Airport Ground Support Vehicles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.4 Billion |

| Market Size (2031) | USD 11.91 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

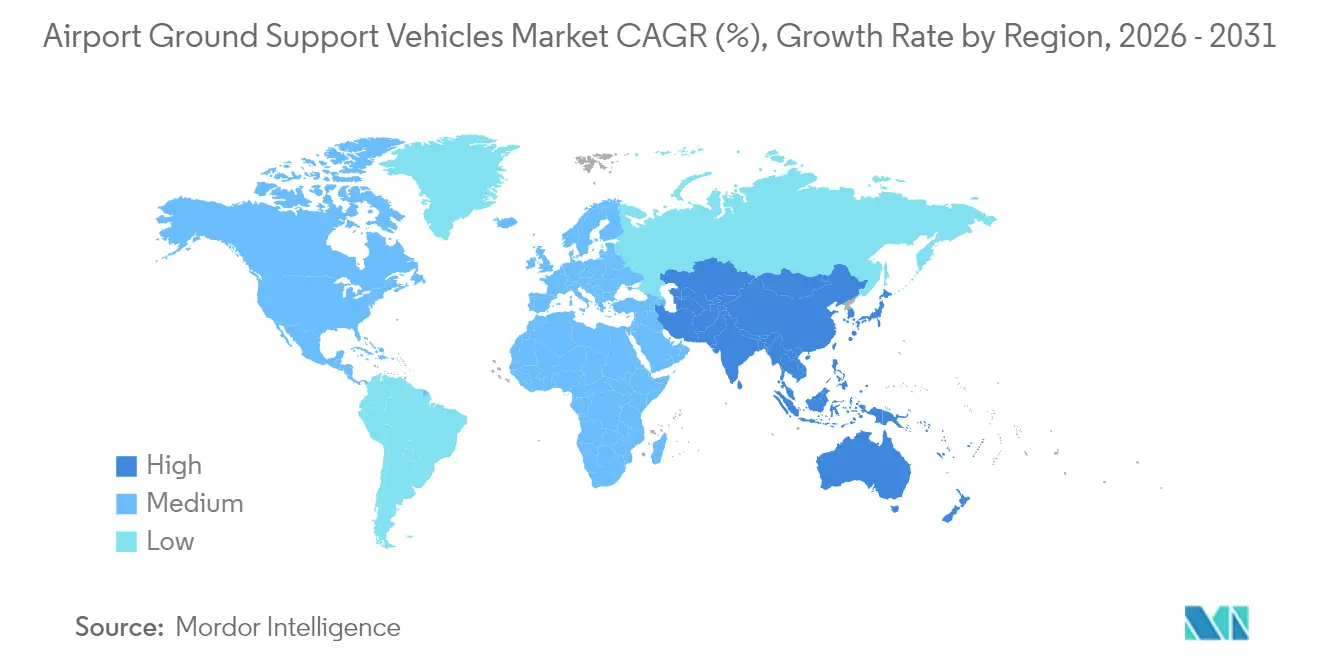

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

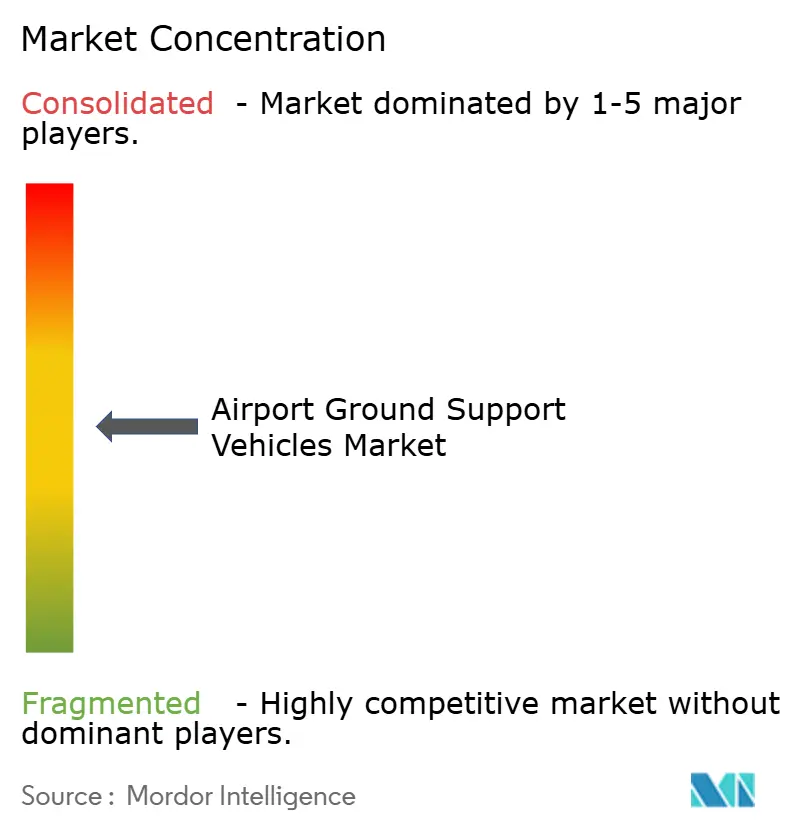

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Ground Support Vehicles Market Analysis by Mordor Intelligence

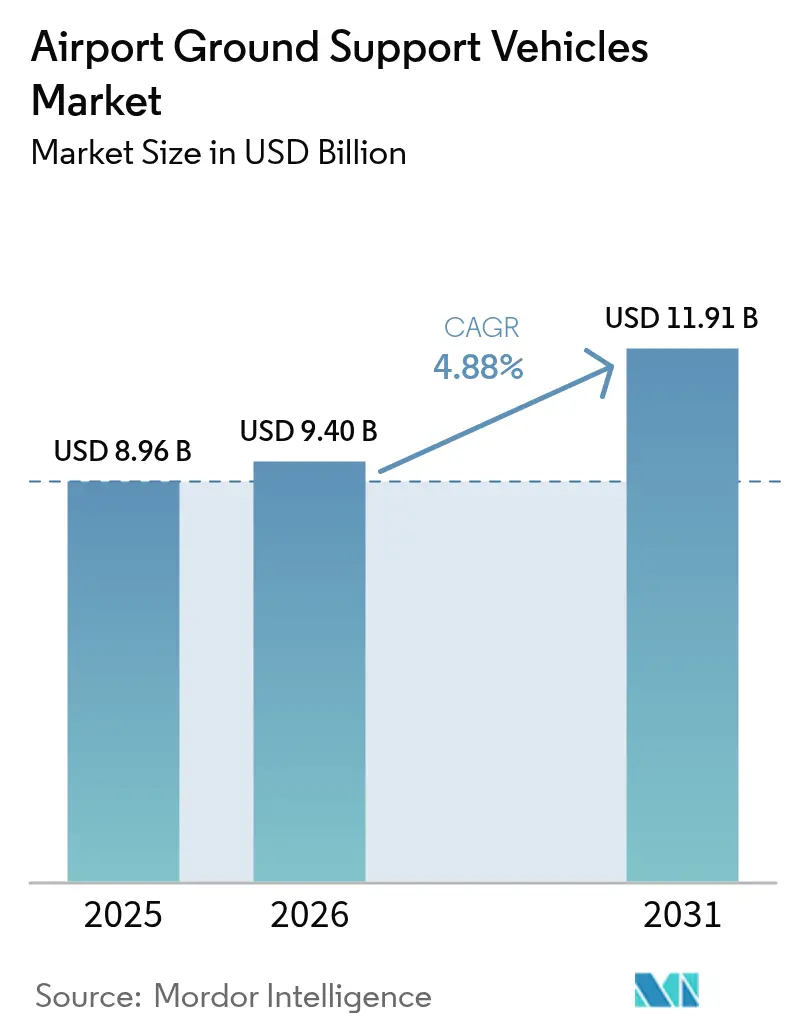

The airport ground support vehicles market size was valued at USD 8.96 billion in 2025 and estimated to grow from USD 9.40 billion in 2026 to reach USD 11.91 billion by 2031, at a CAGR of 4.88% during the forecast period (2026-2031). Growth is shaped by a transition from ownership-heavy models toward flexible leasing and pooling structures that reduce capital intensity during traffic cycles. Electrification mandates are altering procurement timelines and vehicle specifications, while increasing near-term capital requirements for charging infrastructure and battery systems. Operators favor connected and data-rich fleets that compress turnaround times and lift utilization across mixed assets. Competitive strategies increasingly integrate vehicles with telematics, energy management, and lifecycle service contracts.

North America held the most prominent regional position in 2024, while the Asia-Pacific region is set to deliver the fastest regional growth, driven by greenfield airport programs that prioritize net-zero operations from the initial commissioning. Within vehicle types, tugs and tractors account for the largest share today, while de-icing units post the fastest growth as winter operations expand into more geographies. Application demand remains anchored in aircraft handling, with cargo handling rising faster due to the development of dedicated freighters and the increasing demand for time-sensitive logistics service levels. Non-electric powertrains still dominate the installed base, although electric variants are gaining ground as total cost of ownership improves and carbon costs are factored into operations. The ownership mix is fragmenting as carriers divest their fleets and rely on ground support providers and lessors to align expenses with traffic variability.

Key Report Takeaways

- By type, tugs and tractors led with 30.78% revenue share in 2025, while de-icing vehicles are projected to expand at a 7.43% CAGR through 2031.

- By application, aircraft handling accounted for 53.85% in 2025, and cargo handling is forecasted to grow at a 6.61% CAGR to 2031.

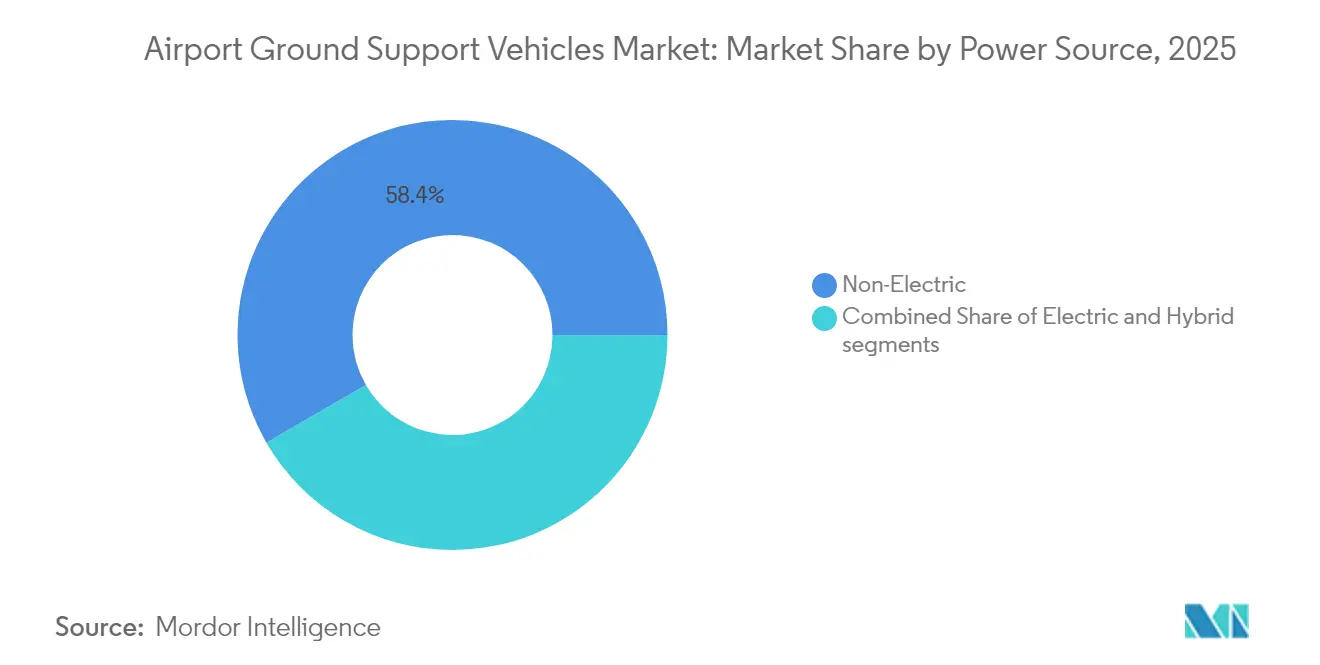

- By power source, non-electric held 58.35% of the installed base in 2025, while electric variants are expected to grow at a 9.55% CAGR through 2031.

- By end user, commercial aviation captured 93.30% of demand in 2025 and is projected to grow at a 5.55% CAGR through 2031.

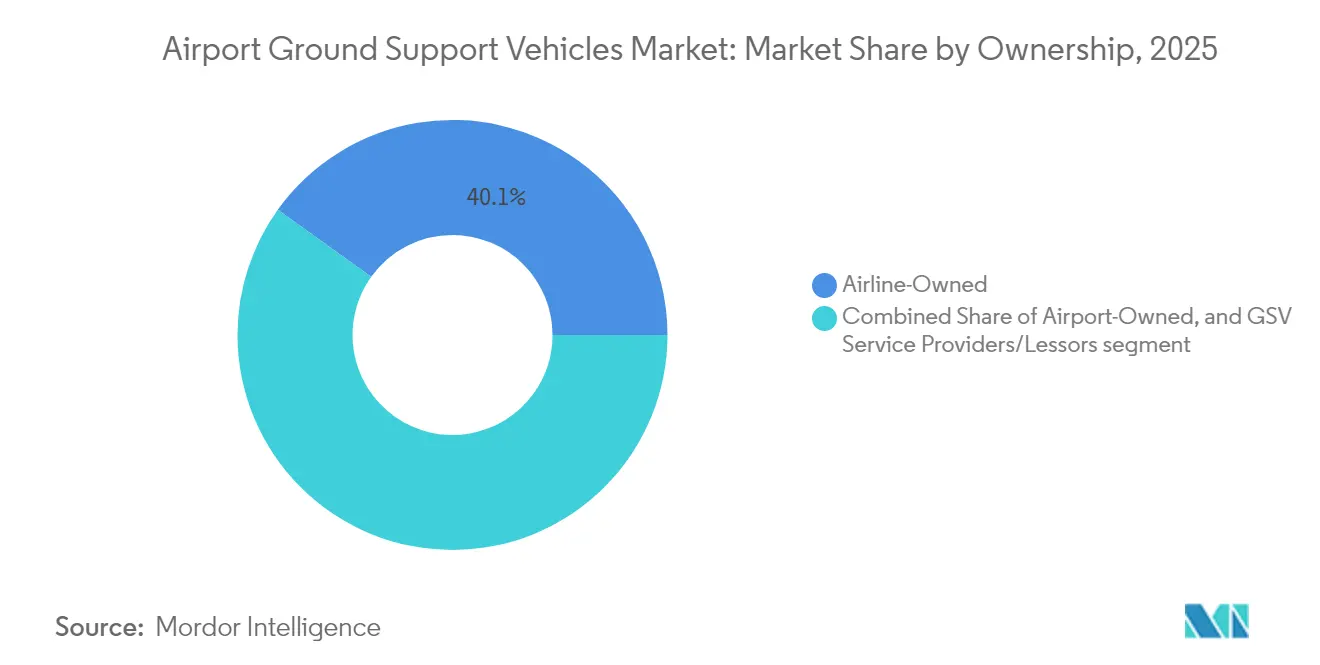

- By ownership, airline-owned fleets held 40.10% in 2025, while GSV service providers and lessors are expected to expand at a 6.64% CAGR through 2031.

- By geography, North America held 34.12% in 2025, and the Asia-Pacific region is projected to be the fastest-growing region at a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Airport Ground Support Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global airport infrastructure requiring enhanced vehicle fleets | +1.2% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Increase in air traffic volume necessitating scalable ground vehicle operations | +1.0% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Policy-driven shift toward low-emission and electric ground support vehicles | +1.5% | Europe, North America, select Asia-Pacific hubs | Long term (≥ 4 years) |

| Availability of government incentives for fleet electrification and modernization | +0.8% | United States, EU member states, China | Medium term (2-4 years) |

| Growth in vehicle leasing, pooling, and fleet-as-a-service models | +0.9% | Global, early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Adoption of autonomous driving technologies and connected fleet management platforms | +0.7% | North America, UAE, Singapore, select Chinese airports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Airport Infrastructure Requiring Enhanced Vehicle Fleets

Large airport programs in Asia-Pacific and the Middle East are bundling ground support vehicles into terminal and apron contracts, which compresses delivery windows and shifts procurement responsibility to airport operators.[1]Airports Council International, “Airport Development,” ACI World, aci.aero India has publicly committed to establishing multiple greenfield airports by 2030, which implies a baseline fleet of dozens of units per site, creating a predictable volume pipeline for suppliers even as site-level schedules fluctuate. Saudi Arabia’s flagship projects, including Red Sea International Airport and King Salman International Airport, are being designed for electric-majority fleets at opening, which sets operational benchmarks for emissions, availability, and lifecycle service arrangements. These projects create demand clusters that differ from replacement cycles, as they drive synchronized multi-vehicle orders more frequently than single-category refresh cycles.

Smaller regional airports are also upgrading fleets with specialized vehicles under national connectivity and resilience mandates that prioritize operational continuity during disruptions and severe weather. The net effect is a stage-gated demand profile that requires manufacturers to flex modular production and staging capacity across categories and sites.

Increase in Air Traffic Volume Necessitating Scalable Ground Vehicle Operations

Passenger volumes recovered faster than many planning baselines in 2024 across several regions, forcing airlines and ground handlers to add vehicles and retrofit dispatch systems outside their nominal replacement cycles.[2] International Air Transport Association, “Economics and Cargo Programs,” IATA, iata.org Turnaround time targets on narrowbody fleets continue to compress, which requires synchronized vehicle choreography and real-time tasking that legacy manual dispatch cannot deliver at scale. As widebody frequencies normalize, airports will require larger refueling capacities and higher-capacity de-icing units, which add weight, increase costs, and necessitate specialized staffing, thereby complicating fleet mix optimization.

Cargo patterns diverge from passenger recovery since dedicated freighter operations remain resilient, which increases demand for main deck loaders, heavier tugs, and cargo transporters capable of higher duty cycles. These dynamics prompt operators to adopt telematics overlays and connected scheduling to balance asset duty time across gates, aprons, and cargo stands, particularly during periods of concurrent activity peaks. Airports and handlers that integrate collaborative decision-making platforms can reduce idle time and align GSV dispatch with updated flight schedules and resource constraints.

Policy-Driven Shift Toward Low-Emission and Electric Ground Support Vehicles

Regulatory and policy frameworks in Europe and North America set binding and programmatic requirements that drive the electrification of airport ground operations and vehicle fleets. California’s Advanced Clean Fleets regulation includes off-road categories at airports, which is pushing operators at large hubs to retire serviceable diesel units on an accelerated schedule and absorb near-term depreciation charges. European decarbonization initiatives and airport accreditation programs require concrete emissions reduction plans for airport-controlled operations by 2030 and beyond, which translates into near-complete GSV electrification at major hubs.

Several Asian regulators tie new airport approvals and expansions to electrification commitments that airports pass through in contracts and tariffs, which reshapes the budget calculus for airline-owned fleets. Procurement is becoming more prescriptive regarding battery chemistry and end-of-life recovery plans, favoring suppliers with closed-loop recycling partnerships and verifiable material traceability. Compliance increases the need for integrated energy management to avoid grid penalties and to balance charging with apron operations during peak schedules.

Availability of Government Incentives for Fleet Electrification and Modernization

Incentives reduce the effective capital cost of electric units and associated infrastructure, which narrows payback periods for high-utilization airports and handlers. In the US, the Commercial Clean Vehicle Credit, established under the Inflation Reduction Act, allows credits to be applied to electric GSVs that meet specific eligibility criteria, including battery sourcing and assembly thresholds. Several EU member states operate grant programs that cover a portion of the incremental cost between diesel and electric units.

Chinese provincial programs support domestically produced electric equipment in targeted regions, which encourages local procurement and shapes competitive outcomes for multinational suppliers. Incentive cliffs can pull demand forward as expiration approaches, creating order backlogs and capacity strains that may increase quality risks if production ramps up without complete validation cycles in place. Procurement functions are adding incentive diligence to their TCO models to ensure that credits and grants are captured during the window of eligibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront acquisition cost of electric and hybrid ground support vehicles | -0.8% | Global, acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Inadequate charging infrastructure and limited grid readiness at airports | -0.6% | Asia-Pacific, Africa, South America, secondary European hubs | Medium term (2-4 years) |

| Supply chain disruptions impacting availability of EV components and semiconductors | -0.5% | Global | Short term (≤ 2 years) |

| Cybersecurity and system integration challenges in autonomous ground vehicle fleets | -0.3% | North America, Europe, select advanced APAC airports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Acquisition Cost of Electric and Hybrid Ground Support Vehicles

Electric units typically carry higher sticker prices compared to diesel equivalents of the same capacity, which is most challenging for operators with shorter fleet refresh cycles at large hubs. Battery packs account for a significant portion of the bill of materials, and aviation-duty requirements for fast charging and extreme temperature performance limit the direct transfer of consumer EV cost curves. Lease financing can alleviate cash needs, but the residual value of electric ground support assets is uncertain due to the rapid pace of battery improvements and evolving charging standards.

Smaller carriers and independent ground handlers often prioritize aircraft investment and defer ground fleet electrification until deadlines force action, which compresses procurement windows and strains supplier capacity. The total cost of ownership is sensitive to diesel fuel costs and duty cycles, which can extend payback periods when volumes dip or when energy rates increase. This cost barrier slows adoption in emerging markets that lack targeted grants or tariff exemptions for electric ground support equipment.

Inadequate Charging Infrastructure and Limited Grid Readiness at Airports

Many airports lack the spare electrical capacity or charger coverage necessary for large fleets, particularly when overnight charging overlaps with other loads. Substation upgrades and dedicated feeders incur multi-million-dollar costs that exceed typical ground equipment budgets and require multi-party approvals across utilities and airport authorities. High-power fast charging for buses, refuelers, and continuous-duty tractors creates demand spikes that can exceed local transformer ratings, necessitating grid reinforcement or on-site energy storage.

Airports in regions with unstable power grids rely on backup diesel generators that cannot support large-scale GSV charging, creating a dependency on hybrids or limited electric vehicle deployments. Charger and vehicle interoperability is still evolving, which creates lock-in risks and complicates multi-vendor fleet strategies in the near term. Programs that fund gate electrification and low-emissions airport projects can reduce the infrastructure gap at large hubs, though rollouts at secondary airports remain slower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialized Vehicles Capture Growth as Fleets Diversify

Tugs and tractors accounted for 30.78% of 2025 revenue, as these assets support pushback, baggage towing, and cargo movement on every turn, thereby anchoring recurring demand within the airport ground support vehicles market. De-icing vehicles are the fastest-growing type, with a 7.43% CAGR through 2031, reflecting climate variability that extends freeze events into regions with limited legacy capacity and stricter glycol containment rules that force the replacement of older units. Replacement pressure is also visible in refuelers as older fleets face tighter fire safety compliance in several jurisdictions. Electric passenger buses align well with range and charging windows, which helps airports report lower emissions for Scope 1 categories and improves airside air quality. Ground power units and pre-conditioned air units grow in tandem with gate electrification programs, which reduce auxiliary power unit usage during aircraft turns. Performance requirements also increase as airports standardize on integrated safety interfaces and remote monitoring across vehicle categories.

De-icing demand is becoming less seasonal in some markets as irregular winter precipitation and cold snaps create new operational requirements at airports that previously held minimal equipment. Environmental compliance is driving the adoption of closed-loop recovery systems and advanced spray control, which will concentrate spending in the near term as operators retire non-compliant assets. Electric refuelers lag in adoption because battery mass can reduce payload and duty cycles, which keeps diesel units in service in many fleets until energy density improves. Electric buses and belt loaders are more suitable where daily duty cycles fit within a single charge window and where on-site charging can be staged near gates and aprons. The airport ground support vehicles market is also witnessing the broader adoption of sensor suites across units, which enhances safety, fault detection, and driver assistance in low-visibility operations. Procurement specifications are expanding to include robustness and cybersecurity baselines for power electronics, in addition to traditional mechanical performance.

By Application: Cargo Operations Outpace Passenger Handling Expansion

Aircraft handling operations captured 53.85% of demand in 2025, which reflects reliance on pushback tugs, lavatory trucks, potable water trucks, and other turn-critical assets that scale directly with flight frequency in the airport ground support vehicles market. Cargo handling is the fastest-growing application, with a 6.61% CAGR, as express logistics and scheduled freighter operations add capacity to meet delivery times and support e-commerce growth. Belly cargo on passenger services has improved, but dedicated freighter fleets require loaders and tractors engineered for higher weights and longer duty cycles, which can stress powertrains and tires. Passenger handling remains stable, as jet bridge expansion reduces apron boarding, although remote stands continue to drive passenger bus needs at growing airports. Pharmaceutical and perishable cargo drive specialized dollies and temperature-controlled transport, which increases equipment cost and training requirements for handlers. Cargo terminal expansions bring synchronized investment in ground support fleets to meet certified handling times and to support specialized cargo unit load devices.

Cargo operations at e-commerce and express hubs require tighter adherence to ground time, which drives the adoption of telematics, RFID tracking, and dispatch optimization across loaders and tugs. Main deck cargo loaders and higher-torque tractors are required for widebody freighters, which differentiate their specifications from those of passenger-focused fleets. Cold chain cargo requires additional validation and monitoring steps at handoff, which necessitates the use of sensors, backup power, and integrated alarms on transport units. Airport cargo villages expand vehicle staging areas and charging positions, which change apron design and ground traffic flows inside secure zones. As dedicated freighter rotations increase, the airport ground support vehicles market must accommodate nighttime peaks when charging windows are constrained by consecutive turns. Software coordination between cargo terminals, yard management, and apron control becomes as crucial as mechanical performance for throughput.

By Power Source: Electrification Accelerates Despite Persistent Grid Constraints

Non-electric powertrains held 58.35% of the installed base in 2025 due to existing fueling infrastructure and range flexibility across duty cycles in the airport ground support vehicles market. Electric variants are the fastest-growing segment, with a 9.55% CAGR, driven by improved batteries, zero-emission mandates, and the increasing total cost of ownership advantages in high-utilization settings. Hybrid systems remain a transitional choice when grid capacity is constrained or when cold-weather performance is a concern, although their share is expected to decline as fast charging improves. Lithium-iron-phosphate (LFP) and similar chemistries provide an adequate range for most tugs, belt loaders, and buses; however, cold-weather derating still requires thermal management strategies at northern airports. Charging infrastructure investments are concentrated in larger hubs, creating a two-speed adoption pattern that depends on access to capital and local utility coordination. Second-life uses of retired packs as stationary storage are being piloted to support charging while deferring grid upgrades.

Energy management platforms are increasingly bundled with chargers to optimize charging windows around scheduled operations and demand charges. Airports integrate charger siting with apron redesign to reduce deadhead driving and to maintain emergency access clearances. Variants such as opportunity charging and battery swapping are explored for high-duty vehicles to minimize downtime during peak periods. Standardization on communication protocols between chargers and vehicles is advancing, which supports multi-vendor fleets and reduces lock-in risks. Carbon pricing and emissions reporting are being factored into procurement models, which strengthens the case for electric unit deployments at hubs subject to fees or emissions caps. These changes reinforce the trajectory toward electric dominance in new procurements while diesel remains in legacy roles until infrastructure and duty cycle alignment is complete.

By End User: Commercial Aviation Dominates but Military Segment Harbors Niche Demand

Commercial aviation accounted for 93.30% of end-user demand in 2025 and is projected to grow at a 5.55% CAGR, driven by expanding passenger and cargo volumes in the airport ground support vehicles market. Military demand follows procurement cycles linked to airlift modernization and expeditionary logistics, which favor durability, fuel flexibility, and operations in harsh environments. Commercial operators standardize fleets across stations to reduce maintenance complexity and training time, which improves interchangeability across handling partners. Military users often require vehicles suitable for temporary airfields and rough terrain, which creates divergent product requirements compared to civilian fleets. Dual-use airports introduce interoperability needs for charging, safety systems, and access control that can influence equipment specifications for both user groups. Early military deployments of electric units focus on bases with stable power provision, where noise and emissions reductions support mission requirements.

Commercial carriers are tightening service-level agreements with handlers that include uptime metrics and response windows, which shifts some risk and performance obligations to service providers. Airlines are revisiting in-source versus outsource decisions at hub and focus airports, which can alter local fleet composition and parts stocking strategies. Military procurement often requires compliance with local content and specific standards, which can limit crossover from commercial product lines. Training and certification requirements differ across commercial and military settings, which affects how autonomy features and telematics are implemented and approved. As both user groups modernize, cybersecurity and system isolation are becoming standard requirements for connected equipment, underscoring the need for equipment vendors to support varied mission profiles without fragmenting product platforms.

By Ownership: Fleet-as-a-Service Models Erode Traditional Airline Control

Airline-owned fleets held 40.10% in 2025, reflecting legacy practices where carriers controlled equipment availability and turn-time accountability within the airport ground support vehicles market. Ground support service providers and lessors are the fastest-growing ownership group, with a 6.64% CAGR, as airlines pivot capital toward aircraft and digital products. Airport-owned shared fleets are common among smaller carriers and regional operations that lack the scale for dedicated purchases. At the same time, some hubs internalize their fleets to streamline apron utilization and maintenance. Leasing models transfer technology obsolescence risk and improve access to the latest-generation electric units and charging infrastructure. Service contracts increasingly bundle predictive maintenance and parts availability to convert variable repair costs into fixed monthly fees. Secondary markets for used ground support vehicles are still in development, which influences lease residuals and pricing as lessors underwrite the risk of remarketing.

Digital marketplaces and telematics platforms are improving pricing transparency and facilitating multi-airport redeployment of assets to match seasonal demand. Airlines and handlers are adding performance clauses to contracts that tie payment to compliance with dispatch and turnaround metrics. Lessors are investing in battery refurbishment and second-life use to improve residual values for electric fleets. Airport operators are working with utilities to secure advantageous tariffs and demand charge mitigation that can be shared with contracted handlers and lessors. These operational and financial shifts reinforce the trend toward variable cost models that better align with traffic volatility. The airport ground support vehicles market is therefore seeing a structural rebalancing of asset ownership toward specialized providers with software and financing capabilities.

Geography Analysis

North America held 34.12% of the market in 2025, reflecting a mature base with active fleet replacement and aggressive zero-emission rules in jurisdictions such as California and New York, which accelerate diesel retirements within the airport ground support vehicles market. The Asia-Pacific region is projected to grow at a 6.94% CAGR through 2031, supported by the commissioning of new airports and terminal expansions in China, India, and Southeast Asia, which will specify electric-majority fleets from the outset. The Middle East continues to deliver large, integrated airport programs that include fleet electrification and digital orchestration from the outset, setting new operating baselines for greenfield sites. Europe faces compressed replacement schedules due to decarbonization commitments that pull forward end-of-life for diesel equipment, which stresses airport capital plans. These regional dynamics create varied baselines for vehicle choice, ownership models, and infrastructure readiness across airport systems.

South America and Africa exhibit slower electrification adoption due to limitations in grid capacity and financing, which hinder the deployment of fast chargers. However, flagship airports such as São Paulo Guarulhos and Johannesburg OR Tambo are advancing pilots that can scale over time in the airport ground support vehicles market. Comparing the 2024 baseline with the 2025 to 2030 trajectory reveals acceleration in the Asia-Pacific and Middle East regions, where new airport construction drives multi-category purchases more than cyclical replacement. North America and Europe lean toward premiumization as electrification raises unit values and software content per vehicle increases, even when overall fleet counts remain stable. Cold climates in Canada and Scandinavia bring energy management and thermal controls into focus to manage battery performance on winter operations. Regional policies for carbon pricing and emissions caps also influence procurement, with European airports integrating emissions costs into business cases at a faster pace than most other regions. Global suppliers are establishing regional assembly facilities for electric units to shorten lead times and comply with local content rules.

Regulatory divergence adds compliance and certification work for multinational manufacturers, since FAA, EASA, and national standards in China do not fully align on safety, electromagnetic compatibility, and software assurance. Domestic content rules in several countries influence procurement and can restrict the use of imported vehicles in publicly financed airport programs. Airports and suppliers manage these constraints through modular designs and certification strategies that reuse cores while localizing shells and software to meet jurisdictional requirements. The airport ground support vehicles market, therefore, is segmented by regulation and financing as much as by fleet composition. Airports that initiate early upgrades to the grid and standardize charging will benefit from vendor competition and faster deployments, creating a clear advantage for regions with aligned airport, regulator, and utility roadmaps.

Competitive Landscape

The airport ground support vehicles market exhibits moderate concentration, with leading manufacturers such as Oshkosh AeroTech (Oshkosh Corporation), Textron Inc., and ALVEST Group maintaining an installed base and service coverage advantage. Meanwhile, regional specialists and adjacent-sector OEMs intensify competition. Incumbents are investing in integrated electrification offerings that pair vehicles with chargers, energy management, and predictive maintenance to secure multi-year service revenue. Automotive and material-handling entrants repurpose electric commercial platforms into baggage tractors and belt loaders, which can reduce costs but lack the depth of aviation certification required for complex vehicles such as refuelers and de-icers. Software-defined fleet models shift the source of differentiation toward telematics and dispatch optimization, which challenges traditional parts-and-service moats. Buyers are favoring turnkey packages with performance guarantees, uptime clauses, and charging buildouts that create stickier supplier relationships. Vendors are also forming partnerships with battery recyclers and energy storage providers to close the loop on materials and to stabilize charging loads.

Manufacturers are responding to infrastructure bottlenecks with solutions that include high-capacity chargers, on-site storage, and load-balancing software that reduces peak demand charges. Integration with airport collaborative decision-making and resource management systems is becoming a key selling point, as it links vehicle dispatch to gate changes, crew timing, and inbound flight updates. White-space opportunities exist in autonomous orchestration, battery swapping for continuous-duty vehicles, and advanced thermal management for cold weather performance. Ground service provider consolidation increases purchasing leverage and raises expectations for uptime and service-level adherence, which pushes vendors to expand warranties and introduce pay-for-performance models. We also see an increased interest in vertical integration for battery packs and power electronics, aiming to reduce dependency on external supply chains. Suppliers are engaging in pilot projects with airports and airlines to validate operations while navigating cybersecurity requirements and airside safety rules.

Investments in large charging hubs at major airports support the rapid expansion of electric fleets and address a key bottleneck in adoption. Regional joint ventures and local manufacturing plants in Asia enable suppliers to meet domestic content requirements and reduce delivery times. Autonomous de-icing trials and battery swapping pilots indicate a growing role for software and energy innovations in high-utilization categories. These moves reflect a competitive field that is investing in both product and infrastructure to secure long-term service relationships.

Airport Ground Support Vehicles Industry Leaders

Mallaghan Group LTD.

ALVEST GROUP

Textron Inc.

Oshkosh AeroTech (Oshkosh Corporation)

Vestergaard Company A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: dnata signed five-year global framework contracts worth over USD 210 million for Ground Support Equipment, placing initial orders of USD 29 million to enhance efficiency, safety, and sustainability across its global operations, serving over 330 airline customers.

- January 2024: dnata’s airport handling division was awarded a 7-year ground handling license by Aeroporti di Roma to establish its operations at Rome Fiumicino Airport (FCO) starting from Q2 2024.

- January 2024: Oshkosh Corporation acquired AeroTech from JBT Corporation for USD 800 million. AeroTech provides aviation ground support products, gate equipment, and airport services to commercial airlines, airports, air freight carriers, ground handling companies, and military customers.

Global Airport Ground Support Vehicles Market Report Scope

Airport ground support vehicles include passenger buses, refuelers, tugs and tractors, lavatory service vehicles, deicers, ground power units, pre-conditioned air units, fuel trucks, and other ground handling systems in airports.

The airport ground vehicles market is segmented based on type, application, power source, end-user, ownership, and geography. By type, the market is segmented into refuelers, tugs and tractors, passenger buses, de-icing vehicles, ground power units, and others. The other segment includes such items as baggage carts, air start units, water service trucks, and catering trucks. By application, the market is segmented into aircraft handling, passenger handling, and cargo handling. By power source, the market is segmented into electric, non-electric, and hybrid. By end user, the market is segmented into commercial and military. By ownership, the market is segmented into airport-owned, airline-owned, and GSV service providers/lessors.

The report also covers the market sizes and forecasts for the airport ground support vehicles market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Refuelers |

| Tugs and Tractors |

| Passenger Buses |

| De-Icing Vehicles |

| Ground Power Units |

| Others |

| Aircraft Handling |

| Passenger Handling |

| Cargo Handling |

| Electric |

| Non-Electric |

| Hybrid |

| Commercial |

| Military |

| Airport-Owned |

| Airline-Owned |

| GSV Service Providers/Lessors |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Refuelers | ||

| Tugs and Tractors | |||

| Passenger Buses | |||

| De-Icing Vehicles | |||

| Ground Power Units | |||

| Others | |||

| By Application | Aircraft Handling | ||

| Passenger Handling | |||

| Cargo Handling | |||

| By Power Source | Electric | ||

| Non-Electric | |||

| Hybrid | |||

| By End User | Commercial | ||

| Military | |||

| By Ownership | Airport-Owned | ||

| Airline-Owned | |||

| GSV Service Providers/Lessors | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and expected growth of the airport ground support vehicles market to 2031?

The airport ground support vehicles market stands at USD 9.40 billion in 2026 and is projected to reach USD 11.91 billion by 2031 at a 4.88% CAGR.

Which regions are leading and growing fastest in airport ground support vehicles?

North America held 34.12% in 2025, while Asia-Pacific is the fastest growing at a 6.94% CAGR through 2031.

Which vehicle types and applications are most important over the forecast period?

Tugs and tractors led with 30.78% in 2025, and de-icing vehicles are the fastest growing at a 7.43% CAGR; aircraft handling led applications with 53.85% in 2025 and cargo handling grows at 6.61% CAGR

How is electrification changing airport ground operations procurement?

Electric variants grow at 9.55% CAGR while non-electric still dominates installed base, as mandates, incentives, and lower total cost of ownership push new orders toward battery platforms where charging capacity allows.

What ownership models are gaining share for ground support fleets?

Airline-owned fleets held 40.10% in 2025 as the legacy model, while service providers and lessors are expanding at a 6.64% CAGR with bundled maintenance and energy services.

Which risk factors could slow adoption of electric ground support vehicles?

High upfront costs, grid and charging constraints, and supply chain bottlenecks in batteries and semiconductors are the main brakes on adoption over the next two to four years.

Page last updated on: