Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 534.70 Billion |

| Market Size (2030) | USD 675.31 Billion |

| Growth Rate (2025 - 2030) | 4.78% CAGR |

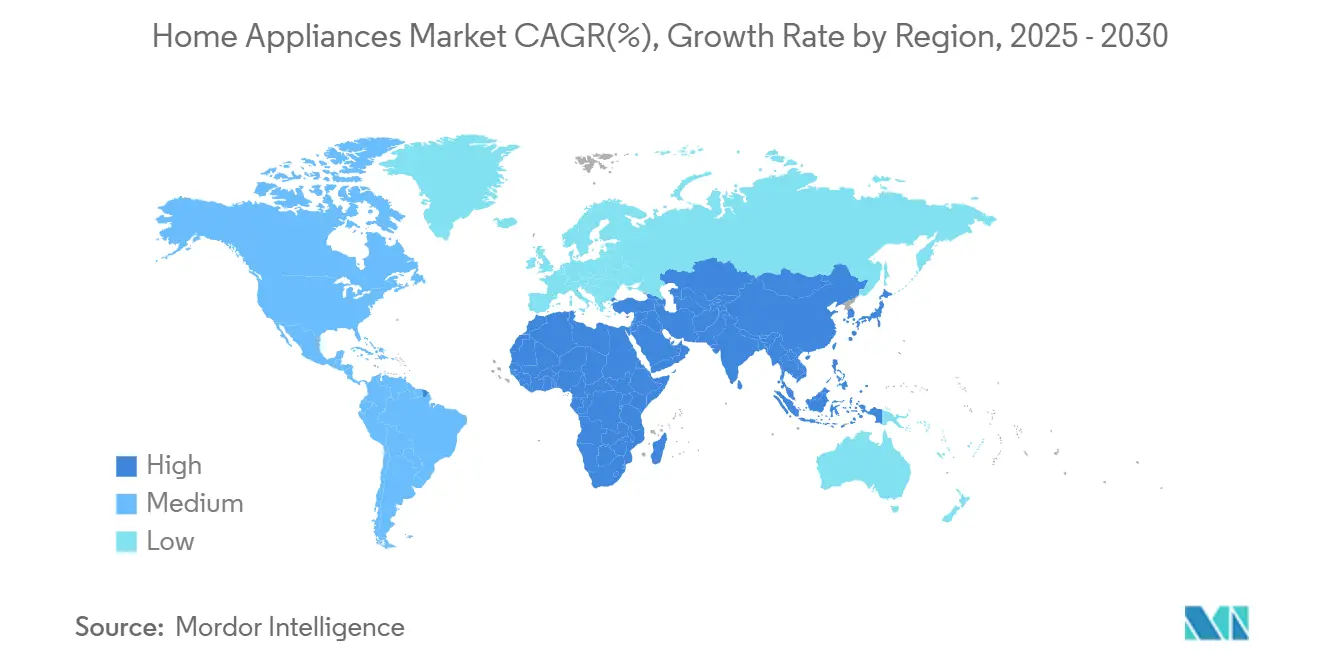

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Home Appliances Market Analysis by Mordor Intelligence

The Home Appliances Market size is estimated at USD 534.70 billion in 2025, and is expected to reach USD 675.31 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

Intensifying sustainability mandates, rapid digitalization, and expanding middle-class spending underpin this steady rise. The adoption of connected appliances now extends well beyond early adopters as mainstream consumers look for time-saving, energy-saving, and health-centric solutions. Manufacturers are accelerating product refresh cycles to comply with stricter efficiency rules, while AI-enabled features help premium brands defend margins. Supply-chain re-engineering and near-shoring keep production agile even as semiconductor allocations favor high-performance computing over traditional electronics. Retail dynamics continue to blur, with shoppers mixing digital discovery, omnichannel price checks, and in-store validation before purchase.

Key Report Takeaways

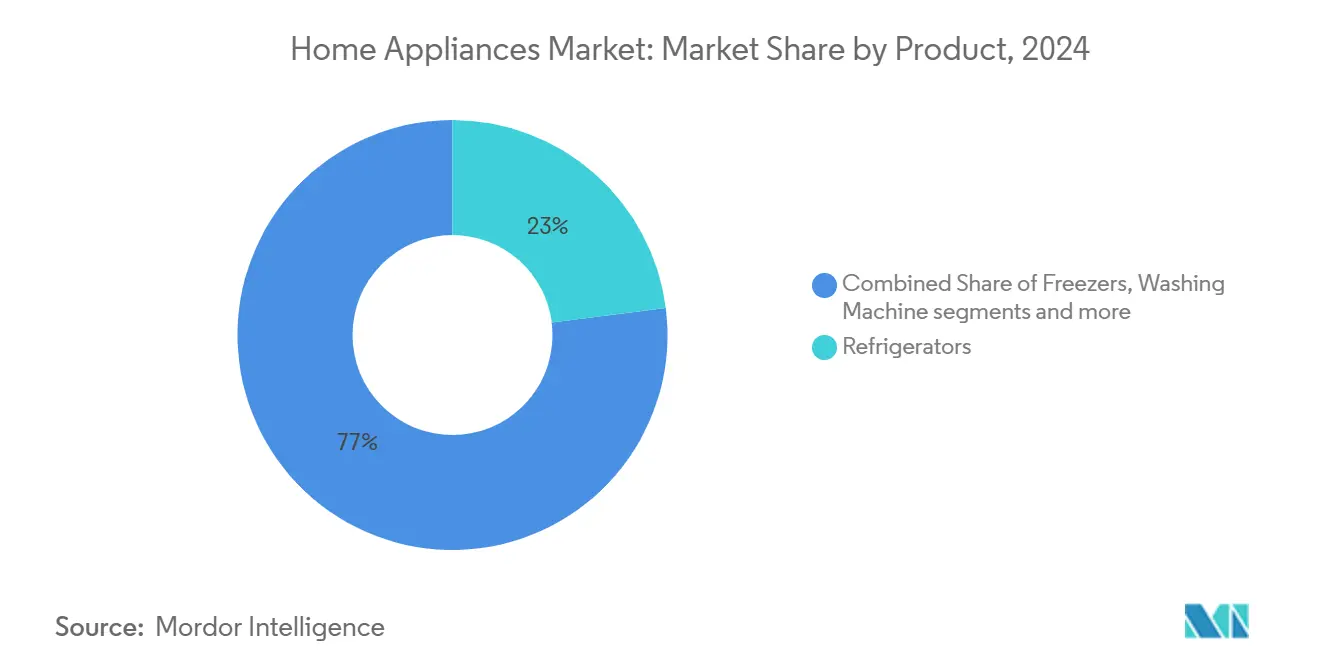

- By product category, refrigerators led with 23% of home appliances market share in 2024; air fryers are projected to expand at an 8.2% CAGR through 2030.

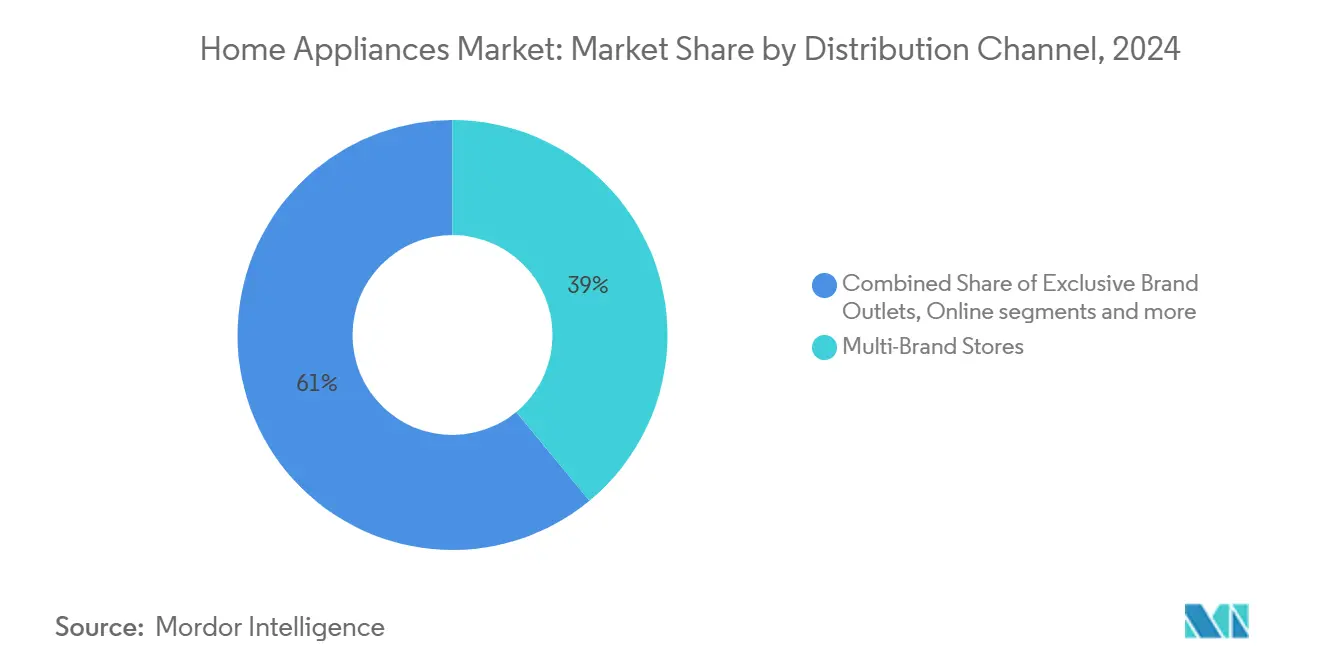

- By distribution channel, multi-brand retail stores held a 39% share of the home appliances market size in 2024, while online channels are set to grow at a 6.7% CAGR to 2030.

- By geography, Asia-Pacific accounted for 46% of the home appliances market share in 2024, whereas the Middle East and Africa region is forecast to post a 6.1% CAGR through 2030.

Global Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and consumer spending power | +1.2% | Global with early gains in Asia-Pacific and Latin America | Medium term (~3- 4 years) |

| IoT-enabled convenience and home automation boom | +1.8% | North America and European Union core, spill-over to Asia-Pacific metros | Short term (≤ 2 years) |

| Stricter energy-efficiency mandates spurring replacement demand | +1.1% | North America and the European Union; emerging adoption in Asia-Pacific | Long term (≥ 5 years) |

| Growth of e-commerce and online sales channels | +0.9% | Global, with the strongest lift in emerging markets | Short term (≤ 2 years) |

| Urbanization and changing lifestyles | +0.7% | Asia-Pacific core, Middle East and Africa, Latin America urban corridors | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

IoT-Enabled Convenience and Home Automation Boom

Connected functionality has become a core purchase criterion for the home appliances market. Refrigerator ranges from Samsung and Haier now integrate voice assistants that reorder consumables, offer food-safety prompts, and monitor energy use directly on screen. LG’s ThinQ platform links laundry, cooling, and cooking products under a single app, while Qualcomm-powered edge-AI chips let devices optimize settings without the cloud, reducing latency and data-privacy risk[1]Samsung Electronics, “Bespoke AI Home Appliances at KBIS 2025,” samsung.com. Mainstream acceptance in North America and the EU is pushing component suppliers to add Wi-Fi, Bluetooth, and advanced sensors as default configurations. As interoperability standards mature, manufacturers gain additional revenue from subscription services, software updates, and in-app marketplaces, reinforcing recurring-revenue models that extend value beyond the initial sale.

Stricter Energy-Efficiency Mandates Spurring Replacement Demand

The U.S. Department of Energy’s 2024 water-heater rule alone is projected to save consumers USD 124 billion over 30 years while elevating heat-pump share from 3% to more than 50% of units sold[2]U.S. Department of Energy, “Energy Conservation Standards for Residential Water Heaters,” energy.gov. Canada’s Amendment 18 adds verification-mark obligations in 2025, prompting early redesigns by market leaders that can absorb testing costs[3]Government of Canada, “Regulations Amending the Energy Efficiency Regulations (Amendment 18),” gazette.gc.ca. Europe’s Eco-design framework tightens dishwasher power ceilings to 223 kWh per year, compelling OEMs to invest in more efficient motors and hydraulic systems[4]Federal Register Editors, “Energy Efficiency Program for Dishwashers,” federalregister.gov. These overlapping regulations compress product lifecycles, accelerate research and development spending on heat-pump compressors, inverters, and low-GWP refrigerants, and raise replacement demand, especially in mature housing stocks across the United States, Germany, and Japan.

Growth of E-Commerce and Online Sales Channels

Retailers report that appliances already represent nearly one-third of total online home-improvement revenue, aided by virtual showrooms, augmented-reality placement, and 48-hour delivery windows. Manufacturers that once relied on dealer networks now pursue direct-to-consumer sites offering extended warranties, installation booking, and branded financing. Because e-commerce compresses price transparency, brands increasingly leverage limited-edition colors, in-app service bundles, and loyalty points to defend average selling prices. Fulfillment complexity encourages regional warehousing near large urban hubs, improving availability while shrinking last-mile emissions. As a result, digital-first shoppers now contextualize in-store visits as verification stages rather than the primary discovery channel, intensifying the need for omnichannel inventory synchronization.

Rising Disposable Income and Consumer Spending Power

Household earnings continue to climb in large emerging markets, lifting first-time purchases of entry-level refrigerators, washers, and microwaves. India’s growing urban middle class, supported by income-tax rebates and affordable-housing incentives, underpins double-digit volume growth for mid-range washing machines and refrigerators, while premium categories perform best in megacities such as Mumbai and Bengaluru. In the United States, sustained wage gains help offset inflation pressure, sustaining remodel activity and demand for high-capacity laundry pairs and French-door refrigerators.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity and freight-cost volatility compressing margins | -0.8% | Global with heightened pressure on import-dependent regions | Short term (≤2 years) |

| High initial costs of smart and energy-efficient appliances | -0.6% | Price-sensitive emerging markets and lower-income segments | Medium term (~3-4 years) |

| Chip-set supply bottlenecks are disrupting production | -0.4% | Global with concentrated impact on smart-appliance hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Commodity and Freight-Cost Volatility Compressing Margins

Tariff shifts and freight capacity mismatches raise landed costs for steel, aluminum, and electronic sub-assemblies used across the home appliances market. The World Bank notes a 4% year-on-year dip in broad commodity prices, yet spot freight rates on key Asia–North America lanes remain volatile due to vessel re-routing and port congestion. OEMs deploy multi-sourcing and regionalization strategies to hedge exposure, but smaller brands lack the volume leverage to secure long-term contracts. Currency fluctuations exacerbate procurement swings for Latin American and African importers, making retail pricing unpredictable and pressuring channel inventories.

High Initial Costs of Smart and Energy-Efficient Appliances

High upfront prices are a major barrier to choosing smart, energy-efficient appliances. Although these models cut energy bills over their lifetime—an advantage where electricity costs run high—they often cost two to four times more than standard alternatives. That price gap puts them beyond the reach of most households in Latin America, Southeast Asia, and parts of Africa. Without subsidies, rebates, or green-financing options, adoption remains limited to wealthier buyers in advanced economies. Although the U.S. Inflation Reduction Act provides credits up to USD 840 for specific appliance classes, awareness remains low among renters and first-time buyers. In developing economies, upfront cost sensitivity steers shoppers toward basic models, extending payback horizons and slowing penetration of connected or high-efficiency versions.

Segment Analysis

By Product: Air Fryers Ignite Small Appliance Revolution

Strong fundamentals keep refrigerators in the top position, representing 23% of the home appliances market size in 2024. Ongoing inverter-compressor upgrades, low-GWP refrigerant transitions, and expanded matte-glass finish options refresh demand cycles. At the opposite end, small appliances led by air fryers record the fastest expansion, with an 8.2% CAGR to 2030. Major brands introduce dual-drawer formats enabling simultaneous cooking of proteins and sides, while ceramic-coated baskets address durability concerns. This momentum elevates OEM bargaining power with upstream component suppliers, fostering investments in rapid-cycle heating elements and smart-thermostat integration.

Washing-machine innovation centers on AI-driven load sensing and auto-detergent dosing that can cut water use by 20%. Dishwasher redesigns follow energy-standard convergence, triggering the adoption of variable-speed circulation pumps and low-temperature detergents. Air-conditioner launches pivot toward R32 and R454b refrigerants paired with Wi-Fi modules for grid-interactive demand response. The cumulative effect across categories broadens the addressable installed base for aftermarket filters, descaling solutions, and subscription consumables, reinforcing recurring-revenue frameworks that firms now embed in business plans.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Multi-Brand Dominance Challenged by Digital Shift

Multi-brand stores continue to attract 39% of global consumer spend thanks to experiential showrooms where shoppers test refrigerator door swing clearance or washer spin-cycle noise. Retailers invest in in-store pickup lockers and same-day delivery to align with e-commerce expectations, while staff training emphasizes cross-selling of water-filters, extended warranties, and installation. Online sales grow at a 6.7% CAGR, lifting the home appliances market to fresh segments in rural zones underserved by physical outlets.

Exclusive brand boutiques expand in premium urban districts, leveraging color-matched accessories and on-site repair centers to drive loyalty. Warehouse clubs win on price leadership for core SKUs and bundle rebates. Direct-to-consumer websites accelerate growth as manufacturers seek data ownership, allowing AI chatbots to recommend filter replacements or software updates based on usage telemetry. The converging channel landscape rewards real-time inventory orchestration, click-to-delivery lead-time transparency, and harmonized returns processes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific holds 46% of global revenue, strengthened by China’s export of 4.48 billion appliances in 2024 and the Belt and Road Initiative that lowers tariff barriers for regional partners. Local champions such as Haier accelerate premiumization, launching glass-door refrigerators and AI washers tailored to niche lifestyle aspirations. Rising urbanization in Indonesia and Vietnam boosts basic large-capacity refrigeration penetration, while Japanese consumers gravitate toward high-end combo ovens with steam and convection modes.

North America remains the second-largest contributor, buoyed by stable housing starts and generous federal tax incentives for high-efficiency appliances. U.S. retailers report robust sales of Wi-Fi-enabled laundry pairs that integrate with energy-utility demand-response programs. Canada mirrors the shift but at a slower cadence due to colder-climate heating requirements, pushing integrated heat-pump dryer adoption into early mainstream phases.

Europe experiences mixed trends: Southern markets see replacement activity as energy bills spike, driving adoption of heat-pump dryers, whereas Northern markets push connected dishwashers to align with local smart-grid initiatives. Meanwhile, the Middle East and Africa region is set for 6.1% CAGR, propelled by rapid household formation, rising incomes in Gulf states, and government electrification drives that widen addressable off-grid appliance segments through solar-ready refrigerators. Latin America exhibits renewed momentum after macroeconomic stabilization in Brazil and Mexico, with government trade-in schemes lifting demand for A+++ rated products.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five participants—Samsung, LG, Whirlpool, Haier, and Midea Group—collectively address every major price band, technology platform, and geography in the home appliances market. Samsung leverages proprietary AI chips and voice assistants to lock in ecosystem stickiness, while LG’s partnership with Microsoft embeds Copilot agents directly into ThinQ-enabled appliances, accelerating feature deployment. Whirlpool’s carved-out European joint venture, Beko Europe, deepens specialization in energy-efficient front loaders, giving the group flexibility to re-allocate capital to North America.

Chinese contenders Hisense and Midea scale aggressively via original brand manufacturing, focusing on side-by-side refrigerators and inverter mini-split air conditioners. Cross-border merger and acquisitions intensifies: Rheem’s USD 1.6 billion acquisition of Fujitsu’s HVAC arm signals a broader convergence between appliance and climate-control portfolios. Component collaboration rises, exemplified by Panasonic’s engagement with Anthropic to build voice-first cooking guidance that iterates through cloud updates.

SharkNinja stands out in the small-appliance segment, growing 14.7% in Q1 2025 through rapid cadence releases of multicookers and robot vacuums. Furthermore sustainability differentiators such as recycled-plastic cabinet panels and carbon-neutral factory certification feature prominently in brand messaging, reflecting stricter EU supply-chain disclosure rules and retailer scorecard demands.

Home Appliances Industry Leaders

-

Whirlpool Corporation

-

Haier Group Corporation

-

LG Electronics, Inc.

-

Samsung Electronics Co., Ltd

-

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Samsung unveiled its Bespoke AI Home Appliances range, highlighted by a 400 W cordless vacuum and upgraded Family Hub refrigerators.

- February 2025: Sharp introduced the Celerity High-Speed Oven, cooking whole chicken three times faster through rapid radiant and convection technology.

- February 2025: Midea America launched the 50/50 Flex 3-Way Convertible Freezer with an extended two-year warranty.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global home appliances market as all newly manufactured electrical or gas-powered equipment used for domestic tasks such as food preservation, cooking, laundry care, room comfort, and cleaning, covering refrigerators, freezers, washing machines, dishwashers, ovens, air conditioners, vacuum cleaners, coffee makers, and similar countertop devices.

Scope exclusion: audio-visual consumer electronics (televisions, set-top boxes, smart speakers) fall outside this assessment.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances (range hoods, cooktops, etc.)

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills and Roasters

- Electric Kettles

- Juicers and Blenders

- Air Fryers

- Vacuum Cleaners

- Other Small Home Appliances (waffle makers, toasters, tea makers, rice cookers, etc.)

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance OEM managers, regional distributors, big-box retail buyers, and after-sales service providers across Asia-Pacific, North America, Europe, and the Middle East to cross-check shipment volumes, price moves, and technology-adoption assumptions.

Desk Research

We began with public macro datasets anchoring demand fundamentals; for example, World Bank household income tables, United Nations urbanization bulletins, and Eurostat dwelling completions. Trade-level inputs came from customs shipment codes, AHAM production releases, and ENERGY STAR efficiency registries. Company 10-Ks, investor decks, and press releases guided average selling price and channel-mix estimates. Select proprietary platforms, including D&B Hoovers and Dow Jones Factiva, supplied firm-level financials and news. The sources listed illustrate our approach, and many additional references supported data collection, validation, and research clarification.

Market-Sizing & Forecasting

A top-down consumption model links household formation, appliance-penetration rates, and replacement cycles. Then, results are sense-checked through sampled bottom-up roll-ups of manufacturer shipments and retail sell-through data. Key variables include new housing starts, electricity-tariff trends, disposable income per capita, e-commerce share of durables, regulatory energy-rating thresholds, and average product lifespans. Multivariate regression produces the forecast, and scenario analysis captures commodity-cost swings. When bottom-up evidence is thin, region-specific ASP benchmarks derived from primary calls bridge the gaps.

Data Validation & Update Cycle

Outputs run through variance filters, peer review, and senior sign-off. We refresh the dataset annually, while any material event such as tariff shifts or major plant closures triggers a rapid revision before release, ensuring clients always receive our latest view.

Why Mordor's Home Appliances Baseline Commands Reliability

Published numbers often diverge because firms blend smart entertainment devices with white goods, apply divergent ASP ladders, or freeze exchange rates at outdated levels.

The most visible gap drivers we observe are broader product scope, optimistic replacement-cycle assumptions, and infrequent model refreshes that some publishers follow.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 534.70 B (2025) | Mordor Intelligence | |

| USD 755.72 B (2025) | Global Consultancy A | Counts audio-visual electronics and uses retail sales values |

| USD 523.60 B (2025) | Trade Journal B | Limited store panel and undercounts online channels |

| USD 687.74 B (2025) | Research Publisher C | Uniform ASP uplift and five-year refresh cadence |

This comparison shows that Mordor's disciplined scope selection, annual refresh, and dual-path modeling give decision makers a balanced, transparent baseline they can confidently build upon.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Home Appliances Market?

The Home Appliances Market size is expected to reach USD 561.63 billion in 2025 and grow at a CAGR of 4.90% to reach USD 713.40 billion by 2030.

What is the current Home Appliances Market size?

In 2025, the Home Appliances Market size is expected to reach USD 561.63 billion.

What is the current size of the home appliances market?

The home appliances market stands at USD 534.70 billion in 2025 and is projected to reach USD 675.31 billion by 2030.

Which region leads the home appliances market?

Asia-Pacific holds the largest regional position, accounting for 46% of global revenue in 2024, supported by high export volumes and rising middle-class consumption.

Which product category is growing fastest?

Air fryers headline the small-appliance category and are expected to post an 8.2% CAGR through 2030, the fastest among tracked products.

How are energy-efficiency regulations affecting sales?

Stricter standards in the United States, Canada, and the EU shorten replacement cycles and boost demand for heat-pump water heaters, high-efficiency refrigerators, and inverter washers.

What role does e-commerce play in appliance sales?

Online channels already account for close to one-third of home-improvement appliance revenue worldwide and are forecast to grow at a 6.7% CAGR as virtual showrooms and rapid delivery improve customer experience.

Who are the key players in the market?

Samsung, LG, Whirlpool, Haier, and Midea group dominate global share, while challengers such as Hisense, Bosch-Siemens Hausgeräte, and SharkNinja expand rapidly through innovation and targeted acquisitions.

Page last updated on: