AC DC Power Adapters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

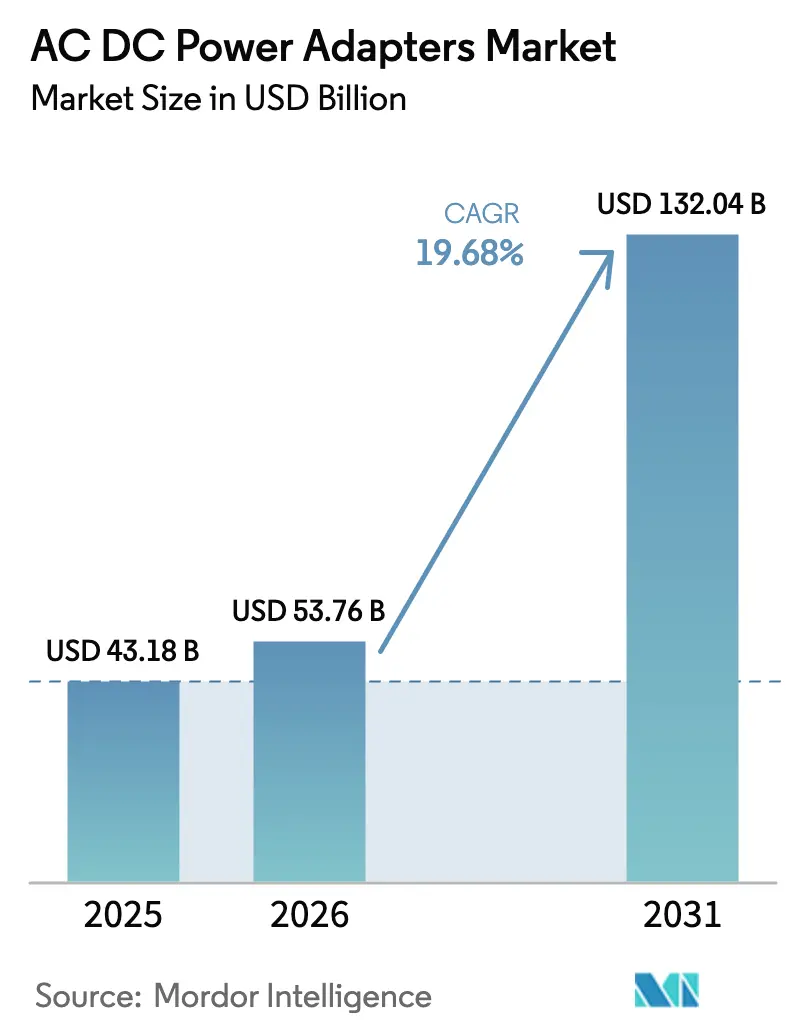

| Market Size (2026) | USD 53.76 Billion |

| Market Size (2031) | USD 132.04 Billion |

| Growth Rate (2026 - 2031) | 19.68% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AC DC Power Adapters Market Analysis by Mordor Intelligence

The AC DC power adapters market size is expected to grow from USD 43.18 billion in 2025 to USD 53.76 billion in 2026 and is forecast to reach USD 132.04 billion by 2031 at a 19.69% CAGR over 2026-2031. Mandatory USB-C Power Delivery compliance, the electrification of automotive infotainment and charging-infrastructure ecosystems, and gallium-nitride-enabled efficiency gains are compressing product-refresh cycles and spurring unit demand. Regulatory deadlines in the European Union and India have synchronized global design roadmaps, while hyperscaler data-center expansion is pulling high-wattage desktop bricks into mainstream use. Suppliers that master rapid GaN platform iteration, modular designs that satisfy circular-economy rules, and multi-port architectures that simplify cable management are capturing outsized share of the AC DC power adapters market. Competitive intensity is rising as vertically integrated Chinese specialists cut prices and accelerate time-to-market, even as Tier-1 incumbents redirect R&D toward 98%-efficient 800-volt racks for artificial-intelligence clusters.

Key Report Takeaways

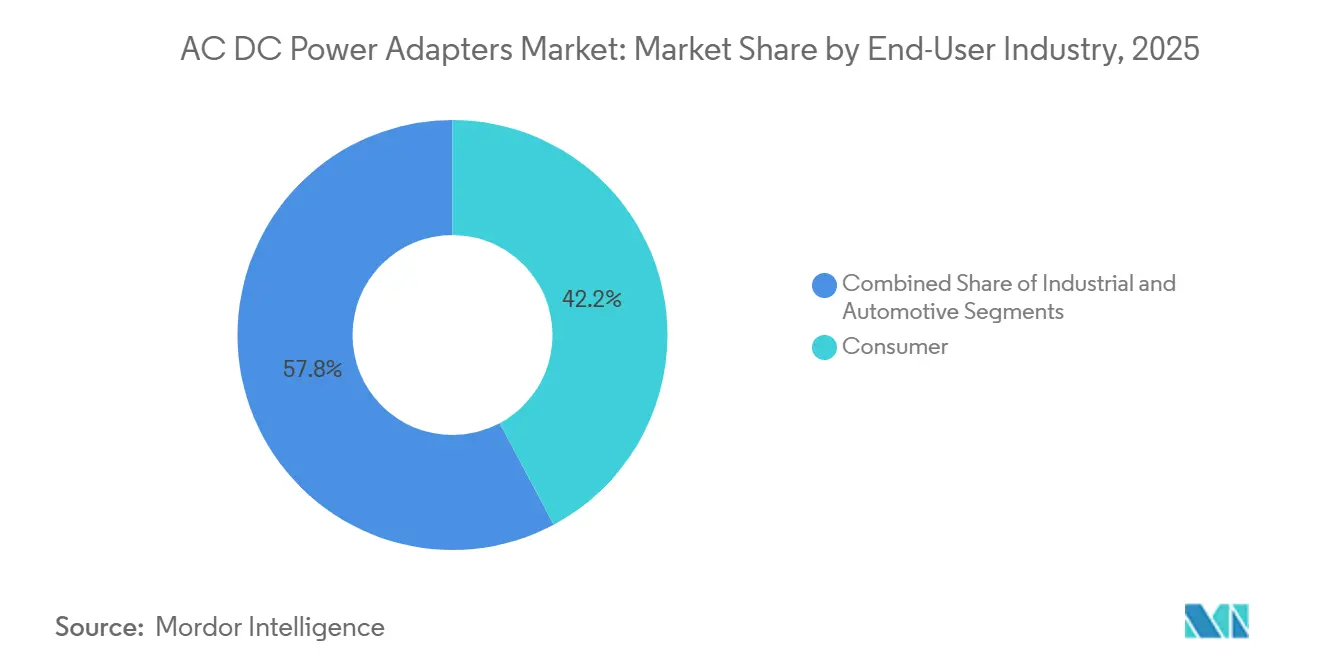

- By end-user industry, consumer electronics led with 42.19% revenue share in 2025, while automotive is projected to expand at a 20.26% CAGR through 2031.

- By output power rating, the 16–45-watt tier commanded 35.54% of the AC DC power adapters market share in 2025 and the 101–240-watt segment is advancing at a 20.58% CAGR to 2031.

- By port type, single-port units held 46.28% of 2025 revenue, whereas ultra-multi-port GaN docks are forecast to grow at a 20.43% CAGR to 2031.

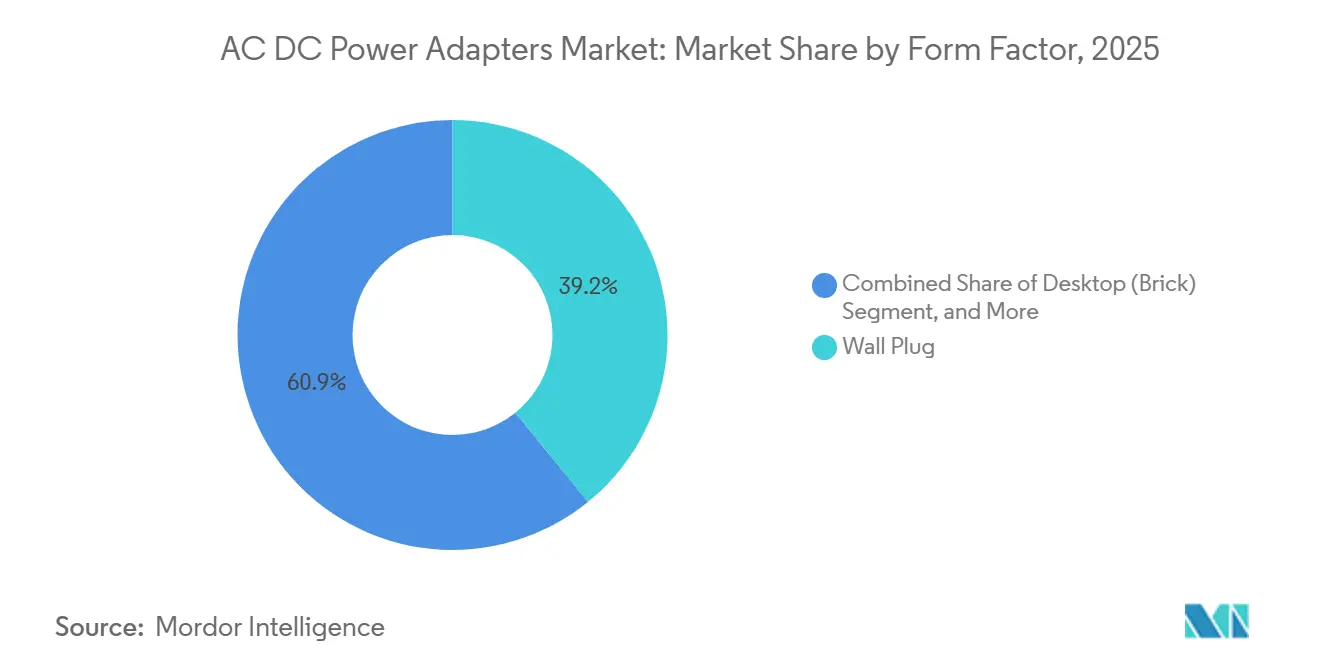

- By form factor, wall-plug adapters accounted for 39.15% of 2025 sales and desktop bricks are rising at a 20.59% CAGR over the forecast period.

- By sales channel, OEM bundling generated 55.19% of 2025 revenue, yet retail aftermarket sales are climbing at a 20.22% CAGR through 2031.

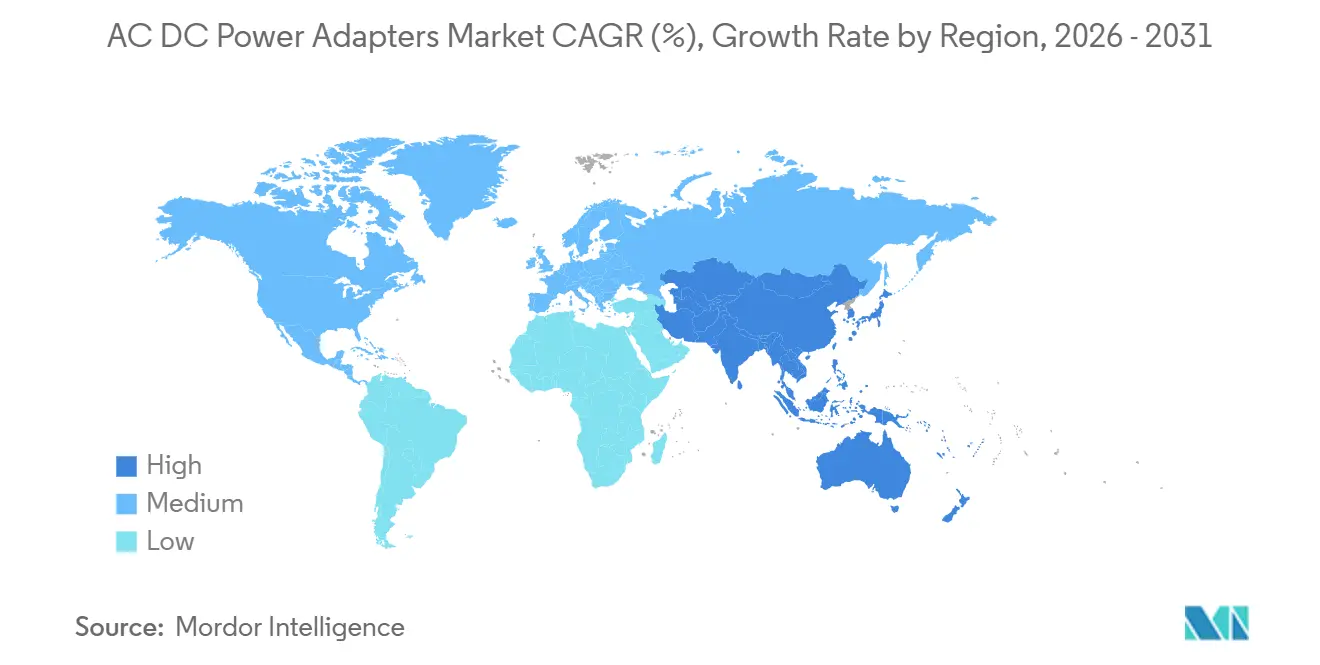

- By geography, Asia-Pacific captured 46.49% of 2025 value and the Middle East is the fastest-growing region at a 20.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AC DC Power Adapters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of USB-C Power Delivery Standards | +4.20% | Global, with early enforcement in EU and India | Short term (≤ 2 years) |

| Proliferation of Consumer Electronics | +3.80% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rapid Electrification of Automotive Accessories | +3.50% | North America and Europe (EV adoption), China (IVI systems) | Medium term (2-4 years) |

| Integration of GaN and SiC Semiconductors | +3.10% | Global, with RandD concentration in Japan, Taiwan, United States | Long term (≥ 4 years) |

| Rising Energy-Efficiency Regulations | +2.40% | EU (Ecodesign 2025/2052), United States (DOE Level VI), China (CCC updates) | Long term (≥ 4 years) |

| OEM Focus on Adapter Modularity for Circular Economy | +1.90% | EU (Right to Repair Directive), North America (state-level legislation) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of USB-C Power Delivery Standards

The European Union’s Common Charger Directive and India’s mirrored mandate have removed 14 proprietary protocols, triggered a synchronized replacement wave and pushed PD 3.1 certifications up 47% year-on-year.[1]USB Implementers Forum, “USB Power Delivery,” usb.org Apple’s migration to USB-C and Samsung’s 60 watt launch signal platform convergence across iOS and Android. Third-party makers such as Anker and Belkin released compliant multi-port chargers inside eight weeks of the EU deadline, showing that agile supply chains can thrive in a rules-driven environment.

Proliferation of Consumer Electronics

Device shipments topped 2.1 billion units in 2025, and hybrid work normalized multi-display, multi-device desks that rely on GaN bricks integrating power, data, and video. Gaming laptops now require 180–240-watt budgets, accelerating high-wattage adoption. IoT endpoints reached 16.7 billion and each draws a dedicated 5–15-watt adapter, fragmenting SKU portfolios and inflating retailer inventory costs.[2]International Energy Agency, “World Energy Outlook 2025,” iea.org

Rapid Electrification of Automotive Accessories

Global Level 2 charging ports climbed to 3.2 million by end-2025, with every station containing 7.7-19.2-kilowatt AC DC modules certified to SAE J1772 and IEC 61851.[3]SAE International, “SAE J1772 Conductive Charge Coupler,” sae.org In-cabin USB-C PD 3.1 sockets are now standard in models such as Ford’s F-150 Lightning and Mercedes-Benz EQS, each supplying up to 120 watts for rear-seat devices.

Integration of GaN and SiC Semiconductors

GaN transistors switch above 500 kHz and cut adapter volume by 40% while attaining 95% efficiency. Anker’s PowerIQ 4.0 reallocates 240 watts across eight outlets in real time, proving GaN’s system-level benefits. SiC substrates are powering 800-volt racks in hyperscale data centers, achieving 98% conversion and 25% cooling savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Safety and EMI/EMC Certification Costs | -2.80% | Global, with highest burden in EU (CE), North America (UL/FCC), China (CCC) | Short term (≤ 2 years) |

| Volatility in Raw-Material Prices | -2.30% | Global, with acute exposure in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Growing Shift Toward Wireless Charging Pads | -1.60% | North America and Europe (premium smartphone segment) | Medium term (2-4 years) |

| OEM Consolidation of Adapters into Device Price | -1.40% | Global, led by Apple, Samsung, Xiaomi, Oppo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Safety and EMI/EMC Certification Costs

Compliance with UL 62368-1, IEC 62368-1, and FCC Part 15 can add USD 5,000-50,000 per SKU and delay launches by up to 16 weeks.[4]SGS, “Testing and Certification Services,” sgs.com Q1 2026 rejection rates rose to 32% as high-frequency GaN designs struggled to satisfy CISPR 32 margins. The EU’s Ecodesign 2025/2052 rule further invalidated legacy certificates by tightening no-load ceilings.

Volatility in Raw-Material Prices

Copper fluctuated inside an USD 8,500-10,200-per-ton range in 2025, raising BOM costs by nearly one-fifth. Chinese export controls lifted gallium prices 35%, squeezing GaN makers without long-term hedges. Silver and rare-earth tariffs added further uncertainty, eroding margins for second-tier vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Automotive Growth Overtakes Legacy Consumer Demand

Automotive applications of AC DC power adapters recorded a 20.26% CAGR, driven by the shift to USB-C PD 3.1 240-watt interfaces in EVs and public chargers. The AC DC power adapters market size tied to consumer electronics remained the largest slice, yet the automotive wave is narrowing the gap as OEMs standardize on high-power USB-C sockets. Scalability benefits from Tesla’s open North American Charging Standard and U.S. federal funding ensure sustained volume. Industrial automation and IoT gateways demand rugged DIN-rail units that command 40-60% premiums, supporting margin diversity.

Momentum in automotive also reshapes supply chains. Suppliers with AEC-qualified lines win contracts for adapter modules that survive −40 °C to +85 °C swings and 10 g-rms vibration. Firmware upgrades that modulate voltage in 20 mV steps are unlocking over-the-air energy management, an advantage unattainable in older barrel-connector designs.

By Output Power Rating: 101-240 W Tier Accelerates

USB-C PD 3.1 erased proprietary plugs on performance laptops, so the 101–240-watt range is growing at 20.58% CAGR. The ≤15-watt slice faces substitution from Qi2 pads, while the 16-45 watt bloc still held 35.54% of 2025 revenue thanks to the smartphone installed base. GaN devices underpin thin, light 180-240 watt bricks that fit airline carry-on regulations, widening addressable enterprise demand.

Vendors now ship firmware-updateable adapters, extending lifetime and aligning with circular-economy rules. High-wattage growth also benefits component makers of high-current Type-C cables and e-marker ICs, embedding new value pools inside the AC DC power adapters market.

By Port Type: Multi-Port Hubs Capture Desk Real Estate

Ultra-multi-port GaN docks that house five or more outlets are tracking a 20.43% CAGR as hybrid workers need one brick for every device. Single-port units still own 46.28% of 2025 turnover because bundling keeps them attached to new devices, but aftermarket buyers increasingly favour two-to-four-port compromises that balance cost and utility.

Programmable power-supply logic in PD 3.1 now reallocates current every 100 µs, maintaining thermal headroom while charging heterogeneous loads. Vendors integrate HDMI and Ethernet to collapse adapter and dock categories, unlocking cross-sell into the broader peripherals wallet.

By Form Factor: Desktop Bricks Answer Cooling and Repair Mandates

Wall-plug units delivered 39.15% of 2025 sales, but desktop bricks are outpacing at 20.59% CAGR because 800-volt racks for AI workloads demand liquid-cooled, field-serviceable modules. Detachable plugs with country-specific blades further ease logistics for global IT fleets.

Modularity aligns with EU Right to Repair rules that require seven-year spare-parts availability, propelling interest in replaceable cables and fan cartridges. Embedded board-mount supplies in medical and industrial machines remain a profitable niche, protected by IEC 60601-1 and similar standards.

By Sales Channel: Aftermarket Retail Redefines Price Anchors

OEM bundling still represents 55.19% of revenue, yet the aftermarket is expanding 20.22% CAGR as brands like Apple drop in-box chargers. E-commerce platforms shorten go-to-market for challengers such as Ugreen and Baseus, compressing price corridors especially in the 16–45-watt band.

Anker’s vertical integration enables two-week concept-to-shelf cycles, reinforcing its 25% share of USB-C adapters. Warranty handling, once a bundling advantage, is neutralized by same-day replacement policies from leading online retailers, smoothing adoption of third-party bricks.

Geography Analysis

Asia-Pacific held 46.49% of 2025 revenue as Guangdong-Shenzhen factories produced 67% of global units and local demand surged alongside a data-center build-out from 12.2 GW to 26.1 GW. China’s State Grid will invest CNY 4 trillion (USD 553 billion) through 2030 to modernize transmission, embedding high-efficiency adapters into smart-grid nodes. India’s June 2025 USB-C deadline accelerated notebook refreshes, while Japan and South Korea expanded 6-inch SiC wafer lines to reduce gallium dependence.

The Middle East is the fastest climber at a 20.49% CAGR as AWS, Azure, and G42 race to add hyperscale capacity, driving demand for 98%-efficient 200 kW racks that tolerate desert heat. North America benefits from USD 7.5 billion federal funding for 500,000 Level 2 chargers, supporting 19.2 kW adapters certified to UL and FCC standards.

Europe’s Common Charger Directive produces a synchronized upgrade wave, particularly in Germany, the United Kingdom, and France, which accounted for 60% of regional imports in 2025. South America wrestles with currency risk that inflates landed costs by up to 35%, nudging OEMs toward localized assembly. Africa, led by South Africa and Egypt, absorbs low-wattage 5–15-watt units as mobile penetration grows, yet counterfeit flow undermines compliance efforts.

Competitive Landscape

The AC DC power adapters market remains moderately fragmented: the top five suppliers Delta Electronics, Lite-On, Anker, Belkin, and Salcomp controlled an estimated 35-40% of 2025 revenue. Anker’s 506-supplier network, 434 of which are Chinese, underpins a cost base 20-30% below Taiwanese peers, supporting a 25% USB-C segment share. Delta and Lite-On pivot toward 800-volt data-center bricks, with Delta investing THB 18 billion (USD 500 million) in a Thailand hub and Lite-On allocating NT$11 billion (USD 352 million) across Taiwan, Vietnam, and North America for 2026 capacity.

E-commerce-native disruptors Ugreen, Baseus, and RAVPower offer multi-port GaN chargers at up to 60% markdowns, accelerating commoditization in the 16–45-watt tranche. Technology differentiation centers on thermal innovation such as embedded heat pipes and graphene pads that maintain 95% efficiency at 150 °C junctions.

Certification rigor is climbing: SGS logged a 32% rise in Q1 2026 failure rates for GaN adapters, and test-lab slots run 12-18 weeks ahead, handicapping firms without in-house EMI chambers. Raw-material hedging, in-region service networks, and firmware-upgradable designs are emerging as decisive advantages in the AC DC power adapters market.

AC DC Power Adapters Industry Leaders

Delta Electronics, Inc.

Lite-On Technology Corporation

Anker Innovations Technology Co., Ltd.

Salcomp PLC

Belkin International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UGREEN released the Nexode 500 W GaN desktop charger with six outputs, the first mainstream unit to hit 240 W on a single port.

- May 2025: Navitas Semiconductor partnered with NVIDIA to co-develop an 800 V HVDC architecture for next-generation data-center power conversion.

- April 2025: Delta Electronics introduced a modular megawatt fleet-charging solution and an ultra-slim 50 kW DC wallbox rated at 97% efficiency.

- March 2025: ABB closed the USD 150 million purchase of Siemens’ wiring-accessories arm in China, adding 230-city distribution coverage.

Global AC DC Power Adapters Market Report Scope

The AC DC Power Adapters Market Report is Segmented by End-User Industry (Consumer, Automotive, Industrial), Output Power Rating (≤15W, 16-45W, 46-100W, 101-240W), Port Type (Single-Port, Multi-Port, Ultra-Multi-Port), Form Factor (Wall Plug, Detachable Plug, Desktop, Embedded), Sales Channel (OEM Bundled, Retail Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Consumer | Personal Computers |

| Laptops | |

| Mobile Devices | |

| Other Consumer | |

| Automotive | EV Charging Adapters |

| In-Vehicle Infotainment and Accessories | |

| Industrial |

| ? 15 W |

| 16-45 W |

| 46-100 W |

| 101-240 W |

| Single-Port |

| Multi-Port (2-4 Ports) |

| Ultra-Multi-Port (?5 Ports, GaN Docks) |

| Wall Plug (Fixed-Pin) |

| Detachable Plug (Interchangeable) |

| Desktop (Brick) |

| Embedded, Board-Mount |

| OEM Bundled |

| Retail Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By End-User Industry | Consumer | Personal Computers |

| Laptops | ||

| Mobile Devices | ||

| Other Consumer | ||

| Automotive | EV Charging Adapters | |

| In-Vehicle Infotainment and Accessories | ||

| Industrial | ||

| By Output Power Rating | ? 15 W | |

| 16-45 W | ||

| 46-100 W | ||

| 101-240 W | ||

| By Port Type | Single-Port | |

| Multi-Port (2-4 Ports) | ||

| Ultra-Multi-Port (?5 Ports, GaN Docks) | ||

| By Form Factor | Wall Plug (Fixed-Pin) | |

| Detachable Plug (Interchangeable) | ||

| Desktop (Brick) | ||

| Embedded, Board-Mount | ||

| By Sales Channel | OEM Bundled | |

| Retail Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will demand for high-wattage USB-C PD 3.1 adapters grow?

Units in the 101-240 watt tier are projected to rise at a 20.58% CAGR through 2031 as gaming laptops and mobile workstations drop proprietary barrel plugs.

Which region is forecast to add the most new adapter capacity?

The Middle East leads growth at a 20.49% CAGR to 2031, driven by hyperscale data-center build-outs requiring 98%-efficient 200 kW desktop bricks.

Why are GaN semiconductors critical to next-generation chargers?

GaN switches above 500 kHz, reducing size by 40% and hitting 95% efficiency, which enables multi-port 240 watt designs without thermal throttling.

What is the biggest barrier to market entry for new adapter brands?

Certification costs from UL, IEC, and FCC can reach USD 50,000 per SKU and delay launches up to 16 weeks, favoring incumbents with in-house EMI labs.

How are right-to-repair policies shaping adapter design?

EU rules require seven-year spare-part support, so vendors are moving to modular desktop bricks with replaceable cables and fans to meet compliance.

Will wireless charging replace low-wattage wired adapters?

Qi2 pads now reach 25 watts, but unresolved heat and foreign-object detection above 30 watts mean wired 5-15 watt adapters will coexist through 2031.

Page last updated on: