Aircraft De-Icing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

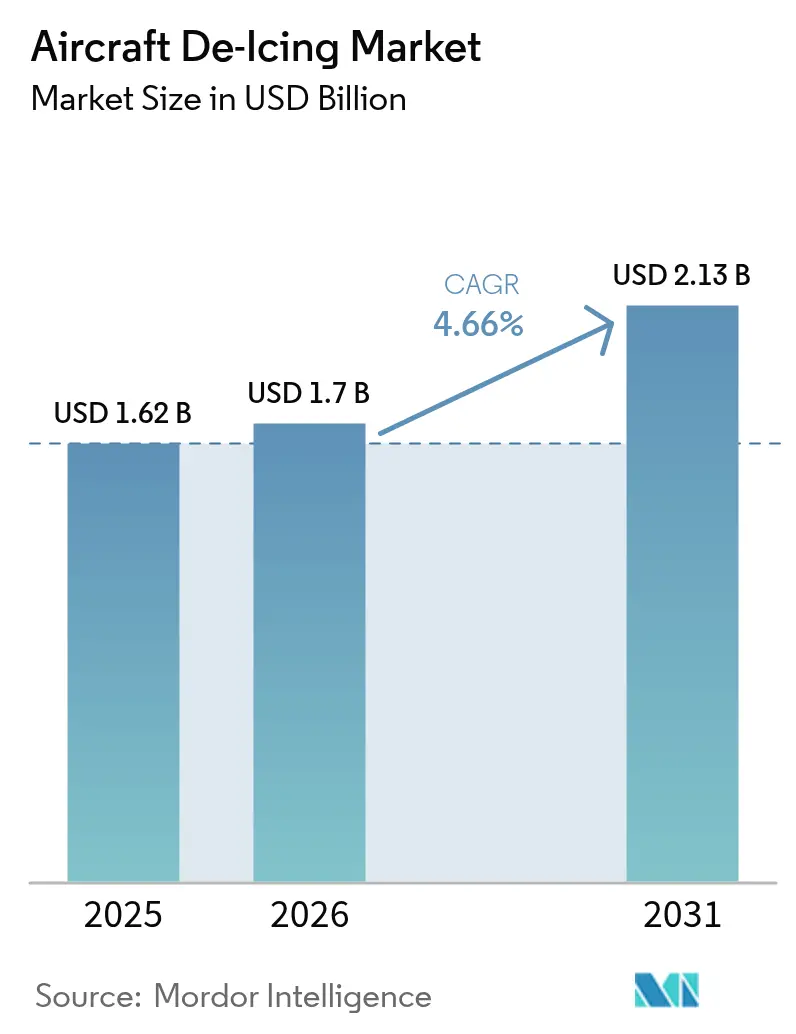

| Market Size (2026) | USD 1.7 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft De-Icing Market Analysis by Mordor Intelligence

Aircraft de-icing market size in 2026 is estimated at USD 1.7 billion, growing from 2025 value of USD 1.62 billion with 2031 projections showing USD 2.13 billion, growing at 4.66% CAGR over 2026-2031. The aircraft de-icing market benefits from larger winter flight schedules at secondary airports, stricter North America and Europe safety rules, and airport investments that favor permanent infrastructure and fluid-recovery systems. Stable demand from commercial airlines, rising e-commerce cargo traffic, and the spread of next-generation narrow-body fleets sustain baseline growth. At the same time, product mix is shifting toward electric equipment, fixed-boom gantry installations, and higher-performance Type IV fluids that extend holdover times. Opportunities are also opening around digital monitoring, predictive maintenance, and glycol-recycling technologies that cut costs and emissions while improving on-time performance. Competitive dynamics remain shaped by OEM electrification roadmaps, airport sustainability targets, and the economics of glycol supply and recovery programs.

Key Report Takeaways

- By end user, commercial airlines led with 45.88% revenue share in 2025; cargo airlines are forecast to grow the fastest at 6.34% CAGR to 2031.

- By equipment type, de-icing trucks held 53.95% of the aircraft de-icing market size in 2025, whereas fixed-boom/gantry systems are set to rise at 6.55% CAGR through 2031.

- By fluid type, Type II products dominated with a 31.74% share in 2025; Type IV is slated for the highest 6.63% CAGR between 2026 and 2031.

- By method, traditional fluid applications made up 80.95% of the aircraft de-icing market size in 2025, but hybrid systems will expand most rapidly at 7.12% CAGR over the forecast period.

- By region, North America commanded 62.20% of the aircraft de-icing market share in 2025, while Asia-Pacific is projected to expand at a 6.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft De-Icing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in winter flight schedules across secondary airports in Northern Latitudes | +1.2% | North America, Europe | Medium term (2-4 years) |

| Heightened safety-compliance penalties for ice-related incidents in EU and US | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Fleet growth of next-gen narrow-body jets with larger wing surface area | +0.8% | Global | Medium term (2-4 years) |

| Expansion of remote de-icing pads to reduce gate-hold times in Canada and Nordics | +0.7% | North America, Europe | Medium term (2-4 years) |

| Electrification initiatives and sustainable ground support equipment adoption | +0.6% | Global | Long term (≥ 4 years) |

| Military Arctic operations modernization in NATO and Russian far-north bases | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Winter Flight Schedules Across Secondary Airports in Northern Latitudes

Secondary airports in cold regions add winter routes that keep aircraft flying year-round. Regional carriers such as SkyWest carried 42 million passengers in the US in 2024. This illustrates how stronger winter utilization lifts demand for mobile de-icing units that can be stationed where permanent gantries are not yet viable. Smaller fields that once closed for part of the season now see traffic spikes, encouraging procurement of multi-purpose trucks and modular fluid tanks that fit constrained apron layouts. Equipment makers are responding with compact chassis, faster boom articulation, and digital spray-rate controls. Safety regulators are likewise paying closer attention to secondary airports, pushing operators to match the procedural rigor of major hubs. These factors raise unit volumes and after-market service opportunities across the aircraft de-icing market.

Heightened Safety-Compliance Penalties for Ice-Related Incidents in the EU and US

The Federal Aviation Administration’s updated ground-deicing guidance for winter 2024-2025 tightened holdover tables and application procedures, prompting airlines and service companies to modernize fleets and train crews to avoid fines. Parallel moves by the European Union Aviation Safety Agency reinforce the same message, classifying icing severity and mandating documented mitigation steps.[1]European Union Aviation Safety Agency, “Icing in Flight,” easa.europa.eu Compliance pressure is accelerating the adoption of sensor-based verification, barcode traceability of fluid batches, and real-time weather-linked decision tools. The aircraft de-icing market, therefore, sees rising demand for software licenses, handheld readers, and on-board cameras that validate spray patterns, expanding revenue streams beyond hardware.

Fleet Growth of Next-Generation Narrow-Body Jets With Larger Wing Surface Areas

Airbus delivered 766 jets in 2024, many with enlarged wings that require broader spray coverage. These aircraft lift fuel efficiency yet stretch legacy boom reach on standard trucks, pushing manufacturers to design high-lift scissor booms and telescopic nozzles. Larger surface areas also increase fluid consumption unless nozzles are optimized; consequently, operators deploy flow-meter feedback loops that adjust spray rate to real-time viscosity and temperature. Equipment with programmable logic controllers and electro-hydraulic stabilization thereby wins share, while research programs such as the Clean Aviation InSPIRe project validate embedded electro-thermal wing protection that could trim external de-icing cycles by 70%.[2]Clean Aviation Joint Undertaking, “InSPIRe Helps Break the Ice,” clean-aviation.eu

Expansion of Remote De-Icing Pads to Reduce Gate-Hold Times

Airports in Canada and the Nordic region are commissioning centralized pads along taxiways, guided by FAA Advisory Circular AC 150/5300-14D, to move de-icing away from gates and accelerate push-back sequences. Remote pads allow parallel processing of multiple aircraft, streamline fluid collection, and limit apron congestion. Transport Canada’s guidelines call for drainage designs that recapture glycol and cut chemical oxygen demand loads. As a result, the aircraft de-icing market gains from integrated gantry systems, underground piping, and high-capacity holding tanks, while service providers offer turnkey engineering, fluids management, and recycling contracts.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Ethylene and Propylene Glycol feedstock prices | -0.6% | Global | Short term (≤ 2 years) |

| Stringent waste-glycol run-off regulations elevating OPEX at US Class-B airports | -0.5% | North America | Medium term (2-4 years) |

| Airline cost-cutting leading to outsourcing price compression in Asia | -0.4% | Asia-Pacific | Medium term (2-4 years) |

| Infrastructure limitations for electric de-icing equipment deployment | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Ethylene and Propylene Glycol Feedstock Prices

Ethylene and propylene glycol prices follow upstream petrochemical swings, squeezing margins for fluid blenders and service providers. Cost spikes encourage airports to recycle spent fluid and airlines to vary concentration based on ambient conditions. St. Louis Lambert International’s 2024/2025 plan highlights blend-to-temperature dosing that reduces consumption in milder conditions. Some carriers hedge costs by contracting multi-year supply volumes, but smaller operators are more exposed, delaying equipment upgrades and limiting market growth in the short term.

Stringent Waste-Glycol Run-Off Regulations Elevating Operating Expenses

The US Environmental Protection Agency’s Airport Deicing Effluent Guidelines oblige facilities with over 1,000 jet departures to capture or treat 60% of effluent.[3]US Environmental Protection Agency, “Airport Deicing Effluent Guidelines,” epa.govCompliance requires separators, storage lagoons, and biological treatment systems that add a capital burden, especially for mid-tier Class-B airports. Clark County Department of Aviation’s environmental guidelines illustrate the procedural depth needed to avoid penalties. While larger hubs can amortize investments over high traffic, seasonal airports face steeper unit costs, dampening near-term equipment purchases and restraining growth in the aircraft de-icing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Commercial Dominance With Cargo Momentum

Commercial airlines held 45.88% of the aircraft de-icing market share in 2025, supported by global route networks that must maintain on-time departures during winter peaks. These carriers favor high-throughput truck fleets and automated mixing plants to tighten turnaround times. Though smaller today, Cargo airlines are expanding the aircraft de-icing market size fastest at a 6.34% CAGR through 2031 as e-commerce drives year-round demand for temperature-insensitive logistics. They often operate at night and in secondary hubs, prompting investments in self-contained de-icing rigs that can travel between airports. Military aviation, while niche, specifies ruggedized equipment for Arctic bases and rapid-deployment kits that perform in extreme cold. General aviation and business jets rely on flexible service models, including heated hangars and portable applicators, representing incremental but steady volume for suppliers.

Commercial carriers also influence fluid standards; their push for longer holdover times speeds the shift toward Type IV formulations. Cargo operators reinforce this trend because extended taxi and loading intervals increase the risk of fluid shear or re-freeze. Military users create spill-over benefits for civil operations by funding R&D in portable electro-thermal blankets and compact power systems that later migrate to regional airport applications. The cross-pollination of requirements keeps the aircraft de-icing market dynamic despite moderate headline growth.

By Equipment Type: Fixed-Boom Infrastructure Closing the Gap

De-icing trucks retained 53.95% of the aircraft de-icing market in 2025, thanks to their versatility and lower initial cost relative to permanent gantries. Modern designs integrate single-engine drivetrains, energy-efficient heaters, and touch-screen diagnostics, cutting fuel burn and maintenance downtime. However, airports with congested winter schedules are pivoting to fixed-boom or gantry systems that process multiple wide-body aircraft simultaneously. This sub-segment will advance at a 6.55% CAGR to 2031, raising its contribution to the aircraft de-icing market size and easing workforce constraints during peak storms. Tow-behind sprayers remain relevant for small airfields, while in-hangar solutions cater to MRO operations and corporate fleets.

Electrification overlays all categories. Vestergaard, Oshkosh, and Textron GSE now publish roadmaps targeting majority electric or hybrid deliveries before 2035, responding to airport carbon-reduction pledges. The shift redefines lifetime cost-of-ownership calculations, with energy price volatility and sustainability incentives tilting purchasing decisions toward battery-electric or hybrid hydraulic platforms. Suppliers that master high-voltage integration and cold-weather battery management will lock in long-term service revenue as customers phase out diesel units.

By Fluid Type: Type IV Advances on Type II Leadership

Type II fluids held 31.74% of consumption in 2025, balancing viscosity, sprayability, and cost. Still, Type IV volumes are accelerating at 6.63% CAGR as operators prioritize longer holdover windows during persistent precipitation. Because Type IV reduces the need for repeat applications, airlines weigh its higher unit cost against lower delays and fluid usage. Recycling programs further strengthen the economics, allowing airports to reclaim and concentrate glycol. Type I glycol-water blends remain indispensable for initial ice removal, yet their share will fall incrementally as anti-icing formulations improve. Type III products stay confined to turboprops and regional jets that need tailored shear performance.

Manufacturers are exploring bio-based glycols and additives that reduce toxicity and improve biodegradability. Clariant’s Safewing portfolio exemplifies this, offering full compliance with FAA and EASA specifications while reducing environmental loads. As regulations tighten, fluid producers demonstrating closed-loop life-cycle management—blend, apply, collect, regenerate—are best placed to capture value in the aircraft de-icing market.

By Method: Hybrid Systems Challenge Fluid Dominance

Fluid spray methods accounted for 80.95% of treatments in 2025; however, hybrid concepts combining ice-phobic coatings with electro-thermal heating will grow at a 7.12% CAGR through 2031. The ICE-WIPS program, led by Japan’s aerospace agency, showed a 70% power-consumption reduction versus legacy hot-bleed air solutions, making it attractive for regional jets and emerging electric aircraft. Infra-red bays and electro-impulse techniques address specific niches where chemical usage must be minimized, such as eco-sensitive locations or defense outposts with limited fluid logistics.

Forced-air systems bridge the gap by combining hot-air blast with lower glycol volumes, enabling airports to meet EPA discharge limits. Equipment vendors increasingly bundle multiple technologies—pre-heat bays, spot electro-thermal panels, and optimized spray heads—into integrated packages tailored to each customer’s climate profile. This convergence broadens supplier portfolios, deepens aftermarket service demand, and enlarges the aircraft de-icing market.

Geography Analysis

North America generated 62.20% of 2025 revenue, underpinning the aircraft de-icing market with its dense hub network, severe winters, and rigorous FAA oversight. Recent investments, such as Syracuse Hancock International Airport’s USD 19.4 million glycol-recycling plant, demonstrate regional commitment to sustainable operations and cost control. The facility is designed to reclaim fluid with glycol concentrations as low as 0.25%, generating up to 550,000 gallons of Type I solution annually. EPA effluent rules further drive adoption of collection systems and pad-based treatments, ensuring that North American demand remains anchored in regulatory compliance and technology refresh cycles.

Europe is the second-largest territory, shaped by EASA’s icing risk classification and the European Green Deal. Clean Aviation initiatives back next-generation wing-ice protection that can cut energy draw by 30% or more, creating fertile ground for suppliers of embedded electro-thermal elements and advanced coatings. Airports across Scandinavia and the Alps invest in remote pads and glycol capture to meet safety and environmental requirements, sustaining equipment orders even in a comparatively mature market.

Asia-Pacific is the clear high-growth frontier, posting a forecast 6.63% CAGR on the strength of expanding airport infrastructure in China, South Korea, and Japan. Many of these facilities are scaling from minimal winter activity to full-season operations, generating first-time purchases of trucks, storage tanks, and fluid bulk plants. Mountainous terrain in parts of China and Korea requires altitude-tolerant systems, while northern Chinese hubs face prolonged sub-zero periods that strain equipment heating capacity. Suppliers that offer modular, quickly deployable fleets and local service partnerships are winning early contracts, positioning the region as a rising share contributor to the aircraft de-icing market size.

Competitive Landscape

The aircraft de-icing market is moderately concentrated, with the top five manufacturers controlling just under 60% of global sales. Vestergaard and Oshkosh set the pace in high-end trucks and gantries, integrating electric drivetrains and telematics to lower lifetime emissions and boost fleet uptime. Oshkosh’s Tempest-i series illustrates the trend: single-engine powertrains, 39% fewer parts than earlier models, and rapid fluid heat-up that saves start-of-shift time. Vestergaard’s 7,600-liter e-MY Lite secures traction among regional airports pursuing noise and emission cuts.

Textron GSE, Clariant, and a cohort of regional players vie for volume in mid-market fleets and fluid supply contracts. Textron targets 75% electric or hybrid output by 2035, signaling strategic alignment with airport carbon goals. Meanwhile, specialized firms such as Cox & Company convert aerospace patents into OEM supply modules, offering hybrid thermal-mechanical de-icing subsystems for wing leading edges. Digital service layers, predictive maintenance dashboards, fluid consumption analytics, and compliance reporting are emerging as competitive differentiators, locking customers into long-term support agreements and recurring software fees.

White-space opportunities persist in growth markets where air service is extending into winter climates for the first time. Suppliers able to deliver bundled solutions, equipment, fluids, training, and recycling as a managed service model are capturing these openings. Collaboration with airport authorities also paves the way for public-private funding of centralized pads and treatment plants, further enlarging addressable demand within the aircraft de-icing market.

Aircraft De-Icing Industry Leaders

Oshkosh Corporation

Vestergaard Company

Global Ground Support LLC

Weihai Guangtai Airport Equipment Co., Ltd.

TUG TECHNOLOGIES CORPORATION (Textron, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Airbus issued its “Pioneering Sustainable Aerospace” manifesto, noting that 30% of the in-service fleet now consists of latest-generation aircraft, a shift that alters wing geometries and de-icing coverage requirements.

- April 2025: Emirates Group’s FY2025 report stated that Emirates SkyCargo uplifted 2.3 million tons, reinforcing cargo’s growing share of winter operations that demand consistent de-icing readiness

- October 2024: Equipmake partnered with Textron Ground Support Equipment Inc. (Textron GSE) to develop an all-electric version of its airport de-icing vehicle. Equipmake provides automotive solutions for trucks, buses, and specialty vehicles, while Textron GSE manufactures airport ground support equipment.

- September 2024: Vestergaard Company introduced the OPTIM-ICE operator-assisted deicing system for narrowbody aircraft wings and stabilizers. The system incorporates LIDAR technology to scan aircraft surfaces and identify appropriate deicing patterns. The software automates nozzle movements according to pre-selected patterns while supporting operator control. The company plans to expand the system's capabilities to include enhanced automation features and compatibility with additional aircraft types.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft de-icing market as yearly revenues from purpose-built ground equipment and certified glycol-based or alternative fluids used to clear or prevent frozen contamination on an aircraft's critical external surfaces before flight. Coverage spans mobile trucks, fixed gantry systems, in-hangar units, tow-behind sprayers, and bulk fluid sales across commercial, cargo, business, and military aviation operations worldwide.

We deliberately leave out runway pavement chemicals, snow-removal vehicles, and any in-flight ice-protection systems.

Segmentation Overview

- By End User

- Commercial Airlines

- Cargo Airlines

- Military Aviation

- General Aviation and Business Jets

- By Equipment Type

- De-icing Trucks (Mobile)

- Fixed-Boom/Gantry Systems

- Tow-Behind Sprayers

- In-Hangar De-icing Systems

- By Fluid Type

- Type I (Glycol-Water)

- Type II

- Type III

- Type IV

- By Method

- De-icing with Fluids

- Infra-red/Electro-Impulse

- Forced-Air/Hot-Air

- Hybrid Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Russia

- France

- Germany

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Australia

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- South America

- Brazil

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ground operations managers, fluid formulators, and equipment engineers in North America, Europe, and Asia-Pacific. These conversations validated typical service tariffs, fleet utilization during peak storms, and emerging shifts toward electric trucks and PFAS-free fluids, closing gaps left by secondary work.

Desk Research

We began by compiling open data from FAA, EASA, and Transport Canada directives, airport movement statistics, United Nations Comtrade glycol trade codes, and SAE G-12 papers. Company 10-Ks, investor decks, and patent filings mined through Questel enriched supply cues, while shipment traces on Volza and tender notices on Tenders Info anchored average selling prices. News archives via Dow Jones Factiva rounded out trend context. The sources listed illustrate the breadth consulted; many additional references supported data checks and clarifications.

Market-Sizing & Forecasting

We start with a top-down construct that multiplies winter scheduled departures by calibrated de-icing incidence rates and average fluid or equipment spend, producing the initial demand pool. Supplier roll-ups and sampled contract values supply a selective bottom-up cross-check; mismatches are reconciled through weighted adjustments. Key drivers include flight movements, liters of fluid per turn, truck replacement cycles, glycol price indices, and regulation timelines. Multivariate regression with scenario analysis projects the base case through 2030, while expert consensus refines elasticity for harsh or mild-winter scenarios.

Data Validation & Update Cycle

Our outputs pass a three-tier analyst review in which anomalies against historic safety bulletins or airport procurement budgets trigger re-work. Models refresh each year, with interim updates when major weather events, regulatory shifts, or material M&A alter assumptions. Clients therefore receive the latest vetted view at delivery.

Why Mordor's Aircraft De Icing Baseline Resists Seasonal Swings

Published estimates often diverge because firms vary in whether they count runway chemicals, assume fixed currency rates, or roll multi-year contracts into a single season.

Mordor's disciplined scope, dual-path estimation, and annual refresh temper such swings and ground the baseline in observable variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.62 Bn (2025) | Mordor Intelligence | - |

| USD 1.67 Bn (2024) | Regional Consultancy A | Includes runway chemical revenue and uses contract-year dollars |

| USD 1.24 Bn (2023) | Trade Journal B | Excludes equipment sales and relies on pre-recovery flight schedules |

| USD 1.41 Bn (2024) | Global Consultancy C | Holds glycol prices constant and omits currency inflation adjustments |

The comparison shows that Mordor's transparent variables, balanced cross-checks, and timely updates yield a dependable, decision-ready baseline for industry stakeholders.

Key Questions Answered in the Report

What is the current value of the aircraft de-icing market?

The aircraft de-icing market is valued at USD 1.7 billion in 2026 and is projected to reach USD 2.13 billion by 2031, reflecting a 4.66% CAGR.

Which region leads the aircraft de-icing market?

North America accounts for 62.20% of 2025 revenue, supported by extensive airport infrastructure and strict FAA regulations.

Which equipment category is growing fastest?

Fixed-boom or gantry systems are expected to rise at a 6.55% CAGR through 2031 as airports invest in permanent, high-throughput infrastructure.

Why are Type IV fluids gaining popularity?

Type IV fluids provide longer holdover times than Type II, reducing repeat applications and supporting on-time departures during continuous snowfall.

How are regulations influencing the market?

Updated FAA and EPA rules, along with EASA directives, are driving investments in advanced monitoring, glycol capture, and electric de-icing equipment.

What role does electrification play in future growth?

Manufacturers aim to supply majority electric or hybrid fleets by 2035, aligning with airport carbon targets and creating new total-cost-of-ownership advantages.

Page last updated on: