Application Specific Communications Analog IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

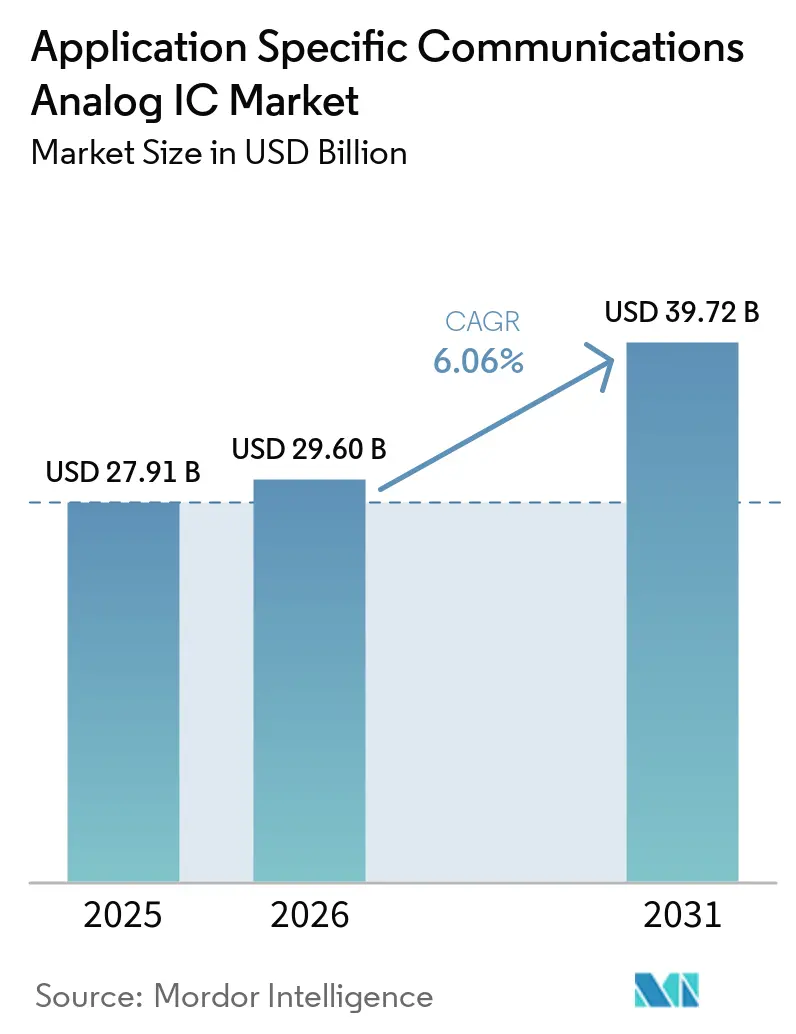

| Market Size (2026) | USD 29.60 Billion |

| Market Size (2031) | USD 39.72 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Specific Communications Analog IC Market Analysis by Mordor Intelligence

The application-specific communications analog IC market size was valued at USD 27.91 billion in 2025 and estimated to grow from USD 29.6 billion in 2026 to reach USD 39.72 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031). New 5G radio rollouts drive the expansion, the widening of IoT adoption, increased analog content in electric vehicles, and reshoring programs that multiply fab investments in the United States and Europe. Power-efficient radio transceivers priced at a premium, stringent thermal rules in millimeter-wave designs, and subsidies that offset greenfield fab costs combine to lift average selling prices despite broader semiconductor inventory corrections. Analog specialists also benefit as defense and critical-infrastructure buyers pay extra for secure, short-lead-time supply from trusted domestic foundries. At the same time, rising labor costs and wafer shortages in compound semiconductors constrain immediate capacity additions, maintaining a firm pricing environment and healthy margins across the value chain.

Key Report Takeaways

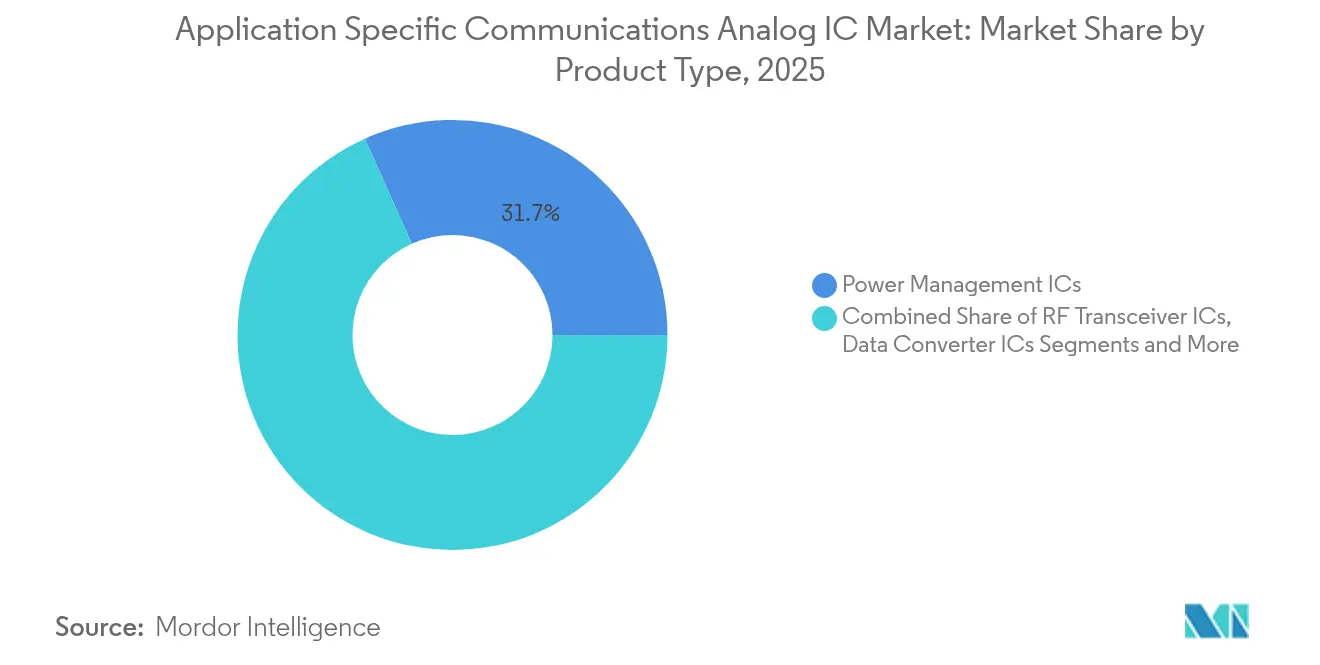

- By product type, power management ICs accounted for 31.68% of the application-specific communications analog IC market share in 2025, while RF transceiver ICs achieved the fastest 8.45% CAGR through 2031.

- By communication standard, 4G LTE and LTE-Advanced held 46.85% revenue share in 2025, whereas 5G New Radio records the sharpest 12.1% CAGR to 2031.

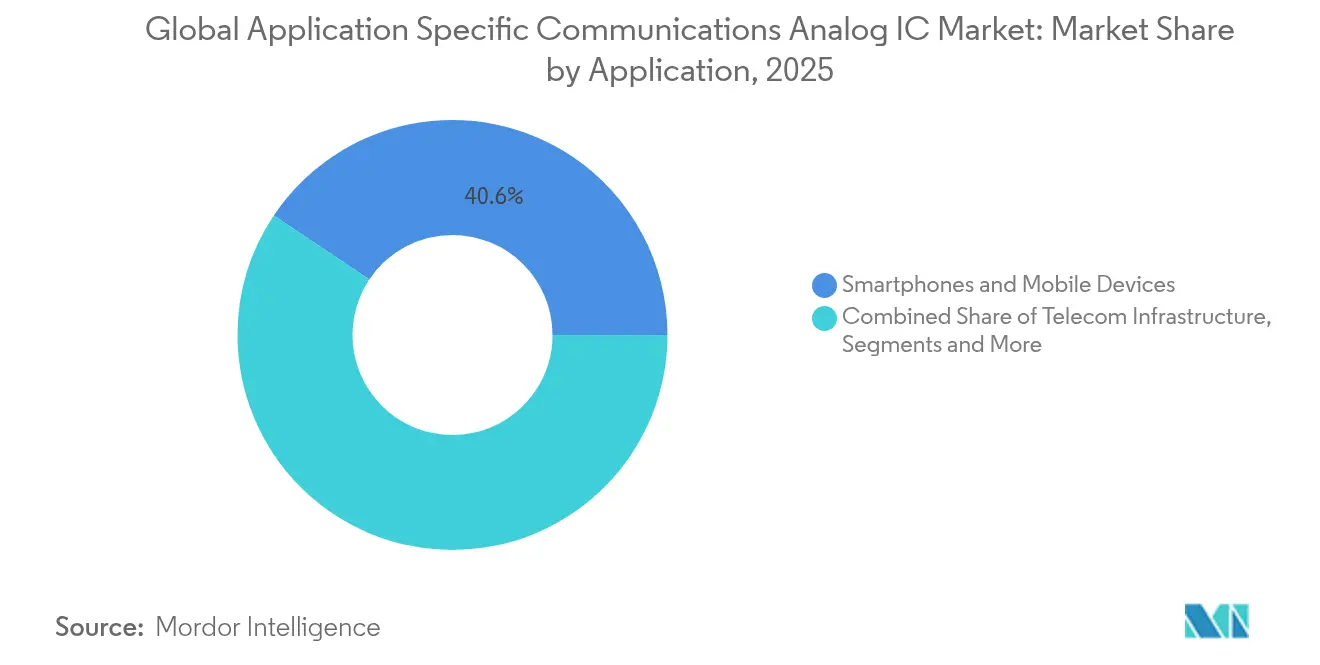

- By application, smartphones and mobile devices contributed 40.62% of the 2025 revenue, while IoT edge devices are projected to exhibit an 10.85% CAGR, becoming the most dynamic opportunity.

- By end-user industry, consumer electronics OEMs captured 37.95% of spending in 2025, while automotive OEMs and tier-1 suppliers advanced at a 11.76% CAGR, driven by the adoption of Ethernet backbones and radar proliferation.

- By geography, Asia Pacific secured 62.74% revenue in 2025 and also produces the highest 9.18% CAGR as China, Taiwan, and India enlarge local manufacturing bases.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Specific Communications Analog IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G infrastructure worldwide | +1.8% | Global, with APAC and North America leading deployments | Medium term (2-4 years) |

| Surge in IoT device deployments driving low-power analog front-ends | +1.5% | Global, concentrated in APAC manufacturing hubs and North America enterprise IoT | Medium term (2-4 years) |

| Rising demand for high-speed data converters in optical networks | +0.9% | North America, Europe, and APAC data-center corridors | Long term (≥4 years) |

| Growth of software-defined radios and Open RAN architectures | +0.7% | North America, Europe, and select APAC markets (Japan, South Korea) | Long term (≥4 years) |

| Electrification and connectivity in automobiles boosting in-vehicle analog ICs | +1.3% | Global, with Europe and China leading EV adoption | Medium term (2-4 years) |

| National semiconductor reshoring initiatives unlocking capex cycles | +0.6% | North America and Europe, spillover to Middle East and India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Infrastructure Worldwide

Commercial 5G networks reached 329 deployments, serving 2.1 billion connections in 2024, and operators plan to surpass 8.6 billion by 2029.[1]GSMA, “The Mobile Economy 2024,” gsma.comEach new base station requires analog front-end modules with sub-1 dB noise figures and thermally robust power amplifiers, increasing the bill of materials value over 4G radios by approximately 40%.[2]Ericsson, “Mobility Report November 2024,” ericsson.comChina Mobile spent CNY 180 billion (USD 25.2 billion) on 5G upgrades in 2024, while Verizon allocated USD 18.5 billion to extend mid-band coverage in the United States. Open RAN trials add fresh demand for IC socket solutions used in timing ICs and interface controllers, even as energy efficiency remains under review. Edge computing engines that support network slicing further raise demand for precision voltage references that keep wide-bandwidth data converters within tight linearity windows.

Surge in IoT Device Deployments Driving Low-Power Analog Front-Ends

Cellular IoT module shipments reached 423 million units in 2024, with NB-IoT connections set to double to 1.9 billion and LoRa connections forecast to reach 1.3 billion by 2030.[3]GSMA, “The Mobile Economy 2024,” gsma.comIndustrial sensors now target ten-year battery life, so designers push quiescent current below one microamp and integrate energy-harvesting support on-chip. Smart-city metering contracts across Europe and the Asia Pacific tend toward NB-IoT for licensed-spectrum reliability, while agriculture and logistics operators in North America favor LoRa for lower infrastructure costs. Nordic Semiconductor’s nRF54 platform, which shipped in 20 days, demonstrates how multi-protocol radio simplifies the bill of materials. AI inference is emerging in asset trackers and wearables, which in turn pulls in analog front-ends capable of dynamic voltage scaling and sensor-interface flexibility.

Rising Demand for High-Speed Data Converters in Optical Networks

Hyperscale data centers transitioned to 400G and 800G coherent optics in 2024, necessitating converters that sample above 100 Gsps with an effective number of bits greater than 6 to safeguard signal integrity. Analog Devices’ AD9081 mixed-signal front-end became a 400G ZR+ reference, demonstrating quad-channel converters that fit CFP2 modules.[4]Analog Devices, “AD9081 Data Converter,” analog.com Clock-and-timing ICs must maintain jitter under 100 fs RMS to drive those converters, a performance achieved by only a handful of suppliers at volume. Co-packaged optics that seat photonics beside switch ASICs tighten thermal drift budgets, pushing designers toward silicon-germanium or indium phosphide nodes. Accelerated AI training clusters inside data centers intensify east-west traffic, making sustained demand for high-speed analog ICs likely through at least 2030.

Electrification and Connectivity in Automobiles Boosting In-Vehicle Analog ICs

Electric vehicles triple analog semiconductor content per car as battery management, high-speed Ethernet backbones, radar, and vehicle-to-everything radios proliferate. Europe and China lead the way in EV adoption, with global sales increasing 31% year-over-year in 2024. High-current power management ICs delivering up to 100 amps with 95% efficiency, 77 GHz radar transceivers achieving sub-4 cm resolution, and Ethernet PHYs supporting 10-Gbps backbones lift the analog value per vehicle from USD 590 in 2024 to USD 1,000 by 2029. Centralized compute zonal architectures replace multiple smaller ECUs; yet, they require robust point-of-load regulation, galvanic isolation, and functional safety compliance to ISO 26262, which can only be met by a narrow vendor pool. Regulation that mandates advanced driver-assistance systems across Europe from 2026 locks in multi-year visibility for automotive-grade analog IC demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating design complexity and verification costs | -0.8% | Global, acute in North America and Europe where labor costs are highest | Short term (≤2 years) |

| Geopolitical export controls on advanced process nodes | -0.6% | APAC (China), spillover to global supply chains | Medium term (2-4 years) |

| Analog talent shortage slowing time-to-market | -0.5% | Global, most severe in North America and Europe | Long term (≥4 years) |

| Supply-chain volatility in specialty wafers | -0.4% | Global, concentrated in GaN and SiGe substrate availability | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating Design Complexity and Verification Costs

Design cycles for advanced analog parts stretched to up to 24 months in 2024 as mixed-signal verification spanned RF, power, and digital domains within a single die. Non-recurring engineering expenses exceeded USD 5 million for leading-edge radios, as multi-standard compliance increased transistor counts and parasitic interactions. Automated layout tools lag behind digital EDA by around ten years, necessitating manual placement that increases engineering labor costs. Advanced process nodes below 28 nm introduce fresh reliability checks for electromigration and hot-carrier injection, each demanding exhaustive corner simulations. Smaller fabless companies face a pronounced cash strain, often ceding high-performance segments to incumbents that can amortize costs across broad product portfolios.

Geopolitical Export Controls on Advanced Process Nodes

The United States expanded semiconductor export restrictions in October 2024, adding 140 Chinese entities to the Entity List and tightening rules on advanced packaging and EDA tools. China responded by curbing exports of gallium, germanium, and antimony, which extended analog IC lead times by up to 12 weeks in the fourth quarter of 2024. The European Union has aligned with licensing demands on dual-use lithography, indirectly limiting the expansion of foundries in the Asia-Pacific region that depend on EUV stepper imports. Multinational suppliers now maintain parallel design flows for restricted and unrestricted markets, resulting in an approximately 12% increase in operating overhead and dilution of scale benefits. The probability of a permanently bifurcated ecosystem remains high, which would fragment vendor roadmaps and delay the time-to-market for high-frequency analog ICs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RF Transceivers Capitalize on 5G and Wi-Fi 6E Momentum

The RF transceiver segment captured USD 8.3 billion in 2025 and is on track for an 8.45% CAGR, which outpaces the application-specific communications analog IC market through 2031. Sub-6 GHz and millimeter-wave radios inside 5G base stations, Wi-Fi 6E routers, and 77 GHz automotive radars lift the overall application-specific communications analog IC market size for this category, supported by premium pricing for sub-1 dB noise figures and 26 dBm output levels. Vendors merge power amplifiers, low-noise amplifiers, and filters in modules as small as 3 mm by 4 mm, shrinking board area for handset and CPE designers. Demand is further heightened by Open RAN deployments that require wide-bandwidth, multi-carrier support within the same hardware to minimize the need for truck rolls during software upgrades.

Although power management ICs held 31.68% of the application-specific communications analog IC market share in 2025, the commoditization of low-voltage regulators and intense price pressure from Chinese IDMs will likely limit their revenue growth to just shy of the market pace. Data converter ICs remain a niche, yet they fetch selling prices above USD 150 per channel in coherent optics or test equipment. Clock-and-timing ICs ride the synchronous Ethernet wave in 5G transport networks, while interface ICs expand with USB-C and automotive Ethernet PHYs that move toward 10 Gbps signaling.

By Communication Standard: 5G NR Overtakes Legacy Standards in Growth Velocity

5G New Radio will post a 12.1% CAGR, solidifying its position as the fastest riser within the application-specific communications analog IC market. Stand-alone 5G cores require radios that span both sub-6 GHz and millimeter-wave bands, driving front-end sales because most operators opt for complete platform swap-outs rather than incremental 4G overlays. Wi-Fi 6E refresh cycles in enterprise and residential gateways create further momentum, particularly as the 6 GHz band needs integrated acoustic-wave filters to mitigate interference.

4G LTE and LTE-Advanced still deliver scale, holding 46.85% share in 2025 and sustaining analog IC demand in emerging-market macro cells. Low-power wide-area networks are split between NB-IoT and LoRa by their regulatory environments, each calling for ultra-low-power front-ends rather than raw bandwidth, which makes price-performance optimization a decisive differentiator. Satellite and mission-critical links occupy a small but lucrative corner that prefers radiation-hardened GaN power amplifiers and SiGe low-noise amplifiers, where lifetimes extend five years or more.

By Application: IoT Edge Devices Outpace Mature Smartphone Segment

Smartphones accounted for 40.62% of 2025 revenue, yet replacement cycles in developed markets have lengthened to nearly 42 months, curbing handset analog IC expansion below the aggregate application-specific communications analog IC market. Conversely, IoT edge devices are advancing at an 10.85% CAGR, with the addition of gas meters, environmental sensors, and smart tags that ship in volumes of tens of millions per year. Their stringent battery budgets require sub-microamp standby currents, driving analog design innovation toward duty-cycled wake-up radios and adaptive power gating.

Telecom infrastructure continues to absorb premium radios and data converters as operators densify urban coverage. Automotive communication systems herald an era where Ethernet backbones, radar, and cellular-V2X quickly raise the cost of analog content above USD 1,000 per vehicle. Industrial automation and robotics extend Time-Sensitive Networking (TSN) and IO-Link protocols across the factory floor, driving the adoption of precision clocking ICs with 100 ns synchronization accuracy.

By End-User Industry: Automotive OEMs Accelerate Analog IC Adoption

Consumer electronics OEMs captured 37.95% of 2025 spending, primarily driven by smartphones, tablets, and laptops; however, cost pressure and incremental innovation are restraining category growth. Automotive OEMs and tier-1 suppliers drive a 11.76% CAGR, powered by the shift to electric powertrains and advanced driver assistance systems. Tesla, BYD, and Volkswagen are moving toward centralized computing that utilizes high-current point-of-load regulators, multi-gigabit Ethernet PHYs, and radar front-ends in common enclosures. Telecommunication operators remain dependable customers for RF and optical interface ICs as they stretch fiber deeper into access networks.

Industrial OEMs, such as Siemens and Rockwell Automation, integrate precision timing ICs to meet deterministic latency targets, while aerospace and defense contractors continue to pay 5-10 times the commercial pricing for radiation-hardened parts. Each group values long-term supply guarantees, which open opportunities for analog vendors able to certify extended temperature and functional-safety variants.

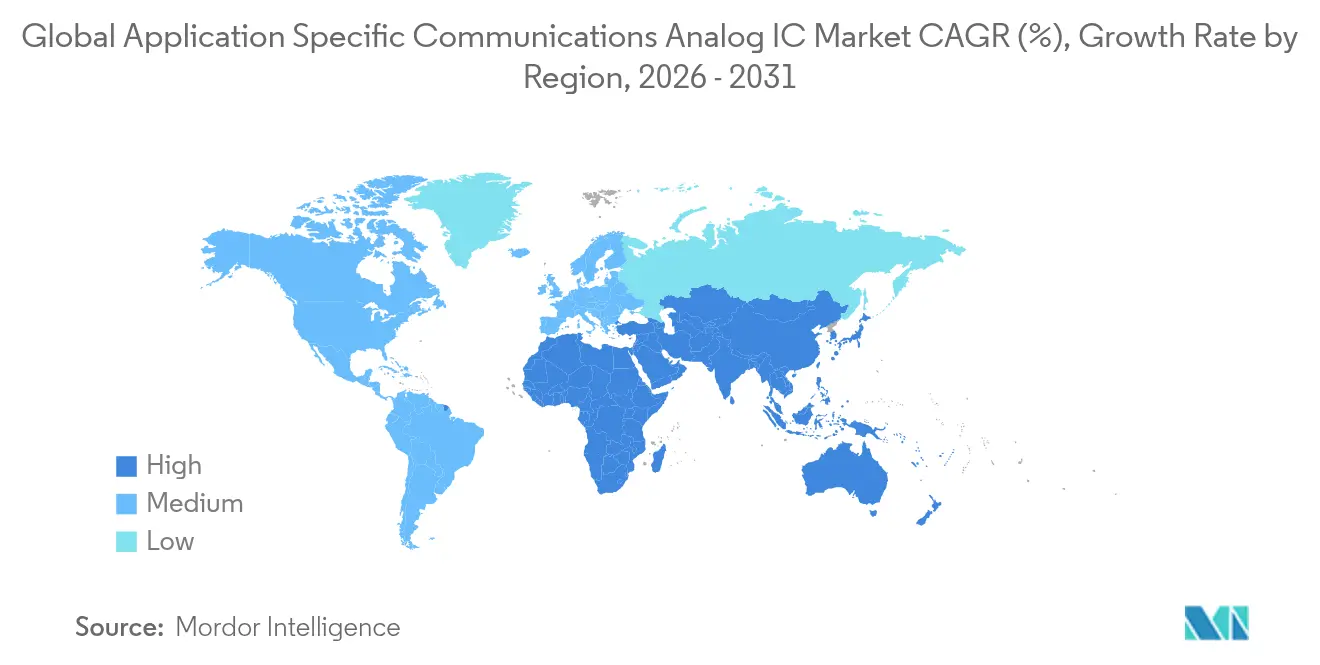

Geography Analysis

The Asia Pacific region accounted for 62.74% of 2025 revenue and is projected to compound at 9.18%, faster than any other region, as China increases its self-sufficiency spending, Taiwan maintains its leadership in specialty foundries, and India funds new fabs through its USD 10 billion incentive pool. China’s third semiconductor investment fund, capitalized at CNY 344 billion (USD 48.2 billion), channels capital toward analog design houses and compound semiconductor fabs. Taiwan Semiconductor Manufacturing Company already exceeds 200,000 analog wafer starts per month on mature nodes, supporting RF, power, and data converter customers at scale.

North America held approximately an 18.41% share, but the CHIPS Act subsidies, valued at USD 52.7 billion, are expected to bolster domestic capacity. TSMC’s USD 65 billion Arizona campus began production of 28 nm and 16 nm analog devices in 2024. Intel’s USD 20 billion Ohio complex targets automotive and industrial analog nodes at 180 nm and 130 nm. Europe, at roughly 12.16%, benefits from STMicroelectronics' and GlobalFoundries' joint investments to support automotive demand in France. South America and the Middle East remain small, but satellite ground station deployment and oil-field telemetry provide profitable niches for rugged analog ICs.

Competitive Landscape

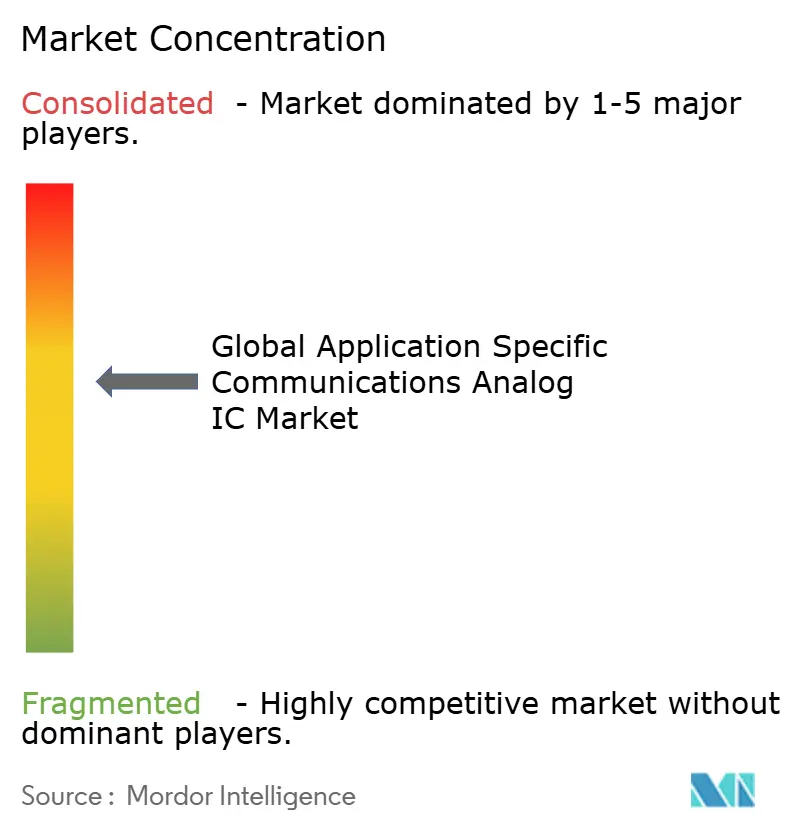

The moderate consolidation of the application-specific communications analog IC market is characterized by the top five suppliers, Texas Instruments, Analog Devices, Infineon Technologies, NXP Semiconductors, and STMicroelectronics, which collectively account for approximately half of the worldwide revenue. Incumbents enjoy scale advantages in vertically integrated manufacturing, proprietary intellectual property, and multi-decade customer ties. Still, Chinese IDMs such as Novosense and Chipanalog compete fiercely in cost-sensitive power management and low-speed interface categories, using aggressive bundled pricing to secure sockets in mass-market handsets and industrial controllers.

Gallium nitride and silicon-germanium mastery increasingly separates leaders from laggards as 5G, Wi-Fi 7, and automotive radar push toward 24-29 GHz and 77 GHz. Analog Devices’ USD 21 billion acquisition of Maxim Integrated strengthened its power management and data converter capabilities, while Renesas’ USD 5.9 billion acquisition of Altium aims to integrate EDA workflows with analog IP to shorten customer design cycles. Skyworks Solutions and Qorvo dominate the smartphone front-end module market, but face margin compression from system-on-chip rivals that integrate passive filters and Bluetooth coexistence controls.

Open RAN acceptance opens doors for Marvell Technology and MaxLinear, whose wide-bandwidth transceivers support split-mount radio units. Defense and aerospace clients tend to favor U.S.-trusted foundries; Qorvo’s USD 300 million Texas GaN expansion meets those security demands. Industrial users favor suppliers with robust functional-safety portfolios and ISO 26262 certifications, a field where Infineon and NXP lead in voltage tolerance and diagnostic coverage.

Application Specific Communications Analog IC Industry Leaders

Texas Instruments Incorporated

Analog Devices, Inc.

Infineon Technologies AG

NXP Semiconductors N.V.

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Texas Instruments commenced output at its USD 11 billion Richardson, Texas, 300 mm fab, adding 40,000 wafer starts a month of analog and embedded processing capacity for automotive and industrial buyers.

- February 2025: Infineon Technologies and Qualcomm Technologies entered a multi-year pact to craft integrated 5G millimeter-wave front-end modules that marry Infineon GaN power amplifiers with Qualcomm transceivers.

- January 2025: NXP Semiconductors rolled out its S32N automotive networking processors that combine 16-port Ethernet switches, Time-Sensitive Networking support, and hardware security in a single die.

- December 2024: Analog Devices acquired Test Motors to bolster motor-control algorithms and power-management IP for robotics and factory automation.

Global Application Specific Communications Analog IC Market Report Scope

The Application-Specific Communications Analog IC Market Report is Segmented by Product Type (RF Transceiver ICs, Power Management ICs, Data Converter ICs, Clock and Timing ICs, Interface ICs), Communication Standard (5G NR, 4G LTE/LTE-A, Wi-Fi 6 and 6E, IoT LPWAN, Satellite and Critical Comms), Application (Telecom Infrastructure, Smartphones and Mobile Devices, IoT Edge Devices, Automotive Communication Systems, Industrial Automation and Robotics), End-user Industry (Telecommunication Operators, Consumer Electronics OEMs, Automotive OEMs and Tier 1s, Industrial OEMs, Aerospace and Defense Contractors), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| RF Transceiver ICs |

| Power Management ICs |

| Data Converter ICs |

| Clock and Timing ICs |

| Interface ICs |

| 5G NR |

| 4G LTE / LTE-A |

| Wi-Fi 6 and 6E |

| IoT LPWAN (NB-IoT, LoRa, Sigfox) |

| Satellite and Critical Comms |

| Telecom Infrastructure |

| Smartphones and Mobile Devices |

| IoT Edge Devices |

| Automotive Communication Systems |

| Industrial Automation and Robotics |

| Telecommunication Operators |

| Consumer Electronics OEMs |

| Automotive OEMs and Tier 1s |

| Industrial OEMs |

| Aerospace and Defense Contractors |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Taiwan | |

| Southeast Asia | |

| Oceania | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | RF Transceiver ICs | |

| Power Management ICs | ||

| Data Converter ICs | ||

| Clock and Timing ICs | ||

| Interface ICs | ||

| By Communication Standard | 5G NR | |

| 4G LTE / LTE-A | ||

| Wi-Fi 6 and 6E | ||

| IoT LPWAN (NB-IoT, LoRa, Sigfox) | ||

| Satellite and Critical Comms | ||

| By Application | Telecom Infrastructure | |

| Smartphones and Mobile Devices | ||

| IoT Edge Devices | ||

| Automotive Communication Systems | ||

| Industrial Automation and Robotics | ||

| By End-user Industry | Telecommunication Operators | |

| Consumer Electronics OEMs | ||

| Automotive OEMs and Tier 1s | ||

| Industrial OEMs | ||

| Aerospace and Defense Contractors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Taiwan | ||

| Southeast Asia | ||

| Oceania | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the application-specific communications analog IC market in 2026?

The application-specific communications analog IC market size reached USD 29.6 billion in 2026.

What CAGR will the market post between 2026 and 2031?

The market is projected to expand at a 6.06% CAGR during the forecast period (2026-2031).

Which product segment grows fastest through 2031?

RF transceiver ICs register the highest 8.45% CAGR as 5G and Wi-Fi 6E radios proliferate.

Which region leads revenue?

Asia Pacific commands 62.74% of revenue and also delivers the strongest 9.18% CAGR to 2031.

Page last updated on: