Anti-retroviral Drugs Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 32.92 Billion |

| Market Size (2031) | USD 40.14 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

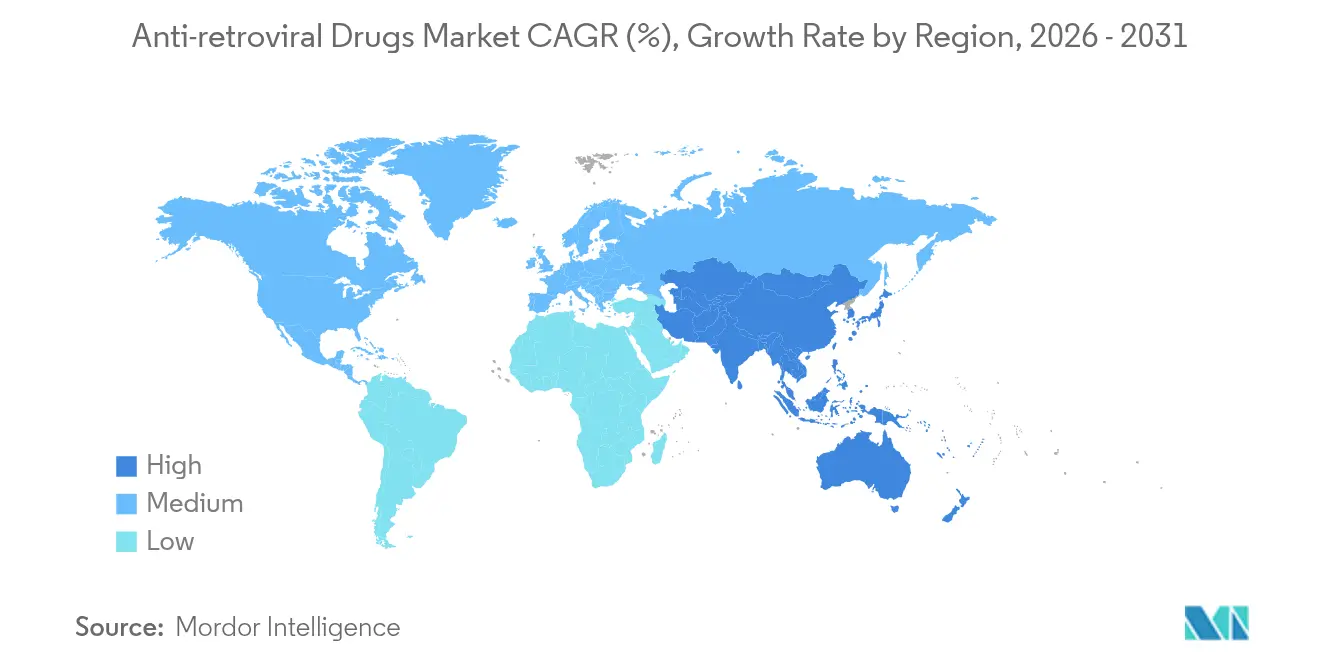

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

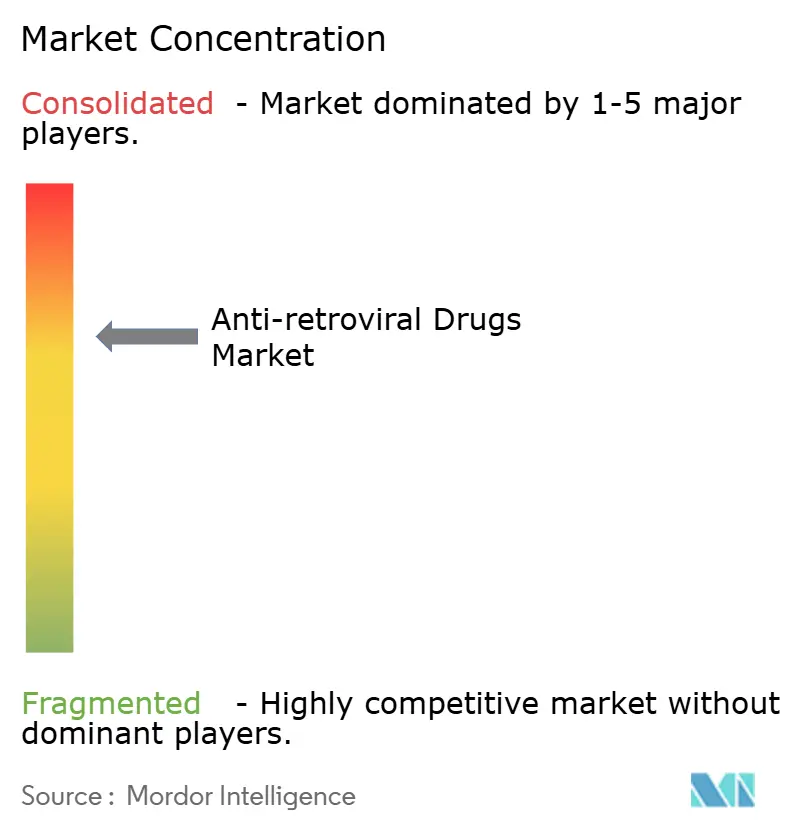

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-retroviral Drugs Market Analysis by Mordor Intelligence

The anti-retroviral drugs market size is expected to grow from USD 31.64 billion in 2025 to USD 32.92 billion in 2026 and is forecast to reach USD 40.14 billion by 2031 at 4.05% CAGR over 2026-2031. This measured pace marks a transition from earlier rapid scale-up to a mature phase where innovation, differentiated access strategies and supply-chain resilience steer growth. Long-acting injectables, once-weekly oral regimens and ultra-durable prophylaxis strengthen adherence and open new prevention segments, while integrated primary care delivery and digital adherence tools broaden therapeutic reach. Competitive intensity is rising as blockbuster patents approach expiry, prompting both branded lifecycle extensions and aggressive generic positioning. At the same time, donor financing, tiered-pricing frameworks and local manufacturing investments continue to anchor demand in low- and middle-income countries, which account for almost all new infections.

Key Report Takeaways

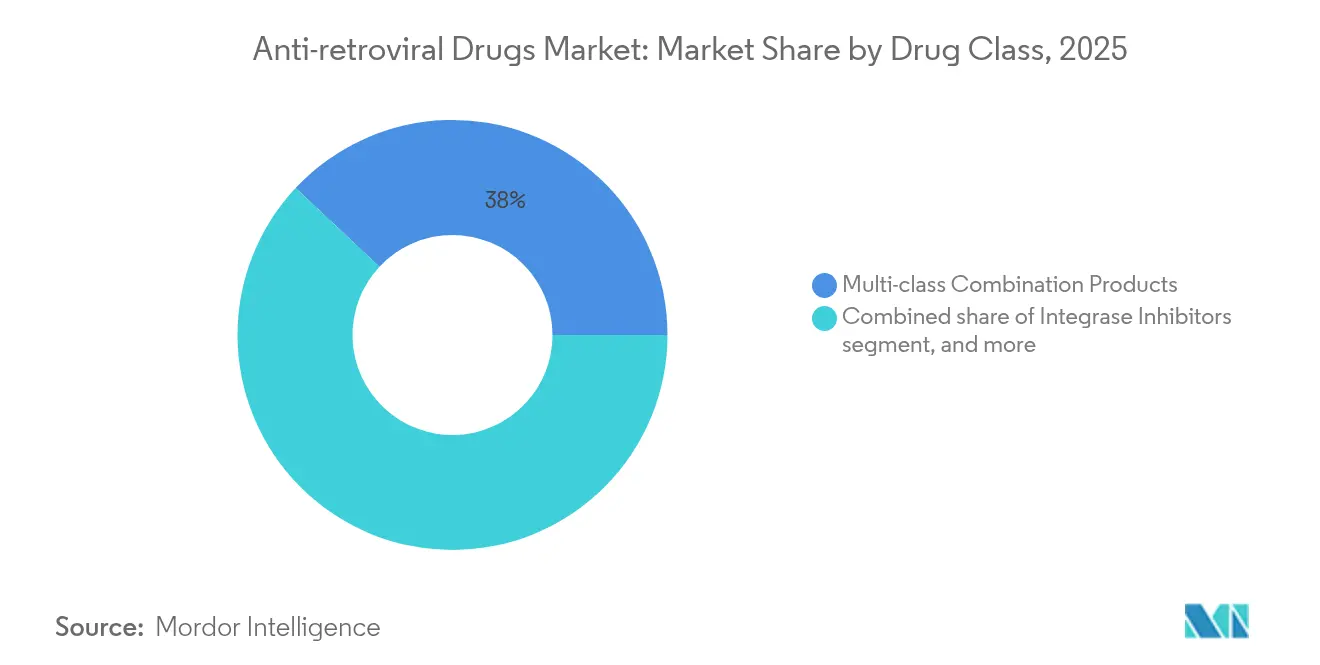

- By drug class, multi-class combination products held 38.02% of the anti-retroviral drugs market share in 2025, and integrase inhibitor-based combinations are advancing at a 6.28% CAGR through 2031.

- By regimen type, single-tablet regimens captured 51.78% of the 2025 anti-retroviral drugs market size, while long-acting injectables are growing fastest at 6.63% CAGR.

- By line of therapy, first-line therapy constituted 54.12% of total revenue in 2025; second-line therapy is expanding at a 6.31% CAGR on the back of rising resistance-driven switches.

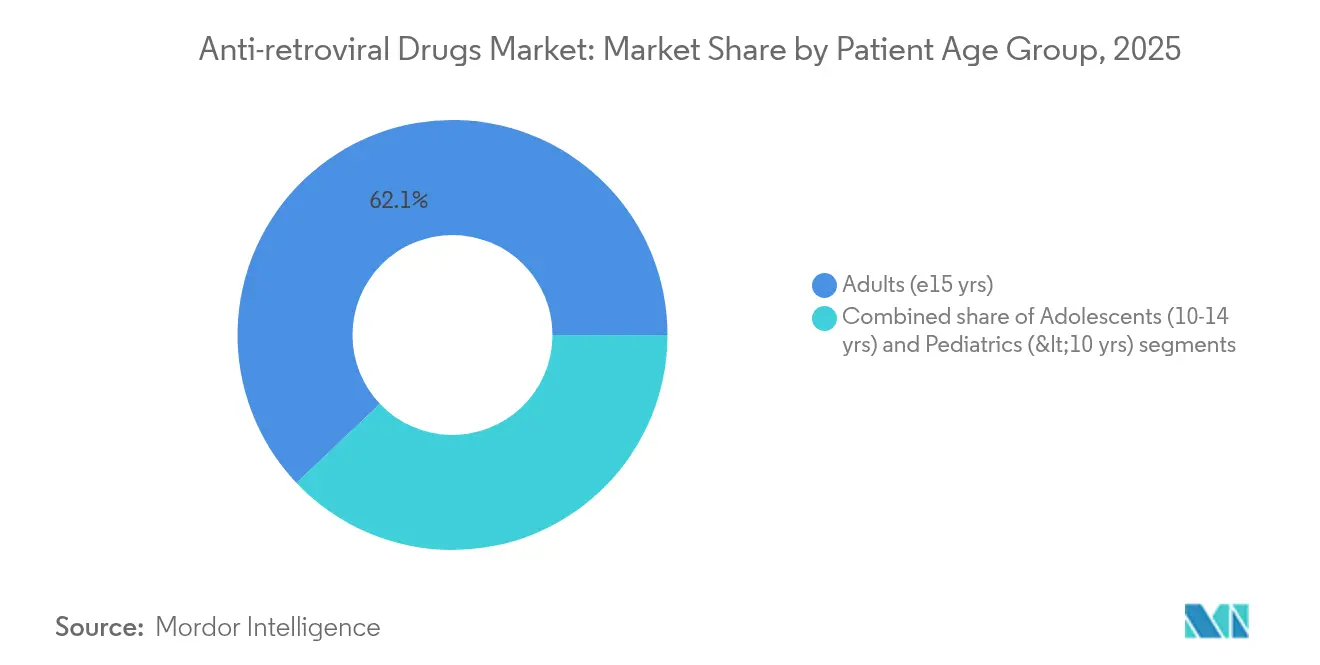

- By patient age group, adolescents aged 10-14 years contributed 7.41% CAGR, the strongest rate among all patient cohorts, in the anti-retroviral drugs market.

- By distribution channel, hospital pharmacies distributed 61.12% of total volumes in 2025 and are projected to lead growth at 7.22% CAGR as hubs for injectables and comprehensive HIV care.

- By region, North America retained 41.95% revenue share in 2025, yet Asia-Pacific registers the fastest regional trajectory at 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-retroviral Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global HIV prevalence and treatment coverage expansion | +1.2% | Sub-Saharan Africa, Eastern Europe, Central Asia | Long term (≥ 4 years) |

| Enhanced public and donor funding for universal ART access | +0.8% | Sub-Saharan Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Ongoing R&D of novel long-acting therapies | +0.6% | North America, Europe, spill-over to LMICs | Medium term (2-4 years) |

| Growing integration of ART within primary healthcare platforms | +0.4% | Sub-Saharan Africa, Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Expansion of digital adherence technologies and remote monitoring | +0.3% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Accelerated regulatory pathways for pediatric ART formulations | +0.2% | Global, priority in high-burden countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global HIV Prevalence and Treatment Coverage Expansion

HIV programmes now target the 33% of people living with the virus who remain untreated, a cohort concentrated in emerging Europe, Central Asia and parts of Latin America. Growing middle-income country budgets, combined with tiered-pricing structures, push the anti-retroviral drugs market into regions where per-capita spending potential is higher than historical Sub-Saharan averages. As more adults age with HIV, comorbidity-tolerant regimens with fewer renal and bone risks gain traction, sustaining volume even where incidence is falling. Universal test-and-treat policies, championed by WHO, keep first-line demand resilient, while scaled viral-load monitoring identifies failure earlier and lifts second-line uptake. These dynamics collectively reinforce a broad base of recurring demand across all lines of therapy[1]World Health Organization, “Global HIV Facts 2025,” WHO.int.

Enhanced Public and Donor Funding for Universal ART Access

The Global Fund’s USD 9.2 billion 2024-2026 allocation underwrites multi-year procurement and strengthens supply chains in 70 countries, anchoring predictable demand for suppliers. PEPFAR’s pivot toward country co-financing spurs national budget lines and invites direct manufacturer-government contracts that shorten cash-flow cycles. Advance purchase commitments and voluntary licences, such as Gilead’s lenacapavir agreement covering 120 countries, encourage earlier generic ramp-up while protecting inventor margins through royalty structures. Collectively, blended finance mechanisms shield the anti-retroviral drugs market from donor fatigue in the medium term, although future macroeconomic stress in high-income donor nations remains a watch-list risk[2]The Global Fund, “Results Report 2024–2025,” Theglobalfund.org.

Ongoing Research and Development of Novel Long-Acting Therapies

FDA clearance of lenacapavir in June 2025 validated the ultra-long-acting paradigm and has accelerated follow-on pipelines. Merck and Gilead’s once-weekly oral lenacapavir-islatravir combination posted 94.2% Week-48 viral suppression, while ViiV Healthcare’s N6LS antibody moves toward pivotal studies aiming for infrequent subcutaneous dosing. Manufacturing complexities—sterile suspension, large-volume depot packaging, cold-chain integrity—create barriers that insulate incumbents, yet present capacity challenges that have triggered more than USD 3 billion in announced injectable plant investments in the United States and Europe since 2024. These innovations rejuvenate pricing headroom in mature Western markets and broaden prevention reach in high-burden regions, although cost-containment constraints temper uptake in low-income settings.

Growing Integration of ART With Primary Healthcare Delivery Platforms

Differentiated service models shift dispensing from specialist clinics toward community health centres where multi-month scripts reduce clinic visits and congested urban facilities. Six-month refills, pioneered during COVID-19, now constitute the default for stable patients in several Sub-Saharan programmes, freeing system capacity and lowering patient travel costs. Task-shifting empowers nurses and community health workers to initiate therapy, expanding initiations in remote districts once underserved by physicians. These shifts reward fixed-dose single-tablet regimens and long-acting injectables that obviate daily adherence concerns. Pharmaceutical field teams are retooling to support training, cold-chain logistics and remote pharmacovigilance, embedding deeper within primary care structures[3]Journal of Global Health Reports, “Six-Month ART Dispensing Evaluation,” Joghreports.org.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent drug resistance and viral mutations | –0.7% | Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Long-term safety concerns and adverse effects | –0.5% | Global, particularly ageing cohorts | Medium term (2-4 years) |

| Supply-chain vulnerabilities in API sourcing | –0.4% | India, China, Sub-Saharan Africa | Short-to-medium term (≤ 4 years) |

| Price erosion from generic competition and reference pricing | –0.3% | North America, Europe, selected LMIC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Drug Resistance and Viral Mutations

WHO surveillance shows dolutegravir resistance of 3.9-8.6% in treatment-naïve patients and 19.6% in those previously exposed, pushing payers toward higher-cost salvage regimens. Resistance testing gaps in low-resource settings mask emerging multi-class failures and complicate guideline updates. The additional laboratory and second-line drug costs strain donor budgets and national insurance schemes, while patent-protected rescue therapies further elevate spend. For suppliers, rising resistance reshapes portfolio priorities toward agents with higher genetic barriers and multimodal modes of action, thereby raising R&D budgets and trial complexity.

Long-Term Safety Concerns and Adverse Effects

As half of people on therapy will soon be over 50 years, renal, cardiovascular and metabolic complications of earlier nucleoside backbones create a growing switch market to safer agents. Real-world neuropsychiatric events with integrase inhibitors and lipid elevations with certain protease inhibitors spark monitoring guidelines that favour regimens requiring fewer ancillary lab tests. Pregnancy safety databases remain limited for most new agents, necessitating post-marketing commitments that heighten pharmacovigilance costs. These concerns modestly dampen growth by encouraging prescriber caution and by extending regulatory review times for first-in-class molecules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Multi-class Combinations Accelerate Treatment Durability

Multi-class combination pills preserved 38.02% revenue in 2025 through simplified dosing and high resistance barriers that support first-line durability. Integrase inhibitor-anchored regimens posted a 6.28% CAGR, the strongest within this class, propelled by once-daily bictegravir- or dolutegravir-based backbones that maintain ≥85% suppression in heavily pre-treated cohorts. Nucleoside reverse transcriptase inhibitors remain a mainstay despite historic bone and renal signals; reformulated tenofovir alafenamide mitigates these risks and extends franchise life. Protease inhibitors continue niche use for boosted salvage regimens but decline as metabolic concerns prompt clinician preference shifts. Novel entry inhibitors and broadly neutralising antibodies, including China’s pending albuvirtide, add pipeline diversity but must demonstrate cost-effectiveness to gain guideline prominence.

Integrase-driven durability and once-daily simplicity help this class capture incremental share from NNRTIs, whose vulnerability to single-point mutations curtails uptake. The anti-retroviral drugs market size for integrase-based combinations is projected to surpass USD 18.64 billion by 2031, reflecting sustained clinical confidence and expanding label indications. Yet, manufacturers must prepare for generic erosion after 2031 as key patents lapse, pressuring them to introduce next-generation boosters or ultra-long-acting depot versions to protect value.

By Regimen Type: Long-Acting Injectables Redefine Convenience

Single-tablet regimens dominated 2025 sales but face heightened competition from depot injections that eliminate daily adherence barriers. The anti-retroviral drugs market share of single-tablet regimens is supported by broad payer familiarity and streamlined distribution, yet their growth moderates to low-single digits as adherence-challenged cohorts pivot to injectables. Long-acting CAB-RPV posted initial uptake in high-income settings, and lenacapavir’s six-month dosing interval sets a new convenience benchmark that could shift payer mix toward specialty pharmacy channels.

Implant technologies remain investigational but present disruptive potential, especially for prevention in high-burden youth populations. Manufacturing scale-up for injectables introduces supply-chain fragilities—cold-chain breaks, device shortages—that suppliers must mitigate through dual-site production and buffer inventory. The anti-retroviral drugs market size dedicated to long-acting modalities is expected to register USD 6.12 billion by 2031 at a 6.63% CAGR, with early commercial success hinging on provider training incentives and reimbursement codes for administration services.

By Line of Therapy: Second-Line Uptake Mirrors Resistance Patterns

First-line regimens continued to command over 54% of 2025 revenue due to universal test-and-treat protocols, yet rising transmitted resistance pushes earlier switches. The anti-retroviral drugs market size attributed to second-line therapy is projected to reach USD 12.86 billion by 2031, expanding 6.31% annually as genotypic testing becomes more accessible and as WHO guidelines recommend rapid cycling after confirmed failure. Third-line or salvage regimens remain specialised but lucrative, with multi-drug rescue cocktails commanding premiums that can exceed USD 6,000 per patient-year in middle-income countries, underscoring affordability challenges.

Successful “test and treat” strategies lengthen patient lifespans, generating cumulative revenue across multiple therapy lines. However, payers increasingly require resistance-guided justification before approving expensive salvage regimens, favouring products that bundle companion diagnostics or offer outcomes-based contracts tied to suppression benchmarks.

By Patient Age Group: Adolescent Needs Drive Formulation Innovation

Adults ≥15 years still generate 62.08% of spending, yet the 10-14 year adolescent bracket grows fastest at 7.41% CAGR as paediatric cohorts age. Care transitions expose historical adherence gaps and complex resistance patterns, stimulating demand for chewable dispersible tablets and game-based adherence support. Tivicay PD and abacavir / lamivudine dispersible fixed doses illustrate early responses, but portfolio breadth remains limited, giving first movers extended market exclusivity. The anti-retroviral drugs market size for paediatric formulations stood at USD 1.65 billion in 2025 and will approach USD 2.54 billion by 2031 as regulators fast-track child-friendly options.

Ageing adult patients produce new pharmacokinetic challenges as polypharmacy becomes routine. Dose adjustments and once-weekly monitoring add service costs but extend therapy duration, smoothing revenue even as incident infections decline in some high-income regions.

By Distribution Channel: Hospitals Emerge as Integrated Care Hubs

Hospital pharmacies kept 61.12% share in 2025 and accelerate at 7.22% CAGR, reflecting their expanding role in administering depot injections, conducting resistance testing and coordinating comorbidity management. Online pharmacies also contribute to channel diversification, growing 5.41% CAGR, but regulatory scrutiny over controlled-substance e-prescribing tempers broader expansion. NGO and donor supply chains remain indispensable in Sub-Saharan markets, but nascent local manufacturing and direct shipment models begin to reduce lead times and buffer stockouts. The anti-retroviral drugs market share transitioning through direct-to-patient delivery will double by 2030, aided by mobile apps that schedule home refills and automated pill dispensers that monitor adherence in real-time.

Hospital-based integrated HIV centres combine pharmacy, counselling and laboratory services and are poised to capture incremental revenue from procedure codes linked to injectable administration, pay-for-performance bundles and telehealth follow-ups. This integrated approach synergises with digital adherence platforms to lock in patient loyalty to specific provider networks.

Geography Analysis

North America commanded 41.95% of anti-retroviral drugs market revenue in 2025, benefiting from early access to breakthrough designations and insurance coverage that routinely reimburses USD 25,000-30,000 per patient-year. Lenacapavir’s FDA approval underscores the region’s innovative pull, yet looming patent cliffs for bictegravir (2036) and dolutegravir (2031) invite price erosion and generic challenges. Payer negotiations emphasise outcomes-based discounts, pushing innovators to supply real-world evidence of sustained suppression and improved adherence.

Europe follows with a robust albeit slower growth trajectory. Harmonised HTA frameworks foster simultaneous multi-country launches, while manufacturing investments such as Eli Lilly’s USD 2.5 billion German injectable complex highlight the continent’s role in global supply security. Cost-effectiveness thresholds drive aggressive tendering, particularly in Central and Eastern Europe, where lenacapavir may compete against lower-cost generics post-2028. EU pandemic-era joint procurement experience informs regional pooled purchasing that could reshape seller pricing power.

Asia-Pacific delivers the fastest regional CAGR at 6.86%, led by China and India, which together house 3.6 million people living with HIV. China’s epidemiology now skews toward heterosexual transmission and older age groups, boosting demand for comorbidity-compatible regimens. Domestic champions scale up antibody and long-acting injectables, while the Belt and Road “health silk road” fosters exports across Africa. India leverages its dominant generic base; companies such as Laurus Labs expanded HIV API capacity 27% CAGR in FY23, supporting both local therapy scale-up and international donor tenders.

Sub-Saharan Africa remains volume-centric, absorbing more than half of global treatment courses, yet donor reliance flattens value growth. Enhanced primary-care integration and six-month multi-dispensing blunt per-patient revenue, but expanding coverage lifts absolute market size. South America and Eastern Europe experience resurgent incidence, offering niche growth but confronting diverse reimbursement and IP landscapes, as demonstrated by Colombia’s compulsory dolutegravir licence that sliced procurement costs by 90%.

Competitive Landscape

The anti-retroviral drugs market is moderately concentrated; the top five suppliers generated roughly 75% of global sales in 2025. Gilead commands 64% of its corporate revenue from HIV therapeutics and continues to invest in long-acting portfolios to offset anticipated patent expiry revenue dips. ViiV Healthcare leverages cabotegravir to strengthen its injectable franchise and pursues voluntary licences to pre-empt compulsory actions in LMICs. Janssen extends its integrase line through lifecycle studies in comorbidity sub-populations, while Merck co-develops once-weekly oral regimens to diversify risk.

Strategic alliances shape pipeline dynamics: Gilead and Merck share platform technologies for lenacapavir-islatravir, and ViiV partners with Aurobindo, Cipla and Viatris for cabotegravir access manufacturing. Real-world evidence platforms that track adherence and suppression now feature in tender evaluations, favouring companies with comprehensive digital support suites. Meanwhile, Chinese entrants like Frontier Biotech prepare to scale albuvirtide internationally, signaling future pricing competition in fusion inhibitor niches.

Anti-retroviral Drugs Industry Leaders

Gilead Sciences, Inc.

ViiV Healthcare (GlaxoSmithKline plc, Pfizer, Shionogi)

Janssen Pharmaceuticals (Johnson & Johnson)

Merck & Co., Inc.

AbbVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA approved lenacapavir (Yeztugo) as the first twice-yearly injectable PrEP, reporting 100% efficacy across 5,000 trial participants in South Africa and Uganda.

- February 2025: Gilead secured FDA priority review for lenacapavir based on PURPOSE studies showing superiority to daily Truvada.

- October 2024: ViiV Healthcare pledged to triple annual supply of long-acting cabotegravir for LMIC markets.

- September 2024: Fidson Healthcare announced a USD 100 million Nigerian plant under China’s “health silk road” to localise ARV production.

- January 2024: Health Canada granted priority review to cabotegravir long-acting prevention, positioning Canada as the first injectable PrEP market in the Americas.

- October 2023: Pharmascience began a USD 120 million sterile injectable expansion in Quebec to triple capacity by 2026.

Global Anti-retroviral Drugs Market Report Scope

As per the scope of the report, anti-retroviral drugs are medications for treating infection by retroviruses, primarily HIV. A retrovirus is a group of viruses that belongs to the family Retroviridae, and they characteristically carry their genetic blueprint in the form of ribonucleic acid (RNA). The anti-retroviral drugs hinder the multiplication of these viruses rather than killing them. The Anti-Retroviral Drug Market is Segmented by Drug Class (Protease Inhibitors, Integrase Inhibitors, Multi-class Combination Products, Nucleoside Reverse Transcriptase Inhibitors (NRTIs), Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs), and Other Drug Class) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Protease Inhibitors |

| Integrase Inhibitors |

| Multi-class Combination Products |

| Nucleoside Reverse Transcriptase Inhibitors (NRTIs) |

| Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs) |

| Entry & Fusion Inhibitors |

| Other Drug Class |

| Single-Tablet Regimens (STRs) |

| Multi-pill Oral Regimens |

| Long-Acting Injectables |

| Implants & Depot Formulations |

| First-Line |

| Second-Line |

| Salvage / Third-Line |

| Adults (≥15 yrs) |

| Adolescents (10-14 yrs) |

| Pediatrics (<10 yrs) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| NGO / Donor Supply Chains |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Protease Inhibitors | |

| Integrase Inhibitors | ||

| Multi-class Combination Products | ||

| Nucleoside Reverse Transcriptase Inhibitors (NRTIs) | ||

| Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs) | ||

| Entry & Fusion Inhibitors | ||

| Other Drug Class | ||

| By Regimen Type | Single-Tablet Regimens (STRs) | |

| Multi-pill Oral Regimens | ||

| Long-Acting Injectables | ||

| Implants & Depot Formulations | ||

| By Line of Therapy | First-Line | |

| Second-Line | ||

| Salvage / Third-Line | ||

| By Patient Age Group | Adults (≥15 yrs) | |

| Adolescents (10-14 yrs) | ||

| Pediatrics (<10 yrs) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| NGO / Donor Supply Chains | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the anti-retroviral drugs market and how fast is it expanding?

The market generated USD 32.92 billion in 2026 and is forecast to reach USD 40.14 billion by 2031, advancing at a 4.05% CAGR.

Which product category is expected to deliver the fastest growth through 2031?

Long-acting injectables lead with a 6.63% CAGR as twice-yearly options such as lenacapavir reshape both treatment and prevention paradigms.

Which region holds the largest revenue share, and which region is growing quickest?

North America commanded 41.95% of 2025 sales, while Asia-Pacific is projected to post the highest regional CAGR at 6.86% through 2031.

How are long-acting therapies likely to change treatment models for providers and payers?

Depot injections eliminate daily pill burden, shift dispensing toward hospital pharmacies for administration services and open the door to outcomes-based reimbursement tied to measured adherence.

What are the principal challenges that could limit market momentum over the next five years?

Rising drug-resistance rates that already reach up to 19.6% in treatment-experienced patients and lingering safety concerns in ageing cohorts together subtract about 1.2 percentage points from forecast CAGR.

How concentrated is the competitive landscape and what does this mean for new entrants?

The top five manufacturers control roughly 75% of global revenue, so newcomers will need niche innovations or strategic alliances to secure meaningful share.

Page last updated on: