Market Overview

| Study Period | 2017 - 2030 |

|---|---|

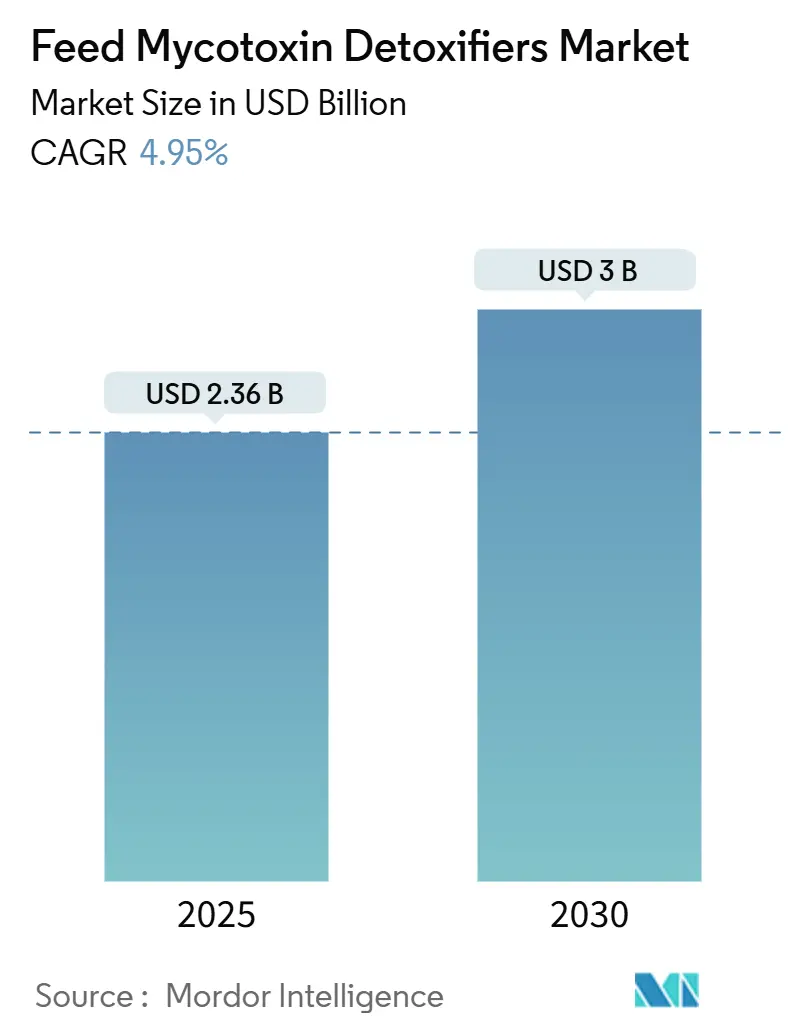

| Market Size (2025) | USD 2.36 Billion |

| Market Size (2030) | USD 3 Billion |

| Growth Rate (2025 - 2030) | 4.95% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Feed Mycotoxin Detoxifiers Market Analysis by Mordor Intelligence

The feed mycotoxin detoxifier market size stood at USD 2.36 billion in 2025 and is forecast to reach USD 3.0 billion by 2030, translating into an 4.95% CAGR over the period. Tightening maximum-limit regulations in the European Union and China, mounting evidence of climate-driven shifts in fungal contamination zones, and rapid expansion of industrial feed capacity in Asia-Pacific together underpin this strong growth momentum. Feed manufacturers are prioritizing broad-spectrum detoxification programs because co-occurrence of up to eight regulated toxins in single grain lots has become common in Serbia, Ethiopia, and other high-risk regions. Commercial mills are embedding automated mycotoxin testing and dosing infrastructure at the design stage, which reduces treatment costs and secures compliance with export-market standards. Competitive intensity is rising as enzyme-based biotransformers gain share by permanently degrading toxins rather than merely binding them, while premium pricing and regulatory gray areas in the Americas continue to temper adoption.

Key Report Takeaways

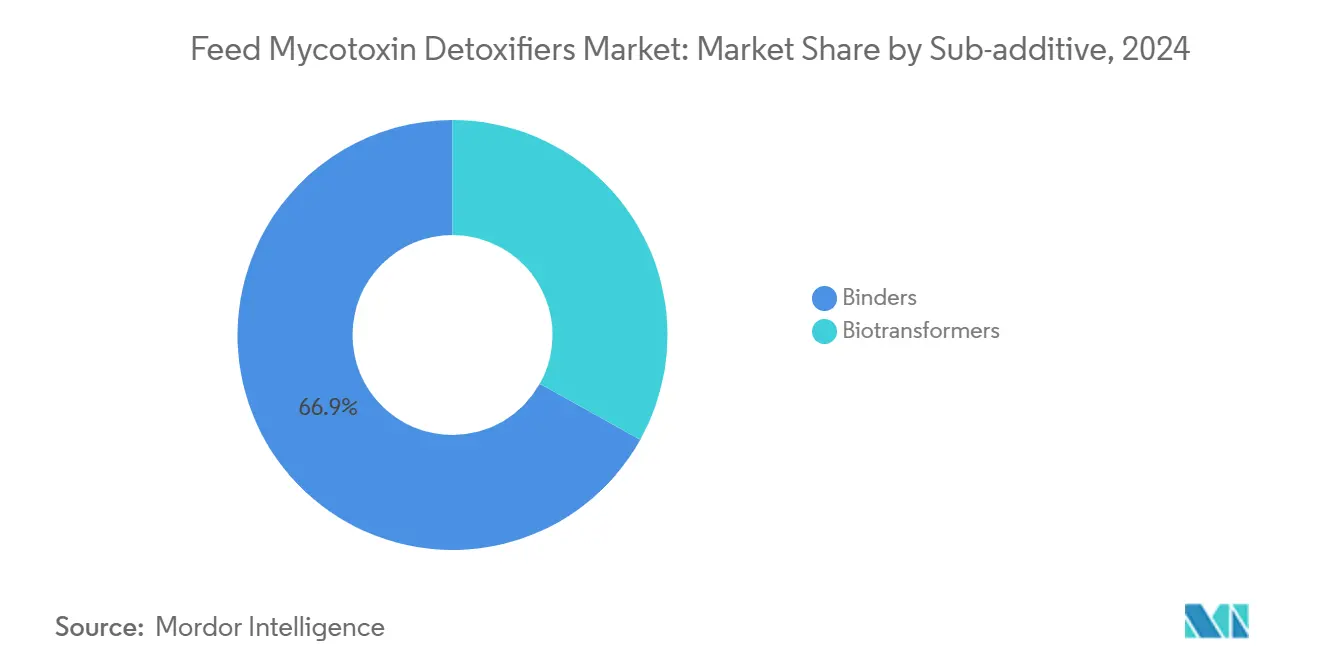

- By sub-additive, binders captured 66.94% of the feed mycotoxin detoxifier market share in 2024, whereas biotransformers are advancing at a 4.95% CAGR through 2030, making them the fastest-growing segment.

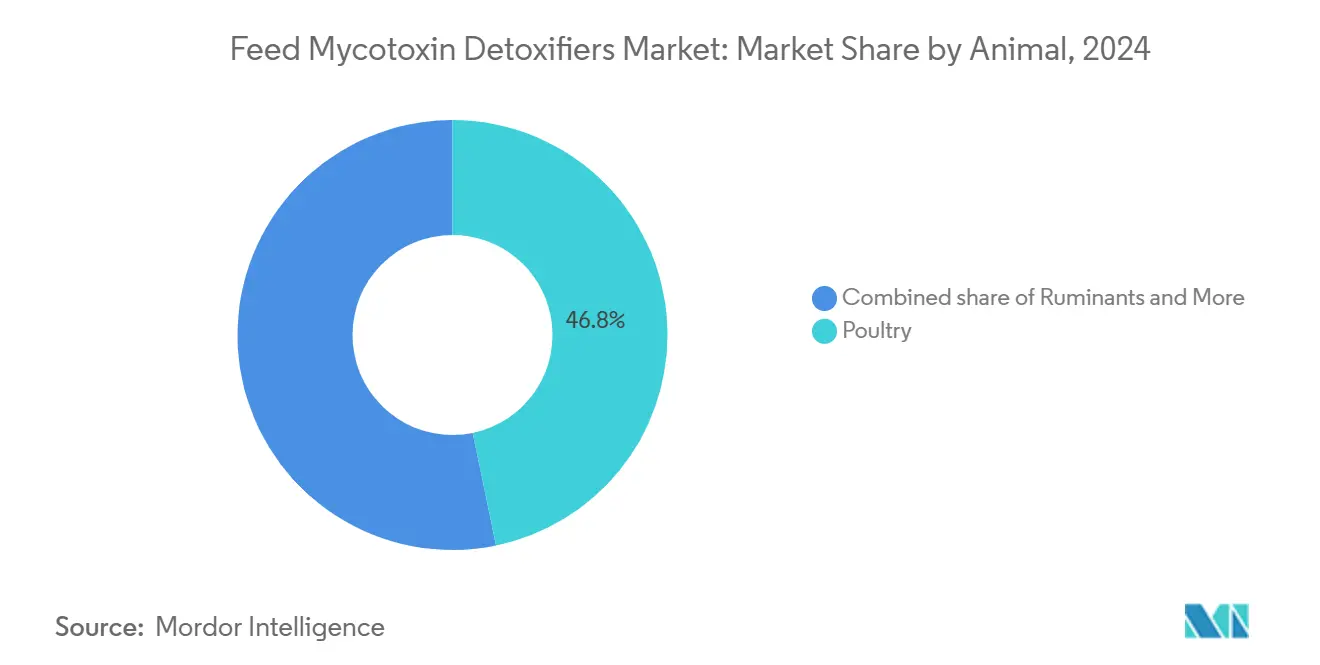

- By animal, poultry led with 46.75% of the feed mucotoxin detoxifier market size in 2024, and is projected to expand at a 5.23% CAGR to 2030, the highest among all livestock categories.

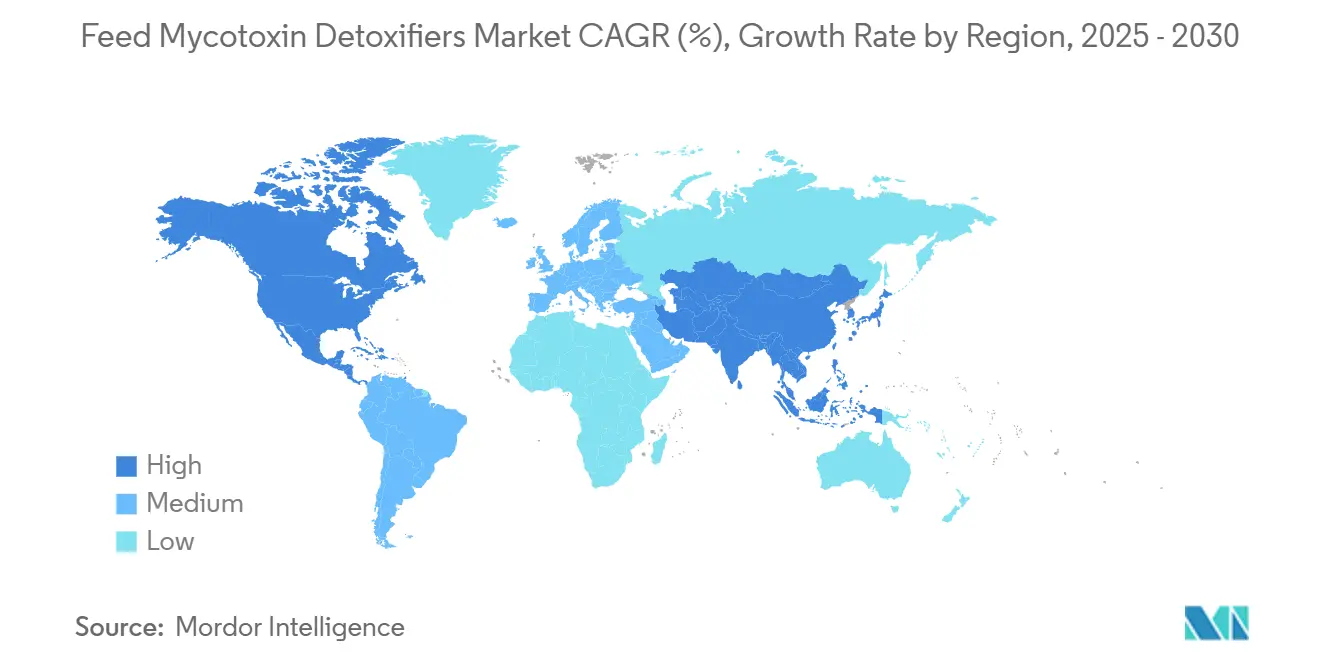

- In 2024, Asia-Pacific dominated the feed mycotoxin detoxifier market, capturing 31.15% of the market share. Meanwhile, North America is projected to experience the swiftest growth, with a forecasted CAGR of 4.65% extending through 2030.

Global Feed Mycotoxin Detoxifiers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of mycotoxin contamination in corn and oil-seed meal streams | +1.8% | Global, highest in Asia-Pacific and Africa | Medium term (2-4 years) |

| Stricter maximum-limit regulations in the EU, China, and Southeast Asia | +1.5% | Europe and Asia-Pacific core | Short term (≤ 2 years) |

| Expansion of commercial compound-feed production capacity | +1.2% | Asia-Pacific core, significant in South America | Medium term (2-4 years) |

| Intensifying protein demand from poultry and aquaculture sectors | +1.0% | Global, early gains in Asia-Pacific and South America | Long term (≥ 4 years) |

| Biotransformer adoption boosted by antibiotic growth-promoter phase-outs | +0.8% | Asia-Pacific and Europe core | Medium term (2-4 years) |

| Climate-change-driven shift in Fusarium and Aspergillus geographic range | +0.7% | Global, highest in Northern Europe and tropical Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Mycotoxin Contamination in Corn and Oil-Seed Meal Streams

Global surveys show fumonisin detection in 89-100% of Serbian maize samples and aflatoxin B1 concentrations as high as 527 µg/kg in drought years, breaching the European Union food limit by more than 100-fold. Ethiopian dairy concentrates posted 80.6% Aspergillus contamination, and 81.42% of isolates produced aflatoxins, highlighting the magnitude of the challenge. China loses 6 million tons of grain annually to mycotoxin degradation, amplifying the economic case for treatment. As climate volatility raises toxin peaks, mills are shifting from single-toxin binders to broad-spectrum solutions. The trend cements routine detoxifier use in high-risk supply chains now viewed as an operational necessity rather than an optional insurance policy.

Stricter Maximum-Limit Regulations in the EU, China and Southeast Asia

Regulatory bodies updated DON thresholds in 2022, forcing rapid reformulation across European and Chinese feed channels. Vietnam’s Circular 61 and Thailand’s new feed code mirrored these measures, widening the compliance net. Export-oriented mills must follow the strictest destination rule, effectively globalizing EU-level constraints. Faster enforcement cycles, often within 18 months, push buyers toward tested detoxifiers instead of incremental solutions. The same rulebooks set specific data requirements for enzyme-based products, favoring suppliers with complete dossiers and deterring late entrants.

Expansion of Commercial Compound-Feed Production Capacity

New mega-mills in Vietnam and Brazil integrate on-line mycotoxin monitoring and precision dosing systems from day one, processing more than 10 million tons per year. Scale purchasing cuts treatment cost per ton below historic thresholds, encouraging full-year programs rather than seasonal interventions. Automation improves dosage accuracy and data capture, reinforcing evidence-based decisions for continuous improvement. Concentration of capacity in humid climates keeps toxin pressure high, ensuring steady demand for detoxification inputs.

Climate-Change-Driven Shift in Fusarium and Aspergillus Geographic Range

Northern Europe has recorded Fusarium levels historically confined to temperate central zones, while tropical Africa experiences an overlap of Aspergillus and emerging Fusarium species. Predictive analytics allow mills to raise detoxifier doses ahead of forecasted risk peaks, preserving animal performance. As seasons become unpredictable, year-round preventive protocols replace the traditional harvest-only approach, supporting continuous demand.[2]Source: CABI Agriculture and Bioscience, “Shelf Life of Aflatoxin Biocontrol Products,” cabiagbio.biomedcentral.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus traditional binders for cost-sensitive farmers | -1.2% | Global, highest in Africa and South Asia | Short term (≤ 2 years) |

| Low awareness among small and backyard livestock producers | -0.8% | Africa and South Asia core | Medium term (2-4 years) |

| Efficacy variability across multi-toxin challenges | -0.6% | Global, high-contamination regions | Medium term (2-4 years) |

| Regulatory gray area for enzyme-based biotransformers in the Americas | -0.4% | Americas core | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing versus Traditional Binders for Cost-Sensitive Farmers

Multi-component products add USD 15–30 per ton to feed costs, while basic clay binders cost only USD 2–5 per ton. The differential strains budgets of smallholders in Sub-Saharan Africa and South Asia, where feed already absorbs more than 70% of production costs. Returns manifest chiefly as avoided losses, a concept that is difficult to quantify for low-margin enterprises. Suppliers are experimenting with seasonal pricing and pay-as-you-benefit models to lower entry hurdles. Packaging detoxifiers into concentrate premixes also spreads incremental cost across multiple nutrients, enhancing acceptance.

Low Awareness Among Small and Backyard Livestock Producers

Surveys in Ethiopia and Bangladesh show that fewer than 30% of smallholders can identify mycotoxin symptoms. Extension agents rarely hold specialized training, limiting outreach of accurate guidance. Informal feed channels dominate these regions, reducing traceability and disincentivizing investments in quality control. Demonstration farms and peer-to-peer learning hubs are being rolled out to showcase tangible benefits and accelerate word-of-mouth adoption. [3]Source: IFPRI, “Livestock Feed Safety in Developing Countries,” ifpri.org

Segment Analysis

By Sub-Additive: Biotransformers Drive Innovation Despite Binder Dominance

Binders accounted for 66.9% of feed mycotoxin detoxifier market share in 2024, while the biotransformers are projected to deliver a 4.96% CAGR through 2030. Binders are led by low-cost bentonite and montmorillonite clays validated over decades of commercial use. The segment benefits from simple registration pathways and abundant raw material supply. Binders are particularly favored for their ability to trap toxins in the animal's gastrointestinal tract, forming a binder-mycotoxin complex that is safely excreted. Their lower cost compared to other detoxifier types and easier usage patterns have also contributed significantly to their market dominance, especially in monogastric animals, where they are predominantly used.

Nevertheless, biotransformers witness the steepest trajectory among sub-additives. These are gaining particular traction in regions with advanced agricultural practices, where farmers are increasingly recognizing their role in improving animal health outcomes and feed efficiency. The segment's growth is also bolstered by rising concerns about feed safety and the increasing demand for innovative solutions in mycotoxin management. The feed mycotoxin binders and modifiers market is anticipated to see significant advancements in this area.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Animal: Poultry Expansion Reshapes Demand Patterns

Poultry feeds generated 46.8% of 2024 revenue, and are growing at a 5.23% CAGR, cementing their role as the largest application, yet growth is stabilizing near overall market averages. This substantial market presence is primarily attributed to the growing population and increasing consumer demand for poultry products worldwide. The Asia-Pacific region, particularly countries like China and India, significantly contributes to this segment's market share due to their large-scale commercial poultry operations and increasing focus on feed quality and safety measures.

Aquaculture also witnessed robust growth, which is primarily driven by the increasing awareness of mycotoxin contamination risks in aquafeed and the growing importance of feed safety in aquaculture production. Swine producers exhibit moderate uptake, and tolerance thresholds are higher than poultry yet lower than cattle, prompting targeted rather than blanket coverage. Ruminants traditionally relied on microbial detoxification in the rumen, but intensively managed dairy operations now supplement binders to curb aflatoxin M1 in milk, securing export-grade safety standards.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific held the largest share of 31.1% of the feed mycotoxin detoxifier market in 2024, fueled by rapid industrial feed expansion and hot-humid climates conducive to fungal growth. New Vietnamese mills with 10 million-ton annual capacity embed automated toxin screening that triggers real-time dosing. China’s farmer-held stockpile of 250 million tons incurs 8% storage losses, equivalent to 6 million tons of contaminated grain that require remediation annually.

The North American region is the fastest-growing region with a CAGR of 4.65% as the feed mycotoxin detoxifiers market demonstrates high technological adoption and a sophisticated understanding of feed safety across the United States, Canada, and Mexico. In Africa, surveys in Ethiopian dairy rations exposing 80.6% Aspergillus incidence confirm a chronic risk that undermines livestock gains from genetic and nutritional improvements. [1]Source: Frontiers in Sustainable Food Systems, “Aspergillus Species Contamination in Concentrate Feeds,” frontiersin.orgClimate modeling shows dual Fusarium and Aspergillus pressure expanding westward, reinforcing the need for continuous toxin management programs.

Europe shows stable growth, driven by tougher DON limits enacted in 2022. Northern growers now combat Fusarium levels once restricted to warmer latitudes. Brazil’s heavy mill investments and lessons from past shipment rejections linked to aflatoxin contamination. Government extension programs in Brazil and Argentina now include mycotoxin management modules, elevating baseline awareness and supporting detoxifier uptake.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market is moderately consolidated, with the top five suppliers commanding a 26.6% share, with Cargill Inc. and Adisseo leading the market. Legacy clay binder portfolios give these multinationals an installed base, yet enzyme innovators such as DSM-Firmenich are eroding incumbent dominance through biotransformer differentiation. Patent filings on heat-stable enzymes and multi-component delivery matrices have climbed sharply since 2023. Strategic acquisitions like Innovad’s purchase of Oligo Basics extend geographic reach and local manufacturing capacity, improving cost competitiveness in price-sensitive markets.

Global distributors such as Brenntag provide market access for mid-tier specialists, but proprietary technical support remains a key differentiator at scale. Combination products blending adsorbent clays with degradative enzymes are attracting joint venture interest, pooling formulation know-how with supply-chain muscle. The regulatory environment rewards firms with comprehensive safety dossiers, accelerating returns for early movers while creating entry barriers for latecomers.

New entrants and smaller players are carving out market share by honing in on niche segments and crafting specialized products tailored to specific animal species or regional needs. Key to their success are forging robust local partnerships, investing in technical know-how, and adopting competitive pricing strategies. These companies proactively navigate potential regulatory shifts and environmental concerns, all while catering to the rising demand for natural and sustainable solutions. Furthermore, the launch of products such as Cargill's toxin binder underscores the industry's dedication to tackling these challenges through innovative solutions.

Feed Mycotoxin Detoxifiers Industry Leaders

-

Adisseo

-

Alltech, Inc.

-

BASF SE

-

Brenntag SE

-

Cargill Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Cargill introduced its new Notox brand of advanced mycotoxin management tools which leverages cutting-edge technology for superior binding efficiency. The company is emphasizing a data-driven approach, utilizing its extensive mycotoxin database to track global contamination risks in real-time and provide customers with risk assessment tools like the Mycotoxin Impact Calculator (MIC).

- October 2025: Alltech launched its next-generation Mycosorb Evo range of mycotoxin binders, designed for enhanced efficacy against a wider spectrum of mycotoxins, including DON, fusaric acid, and Penicillium-derived toxins.

- September 2024: CABI (Centre for Agriculture and Bioscience International) research validated the industrial feasibility of their Aflasafe biocontrol products, confirming a four-year shelf stability that is resilient to variations in storage temperature and packaging material.

Global Feed Mycotoxin Detoxifiers Market Report Scope

Sub Additive

| Binders |

| Biotransformers |

Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

Region

| Africa | By Country | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | By Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | Iran |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | Argentina |

| Brazil | ||

| Chile | ||

| Rest of South America |

| Sub Additive | Binders | ||

| Biotransformers | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Region | Africa | By Country | Egypt |

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

| Asia-Pacific | By Country | Australia | |

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Philippines | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Country | France | |

| Germany | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| Turkey | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Country | Iran | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| North America | By Country | Canada | |

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Country | Argentina | |

| Brazil | |||

| Chile | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF