Market Overview

| Study Period | 2020 - 2031 |

|---|---|

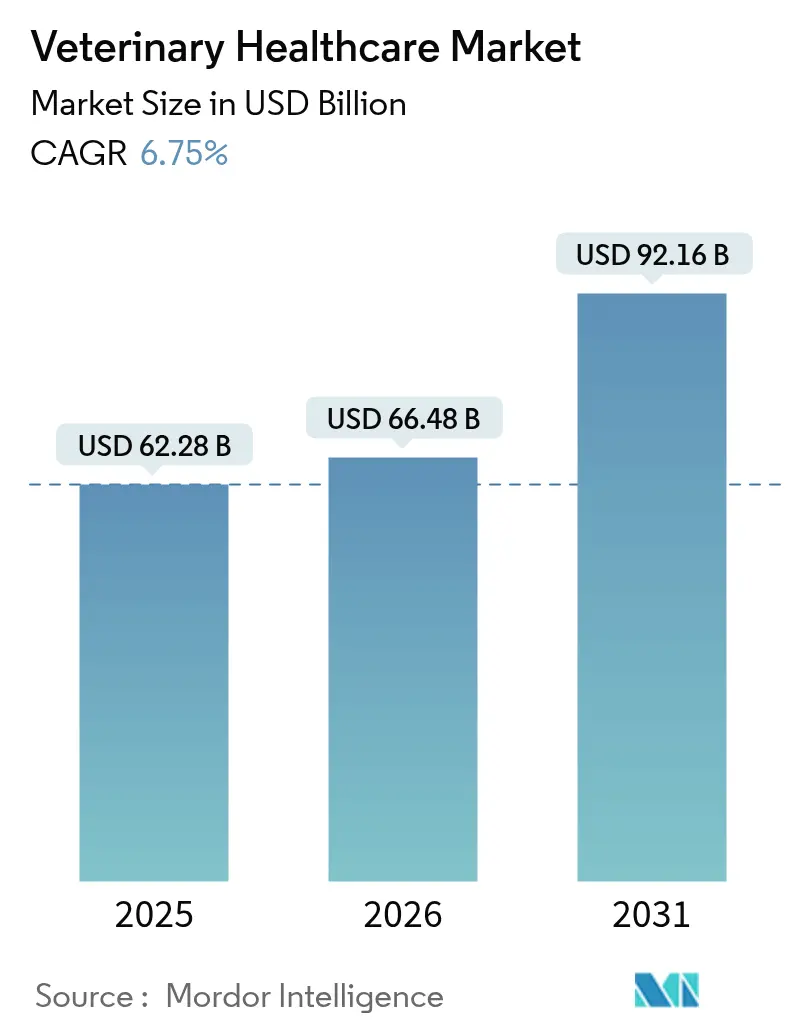

| Market Size (2026) | USD 66.48 Billion |

| Market Size (2031) | USD 92.16 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

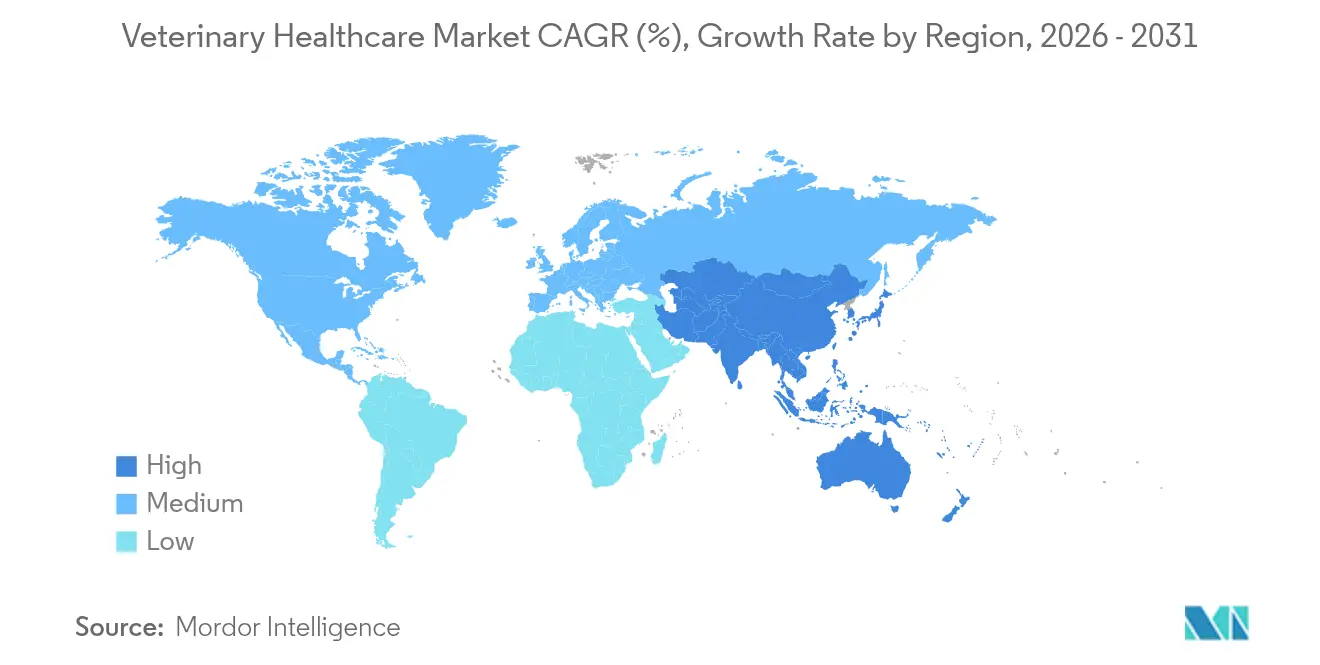

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Healthcare Market Analysis by Mordor Intelligence

The veterinary healthcare market is expected to grow from USD 62.28 billion in 2025 to USD 66.48 billion in 2026 and is forecast to reach USD 92.16 billion by 2031 at 6.75% CAGR over 2026-2031. Companion-animal spending, robust livestock expansion in emerging economies, and rapid digital adoption inside veterinary practices underpin the steady rise in the veterinary healthcare market. Preventive care models are becoming mainstream as owners demand earlier disease detection, insurers encourage risk-mitigation protocols, and regulators tighten biosecurity requirements. Diagnostic innovations, especially molecular point-of-care systems, are reshaping clinical workflows by compressing result turnaround from days to minutes. Meanwhile, therapeutic portfolios evolve toward vaccines, immunomodulators, and novel parasiticides that comply with antimicrobial-stewardship mandates. Digital health platforms link patient records, on-farm sensors, and genetic data, allowing clinicians to navigate complex treatment choices while monetizing real-time insights.

Key Report Takeaways

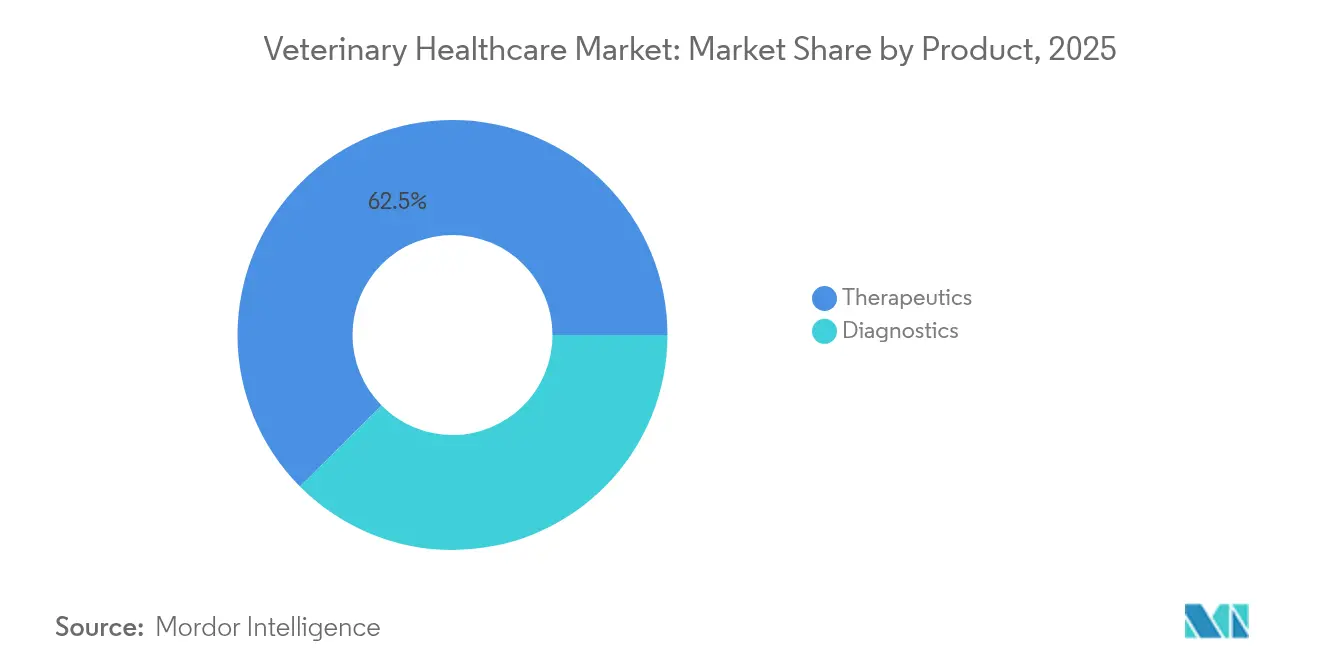

- By product type, therapeutics commanded 62.45% of the veterinary healthcare market share in 2025, while diagnostics is forecast to expand at a 7.12% CAGR through 2031.

- By animal type, dogs and cats accounted for 55.10% of the veterinary healthcare market size in 2025; poultry is advancing at a 6.38% CAGR to 2031.

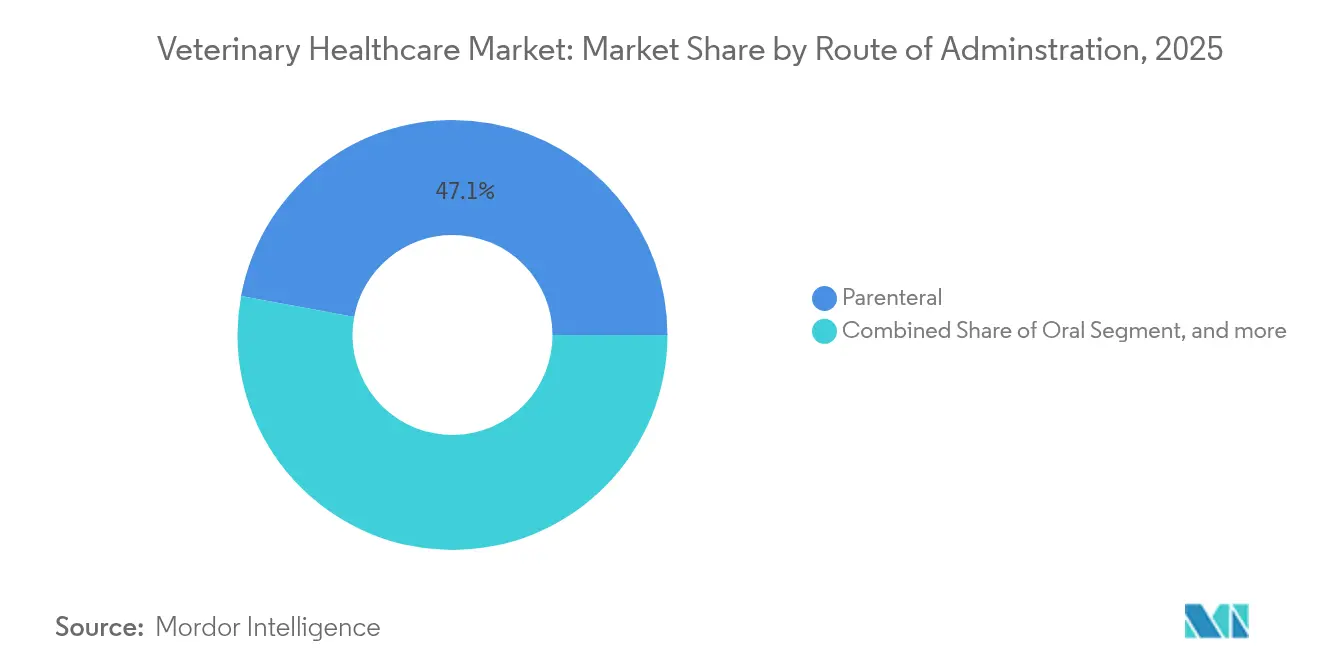

- By route of administration, parenteral products led with 47.10% revenue share in 2025, but oral delivery is projected to rise at a 6.60% CAGR through 2031.

- By end user, veterinary hospitals and clinics held 57.70% of the veterinary healthcare market size in 2025, whereas point-of-care and in-house testing settings are registering the highest growth at a 7.28% CAGR through 2031.

- By geography, North America led with 43.80% revenue share in 2025, whereas, Asia-Pacific is projected to rise at a 8.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Healthcare Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protein-rich diet demand | +1.2% | APAC core; Latin America | Medium term (2-4 years) |

| Pet humanization & spending | +1.8% | North America, EU; urban APAC | Short term (≤ 2 years) |

| Emerging-economy livestock expansion | +1.1% | APAC; spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Mandatory preventive vaccination programs | +0.9% | Early adoption in developed markets | Medium term (2-4 years) |

| Digital transformation of veterinary clinics | +0.7% | North America, EU; gradual APAC rollout | Long term (≥ 4 years) |

| One Health surveillance integration | +0.6% | Global (WHO-driven) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Protein-Rich Animal Products

Livestock producers are scaling operations to meet a projected 40% rise in protein consumption across developing nations by 2030, a dynamic that forces farms to adopt intensive biosecurity and prophylactic protocols[1]Food and Agriculture Organization, “Animal Protein Outlook 2025,” fao.org. Higher stocking densities increase infection risk, so veterinarians deploy blanket vaccination and continuous health monitoring to avoid catastrophic outbreaks. Asian aquaculture operators now embed diagnostic sensors directly into recirculating systems, feeding real-time data to remote veterinarians who adjust treatment regimens on the fly. Precision nutrition programs that combine feed additives with diagnostic feedback loops blur lines between traditional animal health and production. The heightened disease-control costs ultimately expand per-animal healthcare budgets, reinforcing sustained demand in the veterinary healthcare market.

Increasing Pet Humanization and Healthcare Spending

Seventy percent of U.S. households owned at least one pet in 2024, and average annual veterinary outlay climbed to USD 1,480 per household, up 23% from 2019. Owners treat pets as family members, tolerating premium prices for cancer immunotherapies, dental implants, and behavioral tele-consults. Pet insurance penetration remains below 5% worldwide, positioning underwriters to unlock latent demand by spreading high-ticket costs. Demand for wellness plans that bundle vaccines, diagnostics, and nutrition counseling promotes recurring revenue for clinics. This sentiment shift elevates diagnostic compliance, accelerating adoption of point-of-care platforms inside general practices. Growing emotional attachment fuels non-price-sensitive segments, upholding the veterinary healthcare market even during broader economic slowdowns.

Expanding Livestock Production in Emerging Economies

The livestock sectors of Southeast Asia and Sub-Saharan Africa are expanding at 8-12% yearly, dwarfing growth rates in developed regions. International investors fund modern facilities with controlled-environment housing, automated feeding, and on-site labs. Such upgrades demand continuous veterinary oversight, spurring sales of vaccines, biosensors, and rapid diagnostic kits. Yet, infrastructure gaps in cold chain, rural workforce, and regulatory enforcement expose producers to biosecurity lapses. Vendors capable of bundling products with on-farm training and telemedicine support capture disproportionate share in the veterinary healthcare market. Local governments leverage public-private partnerships to raise animal-health standards, broadening market access for multinational suppliers with compliance expertise.

Regulatory Shift Toward Preventive Vaccination Programs

Agencies such as the European Medicines Agency now mandate baseline vaccination for commercial herds, making prophylaxis a prerequisite for market access[2]European Medicines Agency, “Veterinary Vaccination Guidelines 2024,” ema.europa.eu. The U.S. Department of Agriculture expanded interstate movement rules to include updated immunization records, tying certification to digital passports. These requirements create non-negotiable demand for veterinary biologics, boosting cold-chain logistics investments. Manufacturers with large-volume antigen production and freeze-drying know-how enjoy scale advantages. Data-linked vaccine traceability systems connect farmers, regulators, and veterinarians, reinforcing the broader One Health framework and embedding data analytics into daily workflows across the veterinary healthcare market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory compliance and lengthy approval timelines | -0.8% | Highest in U.S. and EU | Short term (≤ 2 years) |

| High cost of advanced therapeutics and diagnostic equipment | -1.1% | Rural areas and emerging markets worldwide | Medium term (2-4 years) |

| Persistent veterinary-workforce shortages in rural regions | -0.5% | North America, Europe, and developing economies’ rural zones | Medium term (2-4 years) |

| Limited insurance coverage for companion-animal healthcare | -0.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance and Approval Timelines

Average development times for novel veterinary drugs now exceed seven years, partly due to the FDA’s 2024 environmental-impact standards that added up to two extra years per submission. Small innovators struggle to finance protracted trials and multiregional dossiers, reducing pipeline diversity. As fee schedules and post-approval surveillance demands climb, firms prioritize blockbuster indications and shelve niche therapies. The resulting innovation bottleneck could slow adoption of next-generation treatments, although partnering deals with contract research organizations help mitigate capital strain. Consolidation among sponsors concentrates regulatory expertise but may intensify pricing power within the veterinary healthcare market.

High Cost of Advanced Therapeutics and Diagnostic Equipment

Digital radiography consoles, molecular PCR analyzers, and advanced biologics require upfront outlays exceeding USD 100,000, an amount many rural clinics cannot absorb without financing support[3]U.S. Department of Agriculture, “Rural Veterinary Infrastructure Report 2025,” usda.gov. Consumables, maintenance, and technician training add another 40-60% across equipment lifecycles, encouraging cautious purchasing. Urban–rural care disparities widen as city practices deploy sophisticated tools that elevate standards-of-care, while rural providers rely on older technology. Without broad insurance coverage, owners pay directly, restricting adoption of expensive modalities. Companies now pilot subscription models and reagent-rental plans that spread costs, aiming to protect long-run growth in the veterinary healthcare market.

Segment Analysis

By Product: Diagnostics Accelerate amid Therapeutics Leadership

Diagnostics generated the fastest revenue growth at a 7.12% CAGR through 2031, even though therapeutics held a 62.45% share of 2025 sales inside the veterinary healthcare market. Point-of-care analyzers integrate hematology, chemistry, and PCR cartridges in compact footprints that suit first-opinion clinics. In-clinic testing boosts case acceptance and captures revenue previously routed to reference labs. Molecular panels detect multi-pathogen profiles from a single swab, supporting precision medicine protocols once confined to human care. Meanwhile, vaccine portfolios underpin the therapeutic stronghold, safeguarding herd health and limiting antimicrobial overuse. Generic competition pressures margins for legacy antimicrobials, so leading firms emphasize biologics, immunomodulators, and targeted parasiticides. Post-patent biosimilar entries spur price competition but widen access in cost-sensitive settings, ultimately expanding the addressable veterinary healthcare market.

Therapeutic pipelines respond to antimicrobial-stewardship guidance with alternatives such as bacteriophage cocktails and probiotic feed additives. Sustained-release injectables minimize handling stress and labor at large livestock units. In companion animals, combination flea-tick-heartworm preventives command premium price points due to compliance convenience. The United States Environmental Protection Agency’s updated residue-limit rules elevate demand for rapid residue diagnostics, binding therapeutic and diagnostic sales strategies. Companies with omnichannel distribution capabilities synchronize product launches across e-commerce, hospitals, and farm-supply outlets to optimize the veterinary healthcare market size momentum.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Animal Type: Companion Animals Prevail, Poultry Takes Flight

Dogs and cats represented 55.10% of 2025 revenue, underscoring the emotional attachment that underpins discretionary spending power in the veterinary healthcare market. Oncology, orthopedic, and chronic-disease segments flourish as owners pursue human-grade care. Pet insurers broaden formularies to mirror human health benefits, expanding coverage of hereditary conditions and behavioral therapy. In contrast, poultry achieved the fastest category growth at 6.38% CAGR as integrators scale operations, and regulators tighten food-safety scrutiny. Vaccination against avian influenza, Salmonella, and Newcastle disease forms a mandatory cost of operation, embedding ongoing demand.

Ruminant and swine segments maintain steady share driven by productivity-linked interventions such as reproductive hormones and rumen modifiers. Equine athletes command high-margin regenerative therapies like stem-cell injections and platelet-rich plasma, tapping affluent owner demographics. Across species, the World Organisation for Animal Health expands surveillance reporting obligations, elevating diagnostic throughputs. Such cross-species dynamics keep the veterinary healthcare market resilient against localized demand shocks.

By Route of Administration: Oral Formulations Gain Traction

Parenteral routes held 47.10% share in 2025 because injectables deliver rapid systemic effect and suit mass-vaccination campaigns inside the veterinary healthcare market. However, oral products are rising at a 6.60% CAGR thanks to chewable tablets, flavored suspensions, and nanoparticle-enhanced bioavailability. Owners favor at-home administration that avoids travel and injection anxiety, boosting adherence. Pharmaceutical scientists refine taste-masking for bitter actives, enabling once-monthly chewables that rival injectables in efficacy. Topical and transdermal formats occupy niche dermatology and chronic-pain segments, while implantable devices gradually emerge for hormone delivery in cattle and feline microdose pain control. Regulatory agencies issue specific palatability testing guidelines, prompting formulators to integrate sensory-panel feedback into product design. The proliferation of diverse delivery options expands the total addressable veterinary healthcare market size.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Point-of-Care Testing Reshapes Practice Economics

Hospitals and clinics controlled 57.70% of end-user revenues in 2025, yet point-of-care (POC) and in-house settings are expected to grow 7.28% CAGR, outpacing every other channel. Miniaturized analyzers now complete CBC, CRP, and multiplex PCR within 10 minutes, supporting on-the-spot treatment plans that heighten client satisfaction. Reference laboratories still process complex histopathology and surveillance assays, but routine profiles migrate into exam rooms. Academic institutes partner with biotech firms to validate AI-powered image-analysis modules that read cytology smears instantly. Clinics using POC platforms capture higher diagnostic yield per visit, offsetting shrinking margins on commoditized pharmaceuticals. Subscription-based device offerings reduce upfront capital, further democratizing access and broadening transaction volumes inside the veterinary healthcare market.

Geography Analysis

North America retained the largest regional share in 2025, propelled by high pet ownership, mature insurance networks, and supportive regulation. Rural-practice loan forgiveness in the United States and workforce grants in Canada mitigate care deserts, extending product uptake into underserved communities. Europe ranked second, supported by pan-EU licensing pathways that streamline product launches and by stringent animal-welfare standards that drive preventive interventions. Manufacturers navigate post-Brexit customs friction through dual warehousing models that secure supply continuity.

Asia-Pacific recorded the fastest growth and is forecast to surpass Europe in absolute sales before 2031. Urbanizing middle-class households in China, South Korea, and India fuel companion-animal spend, while regional livestock modernization programs inject sustained capital into vaccines and diagnostics. Foreign direct investment teamed with local joint ventures accelerates technology transfer, narrowing the gap with developed-market standards. Governments across ASEAN allocate budget to zoonotic-disease surveillance, integrating veterinary services into public-health frameworks, thereby cementing the long-run outlook for the veterinary healthcare market.

South America and the Middle East & Africa post mid-single-digit growth tied to poultry and aquaculture expansion. Currency volatility and uneven regulatory enforcement temper short-term spending, but multinational alliances with regional distributors steadily improve channel efficiency. Pan-regional e-commerce platforms emerge as low-cost supply routes for clinics, tilting competitive balance toward players with omnichannel fulfillment. Thus, geographic diversification acts as a buffer against localized shocks, sustaining the global veterinary healthcare market trajectory.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The veterinary healthcare market features moderate concentration: the top five companies collectively hold roughly 52% revenue share. Global leaders Zoetis, Elanco, and Boehringer Ingelheim wield scale advantages in R&D, regulatory affairs, and omnichannel logistics. Each integrates therapeutics, biologics, and diagnostics, bundling solutions that increase customer stickiness. Patent expirations on blockbuster antiparasitics attract generic entrants, compressing margins yet broadening access across emerging markets. Diagnostic specialists such as IDEXX and Heska differentiate through software-driven platforms that fuse analytics with hardware.

Digital disruptors build tele-triage and remote monitoring services, narrowing the gap between pet owners and clinicians. Cloud-based practice-management suites integrate e-commerce pharmacies, capturing prescription refills and compliance data. Strategic alliances with AI start-ups feed large language models with anonymized case files, enhancing differential-diagnosis support. Manufacturers invest in green-chemistry processes and biodegradable packaging to meet ESG mandates that sway procurement choices. Joint ventures in Asia and Latin America secure local manufacturing footprints, underpinning faster regulatory approvals and lowering landed costs. The interplay of legacy incumbents and agile newcomers cultivates balanced competition that benefits end users across the veterinary healthcare market.

Veterinary Healthcare Industry Leaders

Zoetis Inc.

Boehringer Ingelheim International GmbH

Elanco Animal Health

Merck & Co., Inc.

Ceva Santé Animale

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Merck & Co., Inc. announced that the European Commission (EC) has approved NUMELVI (atinvicitinib) Tablets for Dogs. NUMELVI is a once-daily, first-line treatment, and is the only second-generation Janus kinase (JAK) inhibitor indicated for the treatment of pruritus associated with allergic dermatitis including atopic dermatitis and treatment of clinical manifestations of atopic dermatitis in dogs. With a once-daily treatment regimen, NUMELVI is clinically effective after the first dose.

- January 2024: Dechra launched Cyclofin, an injectable single-dose solution for acute bovine respiratory disease (BRD). Cyclofin is aimed at BRD caused by oxytetracycline-sensitive Mannheimia haemolytica and Pasteurella multocida, where an anti-inflammatory and antipyretic effect is required.

Global Veterinary Healthcare Market Report Scope

As per the report's scope, veterinary healthcare can be defined as the science associated with diagnosing, treating, and preventing animal diseases. The increasing importance of the production of livestock animals is boosting market growth.

The veterinary healthcare market is segmented by product, animal type, and geography. By product, the market is segmented into therapeutics and diagnostics. By animal type, the market is segmented into dogs, cats, horses, ruminants, swine, poultry, and other animal types. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs & Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animal Types |

By Route Of Administration

| Oral |

| Parenteral |

| Topical |

| Other Route of Administrations |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-Of-Care / In-House Testing Settings |

| Academic & Research Institutes |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs & Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Route of Administrations | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-Of-Care / In-House Testing Settings | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for global veterinary healthcare?

Revenues stand at USD 66.48 billion in 2026 and are forecast to reach USD 92.16 billion by 2031, reflecting a 6.75% CAGR.

Which product line is showing the fastest expansion?

Diagnostics leads growth at a 7.12% CAGR through 2031, driven by molecular point-of-care platforms and rapid in-clinic testing.

How does rising pet humanization affect spending?

Owners treat pets as family members, lifting average U.S. veterinary bills to USD 1,480 per household in 2024 and boosting demand for premium therapies and insurance uptake.

Why is poultry health spending accelerating?

Intensive production and biosecurity rules push poultry to a 6.38% CAGR, with mandatory vaccines and rapid pathogen screening becoming routine.

What impact do point-of-care diagnostics have on veterinary clinics?

In-house analyzers deliver results within minutes, raise case acceptance, and are propelling the fastest end-user growth segment at a 7.28% CAGR.

What key obstacles limit broader product adoption?

Lengthy regulatory approvals add up to two years per novel therapy, while equipment costs above USD 100,000 restrict access for rural and emerging-market clinics.