Brazil Fisheries And Aquaculture Market Analysis by Mordor Intelligence

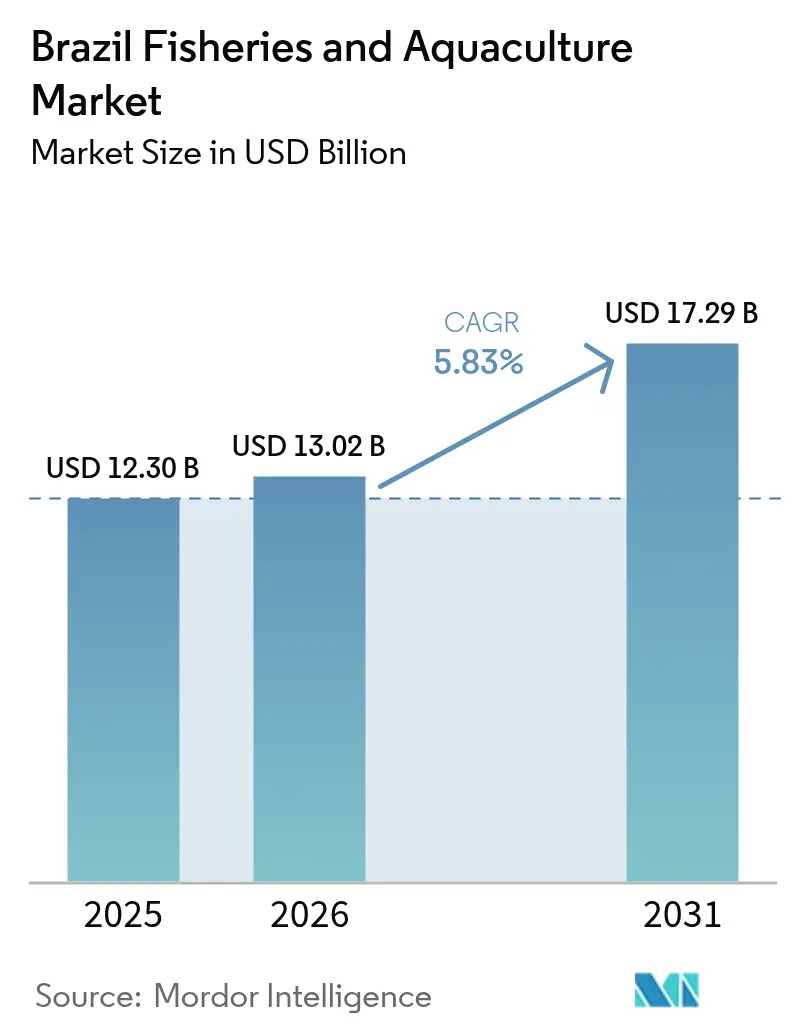

The Brazil fisheries and aquaculture market size is expected to grow from USD 12.3 billion in 2025 to USD 13.02 billion in 2026 and is forecast to reach USD 17.29 billion by 2031 at 5.83% CAGR over 2026-2031. Export-oriented tilapia farming has gained significant traction following the removal of the Import Health Certificate by the United States in October 2024. This policy change resulted in a 138% increase in farmed fish exports, reaching USD 59 million within a year, and facilitated access to premium retail channels in North America for Brazilian producers [1]Source: United States Department of Agriculture, “Import Health Certificate Requirements,” usda.gov. Government-supported biosecurity subsidies have reduced the capital requirements for recirculating aquaculture systems, enabling mid-sized cooperatives to adopt advanced technologies that were previously unaffordable. Rising real wages in urban centers across Southeast and South Brazil have driven an increase in per-capita fish consumption, which rose to 12 kilograms in 2025 from 9 kilograms in 2020, as health-conscious consumers increasingly substitute red meat with aquatic protein. Tilapia remains the dominant species in production, primarily through industrial cage culture in Paraná reservoirs. Meanwhile, Vannamei shrimp is experiencing the fastest growth, supported by biofloc systems that recycle nitrogenous waste and lower feed costs by 20%. Despite these advancements, challenges such as feed price volatility, currency fluctuations, and gaps in disease surveillance continue to hinder market growth. Regulatory developments, including federal offshore zoning and blockchain-based traceability systems, are creating new revenue opportunities and are projected to reshape the Brazil fisheries and aquaculture market by 2030.

Key Report Takeaways

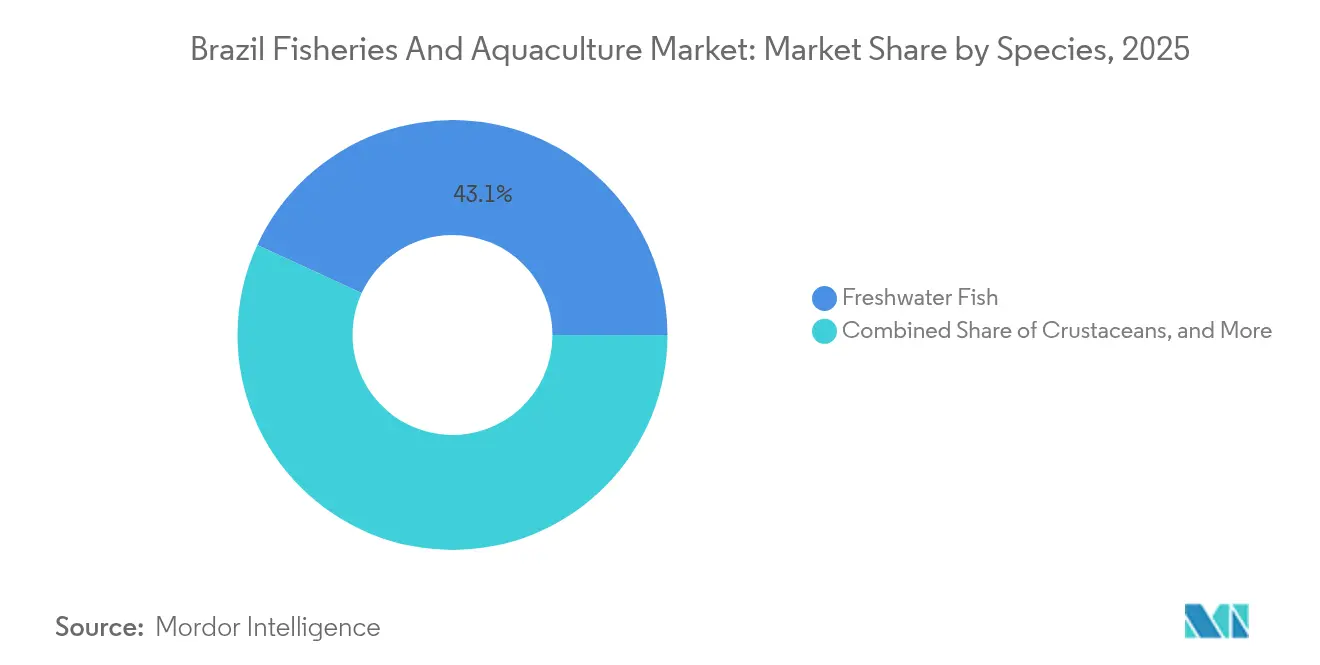

- By species, Freshwater Fish led with 43.12% of Brazil fisheries and aquaculture market size in 2025, while Crustaceans are forecast to grow at 12.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Fisheries And Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Domestic Seafood Demand | +1.5% | National, strongest in Southeast and South urban centers | Long term (≥ 4 years) |

| Government-Backed Biosecurity Subsidies | +1.2% | National, with higher uptake in Southeast, South, and Central-West | Short term (≤ 2 years) |

| Gradual Phase-Out of Wild-Catch Quotas | +1.0% | National, most pronounced in Southeast and South coastal zones | Medium term (2-4 years) |

| Mandatory Farm Bio-Floc Upgrades | +0.8% | National, concentrated in Northeast and Central-West high-density pond zones | Medium term (2-4 years) |

| Blockchain-Based Traceability Pilots | +0.4% | Southeast urban centers (São Paulo, Rio de Janeiro) with early retail adoption | Long term (≥ 4 years) |

| Offshore Cage Zoning Around Islands | +0.3% | South (Santa Catarina coast) and Northeast (Bahia islands) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Domestic Seafood Demand

Rising real wages in Southeast and South urban centers are pushing per-capita fish intake toward 12 kilograms annually by 2030, up from 9 kilograms in 2020, as health-conscious middle-class households substitute red meat with protein-rich aquatic species. This dietary shift is underpinned by government nutrition programs that distribute fish to public schools in North and Northeast regions, normalizing aquatic protein among younger demographics and creating a consumption base that will persist into adulthood. Retail chains such as Carrefour and Pão de Açúcar expanded chilled-seafood shelf space by 20% in 2024, introducing private-label tilapia and shrimp products that undercut branded offerings by 15% while maintaining comparable quality through direct contracts with cage-culture cooperatives. The strategic implication is that domestic demand is transitioning from a price-sensitive, commodity-driven market toward a segmented landscape where convenience, health attributes, and traceability command differentiated pricing, creating white space for producers who can deliver consistent quality and transparent supply chains.

Government-Backed Biosecurity Subsidies

The Ministry of Agriculture's PescAgro program allocated BRL 1.5 billion (USD 300 million) in soft loans for 2024 and 2025, targeting capital expenditures for biosecure hatcheries, recirculating aquaculture systems, and energy-efficient aeration equipment. Interest rates are capped at 6% per annum with 10-year amortization schedules, materially below the 14% commercial lending rate prevailing in Brazilian agricultural credit markets. This subsidy reduces the payback period for a 500-ton-per-year RAS facility from 8 years to 5 years, making intensive land-based systems economically viable for mid-sized cooperatives that previously relied on extensive pond culture. The strategic implication is that government credit is catalyzing a two-tier industry structure, with subsidized operators adopting closed-loop systems that minimize environmental discharge while unsubsidized farms face mounting pressure to comply with tightening effluent standards.

Gradual Phase-Out of Wild-Catch Quotas

Federal environmental agencies are implementing gradual reductions in wild-catch quotas for coastal species such as sardines, mackerel, and grouper, aiming to restore overfished stocks that declined by 30% between 2010 and 2020. These quota cuts shift demand toward farmed tilapia and shrimp, which now supply over 70% of domestic seafood consumption compared to 55% in 2020. The transition is most pronounced in Southeast and South coastal zones, where artisanal fishers are receiving government incentives to transition into aquaculture cooperatives, leveraging their local ecological knowledge to manage cage-culture systems in estuaries and reservoirs. The strategic insight is that quota reductions are accelerating aquaculture's displacement of wild-capture fisheries, yet they also create niche opportunities for producers who can farm pelagic species in offshore cage systems, a technology frontier that remains underdeveloped in Brazil despite favorable oceanographic conditions along the 7,400-kilometer coastline.

Mandatory Farm Bio-Floc Upgrades

Federal Decree 10.987/25 mandates biofloc technology upgrades for high-density pond operations exceeding 20 metric tons per hectare, requiring producers to install aeration systems, mechanical filters, and microbial inoculants that recycle nitrogenous waste into protein-rich flocs, which are consumed by fish and shrimp. Compliance costs average USD 50,000 per hectare, a barrier that disproportionately impacts small-scale operators in the Northeast and Central-West regions who lack access to subsidized credit[2]Source: Empresa Brasileira de Pesquisa Agropecuária, “Biofloc and Genetic Advances,” embrapa.br. Biofloc systems reduce feed costs by 20% and enable stocking densities to double without expanding pond footprints, delivering payback periods of 3 to 4 years for producers who achieve operational proficiency. The strategic implication is that the mandate is consolidating the industry around operators with scale and technical expertise, while simultaneously improving environmental performance and reducing the sector's vulnerability to feed-price volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Salinity Operating Costs | -0.8% | National, most acute in Central-West and Northeast inland shrimp farms | Short term (≤ 2 years) |

| Scarce Hatchery Broodstock Lines | -0.7% | National, constraining Vannamei shrimp and native species expansion | Medium term (2-4 years) |

| Dependence on Imported Feed | -1.0% | National, exposing all producers to foreign-exchange volatility | Short term (≤ 2 years) |

| Aquaculture Disease Surveillance Gaps | -0.9% | National, most severe in Southeast and South intensive cage-culture zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Salinity Operating Costs

Inland shrimp farms in the Central-West and Northeast regions require desalination systems to achieve salinity levels of 15 to 25 parts per thousand, consuming 8 to 12 kilowatt-hours per cubic meter of water, which increases operating expenses by over 22% compared to coastal estuarine ponds. Electricity tariffs averaged 12% annual increases between 2022 and 2024 as Brazilian utilities passed through higher natural-gas and hydroelectric opportunity costs, eroding gross margins below 10% for small and mid-sized operators who lack scale to negotiate industrial power contracts. Producers are exploring solar photovoltaic installations to offset daytime electricity demand, but the upfront capital requirement of USD 100,000 for a 100-kilowatt array deters investment unless additional subsidies or power-purchase agreements are in place that guarantee feed-in tariffs. The strategic implication is that inland shrimp farming faces a cost ceiling that will limit geographic expansion unless renewable energy subsidies or biofloc technology can reduce desalination intensity.

Scarce Hatchery Broodstock Lines

Limited imports of specific-pathogen-free Vannamei shrimp broodstock throttle stocking density improvements, with Brazilian hatcheries relying on fewer than 10 certified genetic lines compared to 40-plus lines available in Ecuador and Thailand. Import restrictions imposed in 2024 to prevent the introduction of Tilapia Lake Virus and White Spot Syndrome Virus have inadvertently constrained genetic diversity, reducing the disease resistance and feed-conversion efficiency gains that international breeding programs deliver. Domestic breeding programs at Embrapa and GeneSeas are developing native broodstock lines, these efforts require 5 to 7 years to achieve performance parity with imported genetics, creating a near-term bottleneck that limits shrimp production growth to 12.5% annually, despite strong export demand. The strategic insight is that genetic constraints are capping productivity improvements across multiple species, underscoring the need for public-private partnerships that accelerate domestic breeding programs while managing biosecurity risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Tilapia Dominance Masks Diversification Gains

Freshwater Fish led with 43.12% of Brazil fisheries and aquaculture market size in 2025, anchored by industrial-scale cage-culture operations in Paraná reservoirs that leverage hydroelectric infrastructure and feed-conversion ratios of 1:4:1 to compete with Asian exporters. Genetic selection programs at Embrapa have reduced grow-out cycles to 6 months in tropical climates and improved disease resistance to Streptococcus agalactiae, enabling stocking densities above 100 kilograms per cubic meter in cage systems. Pelagic species, such as sardines, mackerel, tuna, and barracuda, remain predominantly wild-caught, yet they face price inflation exceeding 15% annually as federal quota reductions aim to restore overfished stocks.

Crustaceans are forecast to grow at a 12.32% CAGR through 2031, driven by biofloc technology that recycles nitrogenous waste into microbial protein and reduces feed costs by 20%, enabling Northeast producers to intensify stocking densities above 150 post-larvae per square meter without expanding pond footprints. Vannamei shrimp, notably lobster, represent niche segments with high profitability but limited production volumes due to long grow-out cycles of 18 to 24 months and capital-intensive hatchery requirements . The strategic implication is that Brazil's aquaculture sector is transitioning from a tilapia monoculture toward a diversified portfolio that balances high-volume, low-margin staples with high-margin niche species, a risk-management strategy that insulates producers from synchronized shocks to any single species.

Geography Analysis

The Southeast region, anchored by Paraná's 180,000 metric tons of annual tilapia production from cage-culture systems in hydroelectric reservoirs and by São Paulo's role as the primary consumption hub for both domestic and imported seafood. Paraná's dominance reflects a convergence of favorable factors, including stable water quality in the Itaipu and Salto Caxias reservoirs, proximity to feed mills and processing facilities, and a cooperative structure exemplified by C.Vale, which integrates hatchery, grow-out, and cold-chain logistics under a single governance model. São Paulo's metropolitan area, with 22 million residents, drives demand for fresh tilapia and shrimp through supermarket chains such as Carrefour and Pão de Açúcar, which expanded chilled-seafood shelf space by 20% in 2024.

The region's growth is tempered by recurring Streptococcus outbreaks that forced emergency harvests in late 2024, depressing farm-gate prices by 19% and exposing the vulnerability of high-density cage systems to synchronized disease shocks. Blockchain traceability pilots launched by Carrefour in São Paulo and Rio de Janeiro are capturing affluent households willing to pay 15% premiums for verified antibiotic-free status, creating a differentiated revenue stream that offsets commodity-price volatility.

Santa Catarina's offshore mariculture pilots, initiated in 2024, are trialing cobia and Atlantic salmon in open-sea net pens positioned 5 kilometers from the coast, a strategic initiative to diversify beyond freshwater species and to capture premium pricing for marine finfish that currently must be imported. Federal decree 11.203/25 unlocked 500 hectares of offshore cage zoning around Santa Catarina and Bahia islands, enabling producers to circumvent land-use conflicts with coastal tourism and mangrove conservation restrictions. The South region's 6.51% forecast growth through 2031, the slowest among all geographies, reflects land-use constraints and environmental licensing requirements that limit pond expansion, pushing producers toward intensive, technology-driven systems that require higher capital investment

Regulatory Landscape

Brazilian fisheries and aquaculture regulation is tightening around origin documentation, quota management, and federal frameworks that lower financing costs for compliant producers. In April 2026, the Ministry of Fisheries and Aquaculture (MPA) and the Ministry of Agriculture and Livestock (MAPA) published Interministerial Ordinance No. 54/2026, defining the Nota Fiscal do Pescado as the official document of origin for fish, which is now the paperwork base used in inspections and traceability across the chain.

Fisheries management continues to be shaped by interministerial quota setting and monitoring. In February 2026, the MPA and the Ministry of Environment and Climate Change (MMA) established capture quotas for the 2026 tainha (Mugil liza) season via an interministerial ordinance, reinforcing stock-based controls alongside official monitoring panels. On the aquaculture side, June to July 2026 included a policy package centered on the Plano Nacional de Desenvolvimento Sustentavel da Aquicultura (PNDSA, 2026-2036) and the Plano Safra 2026/2027 credit lines for the sector, with production financing rates announced at 2% per year and microcredit as low as 0.5%, linking modernization and expansion investments to federal programs.

Value Chain Analysis

Brazil's fisheries and aquaculture value chain spans broodstock and hatcheries, feed and health inputs, grow-out (ponds, cages in reservoirs, and emerging offshore/union-waters operations), processing, cold-chain logistics, and retail and export channels. The chain is increasingly formalized through digital and documentary controls, including the 2026 move to recognize the Nota Fiscal do Pescado as the official origin document and MPA efforts to expand sector databases and modernize catch and production monitoring (for example, the PesqBR application launched in Piauí in July 2026 for artisanal fishing data capture). For aquaculture, subsidized credit under federal programs (including Plano Safra 2026/2027 and earlier PescAgro lines) supports hatchery biosecurity upgrades, aeration, and recirculating systems, enabling mid-sized producers and cooperatives to invest in higher-control production.

Key bottlenecks remain concentrated in inputs and health management. Feed is a dominant cost driver in intensive systems, while disease surveillance gaps and limited access to specific-pathogen-free broodstock constrain productivity improvements in shrimp and some finfish segments. Public R&D and extension activity is increasingly targeted at these pain points: in May 2026, Embrapa Pesca e Aquicultura released a technical protocol for tilapia production in Tocantins aimed at reducing feed use without compromising growth, and in June 2026 it validated a GIS-based sanitary-risk mapping protocol with Italy's IZSVe to manage disease propagation between farms within the same watershed. Downstream, processing and value addition (filleting, chilled distribution, and traceability-linked retail programs) are expanding alongside demand in major urban centers and export-oriented tilapia supply chains.

Market Opportunities and Future Outlook

Policy-driven formalization and cheaper capital create room for professionalized producers to document origin, meet sanitary controls, and scale processing and technology adoption. The PNDSA launched by the MPA in June 2026 sets a 10-year framework (2026-2036) focused on sustainability and sector modernization, while Plano Safra 2026/2027 reduced sector financing rates to 2% per year (and down to 0.5% for microcredit), improving the business case for upgrades such as biosecure hatcheries, aeration, and RAS where licensing and compliance are workable. In parallel, recognition of the Nota Fiscal do Pescado as the official origin document (Interministerial Ordinance No. 54/2026) supports traceability-heavy routes to market, including premium domestic retail programs and export procurement that require auditable documentation.

Opportunities also extend beyond whole-fish sales into processing, circular economy by-products, and technology-enabled farm management that improves survivability and feed conversion under volatile input costs. In May 2026, Codevasf and UFMA inaugurated a facility in Sao Luis, Maranhao, backed by a reported R$ 1 million investment, to convert fish waste (skin, bones, scales) into higher-value inputs such as collagen and oils for pharma and cosmetics, showing how processors can monetize residuals. On-farm, the shift toward digital tools and applied R&D, including Embrapa protocols on feed efficiency and watershed-level disease risk mapping, supports adoption of precision practices that reduce losses in intensive systems. Export-oriented producers also have scope to adjust market exposure as trade conditions change, with a higher contribution from processed formats (for example, fillets) tied to consistent quality and chain-of-custody documentation.

Recent Industry Developments

- June 2026: The Ministry of Fisheries and Aquaculture (MPA) launched the Plano Nacional de Desenvolvimento Sustentavel da Aquicultura (PNDSA) and the Rede PROAQUI, establishing a 10-year national framework (2026-2036) for sector modernization. The plan puts regulatory simplification, productivity, and sustainability at the center of federal coordination, giving producers a clearer programmatic umbrella to align licensing, technical assistance, and investment agendas.

- October 2025: The MPA published its 2024 Aquaculture Bulletin, reporting that aquaculture production in Union Waters grew 20% versus 2023, reaching 148,564.71 tonnes with a gross production value (VBP) of R$ 1.26 billion. The update reinforces the strategic importance of federally managed waters as a scaling pathway for farmed fish volumes and for projects that depend on standardized monitoring and licensing.

- October 2024: The United States Department of Agriculture eliminated the Import Health Certificate requirement for Brazilian fish, removing a non-tariff barrier affecting shipments to North American retail channels. Export-oriented tilapia producers benefited from easier market access, supporting a sharp increase in farmed fish export value over the subsequent year.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the value generated from Brazil's fisheries and aquaculture output, covering farmed and captured aquatic products traded into domestic use and external trade. Values are expressed in USD to keep the view consistent across periods.

Scope exclusions: We exclude upstream inputs like equipment, feed, and medicines, and we also exclude unrelated seafood retail markups that sit outside producer and trade value tracking.

Segmentation Overview

- By Species (fresh only)

- Pelagic Fish

- Sardines

- Mackerel

- Tuna

- Barracuda

- Demersal Fish

- Grouper

- Trevally

- Emperor

- Pomfret

- Freshwater Fish

- Tilapia

- Crustaceans

- Shrimp (Vannamei)

- Lobster

- Mollusks

- Scallop

- Oyster

- Other Species

- Pelagic Fish

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the official supply and trade trail so the model has a clean factual base. We relied on public sources such as FAO FishStat, UN Comtrade, Brazilian trade statistics from MDIC, IBGE production and price series, and MAPA publications on aquaculture and sanitary rules. Where available, we also used peer-reviewed fisheries and aquaculture journals to sense check species level dynamics and farming system shifts.

To fill gaps that public tables do not cover well, we cross checked with company annual reports, investor presentations, and reputable press coverage on harvest cycles, export mixes, and pricing changes. Select paid subscriptions were used mainly for structured company financials and news screening, and a shipment level import export database was used selectively to validate trade direction and unit values. These desk sources are not exhaustive, and many other public documents were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work helped anchor the desk model in day to day operating behavior, particularly on species pricing, farm gate versus first sale value, and how output is routed to exports versus domestic buyers. We spoke with a mix of producers, processors, traders, associations, and logistics and cold chain participants across major producing states, then we rechecked key assumptions with demand side voices such as distributors and foodservice focused buyers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | |

| Mid tier: 56% | Functional/Unit leaders: 30% | |

| Smaller Players: 15% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built using a top down reconstruction, where production volumes by key species groups and the related trade flows are converted into value using observed price trends and unit values. Because fisheries and aquaculture can swing with seasons and biology, the model uses a mix of indicators such as harvested volumes (metric tons), export and import values and volumes, average unit values by product form, feed cost direction as a pressure on farm pricing, and domestic consumption pull as reflected in supply availability and trade balances.

Results are then checked with selective bottom up approximations, including sampled ASP times volume calculations for major species and channel checks on how first sale prices move versus export pricing. When local gaps exist, such as missing prices for a smaller species group, we use proxy unit values from close substitutes and then adjust them after expert feedback. For forecasting, we use scenario analysis supported by trend based smoothing on the main input series, and then we align the forward path with what industry participants expect for capacity additions, disease and biosecurity conditions, and export market access changes.

Data Validation & Update Cycle

Before numbers are finalized, outputs are triangulated against independent signals such as export unit value movements, production growth consistency, and the implied domestic availability after net trade. If a variance looks unusual, we revisit the source series, recheck conversions, and, in some cases, reconnect with respondents to confirm whether the shift is structural or temporary.

A multi step internal review follows so assumptions, calculations, and year on year movements are easy to trace. The report is refreshed annually, and interim updates are made when material events occur, such as regulation changes affecting farming approvals or sudden export demand shifts. Right before delivery, we do a fresh pass on the latest public releases so clients receive the most current view we can support.

Mordor Intelligence's Brazil Analysis of Fisheries and Aquaculture Sector Market Size Compared Against Other Published Estimates

Published market values for Brazil fisheries and aquaculture often do not match because the market is not defined the same way, and some studies lean more on retail spend while others stay closer to production and trade value. Differences also show up when exchange rate timing, the choice of base year, and the way prices are projected are handled differently.

The main gap comes from mixing retail seafood sales with sector value, where Mordor Intelligence treats the market as fisheries and aquaculture value linked to production, consumption balance, and import export flows, instead of counting consumer retail selling price layers and taxes. Another driver is how species and product form are handled, since some estimates use broad seafood categories while others track species groups and unit value trends more tightly. Finally, refresh cadence matters because export volumes, unit values, and policy driven access conditions can move meaningfully within a year, which then shifts the near term baseline.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.3 B (2025) | |

| Global Consultancy A | USD 12.8 B (2024) | Uses a different base year and a faster growth path, and the public summary does not clearly show how export unit values, domestic price pass through, and species level mix are validated year by year. |

| Trade Data Publisher B | USD 7.37 B (2022) | Values seafood at retail selling price and includes taxes across retail categories, which is a narrower demand side view and not directly comparable to a fisheries and aquaculture sector value built from production and trade signals. |

The spread in the table is mainly explained by whether the number is closer to sector value creation or closer to retail seafood spending, and by how base years and currency timing are set. Our approach stays traceable to measurable variables like production volume, net trade, and unit value trends, which makes the final total easier to replicate and explain when assumptions are challenged.

Key Questions Answered in the Report

How fast will the Brazil fisheries and aquaculture market grow to 2031?

It is projected to expand at a 5.83% CAGR, rising from USD 13.02 billion in 2026 to USD 17.29 billion in 2031.

Which species shows the highest growth potential?

Vannamei shrimp leads with a 12.32% annual growth forecast thanks to biofloc ponds that reduce feed costs by 20%.

What role does PescAgro financing play?

Soft loans, capped at 6% interest, shorten the payback period for intensive systems to five years and fund biosecure hatcheries and energy-efficient aeration systems.

Why is blockchain traceability important?

QR code labels enable shoppers to verify farm biosecurity and antibiotic status, earning 15% price premiums and facilitating entry into European markets.

Page last updated on: