Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.68 Billion |

| Market Size (2031) | USD 40.33 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

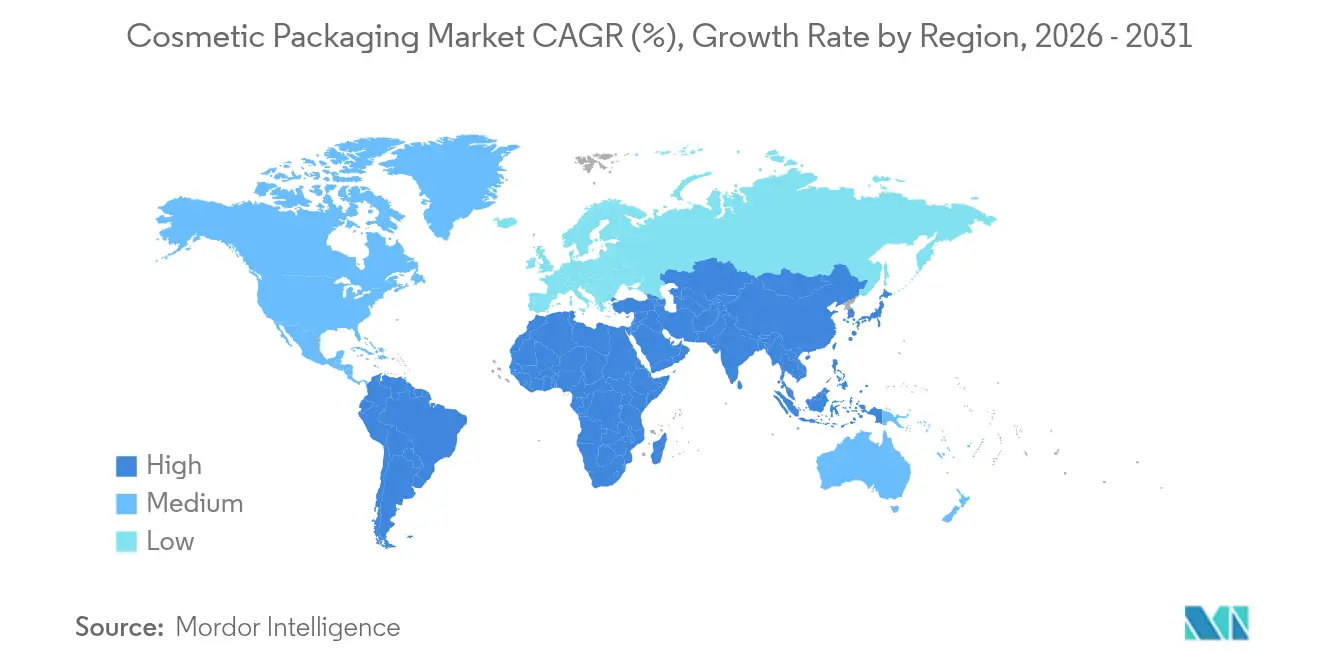

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

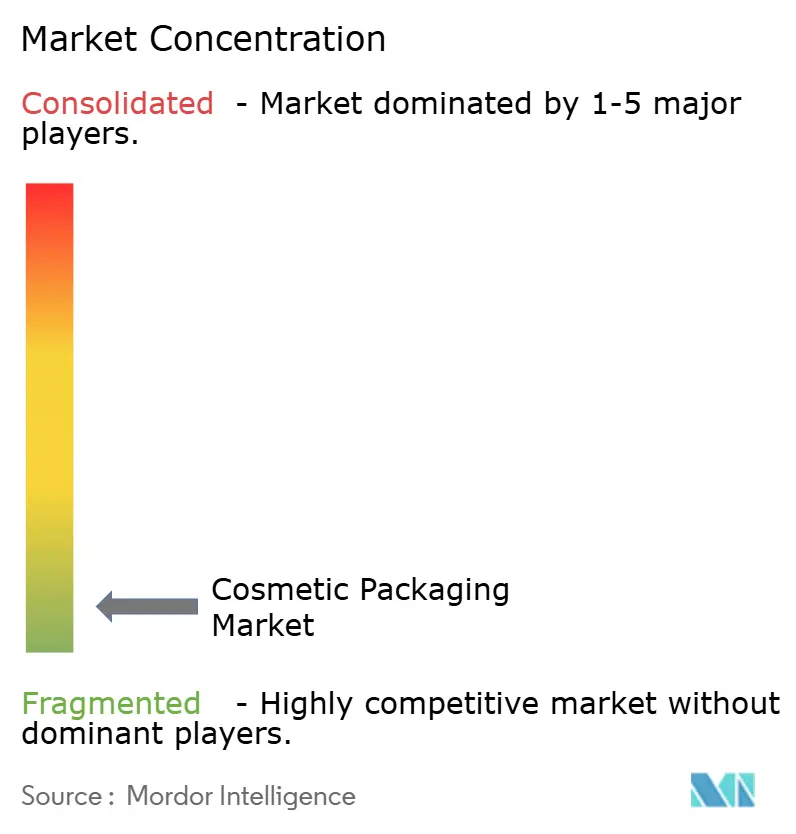

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic Packaging Market Analysis by Mordor Intelligence

The cosmetic packaging market was valued at USD 30.19 billion in 2025 and estimated to grow from USD 31.68 billion in 2026 to reach USD 40.33 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031). The advance mirrors brand responses to the European Union’s Packaging and Packaging Waste Regulation, effective February 2025, which obliges recyclability and extended producer responsibility compliance[1]Source: European Parliament, “Packaging and packaging waste,” europarl.europa.eu . Brands counter rising polyethylene terephthalate costs driven by geopolitical tension and production cuts in China and Europe by accelerating recycled-content usage and lightweight designs. Asia-Pacific remains the growth engine, propelled by sophisticated consumer routines and strong e-commerce logistics; Chinese facial sheet-mask success and premiumization across South Korea and Japan typify the region’s influence. Material choice continues to bifurcate: plastics retain cost leadership while glass advances on luxury, refillable, and circular-economy appeal. Meanwhile, corporate consolidation highlighted by Amcor’s USD 8.43 billion merger with Berry Global bundles scale and R&D to quicken sustainable-packaging rollouts.

Key Report Takeaways

- By material type, plastics commanded 64.02% of the cosmetic packaging market share in 2025.

- By product type, the cosmetic packaging market size for flexible sachets and pouches records the fastest 7.41% CAGR between 2026-2031.

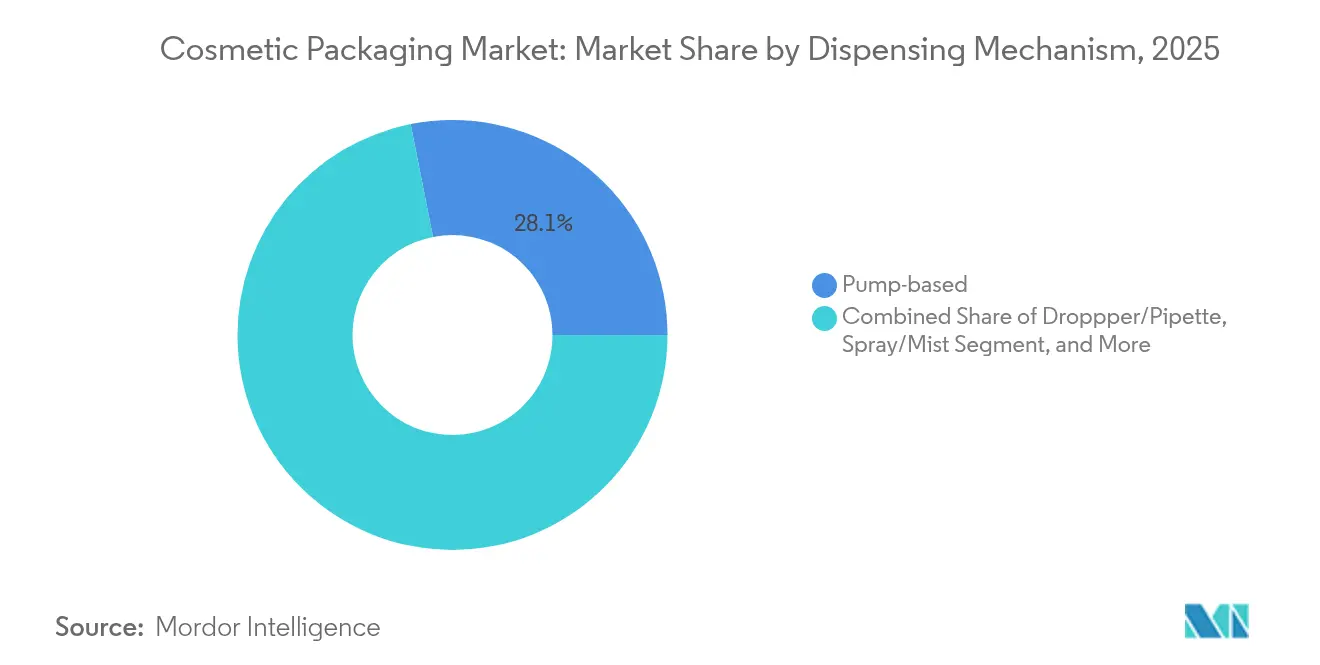

- By dispensing mechanism, pump systems held 28.12% share of the cosmetic packaging market size in 2025.

- By cosmetic type, the cosmetic packaging market size for color cosmetics records the fastest 6.31% CAGR between 2026-2031.

- By geography, Asia-Pacific led with 42.55% share of the cosmetic packaging market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cosmetic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumption of premium and masstige beauty products | +1.2% | Asia-Pacific and North America | Medium term (2-4 years) |

| Shift toward e-commerce-friendly lightweight formats | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Rise of refillable/reusable delivery systems | +0.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rapid adoption of robot-ready secondary packs | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Authentication-enabled smart packaging to curb counterfeits | +0.4% | Global, with priority in luxury markets | Medium term (2-4 years) |

| Brand demand for carbon-label-ready packs | +0.3% | Europe primary, North America secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumption of Premium and Masstige Beauty Products

Luxury cues have migrated into mainstream channels as tactile finishes, heavy-wall glass, and ornate closures shape brand storytelling. L’Oréal’s 2025 World Refill Day push lifted refillable options seventeen-fold in five years without diluting premium positioning. Estée Lauder already supplies 71% of its portfolio in sustainable formats, confirming that environmental progress and upscale image can co-exist. Suppliers thus prioritise high-clarity glass and mono-material pumps that tolerate prestige formulations. The opportunity extends to refill kits that guarantee adjacency sales and invite higher margins. Luxury's embrace of environmental performance raises the bar for all tiers of the cosmetic packaging market.

Shift Toward E-commerce-Friendly Lightweight Formats

Online sales make damage resistance and dimensional-weight savings decisive. Flexible pouches grow at 7.67% CAGR because they ship flat, cut void fill, and slash freight spend. KISS Cosmetics automated its 480,000 ft² facility with intelligent cart-picking and A-Frame dispensing, demonstrating fulfilment economics that favour uniform, lighter packs. Packaging-robot investments are projected to reach USD 7.5 billion by 2032, underlining automation’s role in smoothing multi-SKU flows. Brands that optimise for courier networks rather than retail shelves secure faster cycle times and lower emissions, fortifying the global cosmetic packaging market against logistics volatility.

Rise of Refillable/Reusable Delivery Systems in Prestige Channels

Circular designs are now profit levers rather than pilot programs. Chanel created Nevold in 2025 to build recycled-material supply at luxury specifications. Aptar’s full-plastic Advance pump, launched the same year, aligns engineering tolerances with recyclability and refill ease. Consumer surveys show 78% favor additional refills when convenience matches originals, pushing packaging suppliers to deliver intuitive docking mechanisms and tamper-evident seals. Because refill cartridges typically weigh one-third of primary packs, brands cut material intensity and freight costs while embedding loyalty through proprietary formats. This trend keeps the cosmetic packaging market in step with both climate targets and aspirational brand identities.

Rapid Adoption of Robot-Ready Secondary Packs in 3-PL Fulfilment

Third-party logistics hubs now expect cartons scalable to grippers and automated sortation. GEODIS runs 320 AutoStore robots achieving 250,000 daily picks, proving that throughput jumps when pack dimensions are standardised . Performance Health’s Packsize X5 machines improved productivity 97% by right-sizing corrugated boxes . Cosmetics brands therefore re-engineer secondary packs with defined pick faces, slip-resistant coatings, and QR codes to harmonise with mixed-SKU order profiles. Automation-ready design reduces labour cost, accelerates same-day promise, and future-proofs the cosmetic packaging market against wage inflation.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global recycled-resin price volatility | -0.9% | Europe and North America | Short term (≤ 2 years) |

| Regulatory caps on single-use plastics | -0.7% | Europe expanding to North America | Medium term (2-4 years) |

| Filling-line incompatibility of novel bio-materials | -0.4% | Global manufacturing locations | Medium term (2-4 years) |

| Shrinking landfill capacity driving extended-producer-responsibility fees | -0.6% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Recycled-Resin Price Volatility

European PET hovered at EUR 1,130–1,170 per t in 2024 as anti-dumping rules tightened supply, forcing converters into spot-market bidding wars. Polyethylene and polypropylene followed with five-cent and four-cent per-lb upticks in early 2025 as feedstock costs rose. Brands with 50%-recycled-content pledges thus absorb margin shocks or hedge via vertical integration, such as on-site washing plants. Because high-quality food-grade PCR commands premiums, availability risk constrains design freedom and may slow substitutions away from virgin resin in the cosmetic packaging market.

Regulatory Caps on Single-Use Plastic

The EU will bar several single-use cosmetic packages by January 2030, while California SB 54 orders a 25% reduction in virgin-plastic mass by 2032. France brings forward its non-recyclable ban to 2025, pushing reformulation of sample-sized sachets and travel minis. Each jurisdiction sets different baselines and reporting thresholds, complicating global harmonisation. Brands must therefore juggle SKU localisation, material migration, and compliance audits across the cosmetic packaging market. Those lacking modular design toolkits face accelerated obsolescence of existing moulds and artwork.

Segment Analysis

By Material Type: Glass Gains Despite Plastic Dominance

Plastics held a 64.02% cosmetic packaging market share in 2025 thanks to cost efficiency, clarity, and line-speed compatibility. Polyethylene terephthalate leads for personal-care bottles, polypropylene secures pump stems and closures, while low-density polyethylene shapes flexible tubes. Yet glass races ahead at 8.32% CAGR to 2031 because prestige brands crave heft, scratch resistance, and infinite recyclability. The premium shift lifts the cosmetic packaging market size for glass to meaningful double-digit revenue slices even as total pack count stays lower than plastic. Glass-recycling initiatives such as Estée Lauder’s work with Strategic Materials Inc.improve cullet quality and furnace yields, soothing environmental criticisms. Metallised aluminium and steel remain niche for fragrances and gifting editions where barrier performance and tactile coolness drive shelf impact. Fibre-based board escalates in transit shippers and gift sets, answering e-commerce cushioning needs without raising plastic tax exposure.

Second-generation materials blur lines between categories. Multi-layer PET-aluminium laminates once seen in tubes migrate toward mono-material EVOH-barrier PET that retains recycling stream compatibility. Bio-sourced resins such as polylactic acid win trial runs for limited-edition labels but still battle heat resistance and filling-line friction, limiting scale. Suppliers addressing these hurdles gain early-mover contracts, reflecting how sustainability performance now shapes vendor selection criteria across the cosmetic packaging market. Meanwhile, returnable glass programs aligned with refill stations exemplify how premium credentials fuse with low-impact ambitions to pull glass farther into mainstream assortments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Flexible Formats Challenge Rigid Dominance

Bottles and jars delivered 44.12% revenue in 2025, supported by high filling speeds and shopper familiarity. Wide-mouth jars continue to anchor face creams, while narrow-neck PET bottles dominate shampoos and micellar waters. However, sachets and stand-up pouches compound at a brisk 7.41% CAGR, cutting grams per dose and resisting breakage during courier drops. Right-size technology lets brands switch from one bottle-per-month to five flat sachets per envelope, lowering freight-emissions intensity. Tubes and sticks address on-the-go sunscreen, solid serum, and colour-balm trends, meshing with travel-size regulation and zero-leak expectations. Folding cartons remain favoured in luxury presentations, housing glass flacons or booster vials while conveying brand narratives through soft-touch varnish and foil embossing.

Transit boxes evolve too. Corrugated suppliers deploy algorithmic box-making to trim void fill, supported by Packsize machines that cut board in line with real-time order dimensions. Consumer unboxing gains differentiate omnichannel experiences, prompting QR-printed inserts that trigger digital loyalty rewards. Flexible-pack barrier coatings upgrade to silicon oxide or aluminium oxide, securing fragrance retention and reducing oxygen transmission without disqualifying recyclability. Such advances swell the cosmetic packaging market size credited to flexible formats and re-define mass-premium aesthetics away from solely rigid containers.

By Dispensing Mechanism: Convenience Drives Innovation

Pump systems owned 28.12% of the cosmetic packaging market in 2025, prized for controlled output and airless integrity. New mono-material pumps displace multi-substrate versions, easing end-of-life separation and aligning with PPWR guidelines. Airless PE cylinders shield light-sensitive retinol serums, whereas actuator redesign pares weight by up to 15%, helping brands meet carbon budgets. Stick and twist-up designs are the fastest-rising at 7.86% CAGR, buoyed by solid balm cleaning sticks and vegan foundation blocks. Their glide-up convenience and leak-proof travel rating answer urban mobility lifestyles. Droppers thrive in high-value ampoules where dosage precision underpins efficacy claims, and spray heads keep fragrance and face-mist SKUs relevant in habitual re-application rituals.

Touch-free applicators surface as post-pandemic hygiene norms persist, integrating silicone tips that wash easily. Aptar and Avene’s recyclable airless bottle collaboration shows how brand-supplier partnerships merge barrier science with eco design. Regional preference matters: Asian beauty routines value spatula-free jar lids that flip open one-handed, while North American consumers lean toward pumps to avoid contamination. Across mechanisms, ergonomic upgrades and end-of-life simplicity position dispensing innovation as a fundamental differentiator within the cosmetic packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cosmetic Type: Color Cosmetics Accelerates Growth

Skincare retained 45.01% revenue share in 2025, underpinned by multi-step regimens that spawn cleanser, toner, and essence SKUs, each demanding tailored packaging. Facial serums fetch premium price points, justifying heavy glass droppers or airless pumps with oxygen-scavenging liners. Body-care bottles stretch to family-size litre jugs with pump tops for shower efficiency. Color cosmetics, though smaller in absolute value, outrun most segments at 6.31% CAGR as social-media tutorials spark continuous product launches. Slim stick foundations, cushion compacts, and refillable blush pans fuse compact portability with style, feeding accelerated replacement cycles and enlarging the cosmetic packaging market size captured by make-up.

Hair-care packaging shifts toward professional-grade home treatments, using foil-lined stand-up pouches for mask concentrates that reduce plastic by 60% over tubs. Fragrance remains the design playground: Lumson’s 2025 collection of thirteen glass silhouettes showcases dual-injection colour gradients and tactile stoppers. Eco-concern nudges rollerball fragrance oils in recycled aluminium cylinders for easier curb-side recycling. Niche domains nail serums, brow laminators, hybrid sun-care sticks demand micro-batch moulds and rapid-prototyping partnerships, widening opportunity for agile converters. The widening palette of formulations secures continuous innovation stimulus for the cosmetic packaging market.

Geography Analysis

Asia-Pacific owned 42.55% of cosmetic packaging market revenue in 2025 and will grow at a 7.18% CAGR to 2031, lifted by rising disposable income, advanced K-beauty regimens, and high mobile-commerce penetration. Sheet-mask dominance in China illustrates local appetite for single-use but sophisticated pack forms, making the region a hotbed for minimalist yet functional pouches. Japan and South Korea export design cues globally, such as airless cushion compacts and slim twist balms, giving regional converters first-mover advantages.

North America holds firm value through premium skincare adoption and rapid e-commerce. Refill station pilots appear in beauty specialty retailers, rewarding glass cartridge suppliers with new service contracts. Automation readiness drives widespread acceptance of robot-friendly corrugate and linerless labels. State-level plastic-reduction bills add urgency to lightweight mono-material shifts, redirecting investment towards recycled-content PET and fibre substitution. These moves keep the cosmetic packaging market buoyant despite mature category penetration.

Europe shapes regulatory frameworks that ripple worldwide. Enforcement of the PPWR and escalating eco-contribution fees in France imposes clear packaging recyclability thresholds, accelerating investment in design for disassembly. Luxury fragrance clusters in France and Italy champion glass innovation, including advanced hot-end coating for scratch reduction. Meanwhile, Central and Eastern Europe attract bottle moulding capacity expansions to serve both local brands and export production. Collectively, global regions influence material strategies and technology transfer rates, interlocking demand drivers for the cosmetic packaging market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The cosmetic packaging market is fragmented; numerous niche experts coexist alongside multinational roll-ups. Amcor’s 2025 merger with Berry Global forged an extended platform across flexibles, closures, and healthcare, promising USD 650 million in synergies and USD 180 million annual R&D allocation[3]Source: Amcor, “Amcor completes combination with Berry Global,” amcor.com . The tie-up pushes peers to consider scale alignments or specialty tuck-ins to defend customer portfolios. AptarGroup leverages its 2024 TIME sustainability ranking to court prestige beauty leaders seeking verified low-carbon solutions..

Private equity’s appetite for glass assets stays strong: Movendo Capital and Draycott gained control of Verescence in February 2025 to support furnace decarbonisation and post-consumer cullet adoption. Luxury Cosmetic Solutions Investments’ Eurovetrocap acquisition highlights cross-portfolio synergies in droppers and minis that share pipette tooling. Technology capability, particularly in NFC tags, blockchain security, and carbon tracking, becomes a defensible moat. Start-ups offering AI-driven eco-design software or biopolymer additives attract licensing deals rather than outright acquisition, reflecting the incumbent's wish to add modular tech without diluting core EBITDA.

Regional specialists thrive by applying cultural insight Korean converters refine cushion-compact air pockets for humidity management, while Italian glass-press houses perfect flint clarity for colour-cosmetic bottles. The top five suppliers collectively control under 55% of global revenue, leaving room for mid-sized innovators. Competitive energy will likely escalate around refill infrastructure, PCR-feedstock verticals, and micro-fibre-based transit solutions, anchoring growth trajectories in the cosmetic packaging market.

Cosmetic Packaging Industry Leaders

Albea S.A.

Silgan Holdings Inc

Amcor Plc

International Paper

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: L’Oréal launched #JoinTheRefillMovement for World Refill Day to promote refillable packs across Lancôme and Kiehl’s.

- June 2025: Chanel unveiled Nevold, a unit dedicated to recycled-material innovation at luxury grade .

- April 2025: Aptar Beauty and Laboratoire SVR debuted recyclable airless bottles for dermo cosmetics.

- March 2025: CSI rebranded to Canopy Beauty Packaging, focusing on PCR-rich US-made jars and closures.

- January 2025: Aptar Beauty introduced Advance all-plastic pump collection.

Global Cosmetic Packaging Market Report Scope

A cosmetic substance is used to clean, enhance, or change the appearance of the face, body, hair, fingernails, or teeth. Cosmetic products include make-up, perfumes, skin creams, nail polish, and grooming products such as soap, shampoo, shaving creams, and deodorants. The study tracks the different types of packaging needed for cosmetic products to keep them from spoiling, moisture, UV, and more.

The cosmetic packaging market is segmented by material (plastic, glass, metal, and paper), product type (plastic bottles and containers, glass bottles and containers, metal containers, folding cartons, corrugated boxes, tubes and sticks, caps, and closures, pump and dispenser, droppers, ampoules, and flexible plastic packaging), cosmetic type (hair care, color cosmetics, skincare, men grooming, and deodorants), and geography (North America [the United States and Canada], Europe [the United Kingdom, Germany, France, Italy, Spain, and Rest of Europe], Asia-Pacific [China, India, Japan, South Korea, and Australia & New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [the United Arab Emirates, Saudi Arabia, South Africa, and Rest of MEA]). The market sizes and forecasts are provided in terms of revenue (USD) for all the above segments.

By Material Type

| Plastics | Polyethylene Terephthalate (PET) |

| polypropylene (PP) | |

| Polyethylene (PE) | |

| Other Plastics | |

| Glass | |

| Metal | |

| Paper and Paperboard |

By Product Type

| Bottles and Jars |

| Tubes and Sticks |

| Folding Cartons |

| Corrugated Transit Boxes |

| Flexible Sachets and Pouches |

| Other Product Type |

By Dispensing Mechanism

| Pump-based |

| Dropper / Pipette |

| Spray / Mist |

| Stick / Twist-up |

| Jar / Scoop |

By Cosmetic Type

| Skin Care | Facial Care |

| Body Care | |

| Hair Care | |

| Color Cosmetics | |

| Perfumes and Fragrances | |

| Other Cosmetics Type |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacifc | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastics | Polyethylene Terephthalate (PET) | |

| polypropylene (PP) | |||

| Polyethylene (PE) | |||

| Other Plastics | |||

| Glass | |||

| Metal | |||

| Paper and Paperboard | |||

| By Product Type | Bottles and Jars | ||

| Tubes and Sticks | |||

| Folding Cartons | |||

| Corrugated Transit Boxes | |||

| Flexible Sachets and Pouches | |||

| Other Product Type | |||

| By Dispensing Mechanism | Pump-based | ||

| Dropper / Pipette | |||

| Spray / Mist | |||

| Stick / Twist-up | |||

| Jar / Scoop | |||

| By Cosmetic Type | Skin Care | Facial Care | |

| Body Care | |||

| Hair Care | |||

| Color Cosmetics | |||

| Perfumes and Fragrances | |||

| Other Cosmetics Type | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacifc | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current cosmetic packaging market size and expected growth?

The cosmetic packaging market stands at USD 31.68 billion in 2026 and is projected to reach USD 40.33 billion by 2031 at a 4.95% CAGR.

Which region drives the fastest expansion in cosmetic packaging?

Asia-Pacific leads, commanding 42.55% of 2025 revenue and advancing at a 7.18% CAGR through 2031.

Why are refillable systems gaining ground?

Luxury brands such as Chanel and L’Oréal view refillable packaging as both a circular-economy obligation and a loyalty-building tool, while new pump and cartridge designs make refilling straightforward.

How are regulations shaping material choices?

The EU’s Packaging and Packaging Waste Regulation and state-level US plastic caps push brands toward recyclable mono-materials, higher PCR content, and lightweight formats.

Which dispensing mechanism shows the strongest growth?

Stick and twist-up formats grow at a 7.86% CAGR due to portability, solid-formula demand, and compliance with travel-size liquid restrictions.

How will automation influence future packaging design?

Standardised, robot-ready secondary packs enable higher fulfilment throughput and lower labour costs, making automated compatibility a core design specification.