United Arab Emirates Aquaculture Market Analysis by Mordor Intelligence

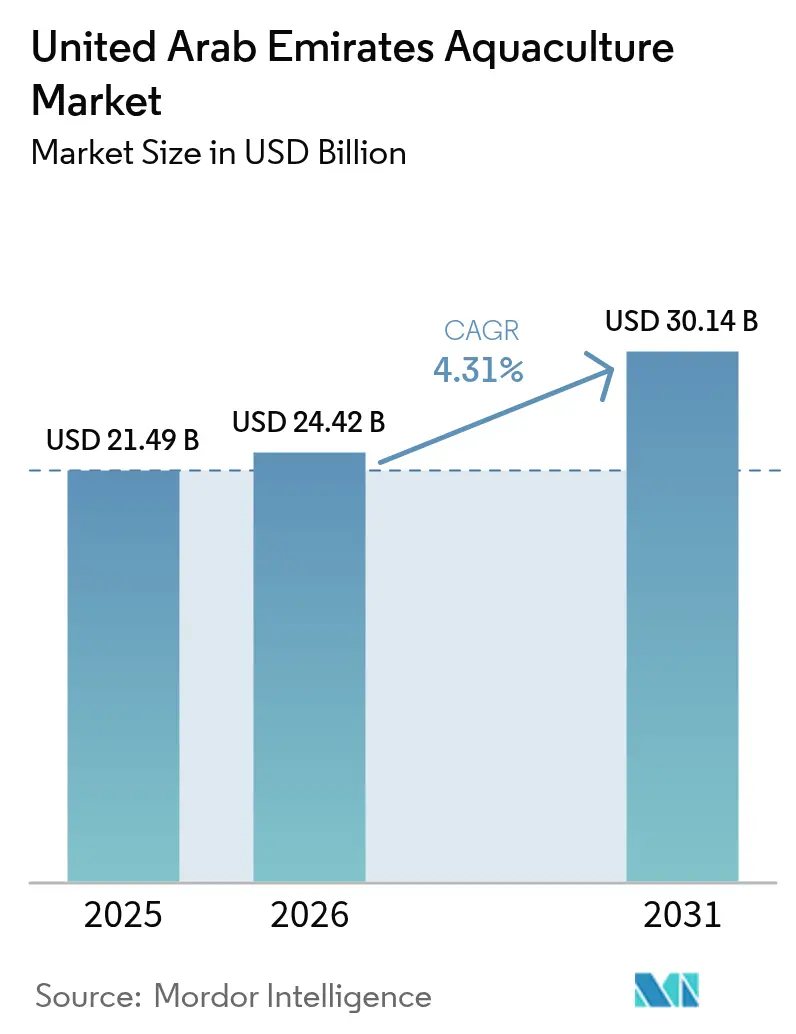

The United Arab Emirates aquaculture market size was valued at USD 21.49 billion in 2025 and is estimated to grow from USD 24.42 billion in 2026 to USD 30.14 billion by 2031, at a CAGR of 4.31% during the forecast period (2026-2031). Growth is unfolding as federal food-security targets push the sector away from reliance on wild catch toward controlled farming that can withstand Gulf salinity and temperature extremes. Shrimp leads current revenues, but Atlantic salmon and rainbow trout are scaling rapidly inside recirculating aquaculture systems that bypass the region’s thermal limits. Biosecurity subsidies, blockchain traceability pilots, and new offshore zones near Delma Island are lowering technical risk and unlocking investment, while Dubai’s fine-dining boom has strengthened premium demand, offsetting higher domestic production costs. At the same time, gradual reductions in wild-catch quotas are lifting farm-gate prices for cage-reared grouper and seabream, reinforcing the commercial rationale for large-scale farms.

Key Report Takeaways

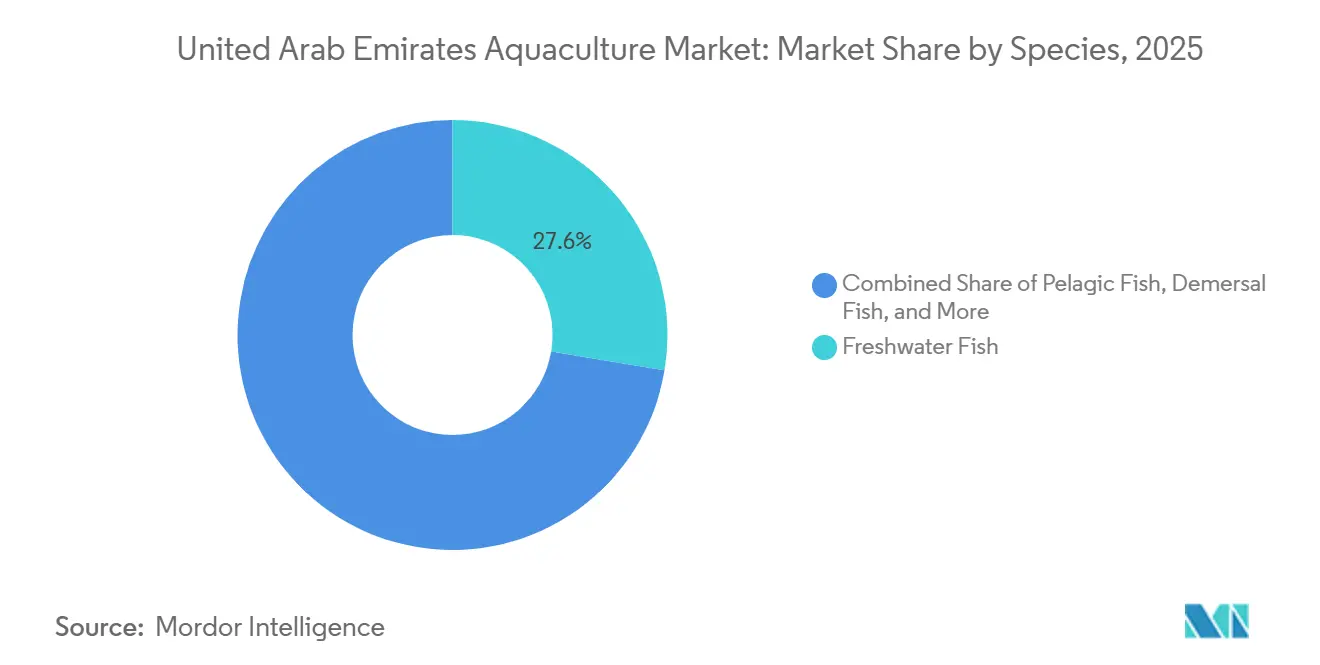

- By species, freshwater fish led with 27.6% of the United Arab Emirates aquaculture market share in 2025, while mollusks are forecast to register a 5.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic per-capita seafood consumption | +2.8% | National, with early gains in Dubai, Abu Dhabi, and Sharjah | Medium term (2-4 years) |

| Federal biosecurity subsidies for hatchery upgrades | +2.1% | National, administered by Ministry of Climate Change and Environment (MOCCAE) | Short term (≤ 2 years) |

| Gradual phase-out of wild-catch quotas | +1.9% | National, with the highest impact in Abu Dhabi, and Fujairah coastal zones | Long term (≥ 4 years) |

| Mandatory adoption of biofloc systems in inland farms | +2.4% | National, concentrated in inland emirates (Sharjah, Ajman, Umm Al Quwain) | Medium term (2-4 years) |

| Blockchain-based traceability pilots for high-value exports | +1.6% | Dubai, Sharjah, and Abu Dhabi export hubs | Medium term (2-4 years) |

| Zoning of offshore cages around artificial islands | +2.5% | Abu Dhabi, Ras Al Khaimah, and Fujairah coastal waters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Per-Capita Seafood Consumption

Expatriate communities, comprising 88% of the United Arab Emirates' population, are driving a shift toward lean proteins that align with wellness trends and Mediterranean culinary preferences. According to FAO Fisheries Statistics, per-capita seafood consumption in the United Arab Emirates reached 26.4 kilograms in 2022 and rose to 28.6 kilograms by 2025[1]Source: Food and Agricultural Organization, “UAE Aquaculture Sheet 2025,” fao.org. This figure surpasses the global average, positioning the United Arab Emirates among the highest seafood consumers in the Middle East. Hotels, restaurants, and catering services account for 75% to 80% of the premium oyster output from Dibba Bay, which ensures harvests are delivered within 24 hours to retain the glycogen sweetness often lost during the three-to-five-day transit of imported oysters. Additionally, the migration of high-net-worth individuals to Dubai and Abu Dhabi is driving increased demand for luxury seafood items such as caviar and salmon. This trend has created a bifurcated market, where premium species command higher prices, offsetting the cost challenges associated with local production.

Federal Biosecurity Subsidies for Hatchery Upgrades

Cabinet Resolution No. 134 of 2023, which governs the export of aquatic life, includes a provision for a 50% capital-expenditure subsidy. Administered by the Ministry of Climate Change and Environment, this subsidy supports hatchery modernization, broodstock quarantine facilities, and polymerase chain reaction diagnostic equipment. Since its implementation, the subsidy program has facilitated 49,230 transactions, reducing the payback period for biosecurity investments from seven years to under four years. This initiative has also enabled smaller operators to compete more effectively with vertically integrated conglomerates. The Food and Agriculture Organization's Inter-Regional Workshop on Integrated Biosecurity Index, held in Abu Dhabi in April 2024, recognized the United Arab Emirates as a regional leader in harmonizing aquatic animal health protocols and capacity-building frameworks. Operators upgrading to closed-containment hatcheries can prevent vertical transmission of disease from broodstock to larvae. This advancement is particularly beneficial for shrimp producers combating white-spot syndrome and early-mortality syndrome.

Gradual Phase-Out of Wild-Catch Quotas

The Ministry of Climate Change and Environment's fourth-quarter circular for 2024 announced a gradual reduction in wild-catch quotas, aiming for a 30% decrease by 2028 and a near-complete phase-out by 2030 for commercially significant demersal species such as grouper, emperor, and pomfret. This measure is intended to restore depleted spawning stocks resulting from overfishing and habitat degradation. Abu Dhabi has achieved 100% sustainable fishing by implementing spatial closures and gear restrictions, demonstrating the effectiveness of these strategies. As wild-catch volumes decline, farm-gate prices for cultured grouper and other demersal species are projected to rise through 2031. This price increase enhances the economic viability of cage-culture operations, which have historically faced challenges in competing with low-cost trawl landings. Additionally, the phase-out creates opportunities for exporters to source farmed products domestically and re-export them to Gulf Cooperation Council countries that continue to depend heavily on wild-capture fisheries.

Mandatory Adoption of Biofloc Systems in Inland Farms

Biofloc technology, which fosters microbial flocs that assimilate ammonia and provide supplemental protein, can lower feed conversion ratios by 25% and reduce water exchange requirements by up to 90%. This makes it particularly suitable for the United Arab Emirates' arid inland regions, where freshwater is both scarce and expensive. The 2027 mandate will require inland tilapia and shrimp farms to upgrade with aeration blowers, carbon-dosing systems, and mechanical clarifiers. While this will increase upfront capital costs by an estimated 30%, the resulting operating cost savings are projected to recover the investment within 3 to 4 years. Research published in February 2025 in the Journal of the World Aquaculture Society by a team from United Arab Emirates University confirmed that aquaponics and biofloc systems can achieve water-use efficiency improvements of 90% to 99% compared to conventional aquaculture. Additional benefits include nutrient recycling and reduced greenhouse gas emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs caused by hypersaline water | -1.8% | National, most acute in Abu Dhabi, and Dubai coastal zones | Short term (≤ 2 years) |

| Scarcity of locally bred brood-stock lines | -1.4% | National, affecting all species except the oyster | Medium term (2-4 years) |

| Dependence on imported premium feed ingredients | -1.2% | National, with the highest exposure in the shrimp and salmon segments | Short term (≤ 2 years) |

| Gaps in real-time aquaculture disease surveillance | -1.0% | National, with only two PCR laboratories serving the entire country | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Costs Caused by Hypersaline Water

Gulf waters frequently exceed 42 parts per thousand in salinity during the summer months. This necessitates the installation of reverse-osmosis units, which increase production costs by USD 0.35 per kilogram and consume energy equivalent to 3.5 kilowatt-hours per cubic meter of treated water. Species such as tilapia, rainbow trout, and Atlantic salmon, which thrive in salinities below 35 parts per thousand, cannot survive direct exposure to the Gulf's ambient conditions. As a result, operators must continuously desalinate water or blend it with brackish groundwater, which itself contains elevated levels of total dissolved solids. In Abu Dhabi and Dubai, operators are also investigating hybrid systems that combine seawater with treated municipal wastewater. However, regulatory approval under the Environment Agency Abu Dhabi's Protected Areas Policy requires prior environmental impact assessments and compatibility studies.

Scarcity of Locally Bred Broodstock Lines

The United Arab Emirates currently relies entirely on imported broodstock for shrimp, salmon, seabass, and seabream, with average lead times of six months from hatcheries located in the United Kingdom, France, Norway, and Thailand. This reliance makes producers vulnerable to freight disruptions. For instance, in 2024, disruptions in the Red Sea and Suez Canal increased transit times by 20% to 30% and led to higher shipping costs. Domestic breeding programs are still in their early stages. Fish Farm LLC's hatchery in Umm Al Quwain produced approximately 6 million fingerlings between 2022 and 2023, but this output meets less than 15% of the national demand[2]Source: Fish Farm LLC, “Press Kit 2025,” fishfarm.ae . Additionally, the lack of locally adapted broodstock hinders the development of genetic gain programs to improve feed efficiency, disease resistance, and thermal tolerance. These traits are essential for species cultivated in Gulf conditions, where summer water temperatures can reach up to 34 degrees Celsius.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Freshwater Fish Hold the Largest Share

Freshwater fish captured 27.6% of the United Arab Emirates aquaculture market share in 2025, driven by tilapia farming systems that integrate hydroponic vegetable production, achieving 90% water savings compared to traditional open-pond systems. Major integrated farms in Al Ain produce over 200,000 tilapia units annually, supplying major retail chains and institutional buyers. These farms maintain stable profit margins through cost-efficient practices, including solar-powered pumps and in-house hatcheries, despite reliance on imported feed. Government support for food security initiatives continues to sustain this segment, although growth may slow as production capacity matures and demand for marine species rises. Despite low import tariffs on chilled tilapia, domestic producers maintain premium pricing due to freshness advantages and halal certification. Additionally, the segment's strong environmental performance aligns with the United Arab Emirates climate objectives, securing public-sector grants and reinforcing its market position.

Mollusks are projected to grow at a 5.2% CAGR from 2026 to 2031, the fastest growth rate in the United Arab Emirates aquaculture market. Dibba Bay Oysters produces 4.5 million oysters annually, supplying fine-dining establishments within 48 hours and showcasing successful commercial operations under local conditions. Key advantages of this segment include minimal feed requirements, natural water filtration, and opportunities to recycle shell waste. The sector's export potential is enhanced by Emirates SkyCargo's network, enabling live product delivery within 10 hours to premium international markets. Research grants awarded to scallop pilot farms in Fujairah in 2025 indicate potential expansion beyond oyster production. While disease management is less complex compared to finfish, advanced biosecurity protocols and monitoring systems are required to address harmful algal blooms effectively.

Competitive Landscape

Abu Dhabi and Dubai play a significant role in the national aquaculture output through their land resources, logistics infrastructure, and government-backed investments. Abu Dhabi's Khalifa Economic Zones Abu Dhabi (KEZAD) aquaculture zone, covering 1.1 square kilometers, includes integrated facilities such as hatcheries, feed storage, and cold-chain networks. This zone is projected to contribute AED 90 billion (USD 24.48 billion) to GDP by 2045. Additionally, the emirate benefits from an AED 2 billion (USD 0.54 billion) subsidy program aimed at farm modernization and certification. Dubai's strategic location near international air freight routes, coupled with strong food-service demand, supports efficient live-seafood logistics operations and enhances production cycles. Fujairah is emerging as a center for marine species production, leveraging its location in the Arabian Sea and its established fishing infrastructure. The emirate's offshore conditions are particularly suitable for oyster cultivation and cage-culture operations, diversifying production beyond inland facilities.

The northern emirates of Ras Al Khaimah and Umm Al Quwain possess brackish lagoons suitable for moderate-scale farming. These regions face challenges in attracting investment due to a limited local market size and a shortage of technical workforce. In response to Saudi Arabia's large-scale expansion of aquaculture, the United Arab Emirates is prioritizing high-value species production, technological advancements, and re-export logistics capabilities. This strategic focus helps the United Arab Emirates manage climate and resource risks while positioning its aquaculture market as a technology-driven leader within the Gulf Cooperation Council (GCC) region.

The Environment Agency Abu Dhabi has conducted hydrodynamic modeling for sites west and southeast of Delma Island. This, combined with the maritime spatial plan designating 12 zones for aquaculture development, has opened 3,800 hectares of new offshore areas[3]Source: Environment Agency Abu Dhabi, “Sea-Cage Aquaculture Project Launch,”ead.gov.ae . These areas feature current velocities exceeding 10 centimeters per second, sufficient to flush metabolic waste and maintain dissolved oxygen levels above 5 milligrams per liter without mechanical aeration. Such advancements further enhance the United Arab Emirates aquaculture capabilities and sustainability efforts.

Geography Analysis

The United Arab Emirates aquaculture market encompasses a comprehensive network of stakeholders across the value chain. These include producers, exporters, importers, regulators, investors, technology providers, and research institutions, all supported by robust government strategies and infrastructure. At the production level, key participants include commercial fish farms, hatcheries, and vertically integrated seafood companies. These entities cultivate finfish and shellfish using advanced systems such as recirculating aquaculture systems (RAS) and marine cages. Downstream stakeholders include processors, distributors, retailers, and export-import agencies that link domestic production to both local and international markets. Additionally, equipment suppliers, industry associations, financial institutions, and investors provide operational and capital support.

Government bodies, including the Ministry of Climate Change and Environment and food-control authorities, play a pivotal role in regulation and facilitation. They offer licensing services, technical guidance, biosecurity controls, and incentives to attract private investment. Regulatory compliance frameworks, such as the Environment Agency Abu Dhabi's Protected Areas Policy and the United Arab Emirates National Action Plan on Antimicrobial Resistance 2025–2031, are enhancing biosecurity and environmental management standards. These frameworks favor operators with the capacity to invest in closed-containment systems and real-time disease surveillance technologies.

The United Arab Emirates has implemented a National Aquaculture Strategy and food security policies to expand local fish production, foster research and innovation, diversify species, and increase exports. Significant investments are being made in infrastructure, technology, and sustainability initiatives. The aquaculture ecosystem in the United Arab Emirates is characterized by coordinated collaboration among government entities, private industry, research institutions, and global trade partners. This positions the sector as a strategic pillar for food security, economic diversification, and regional seafood competitiveness. Technology adoption is emerging as a key competitive advantage. For instance, artificial intelligence-powered monitoring systems have been deployed in the Environment Agency Abu Dhabi's Delma Island cages, while blockchain traceability pilots in Sharjah are enabling early adopters to access premium export markets in the European Union and East Asia.

Recent Industry Developments

- November 2025: Khalifa Economic Zones Abu Dhabi (KEZAD )Group established a 1.1 sq km specialized zone in Abu Dhabi dedicated to aquaculture and related industries. The project aims to strengthen food security and generate more than 60,000 jobs by 2045. This development is part of the Abu Dhabi AgriFood Growth and Water Abundance (Agwa) Cluster, which focuses on increasing the United Arab Emirates's GDP, reducing import dependency, and developing sustainable food production systems.

- September 2025: Finnish land-based rainbow trout producer Finnforel expanded internationally by launching products in the United Arab Emirates (UAE). The company introduced its premium export brand, LoHi, in select LuLu supermarket retail chains across the country.

- November 2024: ADQ, an Abu Dhabi-based investment and holding company, has entered into an agreement with Finnforel, a Finnish aquaculture technology company, to assess the feasibility of cultivating rainbow trout in a land-based facility.

United Arab Emirates Aquaculture Market Report Scope

Aquaculture involves the controlled breeding, rearing, and harvesting of aquatic organisms such as fish, mollusks, crustaceans, and aquatic plants in freshwater, brackish water, or saltwater environments. The United Arab Emirates Aquaculture Market Report is segmented by Species (Pelagic Fish, and more). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Species

| Pelagic Fish |

| Demersal Fish |

| Freshwater Fish |

| Crustaceans |

| Mollusks |

| Other Species |

By Geography

| Production Analysis (Volume) | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destination Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistic and Infrastructure | ||

| Seasonality Analysis | ||

| By Species | Pelagic Fish | ||

| Demersal Fish | |||

| Freshwater Fish | |||

| Crustaceans | |||

| Mollusks | |||

| Other Species | |||

| By Geography | Production Analysis (Volume) | ||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How big is the United Arab Emirates aquaculture market in 2026?

The United Arab Emirates aquaculture market size was valued at USD 21.49 billion in 2025 and is estimated to grow from USD 24.42 billion in 2026 to USD 30.14 billion by 2031, at a CAGR of 4.31% during the forecast period (2026-2031).

Which farming technology is growing fastest?

Recirculating aquaculture systems expand due to biosecurity and year-round harvest advantages.

Why is Dubai seen as the fastest-growing emirate for fish farming?

Sovereign wealth and private equity funding of land-based salmon and shrimp projects plus strong HoReCa demand drive market.

What policy incentives support hatchery upgrades?

Cabinet Resolution 134 of 2023 reimburses 50% of hatchery capex for quarantine units and PCR labs, reducing payback periods to under four years.

Page last updated on: