Aerospace Flexible Metal Hose Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

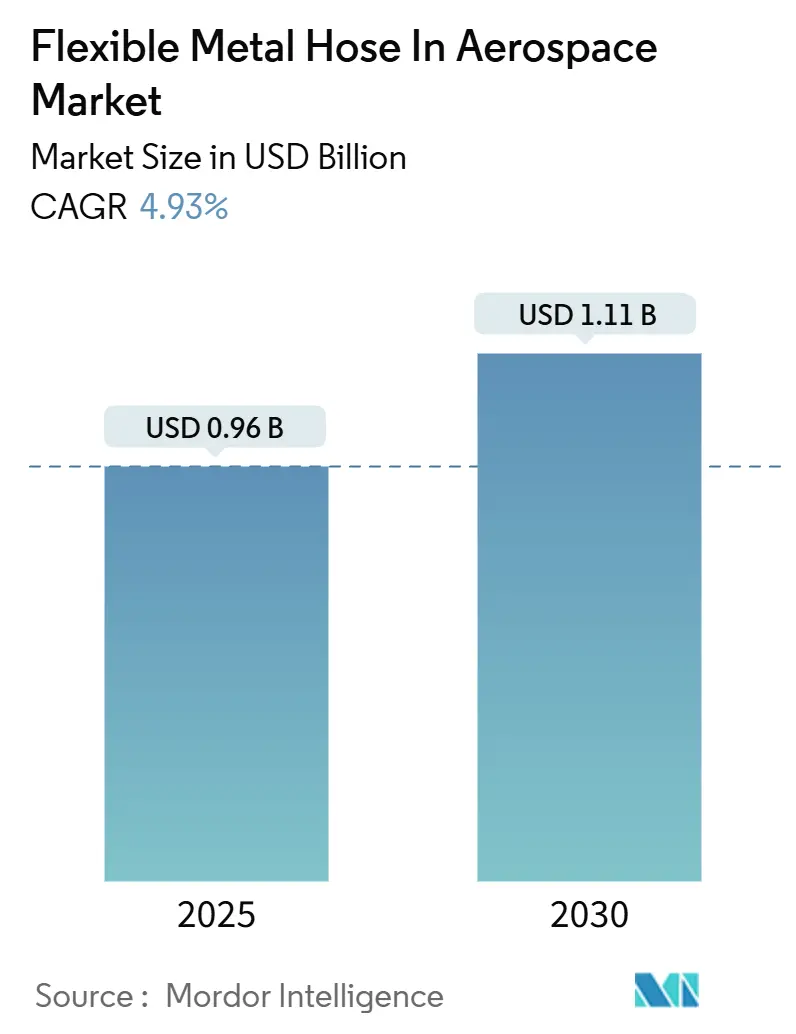

| Market Size (2025) | USD 0.96 Billion |

| Market Size (2030) | USD 1.11 Billion |

| Growth Rate (2025 - 2030) | 4.93% CAGR |

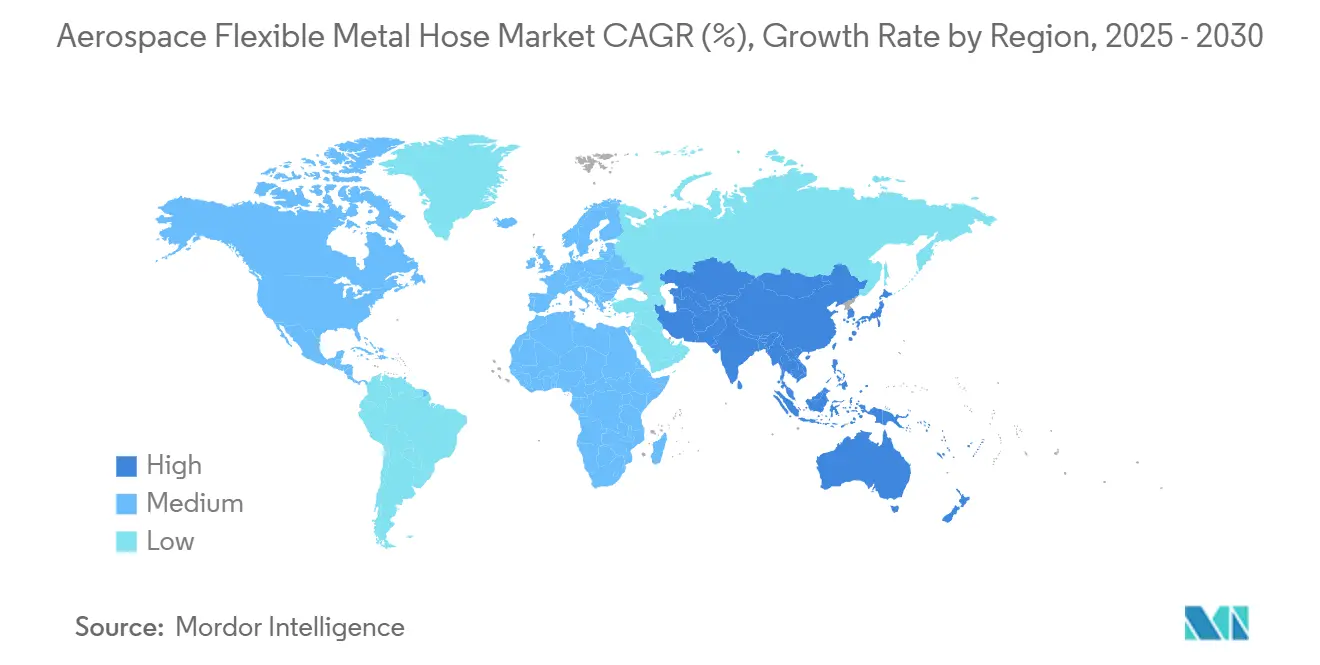

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

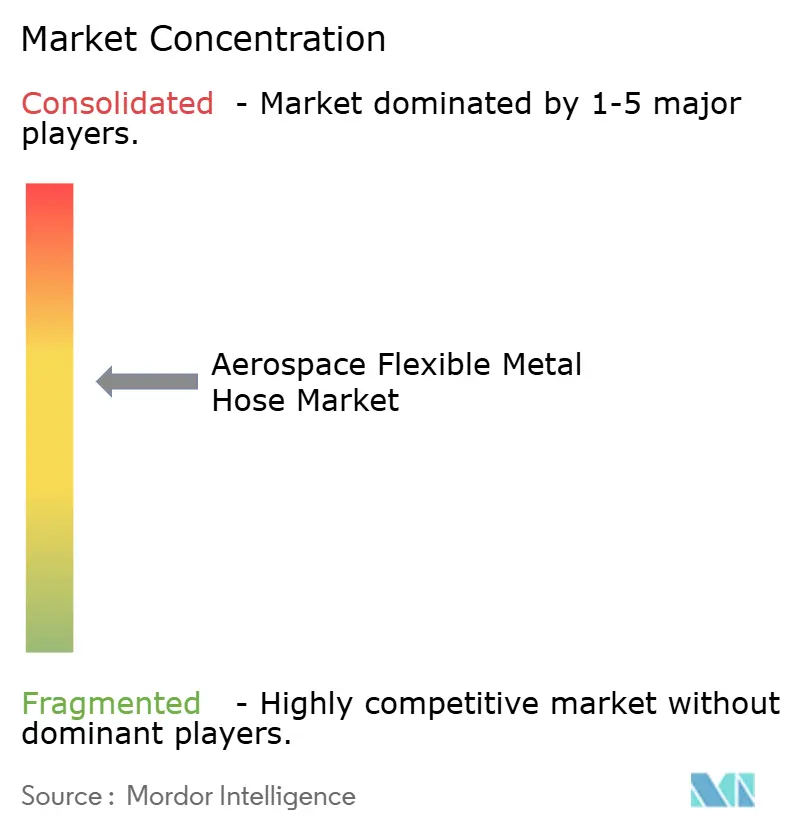

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Flexible Metal Hose Market Analysis by Mordor Intelligence

The aerospace flexible metal hose market size stands at USD 959.2 million in 2025 and is forecasted to reach USD 1,111.98 million by 2030, advancing at a 4.93% CAGR. This expansion reflects a decisive shift toward next-generation propulsion architectures that favor metallic conduits for weight-critical thermal management, high-pressure fuel delivery, and cryogenic hydrogen transfer. Stricter efficiency mandates reinforce demand, the rise of hydrogen aircraft programs, and eVTOL fleet deployment that collectively widen the addressable base for stainless steel, titanium, and Inconel hose assemblies. Certified suppliers benefit from entrenched FAA and EASA standards that favor proven metallic solutions, while additive manufacturing lowers lead times for custom bellows that fit tight airframe envelopes. Material cost volatility and polymer competition in low-pressure circuits moderate growth but have not displaced metallic hoses in flight-critical zones where conductivity, permeation, and fatigue resistance remain decisive.

Key Report Takeaways

- By product type, corrugated hoses held 48.55% of the aerospace flexible metal hose market share in the aerospace market in 2024; bellows-type expansion joints are poised to grow at a 5.36% CAGR through 2030.

- By material, stainless steel commanded 53.23% of the aerospace flexible metal hose market size in 2024, while titanium is projected to expand at a 6.32% CAGR to 2030.

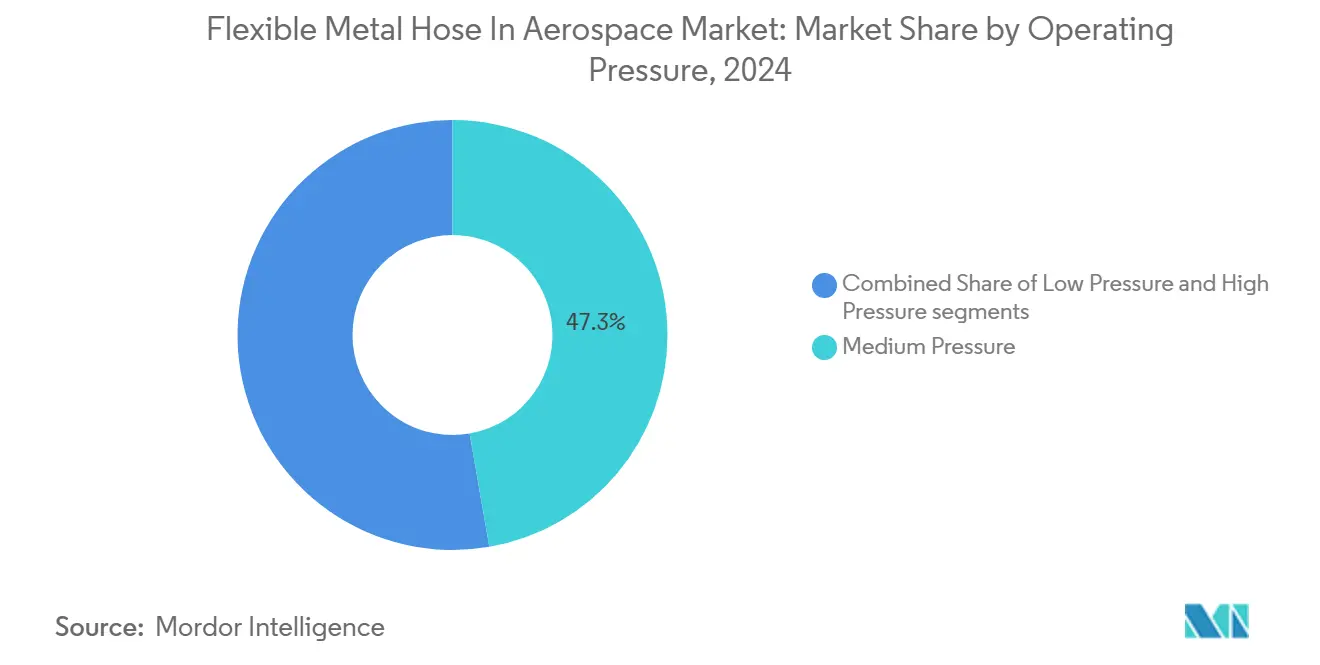

- By operating pressure, medium pressure held 47.26% of the aerospace flexible metal hose market in 2024, while high pressure is estimated to grow at a 4.98% CAGR in the forecast period.

- By application, fuel lines accounted for 59.36% of the aerospace flexible metal hose market size in 2024, yet cryogenic hydrogen lines are advancing at a 7.31% CAGR through 2030.

- Regionally, North America led the aerospace market with 41.77% flexible metal hose in 2024, whereas Asia-Pacific is forecasted to record the fastest 4.27% CAGR up to 2030.

Global Aerospace Flexible Metal Hose Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| In-flight fuel-efficiency mandates driving demand for lightweight corrugated metal hoses | +0.80% | Global; early adoption in EU and North America | Medium term (2-4 years) |

| Adoption of bleed-less electric architectures requiring flexible metallic conduits for thermal management | +0.60% | North America and EU core; APAC spill-over | Long term (≥ 4 years) |

| Increasing R&D in hydrogen-powered aircraft necessitating cryogenic-capable stainless-steel hoses | +1.20% | Global; EU and North America concentration | Long term (≥ 4 years) |

| Expansion of eVTOL fleets with compact hydraulic lines | +0.90% | North America and EU; early APAC deployment | Medium term (2-4 years) |

| Emergence of additive-manufactured metal bellows enabling custom hose geometries | +0.40% | North America and EU hubs | Short term (≤ 2 years) |

| Supply-chain localization initiatives by OEMs creating regional hose-qualification opportunities | +0.50% | APAC core; secondary NA and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

In-Flight Fuel-Efficiency Mandates Drive Lightweight Corrugated Metal Hose Adoption

Airlines face CORSIA carbon-offset fees that sharpen the focus on weight savings across every subsystem. Corrugated metal hoses cut 15-20% mass versus braided designs while exceeding 25-year service life standards under CS-ETSO, giving them a protected role in long-haul fleets.[1]Federal Aviation Administration, “Hydrogen Aircraft Certification Roadmap,” faa.gov FAA’s 2024 hydrogen roadmap removed PTFE from cryogenic fuel circuits, sealing demand for stainless steel and Inconel conduits. EASA added thermal-cycle endurance clauses to CS-ETSO that polymer hoses cannot meet, cementing metallic options across European programs. Retrofits on A320neo auxiliary fuel tanks showed a 0.1% fuel-burn improvement after switching to lightweight corrugated lines, validating operational payback. Airlines highlight the hoses’ maintainability because spiral corrugations resist outer braid fray, lowering unscheduled removals.

Bleed-Less Electric Architectures Require Specialized Thermal-Management Conduits

More-electric aircraft eliminate pneumatic bleed air and shift heat loads to liquid coolant loops that can peak above 400 °C on powertrain inverters. B787 and A350 early adopters needed metallic lines with high emissivity coatings to dissipate heat within the limited bay space.[2]Airbus SE, “ZEROe Hydrogen Aircraft Program,” airbus.com Follow-on programs such as A321XLR push higher watt densities, tightening the operating margin for polymer composites that soften beyond 260 °C. The UK Aerospace Technology Institute assigned USD 870 million equivalent to electric-aircraft R&D in 2024, with 15% apportioned to thermal subsystems—funding that funnels directly to hose suppliers capable of rapid qualification. Flight-cycle testing at 50 Hz vibration proved corrugated stainless lines outlasted PTFE by 3x, reinforcing their fit for new architectures.

Hydrogen Aircraft Development Accelerates Cryogenic-Capable Hose Demand

ZEROe and comparable demonstrators require hoses that stay ductile at −253 °C. SAE AIR8466 introduced minimum bend-radius and permeability ceilings achievable only by multi-layer stainless steel or nickel superalloys.[3]SAE International, “AIR8466 Hydrogen Fueling Station Standard,” sae.org NASA’s upcoming USD 50 million cryogenic facility will qualify full-scale fuel loops, setting de facto benchmarks for hose durability. Early rig tests revealed that bellows-style lines retained flexibility after 10,000 freeze-thaw cycles without micro-cracking, whereas polymer liners embrittled after 800 cycles. IP filings surged to 271 in 2024, with nearly one-quarter covering cryogenic connectors, confirming sustained R&D interest. The elevated technical bar deters new entrants lacking metallurgical depth, consolidating demand among incumbent hose makers.

eVTOL Fleet Expansion Creates Compact Hydraulic-Line Opportunities

Urban air mobility (UAM) craft compress hydraulic and flight-control hardware inside constrained nacelles. Joby Aviation’s prototype places flight-surface actuators mere centimeters from battery packs, rewarding hoses that bend to sub-50 mm radii without kinking. Fatigue tests targeting 10,000+ vertical launches proved stainless corrugated lines preserved burst strength better than micro-bore PTFE. FAA Part 135 pathways introduced eVTOL-specific endurance factors, nudging OEMs toward metallic solutions despite weight trade-offs. The segment’s growth from USD 2.04 billion in 2024 to USD 40.63 billion by 2034 multiplies hose demand across fleet spares and overhaul cycles. Honeywell’s partnership with Vertical Aerospace cites compact metallic conduits as a critical success factor for type-certificate approval.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qualification complexity and extended certification cycles | −0.7% | Global; pronounced in North America and EU | Long term (≥ 4 years) |

| Volatile nickel and specialty-alloy pricing | −0.5% | Global; heavy APAC impact | Short term (≤ 2 years) |

| High-performance polymer competition in low-pressure loops | −0.3% | North America and EU | Medium term (2-4 years) |

| Tier-1 consolidation limiting entry for niche players | −0.4% | Global; NA and EU concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Qualification Complexity Creates Barriers for Innovation Adoption

FAA 14 CFR 27.993 demands 25-year service-life tests that cost USD 2–5 million per hose design and last up to 5 years. When suppliers seek EASA CS-ETSO validation, duplicate environmental cycling enlarges budgets and timelines. CASA inspection advisory AC-145-02 further requires on-wing inspection intervals that favor incumbent metallic constructions. Smaller firms struggle to finance dual-agency compliance, encouraging mergers or supplier exits. The resulting certification inertia slows adoption of new materials and processes even when technical merit exists, trimming potential CAGR by an estimated 0.7 percentage point.

Material-Cost Volatility Pressures Specialty-Alloy Supply Chains

Nickel swung from USD 20,000 per ton in May 2024 to USD 15,000 in early 2025 before rebounding mid-year, injecting margin risk for hose builders who lock pricing early in airframe contracts. Indonesia supplies 63.4% of global nickel, so policy shifts reverberate into aerospace alloy surcharges. MP35N superalloy at USD 80–100/kg means raw material underpins nearly half the finished hose value, limiting the ability to hedge through forward contracts. Section 232 import duties add further cost layers for US plants. Molybdenum’s short-term dip offers temporary respite, but forecasts indicate renewed upward pressure by 2026. Vendors respond with dual-sourcing strategies and inventory buffers, yet cost pass-through to OEMs remains incomplete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bellows Innovation Drives Custom Applications

Corrugated hoses retained 48.55% of the aerospace flexible metal hose market share in 2024 because commercial programs rely on standardized fuel and hydraulic routings. However, the bellows-type joints segment is forecasted to grow fastest at a 5.36% CAGR as additive manufacturing unlocks bespoke shapes for eVTOL nacelles and hydrogen tanks. Corrugated varieties deliver mature qualification pedigrees, simplified repair procedures, and cost advantages in high-volume builds, so their absolute revenue still expands through 2030. Stripwound interlocked lines remain niche, favored only in extreme vibration zones such as helicopter rotor-head lubrication systems, where axial flexibility outweighs added mass.

Bellows' growth reflects the aerospace push for tighter integration. Printed bellows eliminate welded collars, boosting strain life in cryogenic hydrogen loops that face rapid temperature cycling. Airbus prototypes showed 30% lower installation labor and a 12 kg weight reduction across a twin-aisle fuel bay, a tangible gain for airlines. Tier-1s with laser-powder bed fusion capacity—such as Eaton and Senior—shorten OEM design loops, while smaller vendors without additive know-how see their share slip. These dynamics widen the technology gap within the flexible metal hose in the aerospace market.

By Material: Titanium Growth Reflects Weight-Critical Applications

Stainless steel controlled 53.23% of the aerospace flexible metal hose market in 2024, thanks to robust supply chains and favorable cost-to-performance ratios. Titanium usage accelerates at a 6.32% CAGR through 2030 as eVTOL designers trade higher material cost for greater range. Superalloys like Inconel safeguard hoses near turbine hot sections, while aluminum-bronze alloys address niche corrosion risks on carrier-borne aircraft. Stainless remains the default in commercial jets where qualification history and repair familiarity override the 50% weight penalty.

Hydrogen programs push suppliers to reassess alloy menus. NASA’s cryogenic specs deselect several standard steels, steering orders to titanium grade 5 and customized Ni-Cr-Fe blends that stay ductile at −253 °C. Titanium also resists hydrogen embrittlement, a growing concern for long-dwell storage. As a result, titanium’s share edges upward despite fluctuating spot prices. Vendors investing in isothermal-forging and near-net-shape production lock in a competitive advantage, while commodity stainless producers risk commoditization.

By Operating Pressure: High-Pressure Systems Enable Advanced Propulsion

Medium-pressure lines (1,500 to 3,000 psi) commanded 47.26% of 2024 revenue because they cover traditional hydraulic and fuel service. High-pressure lines above 3,000 psi log a 4.98% CAGR as more-electric architectures and compact thermal loops aim for higher fluid density. Low-pressure loops face substitution with high-performance polymers in cabin air and environmental control functions, trimming metallic content in those zones.

Higher pressures let engineers shrink the actuator bore and reduce the total hose length, which is key in eVTOL platforms that tolerate only minimal plumbing. SAE’s revision of AS620 to 6,000 psi burst margins excludes most polymer liners, entrenching metallic dominance in these circuits. Suppliers proficient in autofrettage processing achieve superior fatigue life, differentiating themselves as OEMs raise proof-test thresholds.

By Application: Cryogenic Hydrogen Lines Lead Growth Trajectory

Fuel lines remained the prime application, accounting for 59.36% of the aerospace flexible metal hose market in 2024, anchored by large commercial fleets. Cryogenic hydrogen lines, however, delivered a 7.31% CAGR to 2030, tracking the ramp of ZEROe, NEW JET, and assorted regional concepts. Hydraulic and pneumatic circuits sustain moderate growth tied to narrow-body production, while bleed-air lines recede as bleed-less systems proliferate.

Hydrogen service introduces unique validation, such as dual-wall construction and continuous leak detection ports that conventional Jet-A lines lack. Early test rigs confirmed metallic bellows outperform polymer-lined options in fatigue at cryogenic gradients. Regulatory endorsements from the UK CAA hydrogen gap analysis further institutionalize metallic hoses, providing long-term visibility for suppliers.

Geography Analysis

North America held 41.77% of the aerospace flexible metal hose market share in 2024 on the back of Boeing and Lockheed Martin production upticks, a deep MRO ecosystem, and the FAA’s conservative material stance. Boeing delivered 528 jets in 2024, each incorporating roughly 1.8 km of metallic hose across fuel, hydraulic, and thermal systems.[4]The Boeing Company, “Commercial Aircraft Delivery Report,” boeing.com Canada’s Bombardier and Pratt & Whitney Canada sustain this demand in business-jet and engine segments, while Mexico supplies cost-efficient assembly for tier-1 vendors. Stringent life-limit tracking and AD note compliance preserve metallic incumbency against polymer challenges in the region.

Asia-Pacific posts the fastest 4.27% CAGR to 2030 as COMAC ramps the C919 to 75 units annually and the ARJ21 backlog extends through mid-decade. China’s localization push incentivizes hose makers to set up regional test labs aligning with CAAC standards, shortening certification cycles for domestic programs. Japan’s Mitsubishi Heavy and Kawasaki Heavy provide titanium and superalloy tubing expertise, supporting regional strength in weight-critical eVTOL structures. South Korea leverages advanced forming to embed itself in Chinese procurement channels, while India’s offset-linked orders open fresh supply-chain nodes.

Europe remains technologically mature, anchored by Airbus hubs in France, Germany, and Spain. The bloc’s Clean Aviation and Hydrogen Europe initiatives funnel grants to cryogenic hardware, channeling work to hose allies skilled in sub-zero metallurgy. EASA’s certification authority extends global reach, forcing non-EU suppliers to match its stringent Part-21 production approvals for worldwide sales. Brexit-related customs friction nudges some UK hose content back into continental factories, marginally redistributing revenue but not denting overall EU influence.

Competitive Landscape

The aerospace flexible metal hose market exhibits moderate concentration. Parker-Hannifin Corporation, Eaton Corporation plc, Safran SA, AMETEK, Inc., and Smiths Group plc exceed 45% combined revenue, exploiting multi-year FAA Parts Manufacturer Approval catalogs that simplify airline procurement. Aftermarket leverage is visible in Parker’s 20% jump in 2024 service sales, which offsets materials cost volatility. Tier-1s pursue vertical integration; Safran’s 2025 acquisition of a Collins actuation unit adds captive hose demand and internalizes qualification data previously sourced from partners.

Technology race elements focus on additive bellows and cryogenic assemblies. United Flexible patented a helical convolution style optimized for −253 °C bending, while Senior Flexonics filed for smart-sensor-embedded hoses that report cycle counts to maintenance crews. Mid-size specialists without broad PMA libraries pivot toward APAC localization to win on low tooling costs. Consolidation continues as drawn-out certification burdens overwhelm niche players, consistent with observed M&A activity among hose and fitting makers.

Aerospace Flexible Metal Hose Industry Leaders

Eaton Corporation plc

Safran SA

AMETEK,Inc.

Smiths Group plc

Parker-Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The UK CAA released CAP3124 hydrogen aircraft gap analysis, spotlighting metallic cryogenic hoses as key enablers of commercial hydrogen flight.

- December 2024: SAE International issued AIR8466, defining the first-ever industry criteria for hydrogen fueling-station hoses.

Global Aerospace Flexible Metal Hose Market Report Scope

| Corrugated Hoses |

| Stripwound Interlocked Hoses |

| Bellows-Type Expansion Joints |

| Stainless Steel |

| Inconel and High-Nickel Alloys |

| Titanium |

| Others (Aluminum, Bronze) |

| Low Pressure (Less than 1,500 psi) |

| Medium Pressure (1,500 to 3,000 psi) |

| High Pressure (Greater than 3,000 psi) |

| Fuel Lines |

| Hydraulic and Pneumatic Lines |

| Environmental Control System (ECS) |

| APU and Engine Bleed Air |

| Cryogenic Hydrogen Lines |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Corrugated Hoses | ||

| Stripwound Interlocked Hoses | |||

| Bellows-Type Expansion Joints | |||

| By Material | Stainless Steel | ||

| Inconel and High-Nickel Alloys | |||

| Titanium | |||

| Others (Aluminum, Bronze) | |||

| By Operating Pressure | Low Pressure (Less than 1,500 psi) | ||

| Medium Pressure (1,500 to 3,000 psi) | |||

| High Pressure (Greater than 3,000 psi) | |||

| By Application | Fuel Lines | ||

| Hydraulic and Pneumatic Lines | |||

| Environmental Control System (ECS) | |||

| APU and Engine Bleed Air | |||

| Cryogenic Hydrogen Lines | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the flexible metal hose in aerospace market?

The market stands at USD 959.2 million in 2025 and is forecasted to reach USD 1.11 billion by 2030, expanding at a 4.93% CAGR.

Which region leads demand for aerospace metal hoses?

North America holds 41.77% share due to Boeing, Lockheed Martin, and rigorous FAA standards that favor metallic assemblies.

Which product segment is growing fastest?

Bellows-type expansion joints post a 5.36% CAGR through 2030, driven by additive manufacturing that tailors shapes for space-constrained designs.

How will hydrogen aircraft programs affect hose demand?

Cryogenic hydrogen lines represent the highest 7.31% CAGR because ZEROe and similar projects need stainless or titanium hoses capable of −253 °C duty.

What material shows the strongest growth outlook?

Titanium hoses are projected to expand at 6.32% CAGR as eVTOL and hydrogen platforms prioritize weight savings and hydrogen embrittlement resistance.

What are the main barriers for new hose suppliers?

Lengthy 3-5 year certification cycles and high alloy price volatility raise entry costs, steering the market toward established, qualified players.

Page last updated on: