Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

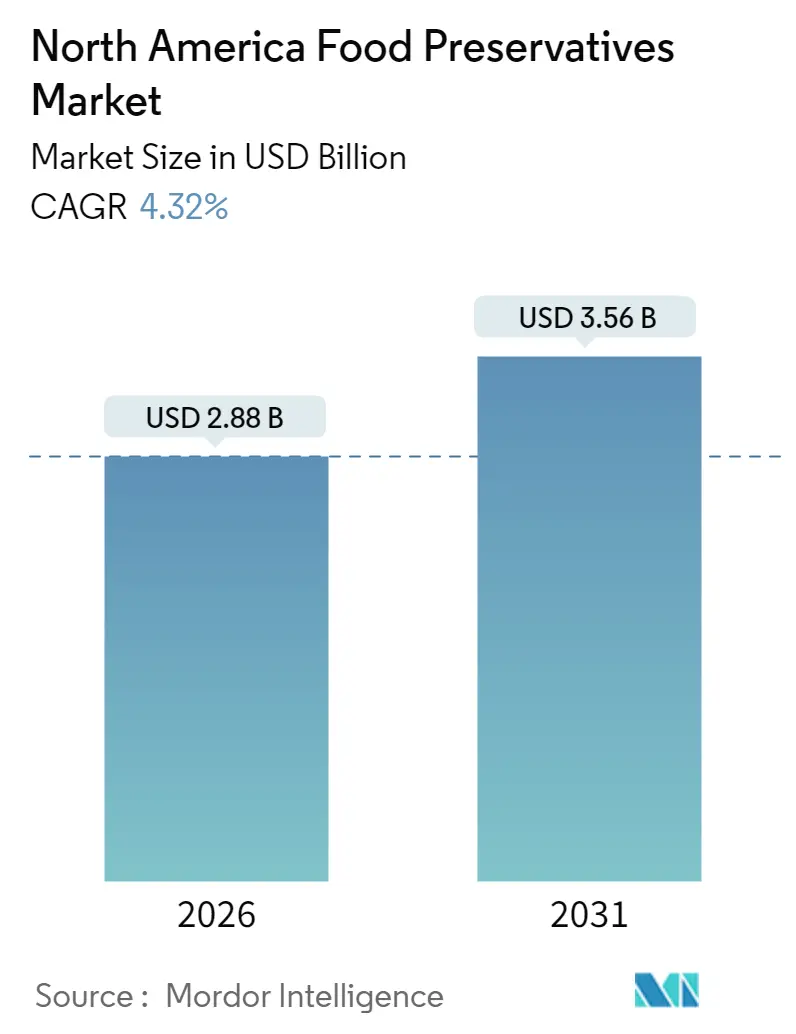

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Food Preservatives Market Analysis by Mordor Intelligence

The North America food preservatives market size in 2026 is estimated at USD 2.88 billion, growing from 2025 value of USD 2.76 billion with 2031 projections showing USD 3.56 billion, growing at 4.32% CAGR over 2026-2031. The market is driven by the increasing demand for processed and convenience foods, which require extended shelf life and preservation of quality. Synthetic preservatives continue to dominate the market in terms of value due to their cost-effectiveness and efficiency in preventing spoilage. However, growing regulatory scrutiny, including state-level bans on specific additives, is reshaping the market dynamics. Additionally, rising consumer awareness regarding health and wellness is fueling the demand for clean-label products, which, in turn, is driving investments toward nature-based alternatives. These natural preservatives, derived from plant and microbial sources, are gaining traction as they align with the evolving consumer preference for minimally processed and chemical-free food products. The market is also influenced by advancements in preservation technologies and the development of innovative solutions to meet the dual objectives of safety and sustainability.

Key Report Takeaways

- By product type, synthetic solutions held 59.78% of the North America food preservatives market share in 2025, while natural preservatives are projected to post a 5.75% CAGR to 2031.

- By function, antimicrobials led with 59.31% revenue share in 2025; antioxidants are set to expand at a 6.02% CAGR through 2031.

- By form, dry and granular formats captured 61.92% share of the North America food preservatives market size in 2025, whereas liquid systems are forecast to grow at 5.42% CAGR to 2031.

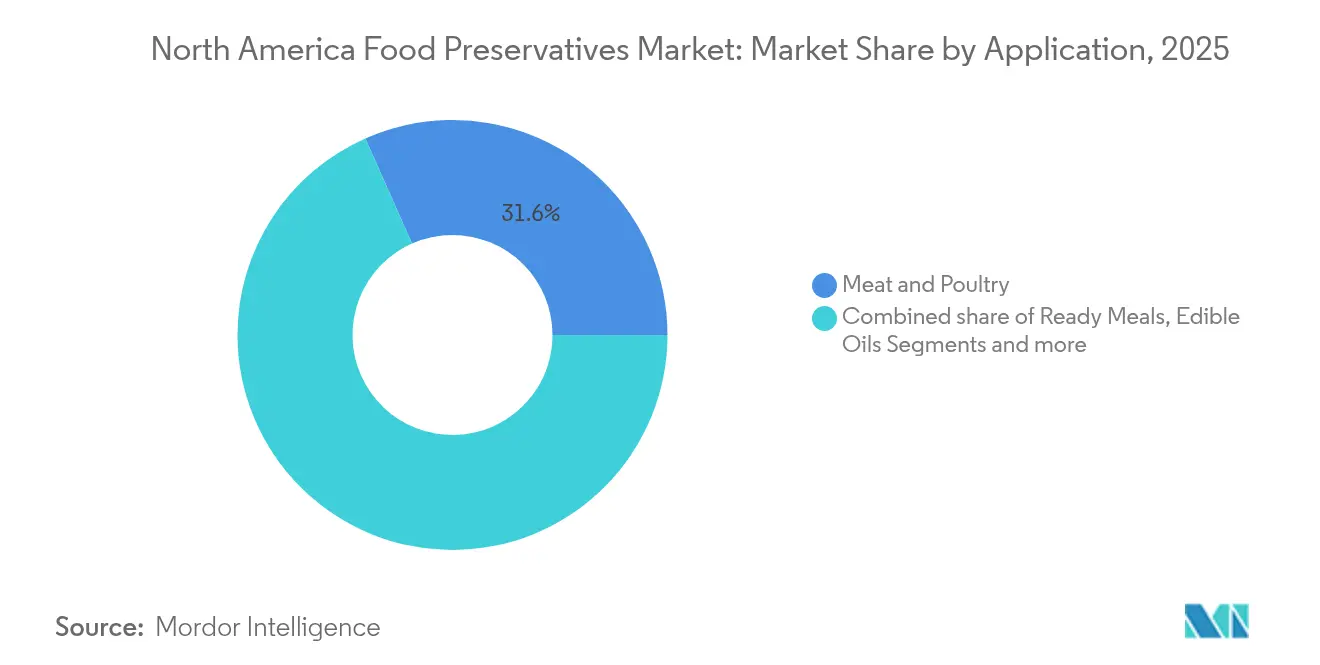

- By application, meat and poultry dominated with a 31.64% share of the North America food preservatives market size in 2025; ready meals recorded the fastest growth at 6.05% CAGR to 2031.

- By geography, the United States commanded 79.88% of the North American food preservatives market share in 2025; Mexico is the fastest-growing market at 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Food Preservatives Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaged bakery sector drives preservatives market | +0.8% | North America, with concentrated impact in US Midwest and Canada | Medium term (2-4 years) |

| Increased demand for processed and convenience foods | +1.2% | North America, with strongest penetration in US urban centers and Canadian metropolitan areas | Short term (≤ 2 years) |

| Growing consumption of packaged and ready-to-eat products | +0.9% | North America, accelerated by post-pandemic consumption patterns | Short term (≤ 2 years) |

| Customized preservation for allergen free foods | +0.6% | US and Canada, driven by regulatory compliance and consumer health awareness | Medium term (2-4 years) |

| Use of antioxidant preservatives in nutrient-rich foods | +0.7% | North America, with premium positioning in health-conscious demographics | Long term (≥ 4 years) |

| Innovation in natural and clean label preservative | +1.1% | US and Canada, with regulatory support and consumer preference alignment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Packaged Bakery Sector Drives Preservatives Market

North America's food preservatives market is being significantly propelled by the packaged bakery sector. As consumers increasingly gravitate towards convenience foods, the demand for packaged bakery items has surged. This uptick has, in turn, heightened the reliance on food preservatives, essential for extending shelf life and ensuring product quality. The Food and Drug Administration (FDA) underscores the importance of food preservatives, noting their pivotal role in thwarting spoilage from microorganisms and oxidation. This not only safeguards food safety but also curtails food waste, which is a growing concern in the food industry. Moreover, the American Bakers Association (ABA) points out that the rising consumer inclination towards ready-to-eat bakery products has intensified the demand for robust preservation methods to meet quality and safety standards. Highlighting the sector's significance, the ABA notes that the U.S. bakery industry boasts an impressive annual revenue of USD 42 billion [1]Source: American Bakers Association, "Bakers Enrich America", americanbakers.org, emphasizing its dependence on preservatives to sustain production and distribution efficiency. Given these dynamics, the demand for food preservatives is poised to persist in the coming years, driven by evolving consumer preferences and the need for extended product shelf life.

Increased Demand for Processed and Convenience Foods

Driven by changing consumer lifestyles and urbanization, the North American food preservatives market is witnessing robust growth, fueled by a surging appetite for processed and convenience foods. Medixiv reports that in 2023, ultra-processed foods constituted over 60% of the caloric intake in the U.S. diet [2]Source: Medrxiv, "Ultra-processed food staples dominate mainstream U.S. supermarkets. Americans more than Europeans forced to choose between health and cost", medrxiv.org. This significant reliance on processed foods highlights the growing consumer preference for products that are quick to prepare and easy to consume, aligning with the fast-paced modern lifestyle. As urbanization accelerates and lifestyles evolve, there's an escalating demand for ready-to-eat meals that cater to convenience without compromising on quality. The FDA's oversight on food preservatives underscores a commitment to safety and quality, bolstering the market's expansion by ensuring consumer trust in these products. With manufacturers increasingly prioritizing shelf life and product integrity, the demand for food preservatives is set to rise, mirroring consumer desires for convenience, longer-lasting food options, and consistent product quality.

Customized Preservation for Allergen Free Foods

The increasing demand for allergen-free foods is one of the key drivers of the market. Consumers are becoming more health-conscious and are actively seeking food products that cater to specific dietary needs, including allergen-free options. This trend has led to the development of customized preservation techniques that ensure the safety, quality, and extended shelf life of allergen-free foods. Manufacturers are investing in innovative preservation methods to meet regulatory standards and consumer expectations, thereby driving growth in the market. Additionally, the rising prevalence of food allergies and intolerances has further amplified the need for effective preservation solutions tailored to allergen-free products, making this a significant factor in the market's expansion. The growing awareness of food safety and the increasing availability of allergen-free products in retail and online platforms have also contributed to this trend. Furthermore, advancements in food preservation technologies, such as natural preservatives and clean-label solutions, are enabling manufacturers to address consumer preferences for minimally processed and chemical-free foods. These developments not only enhance the appeal of allergen-free products but also strengthen their market presence.

Use of Antioxidant Preservatives in Nutrient-Rich Foods

The use of antioxidant preservatives is a significant driver in the North American food preservatives market. These preservatives play a crucial role in extending the shelf life of nutrient-rich foods by preventing oxidation, which can lead to spoilage and nutrient degradation. The rising demand for convenience foods, coupled with the growing awareness of health and wellness among consumers, has amplified the need for effective preservation methods. Antioxidant preservatives not only maintain the quality and safety of food products but also ensure that essential nutrients remain intact during storage and distribution. This has become particularly important in the region, where the consumption of fortified and functional foods is on the rise. Additionally, the increasing focus on reducing food waste has further propelled the adoption of antioxidant preservatives in the region. As manufacturers strive to meet consumer expectations for high-quality, nutrient-dense products, the role of antioxidant preservatives continues to gain prominence in the market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations and approvals process | -0.7% | North America, with heightened impact from FDA GRAS reforms and state-level bans | Short term (≤ 2 years) |

| Consumer awareness of health risks associated with synthetic preservatives | -0.5% | US and Canada, driven by health-conscious demographics and social media influence | Medium term (2-4 years) |

| Limited efficacy of natural preservatives in certain applications | -0.4% | North America, with particular challenges in high-moisture and extended shelf-life applications | Long term (≥ 4 years) |

| Consumer inclination towards fresh foods | -0.3% | North America, concentrated in affluent urban markets with access to fresh alternatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations and Approvals Process

Stringent government regulations and the complex approval processes act as significant restraints in the North American food preservatives market. Regulatory bodies in the region, such as the Food and Drug Administration (FDA) in the United States and Health Canada, enforce strict guidelines to ensure the safety and efficacy of food preservatives. These regulations often require extensive testing, documentation, and compliance with safety standards, which can increase the time and cost for manufacturers to bring new preservatives to market. Additionally, the approval process for food preservatives involves rigorous scrutiny, including assessments of potential health risks and environmental impacts. This can lead to delays in product launches and limit the availability of innovative solutions in the market. As a result, companies operating in this market must allocate significant resources to navigate these regulatory challenges, which can hinder market growth during the forecast period.

Consumer Awareness of Health Risks Associated with Synthetic Preservatives

In the North American food preservatives market, rising consumer awareness regarding the potential health risks associated with synthetic preservatives acts as a significant market restraint. Studies have linked synthetic preservatives, such as sodium benzoate and butylated hydroxyanisole (BHA), to adverse health effects, including allergies and potential carcinogenic risks. According to the United States Food and Drug Administration (FDA), while these preservatives are generally recognized as safe (GRAS) when used within prescribed limits, growing consumer skepticism has led to increased demand for natural alternatives. Additionally, a report by the Organic Trade Association (OTA) highlights that food claims like organic, vegan, and allergen-free are almost 40% more important to Millennials and Gen Z than to older generations in 2024 [3]Source: Organic Trade Association, "Younger, health-conscious consumers are embracing organic, OTA survey shows", ota.com. This shift in consumer preference is expected to challenge the growth of synthetic preservatives in the forecast period.

Segment Analysis

By Product Type: Natural Preservatives Gain Momentum

In 2025, synthetic preservatives dominated the North American food preservatives market, holding a substantial 59.78% market share. Their widespread adoption is attributed to their proven efficacy in preventing spoilage and extending shelf life, coupled with cost-effectiveness. These preservatives are particularly favored in processed and packaged foods, where maintaining product stability over extended periods is critical. Synthetic preservatives, such as benzoates, sorbates, and nitrites, are extensively used due to their ability to inhibit microbial growth and ensure food safety. Despite growing concerns over synthetic additives and their potential health impacts, their established performance, regulatory approvals, and affordability continue to drive their demand in the region.

Conversely, the natural preservatives segment is gaining momentum and is projected to outpace its synthetic counterpart. With a forecasted CAGR of 5.75% from 2026 to 2031, this segment is driven by increasing consumer preference for clean-label products and natural ingredients. Natural preservatives, derived from sources such as plant extracts, essential oils, and organic acids, are becoming popular due to their perceived health benefits and alignment with sustainability trends. Additionally, the rising awareness of the potential adverse effects of synthetic additives has further fueled the demand for natural alternatives. This shift reflects a broader movement toward healthier and more transparent food options in the North American market, with manufacturers increasingly investing in research and development to enhance the efficacy and stability of natural preservatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Function: Antioxidants Outpace Antimicrobials

In 2025, antimicrobial preservatives captured a dominant 59.31% share of the North American market, underscoring their pivotal role in food safety by curbing pathogen growth. These preservatives are especially vital for high-moisture foods, where microbial spoilage poses significant safety challenges. The antimicrobial category includes synthetic choices like benzoates and sorbates, alongside natural options such as cultured dextrose and fermented ingredients that yield organic acids with antimicrobial traits.

Although antioxidant preservatives command a smaller slice of the market, they're set to expand at a robust 6.02% CAGR from 2026 to 2031. Their growth is fueled by their vital function in thwarting oxidative degradation in fat-rich foods. This surge is a testament to rising consumer awareness about the adverse effects of oxidation, including nutritional loss and off-flavors. Notably, plant-based antioxidants are on the rise, with extracts from rosemary and green tea proving as effective as synthetic counterparts like BHA and BHT, especially in meat applications. Moreover, the pivot towards natural antioxidants is bolstered by studies highlighting the enhanced preservation benefits of synergistic combinations of natural extracts, all while aligning with the clean label trend.

By Application: Ready Meals Lead Growth Trajectory

In 2025, Meat and poultry dominated the market, securing a 31.64% share. This segment's dominance can be attributed to the high demand for processed and preserved meat products in the region, driven by changing consumer lifestyles and preferences for convenience foods. The use of preservatives in meat and poultry ensures extended shelf life, maintains product quality, and prevents microbial growth, which is critical for food safety. Additionally, the growing consumption of ready-to-eat and frozen meat products has further fueled the demand for preservatives in this segment. The increasing focus on reducing food waste and enhancing product longevity has also played a significant role in the widespread adoption of preservatives in the meat and poultry industry.

Ready meals are set to emerge as the fastest-growing segment, boasting a projected CAGR of 6.05% from 2026 to 2031. This surge is fueled by consumer preferences for convenient, high-quality meals that boast an extended shelf life. Innovations in preservation technologies, tailored for intricate multi-component food systems, bolster this growth. A standout advancement is microwave-assisted thermal sterilization, which enables swift heating, safeguarding both nutritional and sensory attributes, all while ensuring food safety. The bakery and confectionery sectors remain pivotal in the preservative market, with a keen emphasis on mold inhibition. In contrast, the meat and poultry sector is pivoting towards natural preservation methods. Companies are now crafting clean-label solutions that rival the effectiveness of traditional preservatives, aligning with consumer desires for familiar ingredients.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Dry Formulations Dominates, Liquid Formulations Gain Momentum

In 2025, dry/granular preservatives captured a dominant 61.92% market share, bolstered by their stability, handling convenience, and dosing precision in manufacturing. These preservatives are widely adopted across various applications, particularly in bakeries, where they seamlessly integrate with dry ingredients, and in meat processing, ensuring uniform distribution throughout the product. Their dry form offers significant logistical advantages, including a lighter shipping weight, which reduces transportation costs, an extended shelf life that minimizes waste, and easier storage requirements compared to liquid preservatives. These attributes make them a preferred choice for manufacturers aiming to optimize efficiency and maintain product quality.

Meanwhile, liquid preservatives are set to outpace them with a projected growth rate of 5.42% CAGR from 2026-2031. Their rise is attributed to better dispersion and a growing role in ready-to-eat foods and beverages. Liquids provide manufacturers with distinct advantages, such as easier blending in moisture-rich products and consistent distribution in intricate mixes. Innovations in liquid delivery, like those from Corbion, are boosting their marketability, merging antimicrobial strength with better handling. The surge in liquid preservatives also highlights the rise of natural solutions, as many plant extracts achieve optimal preservation when delivered in liquid form.

Geography Analysis

In 2025, the United States dominates the North American food preservatives market, holding a commanding 79.88% share. Bolstered by a robust manufacturing infrastructure and a dual oversight system at both federal and state levels, the U.S. market is further energized by consumers' willingness to invest in clean labels, paving the way for technological advancements. The country’s focus on innovation and the adoption of advanced preservation technologies further solidifies its leadership position in the region. Additionally, the growing demand for convenience foods and ready-to-eat meals in the United States has significantly increased the need for effective food preservatives, ensuring product safety and extending shelf life.

Canada also plays a significant role in the North American food preservatives market. The country benefits from a well-established food processing industry, which is a key contributor to its market share. Increasing consumer demand for natural and clean-label preservatives, coupled with a strong regulatory framework emphasizing food safety and quality, drives the adoption of innovative preservation solutions. Canada’s export-oriented food industry creates opportunities for the development and application of advanced preservatives to meet international standards. Furthermore, the rising trend of health-conscious consumers in Canada has led to a growing preference for organic and natural food products, which in turn is driving the demand for natural preservatives.

Meanwhile, Mexico stands out with the most pronounced growth trajectory, projected at a 5.08% CAGR through 2031. The country’s growing food and beverage industry, supported by rising urbanization, increasing disposable incomes, and evolving consumer preferences, contributes to its high growth potential in the food preservatives market. Furthermore, the expansion of retail chains and the increasing penetration of packaged and processed foods in Mexico are expected to drive the demand for food preservatives in the coming years. The country’s strategic location and trade agreements with major economies also facilitate the growth of its food processing sector, further boosting the demand for preservatives. Additionally, the increasing focus on reducing food waste and improving food safety standards in Mexico is expected to create opportunities for the adoption of advanced preservation solutions.

Competitive Landscape

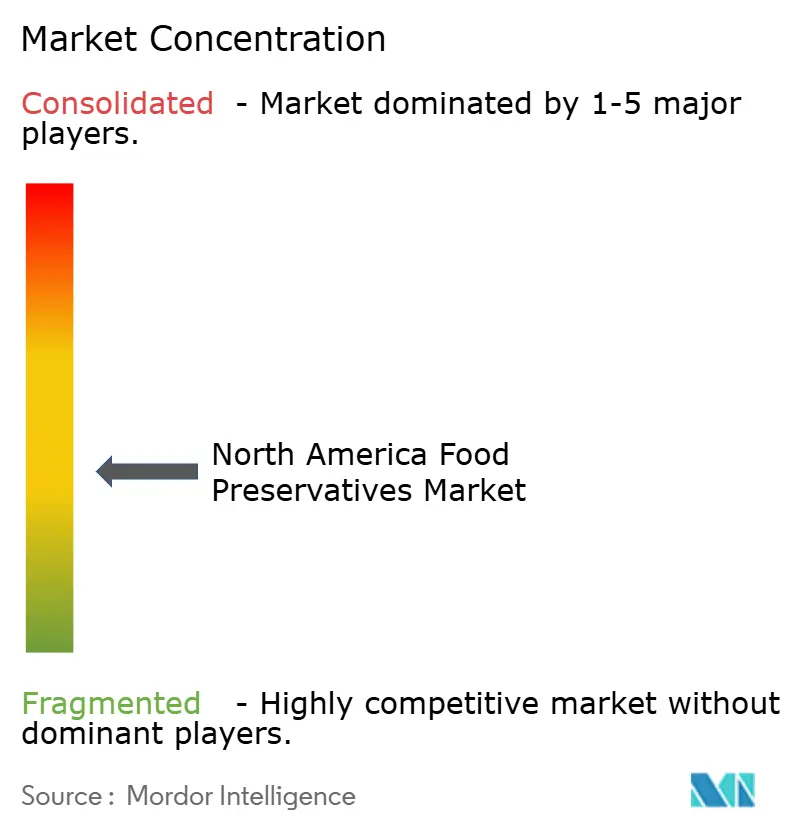

The North American food preservatives market exhibits a moderately fragmented structure. This level of fragmentation fosters a dynamic and competitive environment where numerous players actively compete to secure their market positions. The diversity of participants ensures a wide range of product offerings, catering to the varied demands of consumers and industries across the region. The competitive nature of the market drives continuous innovation, compelling companies to differentiate themselves through unique value propositions and advanced technological solutions. This dynamic interplay between competitors significantly influences the market's growth and development.

Established players in the market leverage their scale advantages to maintain a strong foothold. These advantages include extensive distribution networks, robust brand recognition, and economies of scale, which collectively enable them to sustain their competitive edge. To remain ahead, these companies focus on expanding their product portfolios and improving operational efficiencies. Significant investments in research and development allow them to introduce new and improved food preservatives that align with evolving consumer preferences and comply with stringent regulatory standards. By capitalizing on their resources and market expertise, these players continue to dominate key segments of the market.

Meanwhile, innovative disruptors are reshaping the competitive landscape by introducing technologically advanced solutions tailored to specific market needs. These emerging players often target niche segments, offering specialized products that align with trends such as clean-label ingredients and natural preservatives. By adopting agile business models and leveraging cutting-edge technologies, these disruptors are successfully capturing market share and challenging the dominance of established players. Their ability to address unmet consumer demands and adapt quickly to market changes positions them as key contributors to the evolving dynamics of the North America Food Preservatives Market.

North America Food Preservatives Industry Leaders

-

Cargill, Incorporated

-

Kerry Group plc

-

BASF SE

-

DSM-Firmenich AG

-

Corbion N.V.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Corbion developed a natural mold inhibition solution for bakery products that extended shelf life and maintained quality while addressing consumer preferences for non-synthetic preservatives.

- November 2024: In December 2023, Tate & Lyle announced the acquisition of CP Kelco for USD 1.8 billion, which strengthened its position in the food preservatives market through expanded specialty food and beverage solutions.

- October 2024: Shield V, developed by Kemin Industries, was a clean label ingredient that prevented mold growth in food products. The ingredient maintained food freshness and extended shelf life, benefiting food manufacturers and processors.

- September 2024: Syensqo developed Riza, a fully plant-based range of antioxidants and flavors extracted from rosemary, designed for food preservation and addressing consumer preferences for natural ingredients.

North America Food Preservatives Market Report Scope

Food preservatives are additives used to prevent or retard spoilage caused by chemical changes, improve appearance, along with maintaining food’s nutritional quality.

The North America Food Preservatives Market is segmented by type,

including natural and synthetic. Based on the application, the market is divided into bakery & confectionery, meat & poultry, ready meals, sweet and savory, sauces and dressings, edible oils, and other applications. Based on form, the market is segmented into dry/granular and liquid. Based on function, the market is segmented into antimicrobials and antioxidants. The study also involves the analysis of regions such as the United States, Canada, Mexico, and the rest of North America. The market sizing has been done in value terms in USD for all the above-mentioned segments.

By Type

| Synthetic | Sorbates |

| Benzonates | |

| Propionates | |

| Others | |

| Natural | Nisin |

| Natamycin | |

| Vinegar | |

| Rosemary Extract | |

| Mixed Tocopherols | |

| Others |

By Function

| Antimicrobial |

| Antioxidants |

By Form

| Dry/Granular |

| Liquid |

By Application

| Bakery and Confectionery |

| Meat and Poultry |

| Ready Meals |

| Sweet and Savory Snacks |

| Sauces and Dressings |

| Edible Oils |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Synthetic | Sorbates |

| Benzonates | ||

| Propionates | ||

| Others | ||

| Natural | Nisin | |

| Natamycin | ||

| Vinegar | ||

| Rosemary Extract | ||

| Mixed Tocopherols | ||

| Others | ||

| By Function | Antimicrobial | |

| Antioxidants | ||

| By Form | Dry/Granular | |

| Liquid | ||

| By Application | Bakery and Confectionery | |

| Meat and Poultry | ||

| Ready Meals | ||

| Sweet and Savory Snacks | ||

| Sauces and Dressings | ||

| Edible Oils | ||

| Other Applications | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America food preservatives market?

The market is valued at USD 2.88 billion in 2026.

Which preservative type is growing the quickest?

Natural preservatives, led by cultured dextrose and plant extracts, are advancing at a 5.75% CAGR.

Why are antioxidants gaining traction in North America?

Vitamin-fortified and nutrient-rich foods need oxidative stability, driving a 6.02% CAGR for antioxidant systems.

Which geography offers the highest growth potential?

Mexico posts the fastest expansion at 5.08% CAGR, buoyed by new labelling laws that favour natural preservation technologies.