Alternating Current (AC) Electric Drives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.12 Billion |

| Market Size (2031) | USD 22.6 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

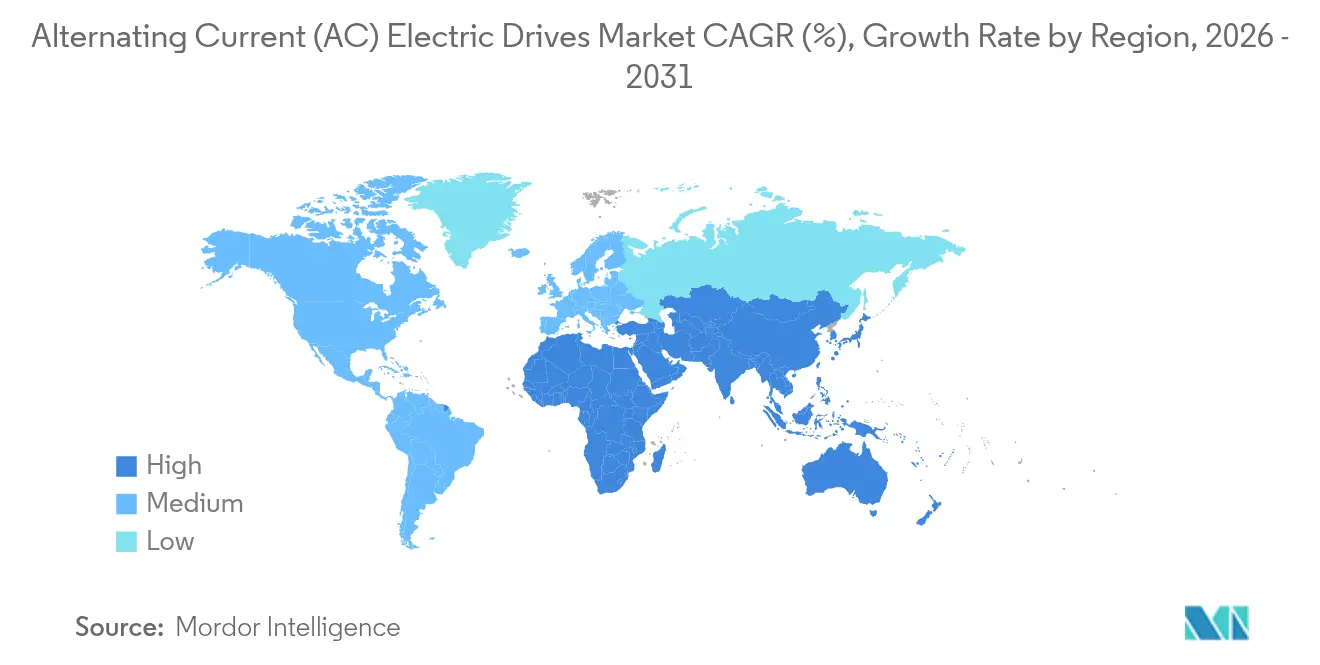

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alternating Current (AC) Electric Drives Market Analysis by Mordor Intelligence

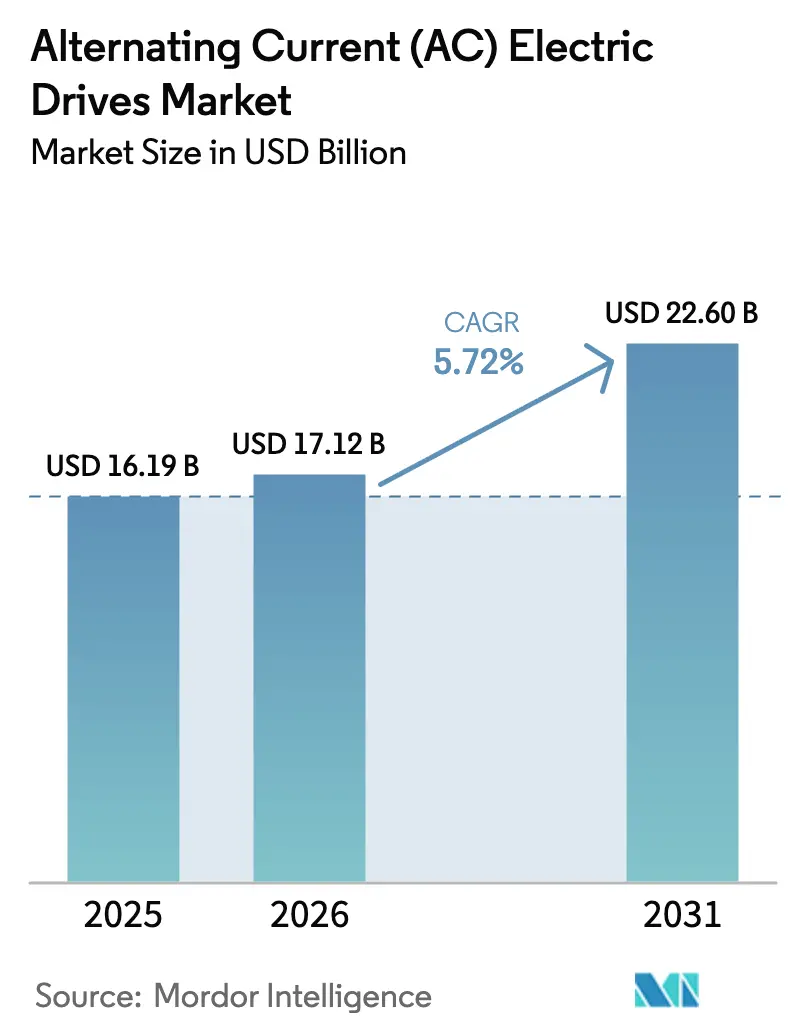

The AC electric drives market size was valued at USD 16.19 billion in 2025 and estimated to grow from USD 17.12 billion in 2026 to reach USD 22.6 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Robust factory automation programs, tightening global efficiency mandates, and falling power-electronics costs underpin this expansion. Manufacturers are migrating from fixed-speed starters to variable-speed architectures to reduce electricity bills that already account for more than 30% of operating expenses in motor-intensive plants. Volatile energy prices magnify the payback advantage, while digital control loops embedded in modern drives shorten commissioning cycles and improve uptime through predictive analytics. Semiconductor makers have reduced the cost per kilowatt of insulated-gate bipolar transistor (IGBT) modules, allowing vendors to incorporate premium features into smaller frame sizes. Parallel demand arises from commercial buildings, where variable-speed compressors, fans, and pumps enable owners to comply with green-building certifications while meeting rising comfort expectations.

Key Report Takeaways

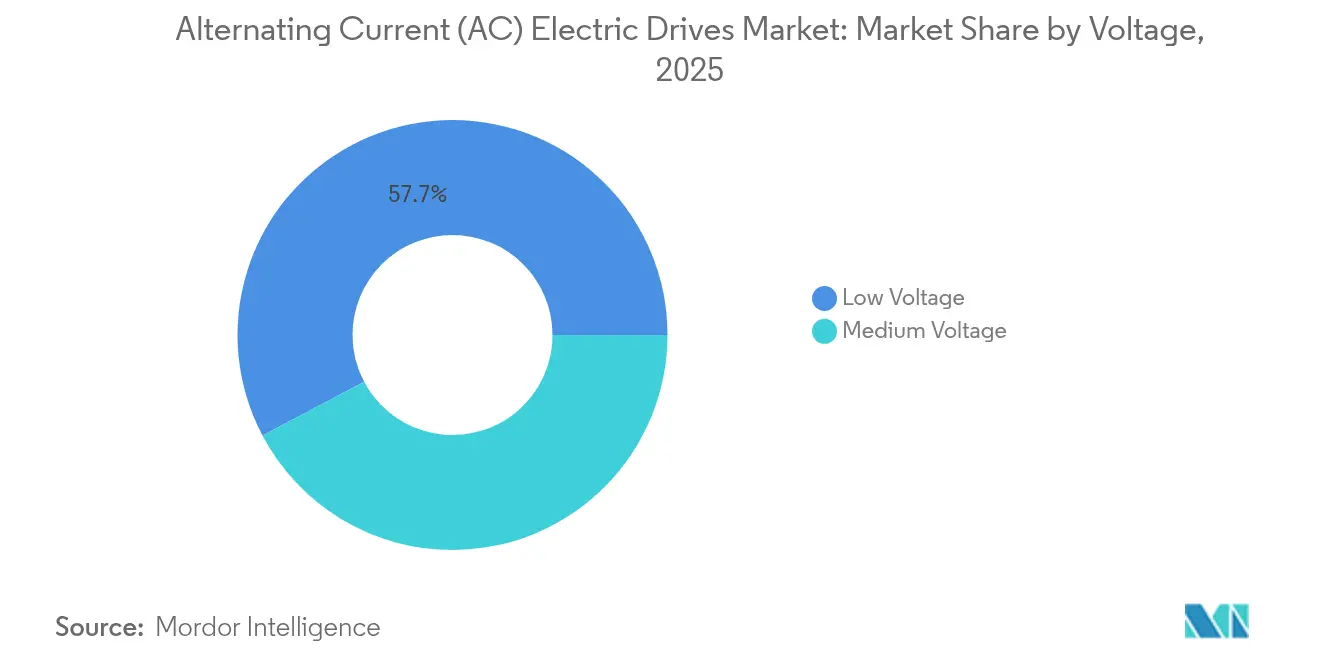

- By voltage, low-voltage systems held 57.74% of the AC electric drives market share in 2025, whereas medium-voltage units are projected to grow at a 7.52% CAGR to 2031.

- By power rating, the up to 1 MW segment accounted for 47.10% of the AC electric drives market size in 2025, while drives above 3 MW are projected to grow at a 7.26% CAGR through 2031.

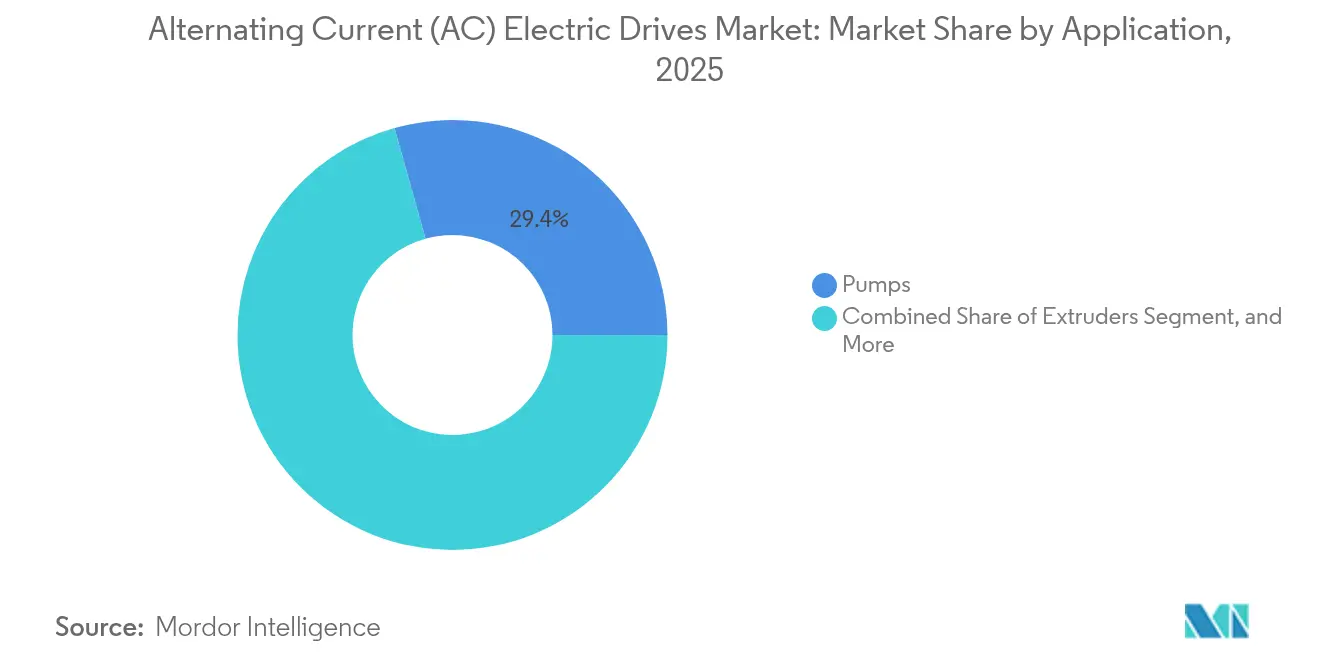

- By application, pumps led with a 29.35% revenue share in 2025; extruders represent the fastest-growing segment with a 6.18% CAGR through 2031.

- By end-user industry, the oil and gas sector retained 23.05% of the revenue in 2025, while HVAC systems are poised for a 6.05% CAGR through 2031.

- By geography, the Asia-Pacific region commanded 35.29% of 2025 revenue, and the Middle East is expected to register the fastest 6.62% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alternating Current (AC) Electric Drives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing automation in manufacturing industries | +1.8% | Global with Asia-Pacific core and spill-over to North America and Europe | Medium term (2-4 years) |

| Rising government regulations and demand for energy-efficient devices | +1.5% | Global with EU and North America leadership | Long term (≥4 years) |

| Declining cost per kilowatt of high-power IGBT modules | +1.2% | Global manufacturing impact with China and Germany leadership | Short term (≤2 years) |

| Rapid expansion of HVAC installations in commercial buildings | +0.9% | North America and EU primary, Asia-Pacific emerging | Medium term (2-4 years) |

| Integration of AC drives with IIoT platforms for predictive maintenance | +0.8% | Global with advanced manufacturing regions leadership | Long term (≥4 years) |

| Surge in variable-frequency drive retrofits in aging industrial plants | +0.7% | North America and Europe mature markets, selective Asia-Pacific adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Automation in Manufacturing Industries

Smart-factory investments accelerate the adoption of AC electric drives in the market because executives view energy-efficiency gains as decisive cost levers. ABB released the ACS8080 medium-voltage platform in November 2024, which runs at 98% efficiency while cutting harmonic distortion by 50%.[1]ABB Ltd., “ABB launches next-generation medium-voltage drive,” abb.com Variable-speed retrofits on fans alone reduce electricity use by up to 30%, freeing up the budget for further automation upgrades. Real-time data transmitted from drives to plant historians supports predictive quality control and reduces unplanned downtime. Governments in China, India, and Indonesia incentivize robotics through tax credits, thereby broadening the addressable installed base for intelligent drives.

Rising Government Regulations and Demand for Efficient Devices

Minimum-energy-performance standards now govern roughly two-thirds of global motor shipments.[2]International Energy Agency, “World Energy Outlook 2023,” iea.org The European Union's Eco-design Directive and the United States Department of Energy's rules require factories to demonstrate quantifiable savings, making AC electric drives' market penetration virtually mandatory in new build lines. The share of electric power in final energy consumption is projected to rise from 29% in 2022 to 52% by 2050, intensifying scrutiny of every motor-driven system. Utilities also reward demand-response participation, allowing facilities equipped with variable-speed drives to monetize flexible load capacity.

Rapid Expansion of HVAC Installations in Commercial Buildings

Heat-pump capacity targets grow from 1.3 TWth in 2021 to 9,000 GW in 2030.[3]International Renewable Energy Agency, “World Energy Transitions Outlook 2024,” irena.org Each new compressor typically ships with a drive to modulate output in line with hourly thermal loads. Property developers specify variable-speed air-handling units to meet LEED, BREEAM, or WELL certification requirements, resulting in steady structural demand. Controls teams integrate drives with building management systems, enabling algorithms that reduce peak demand charges and automate indoor air quality compliance.

Declining Cost per Kilowatt of High-Power IGBT Modules

Wide-bandgap silicon carbide wafers reduce conduction losses by as much as 70%, enabling manufacturers to minimize the size of heat sinks and cabinets. Between 2020 and 2022, SiC MOSFET price points fell 11% and the premium to silicon narrowed to roughly 2.5-3×. Compact footprints unlock retrofit opportunities in space-restricted process plants, propelling the adoption of medium-voltage solutions across pulp and paper, steel rolling, and desalination assets. Vendors channel savings into integrated condition-monitoring sensors, widening the digital value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial installation and maintenance costs | -0.8% | Global with higher impact in emerging markets and SME segments | Short term (≤2 years) |

| Shortage of skilled technicians for drive programming and tuning | -0.7% | Global with acute shortages in advanced manufacturing regions | Long term (≥4 years) |

| Supply chain volatility in semiconductor components affecting lead times | -0.6% | Global with higher impact on European and North American manufacturers | Short term (≤2 years) |

| Harmonics and power-quality concerns limiting adoption | -0.5% | Global with stricter grid codes in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Installation and Maintenance Costs

Total installed cost includes engineering, harmonic-filter banks, cooling upgrades, and operator training, sometimes reaching 2-3× the drive list price. Smaller firms defer projects when payback exceeds two fiscal years. In retrofit scenarios, rewiring panels and verifying power-quality compliance further inflate budgets. Service teams must periodically replace DC-link capacitors and fan assemblies, creating unfamiliar lifecycle obligations for maintenance departments accustomed to simple starters.

Shortage of Skilled Technicians for Drive Programming and Tuning

The U.S. automation ecosystem requires an estimated 870 new mid-skill technicians annually to keep pace with increasing equipment complexity. Drive commissioning demands knowledge of vector control algorithms, fieldbus protocols, and harmonic mitigation techniques. Europe’s REBOOT SKILLS initiative had delivered 1,302 specialized certifications by May 2025, yet vacancy rates remained elevated. Staffing constraints delay plant upgrades, pushing end users toward turnkey service contracts that increase the total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Medium-Voltage Drives Narrow the Gap with Low-Voltage Leaders

Low-voltage units captured the lion’s share of 57.74% in 2025 because most industrial motors draw less than 690 V. However, project developers are consolidating loads, preferring one 4 MW motor over four 1 MW units to simplify maintenance. The AC electric drives market now observes medium-voltage quotations rising at a 7.52% CAGR through 2031, as petrochemical, desalination, and mining projects double down on multi-megawatt pumps. The ACS8080 release illustrates how higher power density and lower harmonics make these drives practical for brownfield sites. Regional oil refineries are adopting 6.6 kV VFDs to reduce steam-turbine auxiliary systems, thereby slashing process-heat emissions under net-zero roadmaps.

In the Asia-Pacific region, local panel builders package medium-voltage cabinets with ring-main units to meet turnkey EPC bids. European players differentiate through integral active-front-end converters that meet stringent grid-code flicker limits. Meanwhile, North American utilities are approving regenerative drive configurations that return braking energy to the network, thereby monetizing power quality improvements. These dynamics indicate an inflection point where medium-voltage penetration may displace low-voltage incumbents in power-hungry verticals by the decade’s close.

By Power Rating: Above-3 MW Drives Deliver Momentum

Systems up to 1 MW still account for 47.10% of 2025 shipments, as OEMs in the food, beverage, and discrete manufacturing sectors typically specify standardized frames for conveyors and mixers. Yet, the AC electric drives market sees above-3 MW installations growing fastest at a 7.26% CAGR, as hydrogen electrolyzer plants, floating LNG vessels, and large-scale carbon-capture units demand precise control of giant compressors. Modern SiC inverters now exceed 7 kHz switching frequency at these ratings without requiring oversized air conditioning, allowing for indoor placement and reduced environmental sealing costs.

Original equipment manufacturers bundle 5 MW drives with active-magnetic-bearing compressors, eliminating lube-oil circuits and boosting plant uptime. In metals and mining, replacing hydraulic couplings with high-power variable-speed drives reduces mechanical stress during mill start-up, thereby extending gearbox life. Service providers capitalize on the ongoing digital transformation by offering cloud-delivered harmonic audits and software patches, making large-scale ownership less daunting for operators previously deterred by complexity.

By Application: Pumps Retain Pole Position as Extruders Accelerate

Centrifugal pumps absorbed 29.35% of 2025 revenue because water treatment, irrigation, and upstream oil fields run thousands of units around the clock. Energy-saving potential remains compelling, with variable-speed retrofits often paying back within 18 months solely on reduced throttling losses. Fans and compressors follow close behind, collectively representing nearly one-third of the AC electric drives market, fueled by data center cooling and industrial gas processing requirements.

Extruders chart the steepest curve, with a 6.18% CAGR, through 2031. Packaging converters demand tight layer-thickness control to curb material waste, and polymer manufacturers exploit torque-limit functions to prevent die clogging. Drive suppliers tailor application firmware with pressure-build-up estimators and melt-temperature compensation, differentiating from generic pump or fan products. Conveyors also benefit from warehouse automation and e-commerce fulfillment expansion, with drives interfacing seamlessly with programmable logic controllers for zero-pressure accumulation zones.

By End-User Industry: HVAC Matches Oil and Gas in Growth Visibility

Oil and gas accounted for 23.05% of the total in 2025, primarily driven by an installed base of high-pressure pumps and compressors that operate continuously for 24 hours a day. Variable-speed retrofits on booster pumps yield multi-million-dollar fuel savings and significant reductions in carbon emissions. Chemicals and petrochemicals maintain a sizable share through demand for process agitators and extruders, while water utilities standardize on drives for variable-speed aeration blowers to reduce peak kWh tariffs.

Commercial HVAC emerges as the fastest-growing segment at a 6.05% CAGR, driven by electrification policies targeting the phase-out of fossil fuels in space heating. European building codes mandate variable-speed ventilation fans, while North American states offer rebates covering up to 25% of drive capital costs for chiller retrofits. Food and beverage processors equip refrigeration racks with synchronized multi-compressor drives to minimize temperature fluctuations, thereby meeting stringent safety regulations.

Geography Analysis

The Asia-Pacific region captured 35.29% of the revenue in 2025, reflecting cross-sector industrialization and supportive government robotics schemes. China’s dominance spans both production and consumption, with local brands cultivating mass-market offerings that shorten lead times. India’s Production Linked Incentive scheme expands demand in cement, steel, and automotive verticals, while Japan champions power-device miniaturization, exporting technology modules to global OEMs.

North America and Europe remain mature yet dynamic. The U.S. Inflation Reduction Act offers tax credits that enhance internal rates of return for energy efficiency retrofits, solidifying the AC electric drives market as a key enabler of decarbonization pathways. European utilities implement dynamic grid-support tariffs that reward facilities that throttle motor loads in response to renewable energy intermittency. Consequently, buyers favor drives with regenerative and low-harmonic capabilities.

The Middle East is on a 6.62% CAGR trajectory, energized by mega-projects such as Saudi Arabia’s NEOM and United Arab Emirates desalination complexes. Integrated petrochemical hubs specify multi-megawatt drives for ethylene crackers and seawater intake pumps. African and South American markets are gaining momentum through mining expansion and water infrastructure investments; however, adoption is tempered by financing constraints and limited after-sales service networks.

Competitive Landscape

Global vendors operate in a moderately fragmented market where top players leverage digital ecosystems to elevate their position beyond commodity status. ABB’s Ability platform links drives, motors, and sensors, enabling health dashboards that predict winding insulation failure months in advance. Siemens strengthened its motion portfolio by acquiring ebm-papst’s industrial drive technology in March 2024, adding compact 60 V modules specifically designed for autonomous mobile robots. Schneider Electric positions its Altivar line around artificial-intelligence-driven energy optimization for process industries.

Chinese manufacturers, such as Inovance and Veichi, continue to gain market share, particularly in mid-tier factories seeking cost-effective solutions with rapid delivery. Western incumbents retain an edge in safety-critical applications thanks to certified functional-safety stacks and global service channels. Component shortages remain a tactical headwind, although falling SiC and IGBT prices ultimately widen profit pools. Partnerships between drive makers and cloud providers accelerate time-to-market for industrial-edge analytics, reshaping competitive factors from pure hardware efficiency to holistic lifecycle value.

Alternating Current (AC) Electric Drives Industry Leaders

ABB Ltd

Siemens AG

Schneider Electric SE

Danfoss A/S

Rockwell Automation Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: WEG announced capacity expansion investments exceeding USD 15 million across Brazilian and Mexican plants to support growing demand for medium-voltage drive systems.

- November 2024: ABB launched the ACS8080 next-generation medium-voltage air-cooled drive featuring up to 98% efficiency and 50% harmonic distortion reduction through advanced MP3C motor control technology. The drive incorporates ABB’s Crealizer open software platform and provides 10× more diagnostic data collection capabilities for predictive maintenance applications across industrial sectors.

- October 2024: Danfoss received recognition for energy-efficiency innovations in its VFD product line.

- September 2024: Yaskawa Electric introduced enhanced servo drive capabilities with improved precision control for robotics.

Global Alternating Current (AC) Electric Drives Market Report Scope

The Alternating Current (AC) Electric Drives Market Report is Segmented by Voltage (Low Voltage, and Medium Voltage), Power Rating (Up to 1 MW, 1 MW – 3 MW, Above 3 MW), Application (Pumps, Fans, Compressors, and More), End User Industry (Oil and Gas, Chemical and Petrochemical, Food and Beverage, Water and Wastewater, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD), Based on Availability.

| Low Voltage |

| Medium Voltage and Others |

| Up to 1 MW |

| 1 MW - 3 MW |

| Above 3 MW |

| Pumps |

| Fans |

| Compressors |

| Conveyors |

| Extruders |

| Other Application |

| Oil and Gas |

| Chemical and Petrochemical |

| Food and Beverage |

| Water and Wastewater |

| Power Generation |

| Metals and Mining |

| Pulp and Paper |

| HVAC |

| Discrete Industries |

| Other End User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Voltage | Low Voltage | ||

| Medium Voltage and Others | |||

| By Power Rating | Up to 1 MW | ||

| 1 MW - 3 MW | |||

| Above 3 MW | |||

| By Application | Pumps | ||

| Fans | |||

| Compressors | |||

| Conveyors | |||

| Extruders | |||

| Other Application | |||

| By End User Industry | Oil and Gas | ||

| Chemical and Petrochemical | |||

| Food and Beverage | |||

| Water and Wastewater | |||

| Power Generation | |||

| Metals and Mining | |||

| Pulp and Paper | |||

| HVAC | |||

| Discrete Industries | |||

| Other End User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the AC electric drives market?

The AC electric drives market size stands at USD 17.12 billion in 2026.

How fast is the sector expanding?

Industry revenue is projected to increase at a 5.72% CAGR from 2026 to 2031.

Which voltage category is growing the quickest?

Medium-voltage drives lead growth with a 7.52% CAGR, outpacing low-voltage units.

Why are variable-speed drives critical for HVAC systems?

They modulate compressor and fan output, achieving 20-50% energy savings and smoother climate control.

Which region offers the highest growth prospects?

The Middle East records a 6.62% CAGR thanks to large industrial and infrastructure projects.

Who are the major players in this field?

ABB, Siemens, Schneider Electric, Rockwell Automation, and Danfoss hold prominent positions supported by extensive service networks and digital platforms.

Page last updated on: