Apparel Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.40 Trillion |

| Market Size (2030) | USD 1.64 Trillion |

| Growth Rate (2025 - 2030) | 3.16% CAGR |

| Fastest Growing Market | South America |

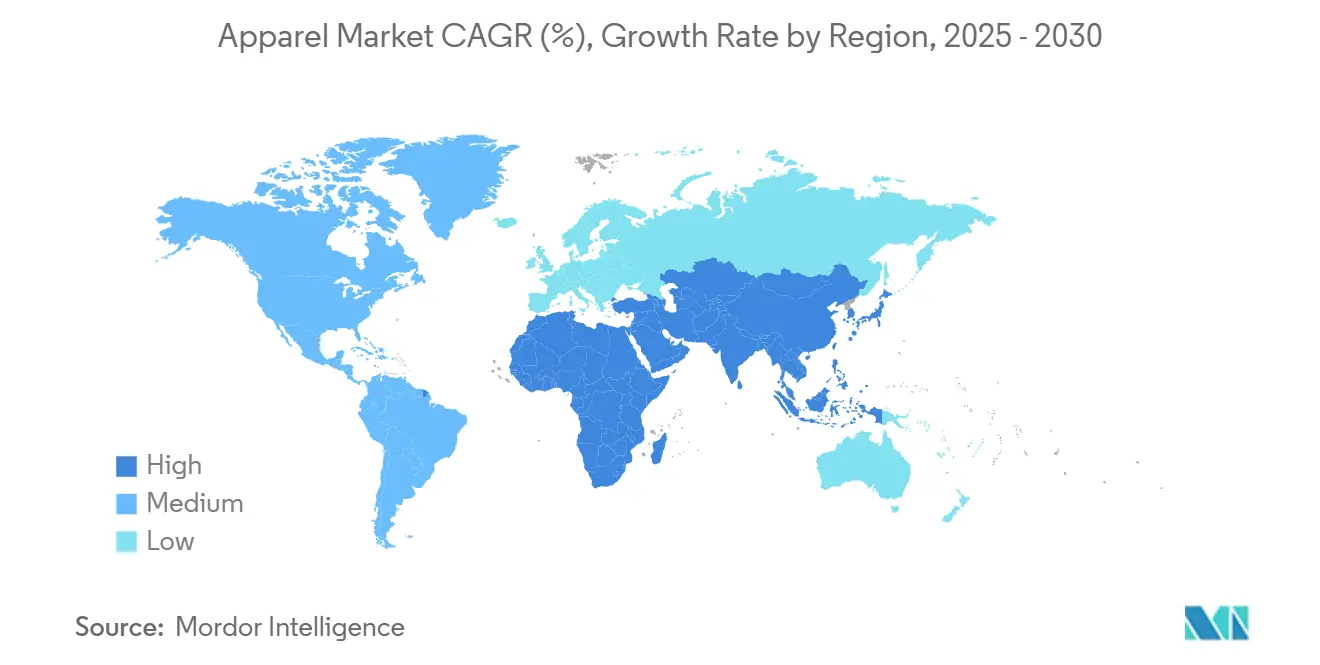

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Apparel Market Analysis by Mordor Intelligence

The global apparel market size is projected to grow from USD 1.40 trillion in 2025 to USD 1.64 trillion by 2030, at a CAGR of 3.16%. The market growth is driven by the recovery in discretionary spending, increased digital adoption, and consumer preference for comfort-oriented clothing, despite inflation affecting purchasing power in developed markets. The younger demographic influences market dynamics by preferring brands that integrate fashionable designs with proven sustainability practices. This has led to increased near-shoring activities, use of recycled materials, and circular economy initiatives, including recycling programs, garment collection, and sustainable packaging. Manufacturers are moving towards environmentally responsible materials while maintaining quality, durability, moisture-wicking capabilities, and color retention. Data-driven merchandising strategies and on-demand manufacturing have shortened production cycles, enhanced inventory management, and reduced markdown losses. These technological advancements enable retailers to forecast consumer preferences, manage stock levels efficiently, and adapt to fashion trends through automated production systems and digital supply chain solutions.

Key Report Takeaways

- By product type, casual wear led with 37.12% revenue share in 2024; sportswear is forecast to expand at a 4.71% CAGR through 2030.

- By end user, women’s apparel commanded 52.31% of the apparel market share in 2024, while children’s apparel records the fastest projected CAGR at 3.09% to 2030.

- By fabric material, cotton accounted for 41.60% of the apparel market size in 2024; Nylon is set to grow at a 5.17% CAGR between 2025-2030.

- By category, the mass segment held 89.12% of 2024 revenue, whereas the premium segment is projected to increase at 5.12% CAGR through 2030.

- By distribution channel, offline stores retained 70.59% share in 2024, yet online stores are rising fastest at a 4.81% CAGR to 2030.

- By geography, Asia-Pacific captured 37.12% of global spending in 2024 and South America is forecast at a 6.01% CAGR, the highest among all regions.

Global Apparel Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Technological innovations in fabric and design | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Sports participation growth | +0.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Social-media-led trend diffusion | +0.5% | Global, stronger in Asia and North America | Short term (≤ 2 years) |

| Globalisation of fashion tastes | +0.3% | Global | Medium term (2-4 years) |

| Sustainability-led purchasing | +0.5% | Europe, North America, emerging in Asia | Long term (≥ 4 years) |

| Gender neutrality and inclusivity | +0.2% | Urban centers worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological innovations in fabric and design

Advanced manufacturing technologies, including artificial intelligence pattern generation, automated cutting, and digital sampling, reduce design-to-prototype cycles from weeks to days. This enables fashion brands to launch smaller collections while minimizing inventory risk. Near-shore manufacturing of small batches reduces freight emissions and allows quick replenishment of popular styles, improving supply chain efficiency. Smart textiles, such as temperature-regulating hoodies and sensor-embedded running shirts, create new revenue streams and enhance profit margins for manufacturers. Fashion companies using machine learning and AI for demand forecasting are seeing significant returns on their technology investments. For instance, Zara integrates artificial intelligence (AI) across its operations to improve efficiency, customer experience, and market position. This technological transformation is notable in the United States and Western Europe, where high labor costs accelerate automation adoption. Production facilities in Vietnam and Indonesia are upgrading their infrastructure with semi-autonomous production lines to maintain their export market competitiveness.

Significant growth in sports participation rate

The global sportswear market experienced significant growth from 2021 to 2024, driven by increased participation in gym activities, running events, and fitness applications. According to data from Sports England, approximately 213,400 people participated in track and field athletics between November 2023 and November 2024, up from 195,900 in 2022-2023.[1]Sport England, "Active Lives Adult Survey November 2023-24", sportengland.org This growth generated higher demand for performance-focused products, including leggings, moisture-wicking shirts, and athletic footwear. The integration of sportswear into everyday clothing expanded its use in workplaces and social settings, increasing overall sales volumes. Athletic brands are partnering with fitness platforms to develop specialized product lines, using consumer data to improve designs and fits. Heritage brands are reintroducing classic athletic styles that appeal to both older consumers and younger generations. The sportswear market is projected to grow faster than the general apparel market through 2029, especially in Asia-Pacific urban centers where health-focused initiatives are increasing. Government initiatives across various countries support this market expansion. In India, the Youth Affairs and Sports Ministry received an allocation of INR 3,794 crore for FY 2025-26, representing a 17% increase from the revised FY 2024-25 allocation. Programs such as Khelo India and Panchayat Yuva Krida Aur Khel Abhiyan (PYKKA) focus on mass participation from athletes in rural areas, infrastructure development, and talent nurturing at the grassroots levels.[2]Ministry of Youth Affairs and Sports, "Welfare and Support Schemes for Sportspersons in India", pib.gov.in

Influence of social media and celebrity endorsements

Social media platforms have transformed fashion retail through short-form videos and live commerce features. Micro-influencers generate immediate increases in product searches, with trend cycles typically lasting three weeks. Fashion companies assess market demand by releasing limited collections through content creators and modifying production based on sales data. Social commerce payment systems have simplified purchasing processes, improving mobile conversion rates. Limited-edition celebrity collaborations, supported by targeted marketing, frequently sell out and appear in secondary markets at premium prices. While viral trends offer growth opportunities, manufacturers need flexible production systems to minimize excess inventory when consumer interest declines. Instagram remains a key digital platform for fashion brands through its visual interface. The platform's features, including Stories, Reels, and IGTV, enable fashion brands to showcase various business elements, from manufacturing processes to fashion shows and styling tutorials. Companies like Zara and H&M operate distinct social media accounts for different countries on platforms like Facebook and YouTube to address specific regional needs.

Globalization of fashion trends

Digital connectivity enables rapid adoption of fashion trends across regions, with styles from major fashion capitals influencing collections globally. International retail chains combine universal wardrobe essentials, including basic t-shirts, denim wear, and formal attire, with localized designs that reflect regional preferences, body types, and cultural elements. Global fashion brands establish design centers in emerging markets to develop market-specific variations of their core products, ensuring better alignment with local consumer preferences and market dynamics. Trade agreements facilitate the development of regional manufacturing networks across multiple countries, reducing dependency on single markets and allowing production closer to consumer demand. For instance, in May 2025, India and the United Kingdom signed a free trade agreement that is expected to increase bilateral trade between the two countries. The agreement includes the removal of tariffs on textile imports from India, which benefits India's apparel industry. This approach helps optimize supply chain efficiency and reduces transportation costs while maintaining product quality.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of Counterfeit Products | -0.4% | Global, with higher impact in Asia and Latin America | Medium term (2-4 years) |

| High Cost Associated With Luxury Brands | -0.3% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Fluctuating Raw Material Prices | -0.2% | Global, with higher impact on mass market segments | Medium term (2-4 years) |

| Supply Chain Disruptions | -0.2% | Europe, North America, with growing influence in Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

Counterfeit products reduce legitimate revenue and damage brand trust, particularly affecting premium brands with high prices and recognizable logos. E-commerce platforms intensify this challenge by enabling sellers to conceal their identities. However, companies now employ advanced image recognition technology and authentication chips with QR codes to help consumers verify product authenticity. Luxury companies collaborate to advocate for enhanced customs enforcement and partner with payment providers to remove unauthorized sellers. Blockchain technology enables tracking of products from raw materials to finished goods, providing verifiable supply chain documentation that is difficult to falsify. Companies implement consumer education programs on identifying authentic products to highlight the value of genuine purchases. The Digital Services Act (DSA), an EU regulation that came into force in November 2022, applies across all EU member states from February 17, 2024. This regulation requires online platforms to actively identify and remove counterfeit products, verify seller identities, and establish illegal content reporting systems. Platforms that fail to comply with these regulations face substantial penalties.[3]European Commission, "Digital Services Act (DSA)", ec.europa.eu

High cost associated with luxury brands

Price differences across markets significantly influence consumer behavior during economic uncertainty, leading to delayed purchases or shifts to lower-priced alternatives. These substantial price variations between regions drive increased grey-market imports, which negatively affect domestic retail performance. In response, luxury brands implement comprehensive uniform global pricing strategies, flexible installment payment options, and enhanced retail experiences with personalized services to maintain their premium positioning. New market entrants in the affordable luxury segment actively compete by offering high-quality products with contemporary modern designs at reduced profit margins. Persistent currency fluctuations create additional complexities and challenges for pricing strategies in major luxury markets, particularly in the Gulf region and East Asia, where exchange rate movements significantly impact purchasing patterns.

Segment Analysis

By Product Type: Comfort-Centric Wardrobes Underpin Steady Demand

Casual wear dominated the market with 37.12% of revenue in 2024, driven by consumer demand for versatile clothing suitable for both work and leisure activities. The sportswear segment is expected to grow at a CAGR of 4.71% (2025-2030), exceeding the overall apparel market growth rate, due to increased fitness participation and athleisure adoption. According to data from Sport England, in 2023-24, approximately 91.4% of children in England participated in sports activities. The Formal Wear segment has adapted through the integration of stretch materials and knit blends that combine professional appearance with comfort. Nightwear and intimate and loungewear segments continue to grow through wellness-oriented offerings and premium material selection. Consumer preferences increasingly favor versatile clothing items that serve multiple purposes, such as polo dresses for office wear and athletic joggers for travel.

Technological advancements enhance product development across segments. Performance features like thermal regulation and anti-odor treatments have expanded from athletic wear into everyday clothing. Manufacturers are implementing modular designs with interchangeable components to reduce inventory complexity while maintaining product variety. Companies using data analytics to track consumer preferences can maintain optimized inventory levels and respond quickly to market trends, helping preserve profit margins in this consumer-driven market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Women's Apparel Dominates While Children's Segment Shows Growth Potential

Women's apparel accounts for 52.31% of global spending in 2024, driven by regular replacement cycles and comprehensive wardrobe requirements. The segment maintains stable volumes during economic downturns through its diverse product range, encompassing business, casual, athletic, and special occasion attire. This product variety serves multiple lifestyle needs, from workplace requirements to recreational activities. The availability of extended sizes up to 6XL broadens market accessibility and provides fitting options across different body types.

The children's apparel segment projects a 3.09% CAGR from 2025 to 2030. Urban parents fuel market growth through increased demand for premium products, including organic cotton materials, skin-safe dyes, and gender-neutral designs. The segment expands as parents prioritize sustainable and safe clothing options for children. The men's apparel market grows through essential wardrobe items, seasonal collections, and direct-to-consumer models that improve fit selection and replenishment. Technology integration in shopping experiences and personalized recommendations increases consumer engagement. The market's expansion into adaptive clothing, with modified designs for mobility-challenged individuals, creates opportunities across consumer groups and demonstrates the industry's focus on inclusive design.

By Fabric Material: Innovation Drives Fiber Portfolio Diversification

Cotton continues to lead the apparel industry with a 41.44% market share in 2024, sustained by its breathability, comfort, and wide consumer acceptance. Enhanced farming practices and processing techniques are strengthening its sustainability profile while maintaining performance. Nylon has emerged as the fastest-growing material, projected to expand at a 5.17% CAGR (2025–2030). Its durability, versatility, and rising adoption in performance wear, coupled with growing investment in recycled and bio-based variants, are positioning it as a key growth driver in the global apparel market.

Polyester and denim retain strong market relevance, supported by the shift toward recycled polyester made from post-consumer plastic waste and sustainable denim technologies that reduce water and chemical usage. Alongside these established fibers, alternatives such as Tencel, hemp, and other bio-based fabrics are steadily gaining traction, reflecting rising sustainability pressures. The industry is also advancing multifunctional textiles with stretch, moisture control, temperature regulation, and antimicrobial features. New entrants, including lab-developed substitutes for animal-based fabrics and textiles from agricultural waste, such as Rethread Africa’s biodegradable materials from sugarcane and corn residues, signal a structural transformation in material sourcing and innovation.

By Category: Mass Market Dominates vs. Premium Growth

The mass category holds a 89.12% market share in 2024, dominating through economies of scale and broad market accessibility. This segment operates on high volume, rapid turnover, and competitive pricing, with market leaders distinguished by efficient supply chains and quick adaptation to trends. The premium segment projects a higher growth rate at 5.12% CAGR (2025-2030), supported by consumer demand for quality products, durability, and brand reputation, with growth driven by social media influence, globalization, and increased disposable income.

The distinction between mass and premium segments continues to blur as mass-market brands develop premium offerings and luxury brands introduce more accessible product lines. This convergence has created a significant middle market segment that balances quality and design with moderate pricing. Both segments show increased focus on brand values and purpose, as consumers base purchasing decisions on corporate ethics and sustainability practices. The premium segment particularly demonstrates a transition from visible luxury to conscious consumption, where heritage, craftsmanship, and environmental responsibility justify higher prices.

By Distribution Channel: Omnichannel Redefines Retail Roles

Offline stores hold a dominant 70.59% market share in 2024, demonstrating the continued significance of physical retail locations despite digital advancement. This market leadership stems from consumers' preference for direct product interaction and immediate purchases, with most retail transactions still occurring in physical stores. Online stores exhibit stronger growth potential with a 4.81% CAGR (2025-2030), supported by enhanced convenience, broader product selection, and improved digital shopping experiences.

Retailers are implementing integrated omnichannel approaches that combine physical and digital platforms to enhance customer experience. Key operational improvements include integrated inventory management systems, AI-based product recommendations, and flexible pickup options such as buy-online-pickup-in-store (BOPIS). Physical stores are transitioning from traditional retail spaces to interactive showrooms, incorporating technologies like smart mirrors and augmented reality (AR) fitting solutions. This integration creates a retail environment where physical and digital channels function as interconnected components of a unified customer experience across multiple platforms.

Geography Analysis

Asia-Pacific remains the largest apparel market, accounting for 37.12% of global revenue in 2024, supported by rising urban incomes and government-led textile innovation clusters. China dominates demand, while India, Indonesia, and Vietnam are witnessing double-digit growth in online apparel purchases. Manufacturing is steadily shifting from coastal China to Bangladesh and Cambodia to optimize costs and manage tariff risks, while Southeast Asian markets continue to scale social-commerce platforms that integrate shopping with entertainment.

South America stands out as the fastest-growing region, forecast to expand at a 6.01% CAGR through 2030. Growth is driven by a young consumer base, increasing digital adoption, and rising demand for affordable yet fashionable apparel. Expanding e-commerce penetration and localized production strategies are also accelerating market uptake, making the region a key opportunity for global and regional brands alike.

North America and Europe maintain strong positions, underpinned by established retail infrastructure and mature consumer preferences. Both regions are integrating experiential formats with digital channels, while consumer decisions increasingly prioritize sustainability, transparency, and ethical sourcing alongside style and price. Europe is additionally benefiting from easing inflation and higher tourism-driven retail activity. Circular economy initiatives, particularly resale and rental models, are gaining momentum in both regions, especially among younger consumers, further reshaping traditional retail dynamics.

Competitive Landscape

The global apparel market features moderate concentration and major players focus on product innovation and business model evolution. Companies invest in sustainable materials and manufacturing processes while creating collections that reflect evolving consumer preferences. Digital transformation remains essential, with brands expanding their omnichannel presence and implementing AR, VR, and AI technologies to improve customer experiences. Brand development and market expansion rely on partnerships with celebrities, designers, and digital influencers. Companies are growing their geographic presence through online and offline channels, particularly in emerging markets. The industry focuses on supply chain optimization and logistics improvements to reduce time-to-market and enhance inventory management.

The clothing industry maintains a fragmented structure, comprising global conglomerates and specialized regional players operating across various price segments and product categories. Global corporations such as VF Corporation, Nike Inc., H&M Group, Fast Retailing Co. Ltd. (Uniqlo) and Adidas AG control significant market share through diverse brand portfolios and extensive retail networks. Regional players maintain strong local positions through market expertise and targeted product offerings. The market experiences ongoing consolidation through mergers and acquisitions, especially in luxury and premium segments, as companies expand their portfolios and improve operational efficiency.

Direct-to-consumer brands and digital-first companies continue to transform traditional retail models. Established companies respond by acquiring emerging brands and technology firms to enhance digital capabilities and reach younger consumers. The industry demonstrates increased collaboration between luxury and streetwear brands, reflecting diminishing boundaries between market segments and the growing importance of casual wear trends.

Apparel Industry Leaders

-

VF Corporation

-

H&M Group

-

Fast Retailing Co. Ltd. (Uniqlo)

-

Nike Inc.

-

Adidas AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zara opened a flagship store at The Grove in Los Angeles, California. The expansion is a part of Zara's expansion strategy in the U.S. market, which combines establishing new locations with upgrading existing stores.

- June 2025: H&M launched its first shop-in-shop at Galeries Lafayette Paris Haussmann. The 63-square-meter space on the children's floor features the premium label H&M Adorables. This marks H&M's first department store presence in France. H&M Adorables offers children's clothes and accessories designed for durability.

- March 2025: Trent Ltd's apparel and lifestyle retailer Westside expanded its presence by opening three new stores in Jodhpur, Jaipur, and Chennai. The Jaipur store spans 31,641 square feet, while the Jodhpur and Chennai stores cover 25,602 square feet and 26,000 square feet, respectively.

- February 2025: Adidas AG launched the A-Type collection under its Adidas Originals lifestyle brand. The collection includes leather Firebird tops, pants, and shorts, along with two cashmere-blend regular-fit T-shirts designed for everyday wear.

Global Apparel Market Report Scope

Apparel includes all kinds of clothes in different styles and fabrics.

The global apparel market is segmented by end-users into men, women, and children. By type, the market is segmented into formal wear, casual wear, sportswear, nightwear, and other types. The market is also segmented by geography into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report offers the market sizes and forecasts in terms of value (USD) for all the above segments.

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear/Loungewear |

| Intimate |

| Other Product Types |

| Men |

| Women |

| Children |

| Cotton |

| Polyester |

| Nylon |

| Denim |

| Other Fabric Types |

| Mass |

| Premium |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Formal Wear | |

| Casual Wear | ||

| Sportswear | ||

| Nightwear/Loungewear | ||

| Intimate | ||

| Other Product Types | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Fabric Material | Cotton | |

| Polyester | ||

| Nylon | ||

| Denim | ||

| Other Fabric Types | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Apparel Market?

The apparel market size is expected to reach USD 1.40 trillion in 2025 and grow at a CAGR of 3.16% to reach USD 1.64 trillion by 2030.

Who are the key players in Apparel Market?

PVH Corp., Inditex, Kering S.A., LVMH and Aditya Birla Group are the major companies operating in the apparel market.

Which is the fastest growing region in Apparel Market?

South America is the fastest-growing region in the apparel market, projected to expand at a 6.01% CAGR through 2030, driven by rising digital adoption, a young consumer base, and growing demand for affordable fashion.

Which product type segment has the biggest share in Apparel Market?

In 2024, casual wear accounts for the 37.41% share in Apparel Market.

Page last updated on: