Allogeneic Human Chondrocyte Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

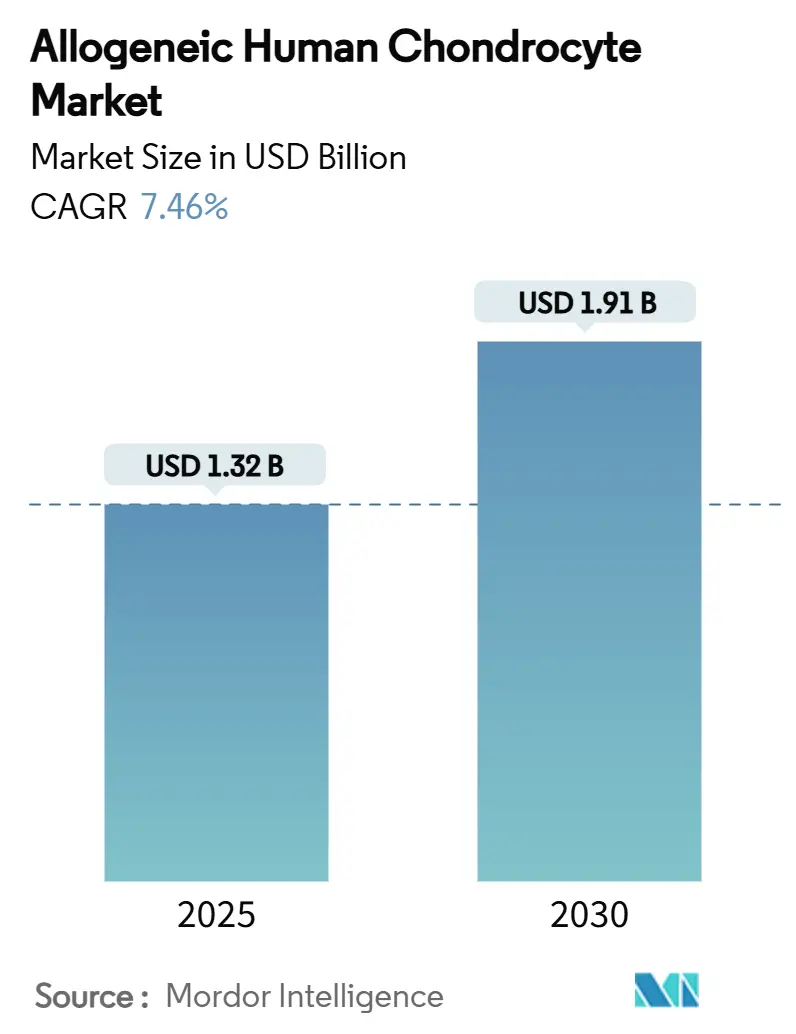

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 1.91 Billion |

| Growth Rate (2025 - 2030) | 7.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Allogeneic Human Chondrocyte Market Analysis by Mordor Intelligence

The allogeneic human chondrocyte market size reached USD 1.32 billion in 2025 and is forecast to reach USD 1.91 billion by 2030, reflecting a 7.46% CAGR over the period. Manufacturing breakthroughs such as quantum hollow-fiber bioreactors are expanding production capacity and lowering per-unit costs, which helps offset historically high therapy prices.[1]Li Yue, Ryan Lim, Brett Owens, “Latest Advances in Chondrocyte-Based Cartilage Repair,” Biomedicines, doi.org Regulatory modernization in South Korea, Japan, the United States, and the European Union is shortening approval timelines and improving reimbursement clarity, giving companies stronger incentives to scale supply.[2]Frances Verter, “South Korea Expands Access to Regenerative Medicine for Serious Illnesses,” parentsguidecordblood.org Competitive intensity is rising as orthopedic device leaders secure cell-therapy platforms, illustrated by Smith+Nephew’s purchase of CartiHeal to broaden its sports-medicine portfolio. Investment momentum remains strong; venture and strategic investors have poured capital into tools that simplify surgical delivery, automate manufacturing, and track patient outcomes, which further expands the addressable base of surgeons and clinics.

Key Report Takeaways

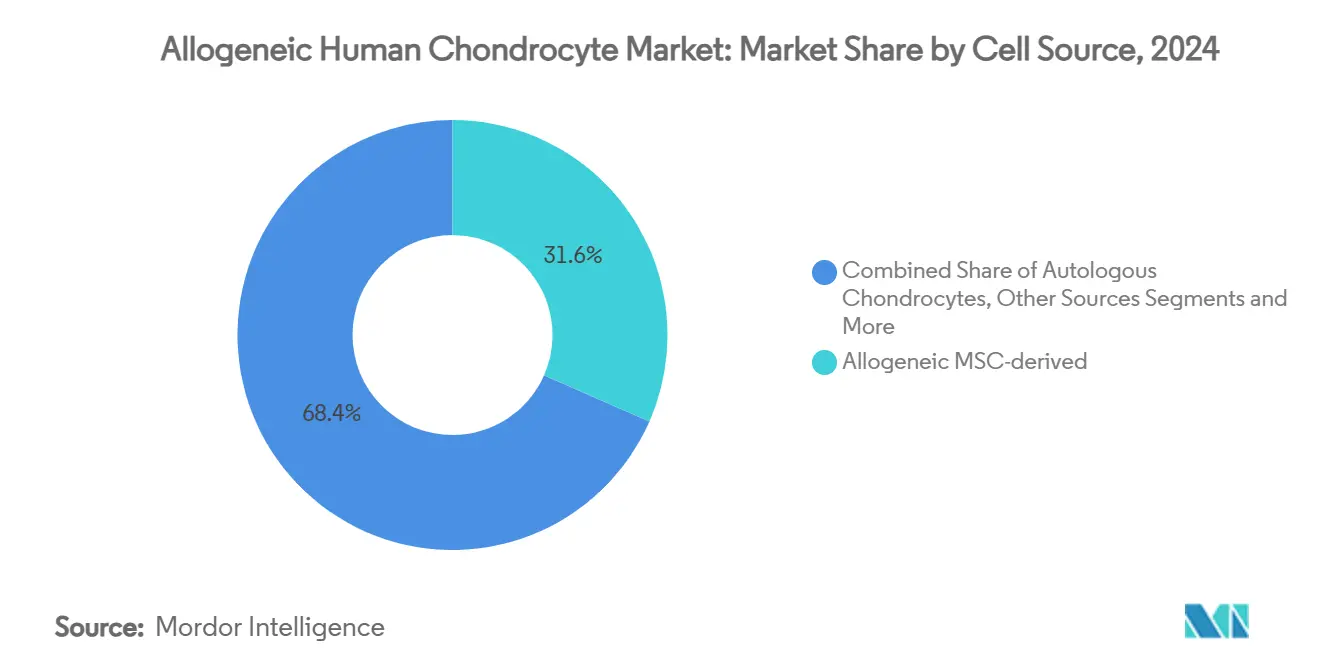

- By cell source, allogeneic MSC-derived chondrocytes led with 31.58% of allogeneic human chondrocyte market share in 2024, while iPSC-derived cells are growing at a 12.48% CAGR to 2030.

- By delivery platform, scaffold-based implants accounted for 39.67% of the allogeneic human chondrocyte market size in 2024; 3D bioprinted constructs show the highest projected CAGR at 12.77% through 2030.

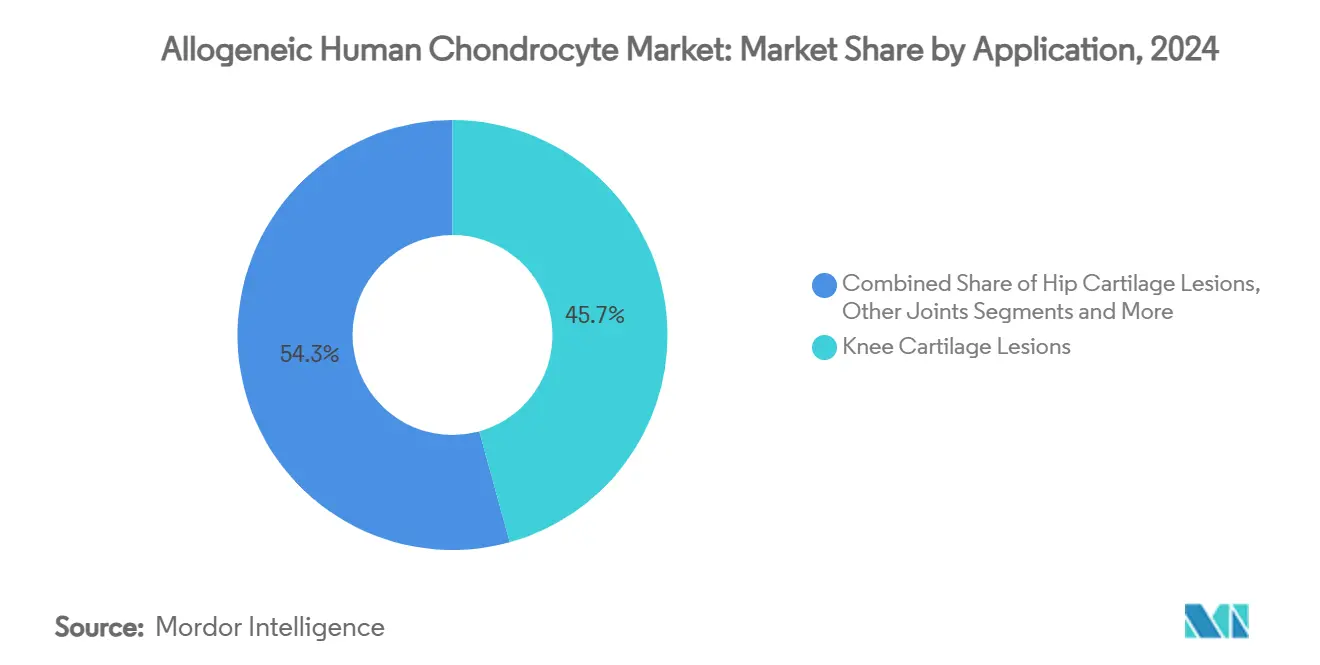

- By application, knee lesions captured 45.71% revenue share in 2024 and hip lesions are advancing at a 10.58% CAGR through 2030.

- By end user, hospitals held 51.34% of the allogeneic human chondrocyte market size in 2024, while ambulatory surgical centers are set to expand at 9.67% CAGR over 2025-2030.

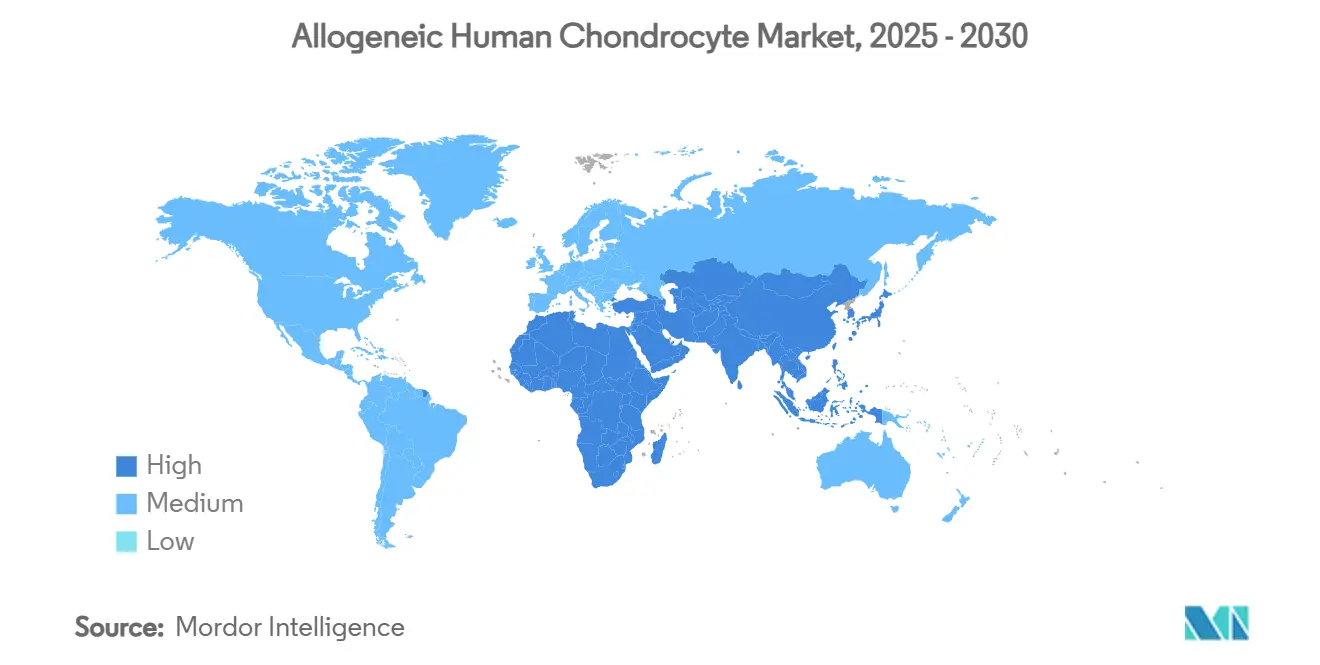

- North America led with 46.52% regional share in 2024; Asia-Pacific is the fastest-growing geography at 9.52% CAGR to 2030.

Global Allogeneic Human Chondrocyte Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoarthritis & sports injuries | +1.8% | North America, Europe, Global | Medium term (2-4 years) |

| Clinical success of Invossa® & Cartistem® | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Favorable reimbursement shifts in US/EU | +1.5% | North America, Europe | Short term (≤ 2 years) |

| Surge in sports-medicine investments | +0.9% | Global, led by North America | Long term (≥ 4 years) |

| Quantum hollow-fiber bioreactors boost yields | +1.1% | Global manufacturing hubs | Medium term (2-4 years) |

| Fast-track ATMP pathways in KR & JP | +0.8% | Asia-Pacific, Global spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis & Sports Injuries

Over 31 million Americans live with knee osteoarthritis, and sports participation is growing across age groups, which continually feeds the candidate pool for advanced cartilage repair.[3]Bo Seung Bae et al., “High Tibial Osteotomy with Allogeneic Umbilical Cord MSCs,” Stem Cell Research & Therapy, doi.orgLongitudinal data show that umbilical cord MSC implantation combined with high tibial osteotomy shrank lesion size from 7 cm² to 0.16 cm² in two years, underscoring the clinical upside of early biologic intervention. Health systems now emphasize preventive measures that postpone or remove total joint replacement, helping payers justify upfront procedure costs. Younger athletes who wish to retain joint integrity are primary adopters, and surgeons have begun positioning allogeneic implants as first-line tools rather than salvage options. This demographic and clinical convergence provides a stable growth platform for the allogeneic human chondrocyte market.

Clinical Success of Invossa & Cartistem

Kolon TissueGene completed Phase 3 dosing in 1,066 patients, the largest dataset in this therapeutic class, which validated allogeneic efficacy while eliminating patient-specific manufacturing delays. These outcomes increased surgeon confidence and prompted the FDA to grant breakthrough status to Nature Cell’s Jointstem, representing the first Korean cell-therapy product with this designation. Long-term data reveal 70-89% of patients report good or excellent function, which pushes more orthopedic centers to add allogeneic lines to their service mix. The programs also accelerated investor interest in next-generation iPSC platforms that promise unlimited cell supply and tighter quality control.

Favorable Reimbursement Shifts in US/EU

Medicare’s Transitional Coverage for Emerging Technologies pathway created a predictable route for advanced therapies to receive temporary national coverage once they secure FDA clearance. UnitedHealthcare followed with clinical policy updates that list specific cellular and tissue-based musculoskeletal products eligible for reimbursement. In Europe, the Joint Clinical Assessment regulation reduces duplicate national reviews, speeding market entry for ATMPs. These aligned policies convert clinical trial wins into near-term revenue, which is crucial for scaling manufacturing. As payers appreciate the lifetime savings from delaying arthroplasty, coverage is expected to broaden further, supporting sustained gains in the allogeneic human chondrocyte market.

Surge in Sports-Medicine Investments

Venture rounds such as Vori Health’s USD 53 million and Restor3d’s USD 70 million highlight investor faith in musculoskeletal innovation. Smith+Nephew allocated nearly USD 3.92 billion to regenerative technologies, signaling that strategic buyers view cell-based implants as core to future sports-medicine portfolios. Capital influx accelerates R&D, broadens clinical education, and subsidizes surgeon training programs. It also finances outcome-tracking software that documents real-world performance, which strengthens payer negotiations. The funding cycle thus feeds a self-reinforcing loop of innovation, evidence generation, and market adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & complex logistics | -1.4% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Safety & regulatory uncertainty | -0.9% | Global, variable by jurisdiction | Medium term (2-4 years) |

| Donor-tissue supply constraints | -0.7% | Global, regional variations | Long term (≥ 4 years) |

| MSC-exosome therapy competition | -0.6% | Global, led by advanced research centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Complex Logistics

A single allogeneic procedure can exceed USD 15,000 once surgery and rehabilitation costs are added, limiting adoption in price-sensitive markets. Cold-chain requirements and fragmented production hubs raise freight expenses and risk batch loss. Manual quality-control steps prolong release times and inflate labor costs. Emerging markets face currency pressures that further widen the affordability gap. Automation and decentralized micro-factories promise cost relief, but broad rollout requires new standards, financing, and workforce training, which will likely take several years.

Safety & Regulatory Uncertainty

The FDA’s mesenchymal stromal cell approval for Ryoncil showed regulators will back innovative products, but the lengthy review highlighted variability challenges that persist across donors and lots. Post-marketing surveillance rules differ widely, from rigorous EU pharmacovigilance to limited frameworks in certain regions, complicating global launch planning. Long-term immunogenicity data remain sparse, fueling caution among payers and surgeons. Harmonizing donor screening standards internationally is slow, prolonging development timelines and raising compliance expense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cell Source: iPSC Innovation Drives Next-Generation Platforms

Allogeneic MSC-derived implants held 31.58% allogeneic human chondrocyte market share in 2024, a position cemented by extensive clinical dossiers that support payer coverage. iPSC-derived platforms are projected to grow at 12.48% CAGR as automated reprogramming and differentiation protocols cut production costs and supply risks. Early preclinical work shows iPSC chondrocytes form hyaline-like tissue without hypertrophy, meeting biomechanical demands for weight-bearing joints. The International Society for Cell and Gene Therapy is crafting global guidelines to standardize iPSC manufacturing, which should quicken regulatory reviews.

Autologous implants still serve niche cases where immune compatibility overrides convenience, but increased procedure cost and two-stage surgery limit broad uptake. Umbilical cord-derived cells provide an immunologically privileged alternative with favorable donor supply, yet require specialized cryopreservation networks. Articular chondrocytes isolated from cadaveric joints bridge the gap between MSC and iPSC platforms, though their expansion potential is lower, restricting scalability. As iPSC cost curves fall, they are expected to capture an expanding slice of the allogeneic human chondrocyte market size, reshaping the competitive landscape.

By Delivery Platform: 3D Bioprinting Transforms Surgical Approaches

Scaffold-based systems accounted for 39.67% of the allogeneic human chondrocyte market size in 2024, reflecting surgeon familiarity and solid long-term data. Matrix-induced ACI blends scaffold support with simplified implantation, appealing to high-volume centers. Injectable suspensions let clinicians treat smaller defects arthroscopically, minimizing OR time and recovery. Gene-enhanced cells are entering early trials aimed at up-regulating anabolic factors for superior cartilage integration.

3D bioprinted constructs will rise at 12.77% CAGR as high-resolution printers create patient-matched implants that replicate native curvature and thickness. Material advances in composite hydrogels enhance mechanical strength without sacrificing nutrient diffusion, solving prior durability issues. The FDA is circulating draft guidance on personalized implants that separates printer validation from cell-line validation, easing approval complexity. As capital investment lowers printer cost and boosts throughput, many tertiary centers intend to install onsite units, pulling procedure volume from central labs and broadening access across the allogeneic human chondrocyte market.

By Application: Hip Lesions Gain Momentum as Techniques Advance

Knee lesions remained dominant at 45.71% share in 2024 because sports injuries and osteoarthritis primarily affect the knee and because existing surgical protocols are mature. Ankle and foot lesions benefit from minimally invasive techniques that allow precise placement in confined joint spaces. Shoulder and elbow procedures are growing as arthroscopic instrumentation improves and throwing-related injuries rise among amateur athletes.

Hip lesions are projected to climb at 10.58% CAGR as arthroscopic portals and flexible delivery cannulas overcome historical access barriers. Early cohorts demonstrate pain relief and motion gains comparable to knee outcomes when surgeons adhere to strict cartilage defect sizing criteria. Payers are beginning to reimburse hip indications in select U.S. states, citing evidence that biologic repair averts costly arthroplasty in younger adults. As clinical experience deepens, hip procedures will represent a growing share of the allogeneic human chondrocyte market size, diversifying revenue streams for implant suppliers.

By End User: Ambulatory Centers Drive Access Expansion

Hospitals controlled 51.34% of allogeneic human chondrocyte market size in 2024 due to infrastructure capable of managing advanced biologics and perioperative risks. Academic institutes pioneer protocols and train fellow surgeons, preserving their role as innovation incubators. Orthopedic clinics contribute follow-up data that validate real-world effectiveness and inform revisions to rehabilitation guidelines.

Ambulatory surgical centers are on pace to grow 9.67% annually through 2030 as MACI Arthro’s arthroscopic format and standardized instrumentation lower complication rates, making outpatient settings viable. Insurers prefer ambulatory sites because bundled payments average 30% lower than hospital charges. Manufacturers now offer turnkey freezer units and remote temperature tracking to simplify biologic storage for centers without pathology labs. Broader ASC uptake will expand procedure volumes in suburban and rural regions, fueling additional demand in the allogeneic human chondrocyte market.

Geography Analysis

North America held 46.52% of the global share in 2024 and continues to benefit from Medicare coverage pathways and robust private-payer adoption. U.S. academic alliances foster rapid translation from trials to practice, while Canadian provincial funds back regenerative medicine centers that broaden patient access. Mexico’s medical-tourism sector attracts self-pay patients from the United States, generating incremental revenue for cross-border clinics. FDA oversight supplies regulatory clarity, but heightened post-market evidence requirements compel firms to allocate resources for longitudinal registries, raising entry costs for smaller players.

Asia-Pacific is projected to post 9.52% CAGR, the fastest worldwide. South Korea’s expanded regenerative medicine law opened the door to hospital-based cell-therapy programs that operate under streamlined oversight, immediately enlarging the treatment pool. Japan’s conditional approval route encourages early revenue as long as real-world data confirm safety and effectiveness. China’s domestic biotech incentives have spawned vertically integrated supply chains that lower material costs, improving affordability for urban hospitals. India’s orthopedic device corridor in Gujarat is ramping production capacity that may support regional kit assembly, trimming import duties. Singapore’s Health Sciences Authority harmonizes trial documentation across ASEAN, giving sponsors a hub for multi-country studies that underpins future launches.

Europe remains a key market, anchored by the European Medicines Agency’s centralized ATMP approval system that offers continent-wide authorization. Germany and the United Kingdom lead adoption on the back of national health-service funding and advanced surgical training programs. France’s tax credits for bioprocessing CapEx encourage local manufacturing, ensuring security of supply. Italy leverages hospital exemption rules to craft tailored batch runs for complex cases, but inconsistent implementation across regions adds administrative burden. Overall, the region supplies stable demand but requires country-specific reimbursement strategies, underscoring the need for locally generated health-economic evidence as the allogeneic human chondrocyte market evolves.

Competitive Landscape

The field shows moderate concentration and room for consolidation as device majors acquire niche cell-therapy innovators. Smith+Nephew’s CartiHeal deal integrated a proven implant with global sales infrastructure, highlighting how scale can accelerate clinic education programs and tender penetration. Mesoblast’s Ryoncil approval provided the first regulatory template for allogeneic MSC products, prompting peers to benchmark their dossiers accordingly. Quantum hollow-fiber systems differentiate manufacturers on cost and throughput, while iPSC pipelines promise a leap in supply security.

Market participants focus on data generation over price discounting. Large registries powered by electronic-health-record integration collect outcome metrics that validate payer value propositions. Pediatric cartilage repair, previously underserved, is emerging as a white-space where allogeneic cells may avoid donor-site morbidity. Combination products that pair cells with bioactive scaffolds or growth-factor eluting matrices are in early trials. Disruptors developing automated closed-system manufacturing could undercut incumbents on cost, accelerating adoption in community hospitals and ASCs, which will shift share dynamics inside the allogeneic human chondrocyte market.

Allogeneic Human Chondrocyte Industry Leaders

Kolon TissueGene

MEDIPOST

Smith+Nephew

Vericel

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nature Cell won FDA breakthrough therapy designation for Jointstem, the first Korean cell-therapy product to secure the label.

- December 2024: The FDA approved remestemcel-L-rknd (Ryoncil, Mesoblast) for pediatric steroid-refractory acute graft versus host disease, marking the first FDA-cleared MSC therapy.

- August 2024: Vericel received FDA clearance for MACI Arthro, the first cellularized scaffold designed for arthroscopic cartilage repair procedures.

Global Allogeneic Human Chondrocyte Market Report Scope

| Autologous Chondrocytes |

| Allogeneic Articular Chondrocytes |

| Allogeneic MSC-Derived Chondrocytes |

| iPSC-Derived Chondrocytes |

| Umbilical-Cord Chondrocytes |

| Other Sources |

| Scaffold-Based Implants |

| Injectable Cell Suspensions |

| Matrix-Induced ACI (MACI) |

| 3-D Bioprinted Constructs |

| Gene-Enhanced Allogeneic Cells |

| Knee Cartilage Lesions |

| Ankle & Foot Lesions |

| Hip Cartilage Lesions |

| Shoulder & Elbow |

| Other Joints |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopedic & Sports-Medicine Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cell Source | Autologous Chondrocytes | |

| Allogeneic Articular Chondrocytes | ||

| Allogeneic MSC-Derived Chondrocytes | ||

| iPSC-Derived Chondrocytes | ||

| Umbilical-Cord Chondrocytes | ||

| Other Sources | ||

| By Delivery Platform | Scaffold-Based Implants | |

| Injectable Cell Suspensions | ||

| Matrix-Induced ACI (MACI) | ||

| 3-D Bioprinted Constructs | ||

| Gene-Enhanced Allogeneic Cells | ||

| By Application | Knee Cartilage Lesions | |

| Ankle & Foot Lesions | ||

| Hip Cartilage Lesions | ||

| Shoulder & Elbow | ||

| Other Joints | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Orthopedic & Sports-Medicine Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the allogeneic human chondrocyte market?

The market is valued at USD 1.32 billion in 2025 and is forecast to reach USD 1.91 billion by 2030.

How fast is demand for allogeneic cartilage implants growing?

Demand is rising at a 7.46% CAGR, fueled by better clinical outcomes and supportive reimbursement policy.

Which cell source is expanding the quickest?

IPSC-derived chondrocytes show the highest growth, projected at 12.48% CAGR through 2030.

Which region offers the strongest future growth?

Asia-Pacific leads with a projected 9.52% CAGR thanks to streamlined approval pathways and government investment.

Why are ambulatory centers important to future adoption?

Ambulatory surgical centers deliver outpatient procedures at lower cost, driving 9.67% CAGR for this site of care.

What technology most reduces manufacturing cost?

Quantum hollow-fiber bioreactors improve yield and cut per-unit expense, helping address historical cost barriers.

Page last updated on: