Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

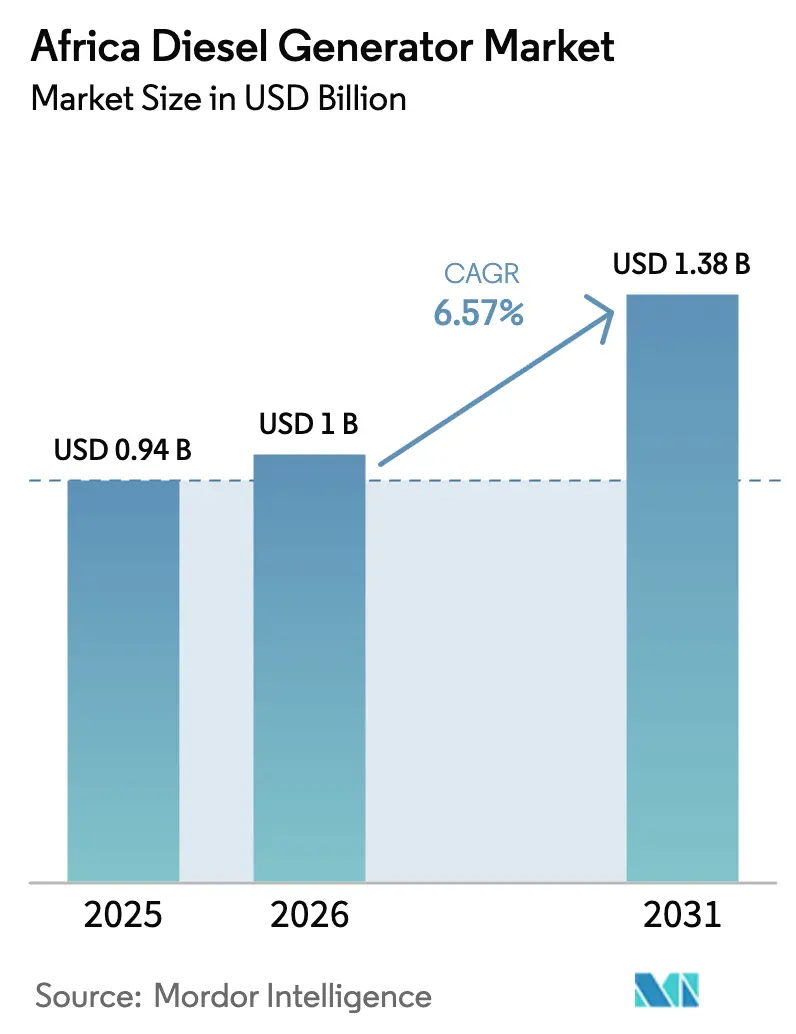

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Diesel Generator Market Analysis by Mordor Intelligence

Africa Diesel Generator Market size in 2026 is estimated at USD 1 billion, growing from 2025 value of USD 0.94 billion with 2031 projections showing USD 1.38 billion, growing at 6.57% CAGR over 2026-2031.

This growth curve reflects entrenched structural power-supply deficits, with Sub-Saharan grids experiencing an average of 56 hours of monthly outages in 2024, compelling enterprises to self-insure through captive generation.(1)Afrobarometer, “Grid Outages and Power Reliability in Sub-Saharan Africa,” afrobarometer.org At the same time, 12 newly commissioned Tier III and Tier IV data-center facilities in Nigeria, Kenya, and South Africa adopted multi-megawatt standby arrays that overwhelmingly favor diesel over gas due to limited pipeline infrastructure.(2)Digitalisation World, “Caterpillar Joins Africa Data Centres Association,” digitalisationworld.com Telecom-tower densification added 8,200 sites across Nigeria and Kenya during 2024, most designed around hybrid diesel-solar microgrids where grid extension remains uneconomic. Together, these vectors keep the African diesel generator market front-of-mind for investors looking to capitalize on resilient power demand in a continent grappling with chronic grid unreliability.

Key Report Takeaways

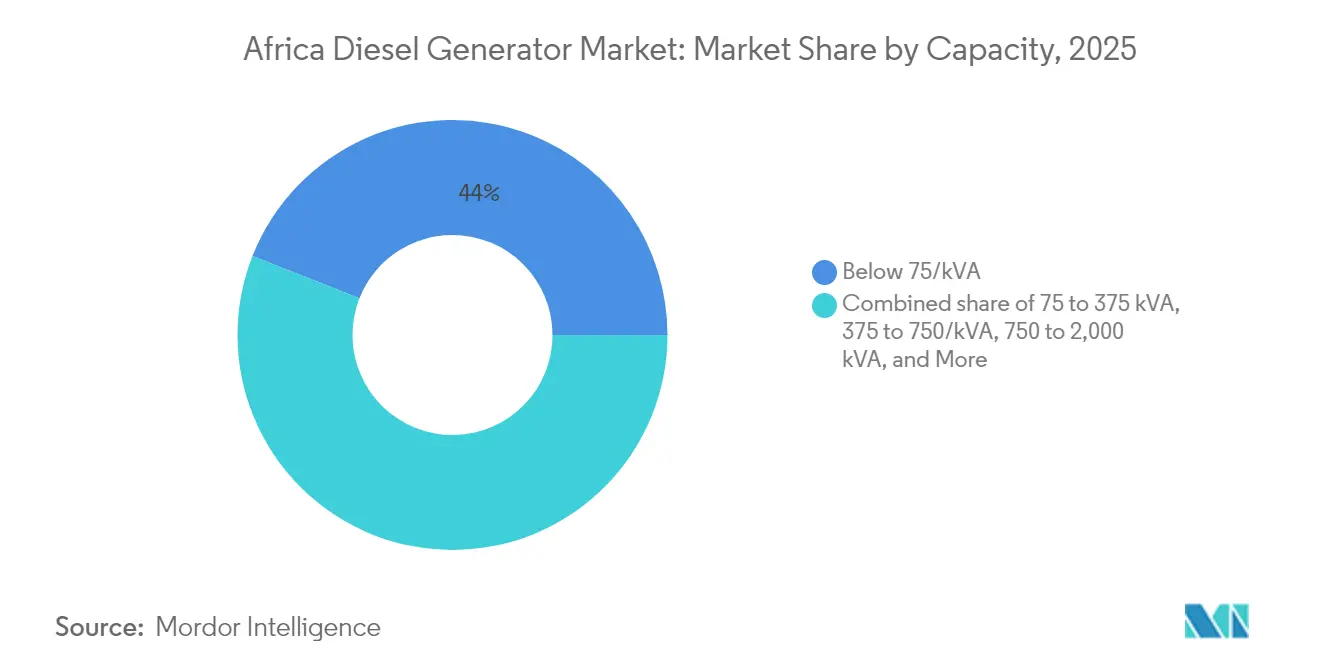

- By capacity, units below 75 kVA led with a 44.02% revenue share of the African diesel generator market in 2025, while the 375-750 kVA band is forecast to grow at an 8.45% CAGR through 2031.

- By application, standby and backup power commanded a 63.25% share in 2025; peak-shaving and load-management deployments are projected to advance at a 7.86% CAGR through 2031.

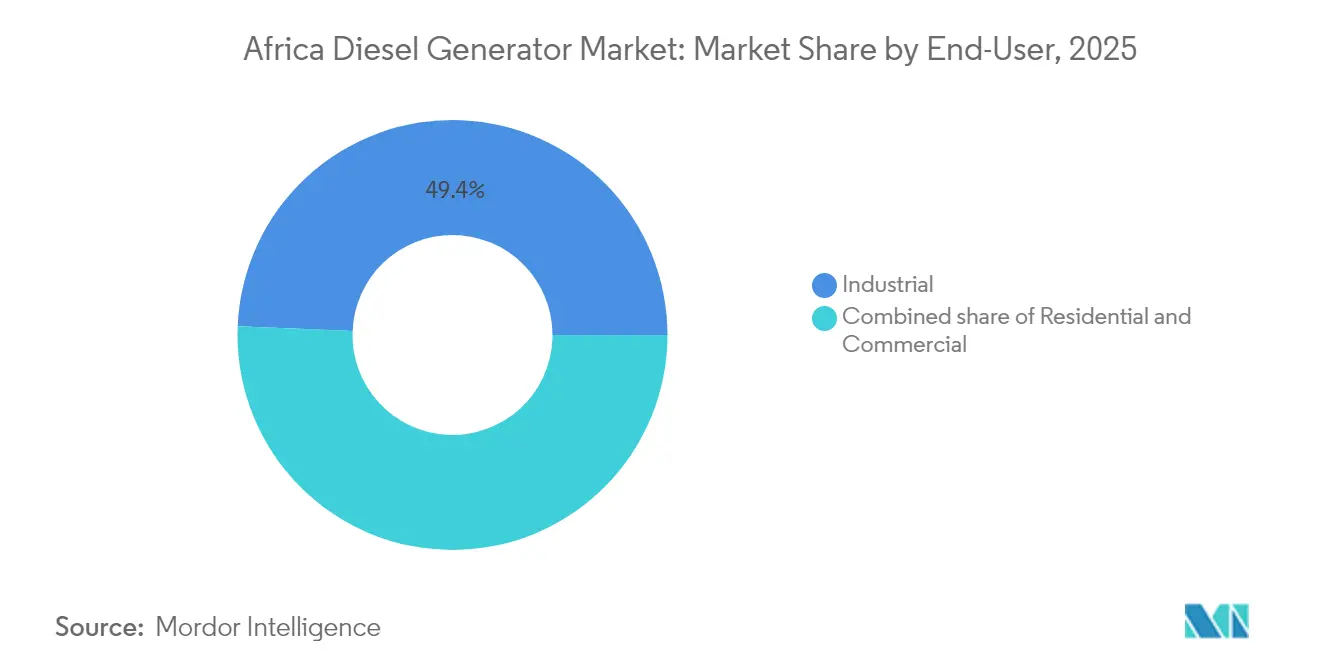

- By end user, industrial customers accounted for a 49.35% share in 2025, while the commercial segment is projected to expand at an 8.14% CAGR to 2031.

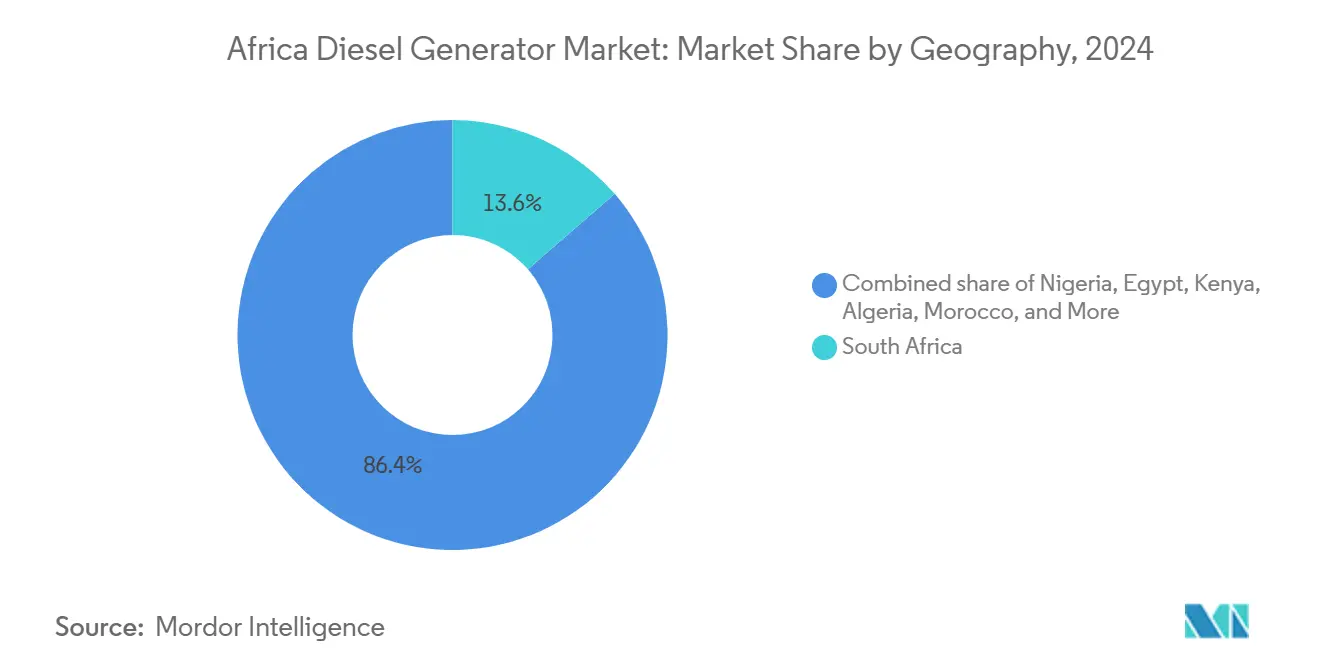

- By geography, South Africa contributed a 13.45% revenue share in 2025, whereas Nigeria is forecast to post the fastest growth of 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency of grid outages | +1.2% | Nigeria, Kenya, South Africa, Rest of Sub-Saharan Africa | Medium term (2-4 years) |

| Data-center build-out (Tier III / IV) | +1.5% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Telecom-tower densification | +0.9% | Nigeria, Kenya, Rest of Africa | Medium term (2-4 years) |

| Mining shift to captive power | +0.8% | DRC, Zambia, Tanzania, South Africa | Long term (≥ 4 years) |

| Corporate demand for HVO-ready gensets | +0.6% | South Africa, Nigeria, Kenya | Medium term (2-4 years) |

| AfCFTA-driven cross-border rental fleets | +0.5% | Pan-African | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency of Grid Outages in Sub-Saharan Africa

Persistent grid unreliability anchors demand across the Africa diesel generator market, with 34 countries averaging 56 hours of monthly outages in 2024. Nigeria’s grid collapsed 12 times during the first half of the year, forcing industrial users to run gensets in prime-power mode, which accelerates wear and shortens replacement cycles. Kenya’s electrification drive connected 1.2 million households, yet voltage fluctuations remain endemic, motivating peri-urban buyers to install small diesel units.(3)World Bank, “Energy Access and Grid Reliability in Africa,” worldbank.org South Africa endured Stage 6 load-shedding for 118 days, prompting hospitals, data centers, and factories to deploy permanent backup arrays sized for 8-12 hours of autonomous runtime. Under-funded utilities defer grid upgrades, creating a self-reinforcing loop that keeps diesel a default hedge against supply risk for the coming decade.

Rapid Build-Out of Data-Center Capacity Across Nigeria, Kenya & South Africa

Hyperscale and colocation operators commissioned 12 Tier III and Tier IV sites in 2024, each requiring 2-10 MW of N+1 or 2N diesel redundancy. Caterpillar joined the Africa Data Centres Association in 2024, signaling OEM confidence that cloud providers view diesel as the most bankable standby option where gas infrastructure is absent. Microsoft and Equinix announced new campuses in South Africa and Kenya, citing the need for low latency and favorable power purchase structures that bundle grid supply with on-site diesel. Uptime Institute rules mandate concurrent maintainability, practically locking in high-specification diesel arrays that can black-start within 10 seconds. While operators explore battery ride-through solutions, diesel retains a 5-7-year advantage for multi-megawatt backup, cementing its place at the heart of the Africa diesel generator market.

Telecom-Tower Densification for 4G & 5G Roll-Outs

TowerXchange recorded 8,200 new tower sites across Nigeria and Kenya in 2024, with 72% of these sites operating hybrid diesel-solar power systems.(4)African Review, “Perkins Engines: Strengthening the Core,” africanreview.com Caterpillar released a modular microgrid solution that claims up to 80% diesel savings by integrating solar PV, storage, and a right-sized genset, marketed under Energy-as-a-Service contracts. MTN Nigeria and Airtel Kenya both signed performance-guaranteed tower-power agreements in 2024, shifting capital expenditure (capex) to operational expenditure (opex) and transferring fuel-price risk to suppliers. GSMA noted a 6.8% growth in African mobile subscribers and a 42% surge in data traffic, ensuring a steady pipeline of new tower sites that will rely on diesel-centric hybrids for reliable uptime.(5)GSMA, “Mobile Economy Africa 2024,” gsma.com Limited regulatory oversight for rural towers allows uptime and total cost of ownership to outweigh emissions concerns, reinforcing diesel’s relevance across the Africa diesel generator market.

Mining Sector’s Shift from Grid to Captive Power in Central & Southern Africa

Copper, cobalt, and gold miners in the DRC, Zambia, and Tanzania are unplugging from unreliable grids to ensure 24/7 processing power. Atlas Copco expanded its rugged QES line up to 500 kVA in 2024, specifically addressing the mobility and synchronization demands of mining contractors. Aggreko’s 8 MW flare-to-power project in Egypt converted waste gas into captive power generation, saving USD 25 million and setting a template for African miners looking to monetize off-gas. With grid tariffs above USD 0.12/kWh and chronic voltage instability, miners prefer diesel generators in the 750-2,000 kVA range for critical loads. Rising battery-mineral demand worldwide keeps the Africa diesel generator market exposed to sustained prime-power sales from the mining vertical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar-battery hybrids reaching price parity | -1.1% | South Africa, Kenya, Nigeria | Short term (≤ 2 years) |

| Diesel import-price volatility post-IMO reforms | -0.7% | All African markets | Medium term (2-4 years) |

| Stricter emission caps in South Africa & Nigeria | -0.6% | South Africa, Nigeria | Medium term (2-4 years) |

| Gas-fired small-modular turbines > 2 MW | -0.5% | Nigeria, Egypt, Algeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Price Parity of Solar-Plus-Battery Hybrids

Utility-scale solar with four-hour lithium-ion storage now delivers power at USD 0.15-0.18 /kWh in high-insolation African regions, outcompeting diesel’s USD 0.22-0.28 operating cost for continuous duty. Malawi’s 2024 decision to replace Aggreko diesel rentals with a grid-scale battery underscores shifting economics and sends a cautionary signal to rental operators in the Africa diesel generator market. For standby uses with less than 500 runtime hours annually, solar-battery systems with six-hour autonomy already outperform diesel on total cost of ownership, potentially threatening future replacement sales.

Stricter Emission Caps in South Africa and Nigeria

South Africa’s NEM: AQA and Nigeria’s NESREA tightened particulate-matter and NOx limits for new gensets above 560 kW in 2024, effectively mandating Tier 4 Final or Stage V compliance. Compliance adds USD 8,000-15,000 per genset for SCR and DPF systems and requires a consistent diesel exhaust fluid supply, a challenge in remote regions. Municipalities issued fines of up to USD 108,000 for non-compliant fleets, prompting large buyers to delay purchases or explore gas turbines when gas is readily available. This regulatory friction slows mid-range unit turnover and tempers growth across the Africa diesel generator market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Small Units Dominate, Mid-Range Accelerates

Below 75 kVA gensets captured 44.02% of the 2025 revenue, reflecting mass adoption by urban households, corner stores, and telecom base stations that require 10-50 kW of backup power during persistent load shedding, this category is highly fragmented, served by Chinese and Indian brands competing on upfront price. Units in the 75-375 kVA bracket accounted for roughly 29.72% of the Africa diesel generator market share in 2025, supplying hospitals, malls, and hotels that favor quieter, enclosed sets with improved fuel efficiency.

The 375-750 kVA range is forecast to advance at an 8.45% CAGR, the fastest of any band, driven by data centers, mining, and large telecom hubs that require scalable, parallel-ready packages. Atlas Copco’s June 2024 QES launch directly targets this segment with features that enhance synchronization and ruggedization. Higher ratings between 750 kVA and 2 MW serve utilities, smelters, and petrochemical complexes that prioritize total life-cycle cost and emission compliance over sticker price. Perkins’ forthcoming 2606 Series engine addresses this upper-mid tier with HVO compatibility and extended maintenance intervals. Above 2 MW, gas-fired turbines begin to erode diesel demand; yet, diesel persists where fuel logistics or transient loads favor piston engines, keeping this slice pertinent to the broader African diesel generator market.

By Application: Backup Dominates, Peak-Shaving Gains Traction

Standby and backup duty accounted for 63.25% of 2025 demand, demonstrating diesel’s entrenched role as insurance against grid collapse, especially for mission-critical loads that require black-start reliability within seconds. Data centers, hospitals, and banking facilities invest heavily in redundant arrays that may operate for only a few hundred hours per year yet represent significant capital expenditures.

Prime and continuous power use spans off-grid mining, remote telecom, and isolated industrial operations that run gensets 6,000-8,000 hours annually. Rising solar-battery parity pressures this usage bracket, yet a lack of storage depth and harsh ambient conditions preserve diesel relevance in many locales. Peak-shaving and load-management deployments are growing at 7.86% CAGR as South Africa and Nigeria expand time-of-use tariffs that penalize high daytime draw. Here, DERMS-enabled gensets enable facility managers to arbitrage tariffs and participate in grid-service markets, positioning diesel generators as active grid assets rather than passive insurance, an emerging narrative within the African diesel generator market.

By End User: Industrial Core, Commercial Upswing

Industrial players, including miners, manufacturers, and oil and gas companies, held a 49.35% share of the African diesel generator market size in 2025, driven by captive power needs where grid availability or quality fails to meet process-reliability thresholds. Aggreko’s Egypt flare-to-power showcase demonstrates how industrial buyers can leverage hybrid diesel-gas strategies to simultaneously reduce costs and emissions.

Commercial customers, data centers, hotels, hospitals, and malls are projected to expand at an 8.14% CAGR, outpacing industrial growth as service-sector GDP rises faster than manufacturing output in key economies. Data-center proliferation alone adds multi-megawatt backup opportunities. Residential uptake, though smaller in value terms, maintains volume momentum for sub-30 kVA imports, especially in Nigeria and South Africa. Together, these patterns diversify end-user exposure and prolong the diesel demand baseline across the African diesel generator industry.

Geography Analysis

Nigeria anchors a 8.92% CAGR outlook, founded on chronic grid collapses, 12 events in the first six months of 2024 alone, and a rapid telecom-tower rollout that added 4,800 new hybrid-powered sites. Oil-field flaring regulations also catalyze on-site generation projects that favor large diesel or dual-fuel gensets, reinforcing revenue visibility for suppliers.

South Africa retained 13.45% of the 2025 market share, despite having a comparatively advanced grid architecture, largely due to Eskom’s record 118 days of Stage 6 load-shedding. Stricter NEM: AQA standards elevate capex for compliant units above 560 kW, but corporate buyers still prefer Tier 4 Final equipment to mitigate reputational risk. Solar-battery parity at USD 0.18/kWh introduces substitution in prime-power niches, yet diesel remains the standby gold standard, thus maintaining South Africa’s pivotal role within the African diesel generator market.

Kenya, Egypt, Algeria, and Morocco form a rising second tier in spending. Kenya gained four new Tier III data centers in 2024, Egypt’s rail modernization and oil projects drive steady demand, and AfCFTA tariff relief enables Algerian and Moroccan contractors to source gensets duty-free from pan-African rental fleets. The wider Rest-of-Africa cohort, including DRC, Zambia, Tanzania, and Côte d’Ivoire, benefits from mining and infrastructure ventures that lack fuel pipelines and therefore lean on diesel, preserving geographic breadth for the Africa diesel generator market.

Regulatory Landscape

Regulation affecting diesel generator procurement in Africa is shaped by national environmental rules alongside continent-level standardization and efficiency initiatives. In 2024, South Africa administered tighter particulate and NOx limits for new gensets above 560 kW under NEM:AQA, while Nigeria tightened requirements via NESREA, pushing larger standby packages toward higher-emissions-control configurations and raising the compliance focus for Tier 1 OEMs and major buyers.

On harmonization, the African Electrotechnical Standardization Commission (AFSEC), operating under the African Energy Commission (AFREC), is a key platform for aligning electrotechnical standards across AU member states. The AU also advanced energy-efficiency policy via the African Energy Efficiency Strategy and Action Plan adopted in December 2024, with MEPS handbook and implementation guidance work scheduled for 2025-2028, which can tighten product and documentation requirements over time. Trade and tariff administration remains country-specific, with reference points such as Nigeria Customs Service import and export procedures (2025) and South Africa ITAC activity, including the March 2026 Gazette-linked workstream on tariff structures in energy-related value chains, reinforcing the need for correct tariff classification and local compliance planning for imported power equipment.

Competitive Landscape

Multinational OEMs, including Caterpillar, Cummins, Atlas Copco, Kohler, Wärtsilä, and Perkins, collectively held a 45% share through branded dealers and rental fleets that bundle installation, telemetry, and multi-year service contracts. Regional assemblers and Chinese manufacturers dominate sub-200 kVA sales, where price eclipses emission compliance, fragmenting the lower tiers of the Africa diesel generator market.

Tier 1 OEMs differentiate themselves through technology: Caterpillar’s 2024 hybrid microgrid for telecom towers promises up to an 80% fuel reduction, while Perkins’ 2606 Series engine combines HVO compatibility with extended 1,000-hour service intervals. Aggreko and APR Energy leverage AfCFTA’s tariff cuts to redeploy fleets pan-continentally, squeezing local rental firms on large infrastructure bids.

Emerging threats center on solar-battery integrators that are expected to reach cost parity for many duty cycles in 2024, and on small, modular gas turbines exceeding 2 MW in gas-rich markets. OEM response includes hybrid packages, digital asset management, and ESG-aligned fuel flexibility to protect share in the Africa diesel generator market.

Africa Diesel Generator Industry Leaders

Cummins Ltd.

Caterpillar Inc.

Atlas Copco AB

Aggreko PLC

AKSA Power Generation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is hybridization of installed diesel power assets, supported by utility and public-sector efforts to reduce fuel bills while keeping dispatchable capacity. In July 2026, Kenya’s Rural Electrification and Renewable Energy Corporation (REREC) approved integrating solar into 20 existing diesel power plants, explicitly linking the program to annual fuel expenditure above KES 1.16 billion, which creates a defined retrofit pipeline for controls, storage, right-sized gensets, and long-term service. A similar utility-led pathway is forming in North-West Africa, where John Cockerill signed a July 2026 contract with SOMELEC in Mauritania to hybridize ten thermal power plants with solar and battery storage, targeting a 3 million liter annual diesel reduction. This shifts the opportunity toward hybrid controls, synchronization, and aftersales capability rather than diesel-only supply.

Mining and other remote industrial loads continue to procure prime and base-load generation where grid extension is uneconomic. This sustains demand for containerized and modular diesel plants, and for refurbishment-led solutions, such as USP&E supplying 25 MW of diesel-fired base-load power using refurbished Wabtec GE16V250 generator sets to the Zondereinde mine in South Africa (February 2026), and MechVolt Power executing 500 kW containerized diesel deliveries with a 500 kW commissioning partnership in Zambia’s Copperbelt (June 2026). Alongside prime-power deployments, grid-connected renewables raise the value of fast-start standby and peaking capability at mission-critical sites, reinforcing opportunities for OEMs and rental fleets that can offer compliant gensets bundled with storage, microgrid controllers, and performance-based O&M across Nigeria, Kenya, South Africa, and mining corridors in Central and Southern Africa.

Recent Industry Developments

- June 2026: Cummins Power Generation introduced new QSK78 engine-based generator sets for 50 Hz markets, positioning the line for large, mission-critical applications such as data centers. The launch improves high-capacity product availability in Africa where pipeline gas access is limited and black-start requirements keep diesel as the default standby architecture.

- April 2026: Cummins launched a battery energy storage system (BESS) offering for the Southern African market and installed a C1500B5ZE BESS unit at its Midrand head office microgrid. Adding storage to the portfolio supports hybrid configurations that reduce diesel runtime while protecting uptime for commercial and industrial customers facing load shedding.

- June 2024: Atlas Copco expanded its QES mobile diesel generator range up to 500 kVA, adding features oriented to synchronization and rugged rental use in mining and construction. The move reinforced competitive intensity in the mid-range segment used for parallel operation and temporary power, where serviceability and fleet utilization influence purchasing decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers diesel generator sets sold and installed across Africa, measured in revenue terms. The view includes units used for prime power and backup power where diesel is the fuel type and the generator is a stationary power solution.

Scope exclusions: Portable diesel generators, gasoline or gas gensets, and non-generator power sources (such as batteries and solar inverters) are not counted.

Segmentation Overview

- By Capacity (kVA)

- Below 75 kVA

- 75 to 375 kVA

- 375 to 750 kVA

- 750 to 2,000 kVA

- Above 2,000 kVA

- By Application

- Stand-by/Backup Power

- Prime/Continuous Power

- Peak-shaving/Load Management

- By End User

- Residential

- Commercial

- Industrial

- By Geography

- Nigeria

- South Africa

- Egypt

- Kenya

- Algeria

- Morocco

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand context for gensets in Africa and then checking what can be supported with public series. We reviewed sources such as the World Bank (electrification rates, access, and macro indicators), IEA and IRENA publications (power system context), national electricity regulator and utility dashboards where available (outage and supply gaps), UN Comtrade for trade flows using generator-related HS codes, and African Development Bank energy and infrastructure reports.

To translate this context into a workable sizing model, we also used company annual reports and investor presentations. We reviewed customs and port notes as cited in reputed press, and we checked public tender portals to understand procurement patterns. In addition, paid subscriptions for company financials and intelligence, shipment-level import-export data, and patent databases were used selectively to cross-check product mix, pricing direction, and supplier footprints. These desk sources are illustrative, and many other public and paid references were consulted to fill gaps and validate assumptions.

Primary Interviews and Surveys

Primary work was used to pressure-test demand drivers and pricing, because Africa often has uneven reporting by country and project type. We spoke with a mix of generator OEM-side teams, distributor and rental channel participants, EPC and contractor contacts, and end users across telecom, mining, construction, commercial buildings, and public infrastructure, with coverage spread across major African sub-regions.

These conversations helped confirm typical kVA buying ranges, the split between backup and prime usage, and how diesel price movement and currency conversion tend to show up in quoted prices and realized revenue.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 41% | |

| Smaller Players: 22% | Managers: 46% |

Market-Sizing & Forecasting

The sizing logic is built from a top-down demand pool view, where power reliability and user need are converted into generator demand by country and then rolled up to an Africa total. The totals are then checked with selective bottom-up approximations, such as sampled ASP x unit volumes for common kVA bands and channel checks on distributor throughput, and adjustments are made when the two views disagree.

Inputs used in the model include grid reliability and electrification signals, diesel fuel pricing direction, project activity in construction and infrastructure, mining output indicators, telecom tower additions, and the typical replacement cycle for backup gensets. Where public data is patchy, gaps are handled by using proxy indicators (like GDP by sector and import trend patterns) and then reconciling them with interview-based normalization factors.

For forecasting, scenario analysis is applied with country-level demand drivers and fuel and currency sensitivities, followed by a smoothing step to avoid unrealistic jumps in unit demand or ASPs. The final outlook is reviewed against expected build activity, outage expectations, and likely procurement timing for large projects.

Data Validation & Update Cycle

Model outputs are validated through multiple checks, including consistency against trade trend direction, country demand signals, and the implied unit volumes behind the revenue totals. When a country line item looks abnormal, the drivers are revisited, and follow-up calls are triggered to confirm whether it is a real shift or a data artifact.

Before sign-off, the work goes through step-by-step analyst review so assumptions, conversions, and country roll-ups are consistent across the file. Reports are refreshed annually, and interim updates are made when there are material events such as currency moves, fuel shocks, or policy changes that can quickly change purchase behavior. Right before delivery, a final pass is completed so clients receive the most current view.

Mordor Intelligence's Africa Diesel Generator Market Estimate Compared With Other Published Estimates

Published market sizes for Africa diesel generators can look far apart, even when the topic sounds the same at first glance. This usually comes from differences in the year used, which currencies are applied and when they are converted, and whether pricing is modeled as a stable average or allowed to move with fuel and local tender realities.

In this study, the refresh cadence and the timing of FX and ASP updates are treated as first-order inputs, which helps avoid overstating revenue during sharp currency swings, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.00 B (2026) | |

| Regional Consultancy A | USD 1.20 B (2024) | Uses an earlier base year and may not fully normalize currency conversion timing across African markets, which can inflate the USD total when local currencies later weaken. |

| Industry Publisher B | USD 1.70 B (2032) | Uses a longer horizon and can assume smoother ASP progression, which may not reflect tender-driven pricing resets and the mix shift between backup and prime power in different countries. |

The spread is mostly explained by year alignment and how pricing and currency are handled, rather than by a single demand assumption. By keeping the market tied to repeatable signals like outage need, sector activity, and realistic ASP movement, the final number stays traceable and easier to reconcile across countries.

Key Questions Answered in the Report

How large is the Africa diesel generator market today?

The Africa diesel generator market size reached USD 1 billion in 2026 and is set to hit USD 1.38 billion by 2031.

What is the expected growth rate through 2031?

A forecast CAGR of 6.57% drives expansion as grid-reliability problems persist.

Which capacity band is growing the fastest?

Gensets rated 375-750 kVA are forecast to post an 8.45% CAGR, buoyed by mining and data-center demand.

Why is Nigeria the fastest-growing geography?

Monthly grid collapses, tower densification and flaring-to-power investments push Nigeria toward a 8.92% CAGR.

How are emission rules shaping procurement choices?

South Africa's NEM:AQA and Nigeria's NESREA now require Tier 4 Final compliance above 560 kW, driving buyers to premium OEMs with after-treatment expertise.

Will solar-battery hybrids displace diesel soon?

Solar-battery systems already beat diesel on cost in select standby use cases, but diesel remains dominant for multi-megawatt, instant-start backup where storage depth is still insufficient.

Page last updated on: