, while security-focused carriers tout BASC credentials to win electronics and pharma contracts.

Sustainability credentials emerge as a fresh differentiator. Early adopters of battery-electric trucks in Buenos Aires secure flagship accounts with retailers chasing net-zero pledges. Fleets retrofitting tractors for B100 biodiesel enjoy fuel rebates and PR value as “green” partners. Over time, capital requirements for alternative-fuel assets may accelerate consolidation inside the Argentina road freight transport market.

Argentina Road Freight Transport Industry Leaders

Andreani Logistica S.A.

TASA Logistica

Logística Urbana S.A.

OCASA

DHL Supply Chain Argentina

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Andreani Logistica S.A. Launched a new cross-border unit to handle larger and more complex international cargo shipments, adding solutions for import/export, aerial, and maritime transport.

- March 2025: Andreani Logistica S.A. Partnered with Nestlé Argentina to operate a USD 15 million automated distribution center (DC) in Córdoba, improving temperature-controlled logistics and FMCG (fast-moving consumer goods) operations.

- March 2025: Yusen Logistics Argentina collaborated with Toyota Argentina, launching a bitren truck operation (a long-haul high-capacity vehicle) between the Port of Buenos Aires and the Zarate Campana hub.

- January 2025: Yusen Logistics Argentina enlarged its Buenos Aires warehouse by 40% to support e-commerce fulfillment demand and ensure improved storage/handling capacity for growing parcel volumes.

Argentina Road Freight Transport Market Report Scope

| Domestic |

| International |

| Manufacturing |

| Oil, Gas, Mining and Quarrying |

| Agriculture, Fishing and Forestry |

| Construction |

| Wholesale and Retail Trade |

| Other End-Users |

| Full Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Containerised |

| Non-Containerised |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperatured Controlled |

| Temperatured Controlled |

| By Destination | Domestic |

| International | |

| By End-User Industry | Manufacturing |

| Oil, Gas, Mining and Quarrying | |

| Agriculture, Fishing and Forestry | |

| Construction | |

| Wholesale and Retail Trade | |

| Other End-Users | |

| By Truckload Specification | Full Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| By Containerization | Containerised |

| Non-Containerised | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperatured Controlled |

| Temperatured Controlled |

Key Questions Answered in the Report

How large will Argentina’s road freight sector be by 2031?

It is projected to reach USD 17.41 billion by 2031, expanding at a 4.62% CAGR from 2026.

Which segment is growing the fastest?

Temperature-controlled logistics, propelled by pharmaceutical and chilled-beef exports, are advancing at an 8.83% CAGR.

What share do domestic hauls hold in 2025?

Domestic movements account for 62.89% of the 2025 Argentina road freight transport market size.

Why are digital freight platforms important?

They cut empty kilometers from 40% to 25% for SMEs, lifting utilization and enabling competitive pricing.

How is infrastructure affecting performance?

Plan Vial 2030 dual-carriageway upgrades have already trimmed transit times up to 30% on core corridors, boosting truck productivity.

What security challenges do carriers face?

Cargo-theft hotspots along Buenos Aires-Rosario have raised insurance premiums by as much as 25%, pressuring smaller fleets.

Page last updated on: