Metal Packaging Market Size

| Study Period | 2019 - 2029 |

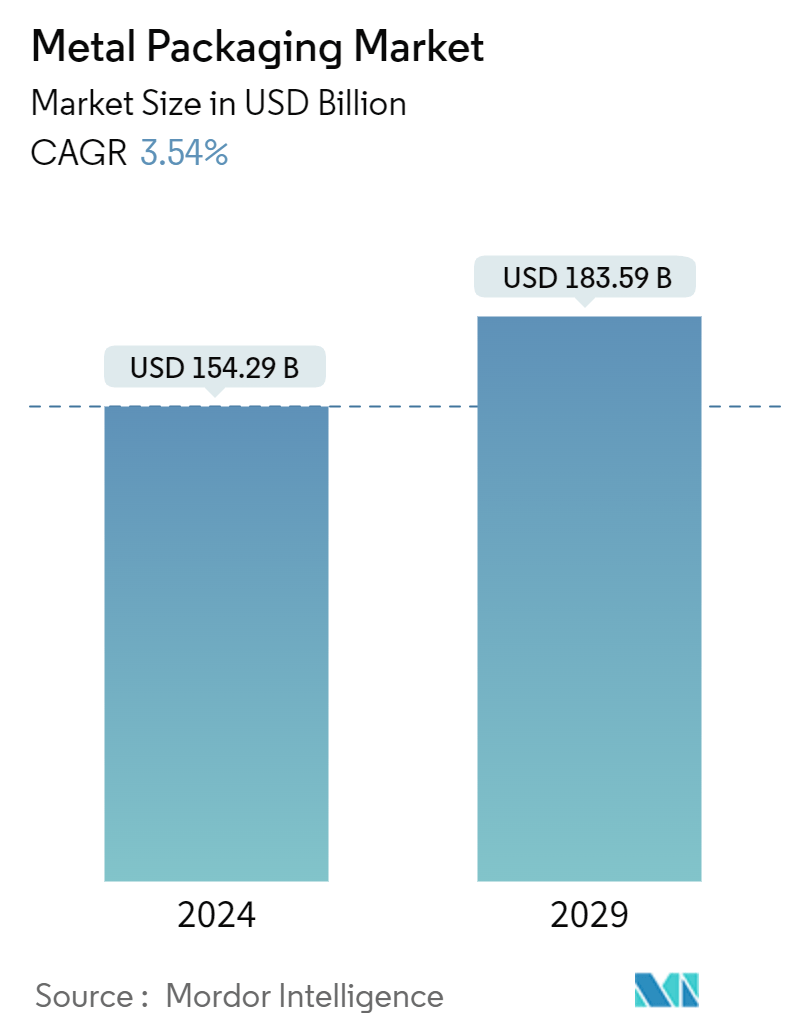

| Market Size (2024) | USD 154.29 Billion |

| Market Size (2029) | USD 183.59 Billion |

| CAGR (2024 - 2029) | 3.54 % |

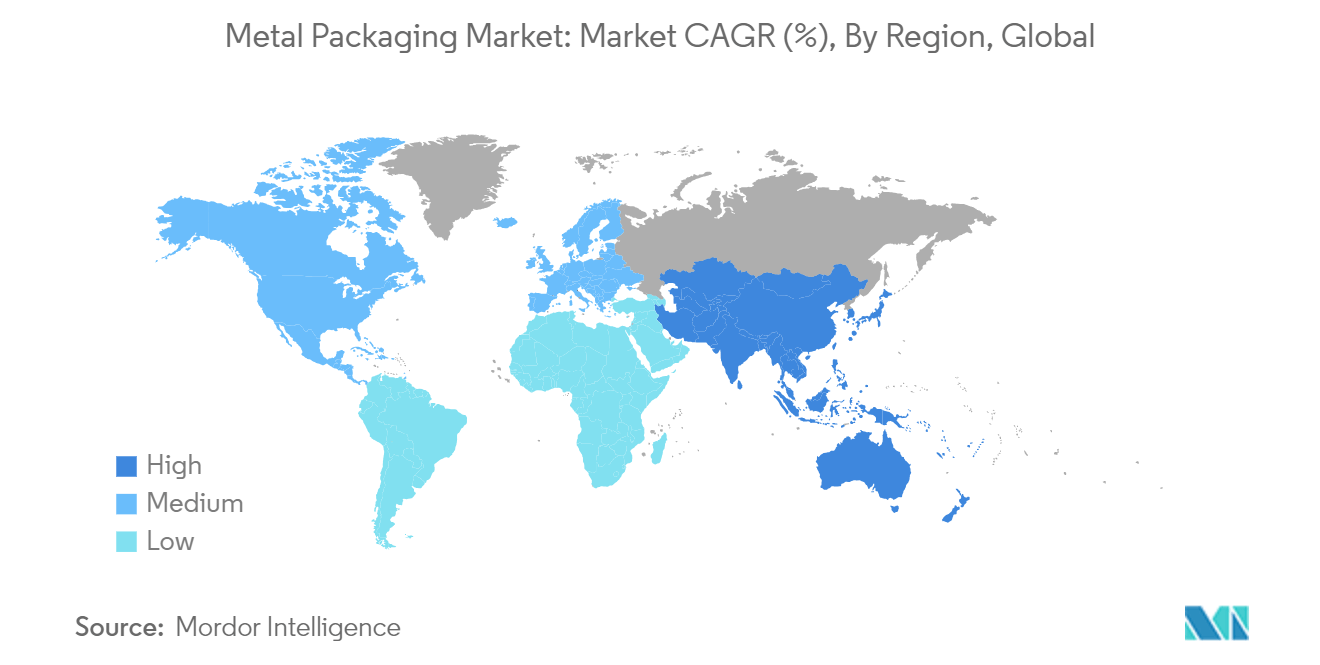

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Metal Packaging Market Analysis

The Metal Packaging Market size is estimated at USD 154.29 billion in 2024, and is expected to reach USD 183.59 billion by 2029, growing at a CAGR of 3.54% during the forecast period (2024-2029).

The metal packaging market demonstrates resilience and growth, driven by diverse factors such as increasing industrial activities, expanding food and beverage consumption, and growing environmental awareness. Due to its durability and protective qualities, industrial metal packaging, including IBCs, bulk containers, drums, and closures, is witnessing steady demand from sectors like chemicals, lubricants, and agricultural products.

- The metal cans segment experiences robust growth, fueled by rising demand for storage cans in packaged food and beverages and increasing demand for aerosol cans in various end-user industries such as cosmetics, automotive and industrial, paints and varnishes, and pharmaceuticals. The shift toward sustainable packaging solutions amplifies the adoption of metal packaging, given its recyclability and environmental benefits. With evolving consumer preferences and regulatory measures favoring eco-friendly packaging, the global metal packaging market is poised for continued expansion, offering opportunities for innovation and collaboration among industry players worldwide.

- Metal is an infinitely recyclable and economically valuable material that can unlock the full potential of packaging, helping to build and accelerate brands while inspiring millennials. Today's consumers demand more customized products and are increasingly concerned with environmental sustainability. Aerosol can packaging is a highly recyclable option that retains its physical properties, ensuring it will remain available for future generations. As more companies adopt aerosol cans for their products, this packaging type's future looks promising.

- Metal containers, particularly those composed of steel and aluminum, provide exceptional durability and protection, making them the preferred container for industries that prioritize product integrity. The continued global expansion and industrialization, especially in developing economies, are expected to stimulate the demand for industrial lubricants and fluids. As a result, there will be a surge in the requirement for dependable and robust packaging solutions, positioning metal packaging for significant expansion.

- The packaging of industrial lubricants, oils, and fluids has undergone significant changes over the years due to fluctuations in material availability and rising costs. Additionally, packaging components and functional design advancements have contributed to this evolution. Notably, sustainability has become an increasingly critical aspect of lubricant packaging as the industry prioritizes environmentally responsible practices.

- Metal packaging is encountering significant competition from alternative packaging solutions. Significant investments in the development of biodegradable plastics impede the market's growth. Plastic is the preferred choice due to its economic advantages over metal. Plastic drums are lighter than steel drums, which makes them easier to move and transport. Additionally, plastic barrels have lower shipping costs than metal drums due to their weight difference.

Metal Packaging Market Trends

Beverage Cans are Expected to Witness Major Growth

- Alcoholic beverages in metal cans have become increasingly popular in recent years due to various benefits and consumer preferences. Canned alcoholic beverages typically come in standard portion sizes, making it easier for consumers to monitor their alcohol intake. This is especially important for drinks with a high alcohol content. Aluminum is exceptionally lightweight, making it an excellent choice for packaging products that need to be easily transported, such as beverages. Lightweight packaging can also reduce transportation costs and carbon emissions.

- Due to rising health consciousness among consumers, the adoption of energy drinks increased, further surging the demand for metal cans. Consumers are becoming increasingly aware of their sugar intake and its impact on their health and well-being. As a result, there is a growing need for sugar-free, natural, and organic drinks. The evolving landscape of the beverage industry has been a critical driver for the growth of the metal cans market in the non-alcoholic beverage sector.

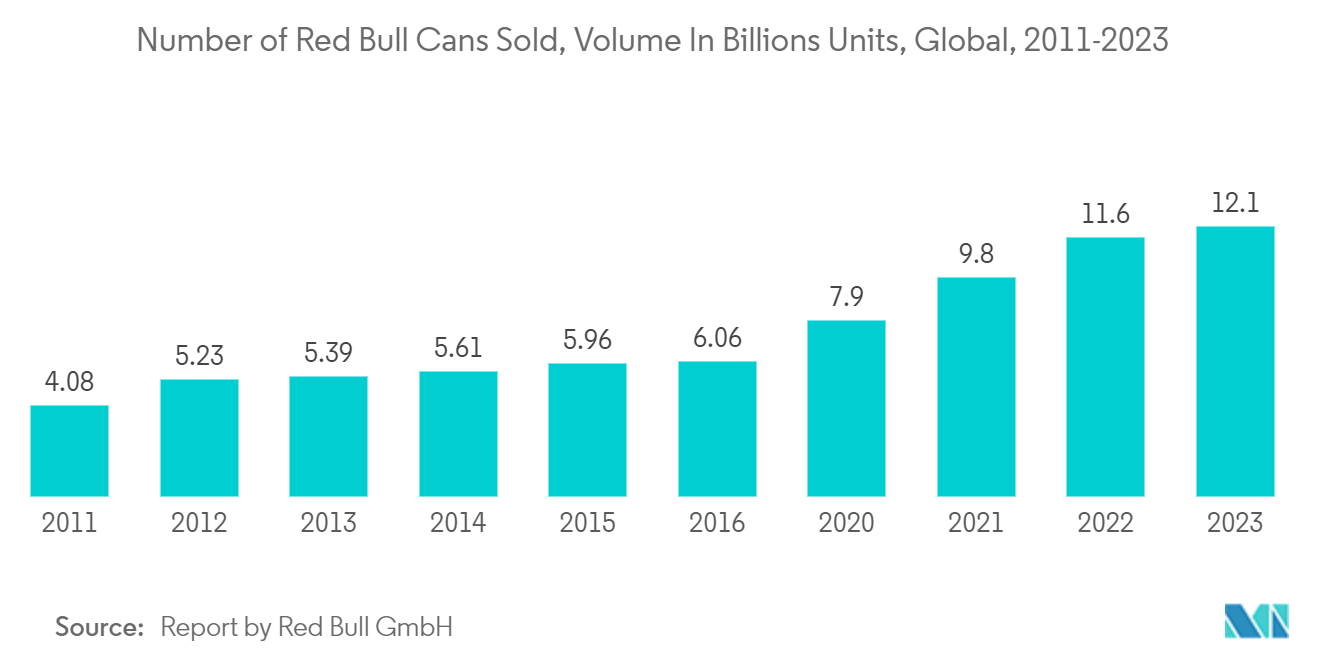

- For example, Red Bull is one of the most popular energy drinks in the United States, controlling about 39.5% of the market. According to the latest information published by Red Bull, the company sold 12.10 billion cans in 2023, more significant than the previous year's count of around 11.60 billion.

- Product launches by manufacturers in the non-alcoholic beverage sector significantly contribute to market growth. For instance, in January 2023, PepsiCo launched Starry, a lemon and lime carbonated soft drink with a crisp and refreshing taste. Carbonated soft drinks are traditionally packed in cans, and PepsiCo's introduction of Starry adds another product to the market that relies on metal cans for packaging.

- In January 2023, Monster Energy Ltd, a well-known energy drink brand, introduced its new zero-sugar beverages in aluminum cans. This increased demand for Monster Energy zero-sugar beverages can directly contribute to a higher demand for aluminum cans as the primary packaging choice for the product.

- Aluminum cans are gaining popularity owing to their exceptional technical properties and the fact that they are recyclable, thermally conductive, and highly lightweight. The beverage brands are also adopting metal cans due to growing environmental concerns about plastic. According to data from The World Counts, the world's beer and soda consumption is at about 180 billion aluminum cans annually. This is 6,700 cans every second, enough to go around the planet every 17 hours.

Asia-Pacific is Expected to Register the Fastest Growth

- With the nation's sizeable manufacturing and consumer goods sectors, China has one of the biggest markets for metal packaging worldwide. The food and beverage, pharmaceutical, cosmetic, and home goods industries are the main drivers of the need for metal packaging.

- China witnessed a surge in the adoption of sustainable packaging solutions due to heightened environmental consciousness and regulatory measures. Manufacturers are looking into possibilities like can coatings that are environmentally friendly and recyclable metals. Developing recyclable materials and environmentally friendly production processes will be fueled by stricter environmental legislation and customer demand for sustainable packaging.

- For instance, in October 2023, Budweiser Brewing Company APAC Limited started a "Can-to-Can" recycling program in China to increase the proportion of recycled aluminum cans and meet its targets of cutting carbon emissions by 35% by 2025. The company committed to taking the lead in advancing China's twin carbon targets and achieving net zero across its entire value chain by 2040. China has set an ambitious goal of peaking carbon dioxide emissions before 2030 and being carbon neutral by 2060 to pave the way for a cleaner and more environmentally friendly future. This is expected to fuel the country's growth of metal packaging solutions.

- India's can and industrial metal packaging market has been steadily expanding due to several factors, including the country's growing paint and coating, personal care, and food and beverage industries. The benefits of metal packaging solutions include strength, recyclability, and barrier qualities. They are extensively utilized in industries like food and beverage, pharmaceuticals, personal care, and chemicals, including paints and coatings.

- Technological and manufacturing process innovations have increased the industry's quality, efficiency, and customizability of metal packaging solutions. With the sixth-largest economy in the world right now, India is quickly industrializing and opening up new prospects for both large and small businesses. This is anticipated to drive the growth of the country's metal packaging market.

Metal Packaging Industry Overview

The metal packaging market is fragmented, consisting of significant players such as Ball Corporation, Crown Holdings Inc., Silgan Holdings Inc., Can-Pack SA (CANPACK Group), and Ardagh Metal Packaging SA (Ardagh Group). The key players in the market are focusing on increasing their market presence by introducing new products, expanding their operations, or entering strategic mergers and acquisitions.

- In February 2024, Ardagh Metal Packaging announced the collaboration with Britvic Soft Drinks and the launch of the innovative high-end design for the brand’s new Tango Mango cans. The high-end, eye-catching design will help the brand elevate the consumer experience through visual appearance.

- In November 2023, Mauser Packaging Solutions entered into an agreement to acquire a manufacturer of tin-steel aerosol cans and steel pails based in Mexico, Taenza, SA de CV. The acquisition strategy will help the company better serve its customers by combining Taenza’s expertise and strong local presence.

- In October 2023, Colep Packaging announced the joint venture with Envases Group to build an aerosol packaging plant in Mexico. This will help the company bring together the expertise to serve North and Central American customers and remain competitive by expanding the production capacity and portfolio.

- In October 2023, Ball Aluminum Cups and Denver Arts & Venues announced the installation of a reverse vending machine, RVM, in Red Rocks Amphitheatre's Top Plaza to improve aluminum recycling at the venue. RVM aims to increase recycling rates at Red Rocks and inform consumers about the benefits of using aluminum.

Metal Packaging Market Leaders

Ardagh Metal Packaging SA (Ardagh Group SA)

Ball Corporation

Crown Holdings, Inc.

Can-Pack S.A.

Silgan Holdings

*Disclaimer: Major Players sorted in no particular order

Metal Packaging Market News

- February 2024 - Hart Print, a subsidiary of Ardagh Metal Packaging engaged in digital printing on aluminum cans, expanded its presence in the United States by opening its third production facility in Maryland. The company aims to increase the annual printing capacity by at least 100 million cans to cater to the demand in the region.

- October 2023 - Crown Holdings Inc. completed its previously announced acquisition of Helvetia Packaging AG, a beverage can and end manufacturing facility in Saarlouis, Germany. As a result of the acquisition, Crown will acquire Helvetia's existing customer base, accompanying contracts, and 200 current employees. The addition of this facility will allow Crown to expand its European beverage can platform in Germany and add approximately one billion tonnes of annual capacity, which will help meet the growing customer demand for recyclable beverage cans.

Metal Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Impact of Geopolitical Scenario on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 High Recyclability Rates of Metal Packaging

5.1.2 Convenience and Lower Price Offered by Canned Food and Beverage

5.2 Market Restraints

5.2.1 Presence of Alternate Packaging Solutions

6. MARKET SEGMENTATION

6.1 By Material Type

6.1.1 Aluminium

6.1.2 Steel

6.2 By Product Type

6.2.1 Cans

6.2.1.1 Food Cans

6.2.1.2 Beverage Cans

6.2.1.3 Aerosol Cans

6.2.2 Bulk Containers

6.2.3 Shipping Barrels and Drums

6.2.4 Caps and Closures

6.3 By End-user Industry

6.3.1 Beverage

6.3.2 Food

6.3.3 Cosmetics and Personal Care

6.3.4 Household

6.3.5 Paints and Varnishes

6.4 By Geography***

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.2.4 Spain

6.4.2.5 Italy

6.4.3 Asia

6.4.3.1 China

6.4.3.2 India

6.4.3.3 Japan

6.4.3.4 South Korea

6.4.3.5 Australia and New Zealand

6.4.4 Latin America

6.4.4.1 Brazil

6.4.4.2 Mexico

6.4.4.3 Argentina

6.4.5 Middle East and Africa

6.4.5.1 United Arab Emirates

6.4.5.2 Saudi Arabia

6.4.5.3 South Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

7.1.2 Ball Corporation

7.1.3 Crown Holdings Inc.

7.1.4 CANPACK SA (CANPACK Group)

7.1.5 Silgan Holdings Inc.

7.1.6 Greif Inc.

7.1.7 TUBEX Packaging GmbH

7.1.8 Mauser Packaging Solutions

7.1.9 Nampak Limited

7.1.10 Colep Packaging (RAR Group Company)

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Metal Packaging Industry Segmentation

Metal packaging is a long-lasting industrial and consumer packaging solution comprised mostly of two key materials, i.e., steel and aluminum. The scope of the metal packaging market is limited to B2B demand. The package type has outstanding qualities like durability, flexibility, and cost-effectiveness, providing various advantages over other packaging solutions for specific industrial applications. Aluminum is a reasonably simple metal to sterilize for use in packaging. Due to its superior barrier protection and strength, it is an excellent choice for packing materials.

The metal packaging market is segmented by material type (steel and aluminum), product type (cans [food cans, beverage cans, and aerosol cans], bulk containers, shipping barrels and drums, caps and closures, and other product types), end-user industry (beverage, food, cosmetic and personal care, household, paints and varnishes, and other end-user industries), and Geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Spain, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material Type | |

| Aluminium | |

| Steel |

| By Product Type | |||||

| |||||

| Bulk Containers | |||||

| Shipping Barrels and Drums | |||||

| Caps and Closures |

| By End-user Industry | |

| Beverage | |

| Food | |

| Cosmetics and Personal Care | |

| Household | |

| Paints and Varnishes |

| By Geography*** | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Metal Packaging Market Research FAQs

How big is the Metal Packaging Market?

The Metal Packaging Market size is expected to reach USD 154.29 billion in 2024 and grow at a CAGR of 3.54% to reach USD 183.59 billion by 2029.

What is the current Metal Packaging Market size?

In 2024, the Metal Packaging Market size is expected to reach USD 154.29 billion.

Who are the key players in Metal Packaging Market?

Ardagh Metal Packaging SA (Ardagh Group SA), Ball Corporation, Crown Holdings, Inc., Can-Pack S.A. and Silgan Holdings are the major companies operating in the Metal Packaging Market.

Which is the fastest growing region in Metal Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Metal Packaging Market?

In 2024, the Asia Pacific accounts for the largest market share in Metal Packaging Market.

What years does this Metal Packaging Market cover, and what was the market size in 2023?

In 2023, the Metal Packaging Market size was estimated at USD 148.83 billion. The report covers the Metal Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Metal Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Metal Packaging Industry Report

Statistics for the 2024 Metal Packaging market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Metal Packaging analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.