Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

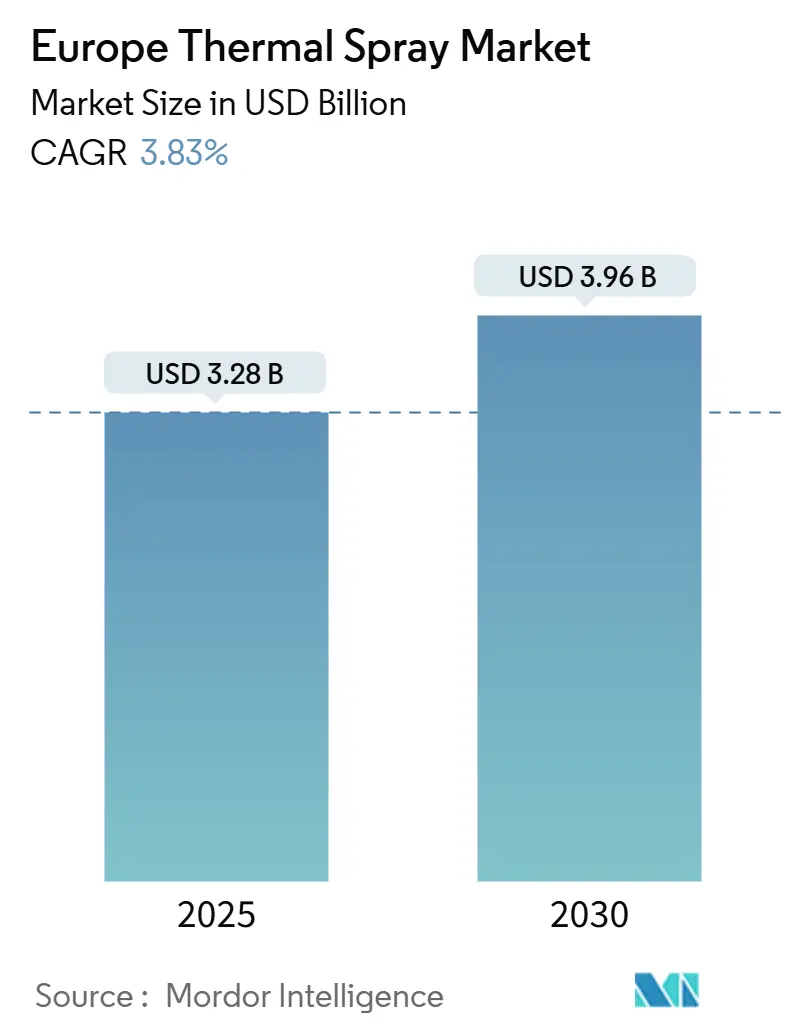

| Market Size (2025) | USD 3.28 Billion |

| Market Size (2030) | USD 3.96 Billion |

| Growth Rate (2025 - 2030) | 3.83% CAGR |

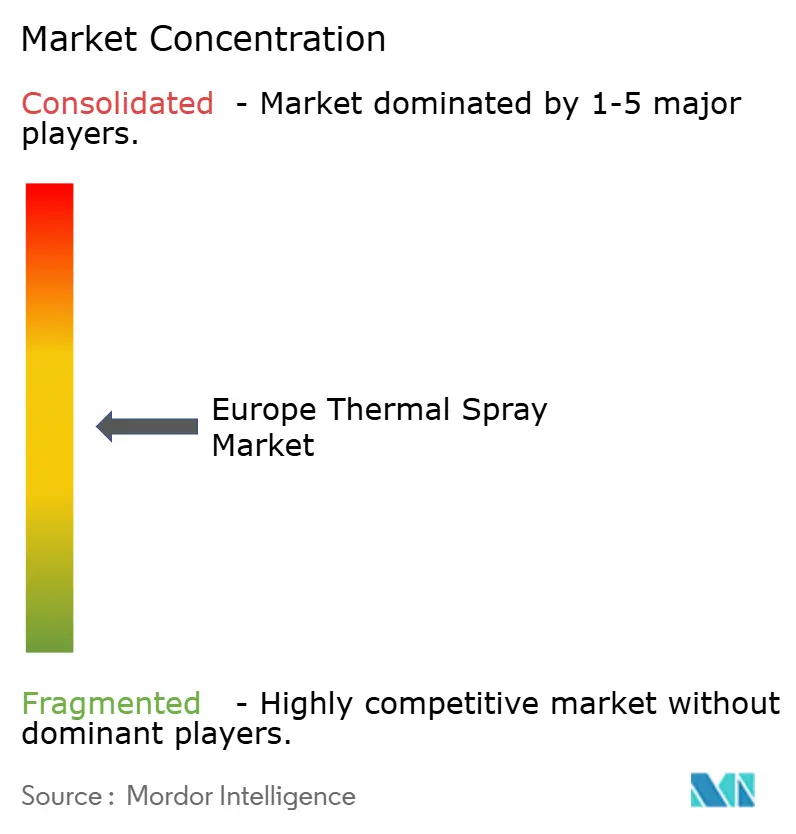

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Thermal Spray Market Analysis by Mordor Intelligence

The Europe Thermal Spray Market size is estimated at USD 3.28 billion in 2025, and is expected to reach USD 3.96 billion by 2030, at a CAGR of 3.83% during the forecast period (2025-2030). Demand is shifting toward aerospace turbine refurbishment and electric-vehicle brake systems, two applications now competing for the same high-velocity oxygen fuel (HVOF) capacity that previously served diesel-engine rebuilds. Equipment purchases outpace consumables as coating houses install robot-integrated spray cells with real-time AI path correction, trimming scrap, and meeting stricter traceability rules. Combustion-based processes remain dominant because they deposit material 15%-25% faster than plasma methods, a decisive edge in high-volume automotive work. At the same time, China’s rare-earth export quotas have inflated yttria-stabilized zirconia (YSZ) powder costs, pushing European buyers to qualify ceria- and magnesia-stabilized alternatives despite shorter cyclic life.

Key Report Takeaways

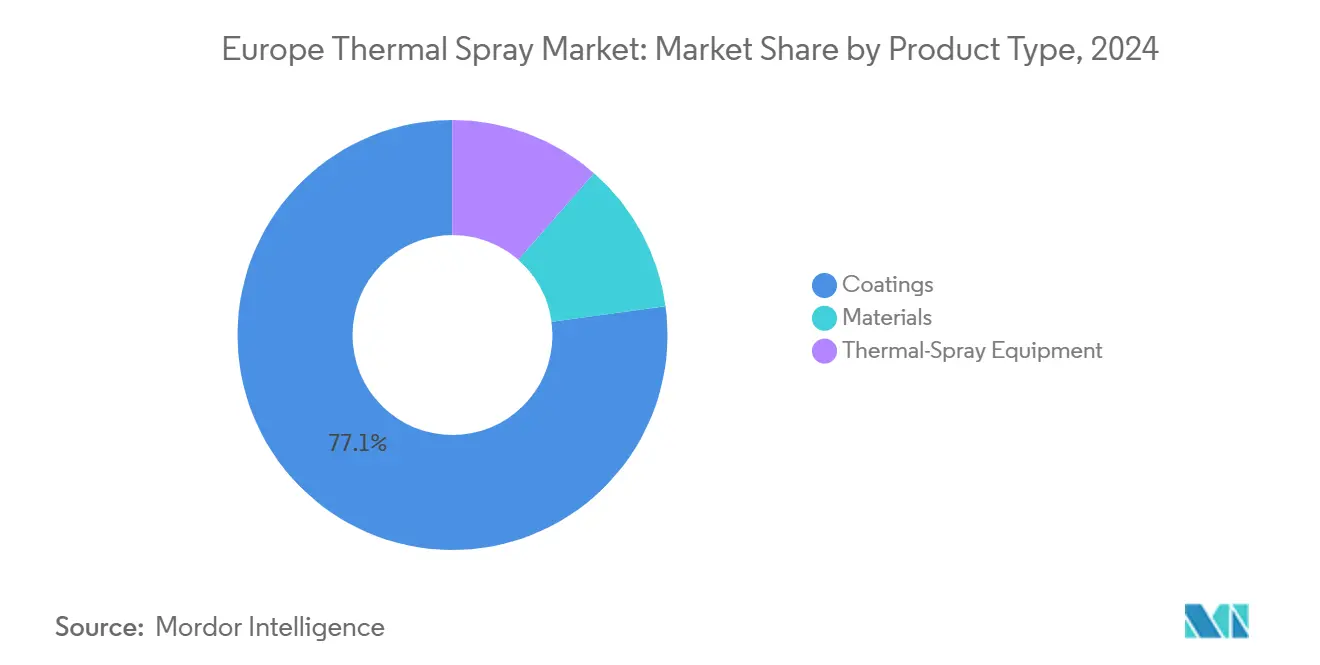

- By product category, coatings held 77.13% of the Europe thermal spray market share in 2024, while thermal spray equipment is projected to record the fastest 3.95% CAGR through 2030.

- By process, combustion methods commanded 72.11% of the Europe thermal spray market size in 2024 and are forecast to expand at a 4.12% CAGR to 2030.

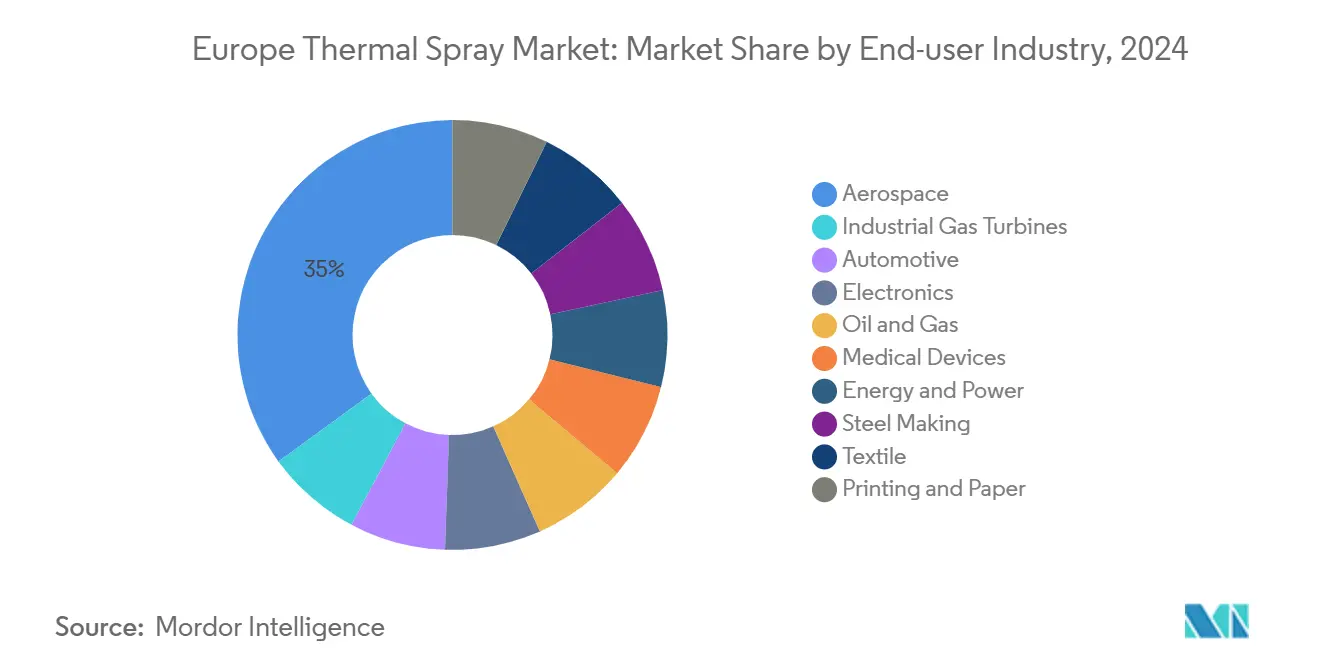

- By end-user, the aerospace sector led with a 34.99% revenue share in 2024; electronics is poised to deliver the highest 3.96% CAGR through 2030.

- By geography, Germany accounted for the fastest 4.06% CAGR, while the Rest of Europe represented 33.37% of the Europe thermal spray market size in 2024.

Europe Thermal Spray Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive and aero-engine demand | +1.2% | Germany, France, UK, Spain, Italy | Medium term (2-4 years) |

| Medical-grade Ti and HA implant coatings | +0.6% | Germany, France, UK, Nordics | Long term (≥ 4 years) |

| EU decarbonization mandates for turbines | +0.9% | Pan-European, focus on Germany, France, Nordics | Short term (≤ 2 years) |

| HVOF ceramics for EV rotors | +0.7% | Germany, France, Spain, Italy | Medium term (2-4 years) |

| AI-optimized spray paths | +0.4% | Germany, France, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Thermal-Spray Demand in Automotive and Aero Engines

Pratt & Whitney’s geared-turbofan (GTF) fleet logged 3.2 million flight hours in 2024, driving a surge in blade-tip abradable coating replacements that consumed 45 metric tons of aluminum-polyester powder across European maintenance, repair, and overhaul sites[1]Pratt & Whitney, “GTF Fleet Update,” prattwhitney.com. Volkswagen’s Salzgitter plant simultaneously adopted cold-spray aluminum coatings for battery enclosures, improving heat dissipation and shortening fast-charge cycles by 30%. Automotive work now yields thinner deposits than legacy cylinder-bore jobs, thereby compressing material throughput per cell hour, whereas aerospace tasks still command premium pricing because FAA and EASA traceability requirements lock in certified applicators. Mid-tier shops are therefore specializing, since equipment optimized for 50-micron abradables cannot switch economically to 500-micron wear-resistant overlays without separate guns. This bifurcation channels high-margin aviation projects toward automated Western European facilities while cost-sensitive EV parts migrate to lower-wage Eastern European sites.

Medical-Grade Ti and HA Coatings for Implants

The EU Medical Device Regulation tightened biocompatibility documentation in 2024, adding EUR 120,000 per coating line in compliance costs and prompting consolidation among ISO 13485-certified applicators. Zimmer Biomet reported a 96.8% survivorship rate at 15 years for plasma-sprayed hydroxyapatite (HA) on femoral stems, outperforming grit-blasted titanium by 2.3 percentage points. This result sustains a EUR 18 coating premium even amid reimbursement pressure. Laser powder-bed fusion implants introduce rough surfaces that require grit-blast smoothing; Fraunhofer IWS demonstrated post-spray laser remelting to raise bond strength 55% while preserving HA crystallinity[2]Fraunhofer IWS, “Hybrid Laser–Spray Processing,” fraunhofer.de. Smaller Italian and Spanish firms lack capital for such hybrid lines, ceding share to vertically integrated giants such as Stryker and Smith & Nephew.

EU Decarbonization Mandates for Turbines and Boilers

The 2024 revision of the Industrial Emissions Directive reduced NOx limits to 50 mg/Nm³ for large gas-fired boilers, requiring operators to operate at 1,450°C and accelerating oxide-scale spallation. Siemens Energy found that applying YSZ top coats to SGT-800 turbines reduced hot-section maintenance costs by 22% over three years, prompting orders for 140 sets across German and Dutch combined-cycle plants. However, China’s export quotas lengthened YSZ powder lead times from 6 to 14 weeks, favoring coating houses with captive powder production. Utilities have queued rotors for 9-12 months, and Eastern European applicators have added second shifts to absorb overflow demand.

Rapid Uptake of HVOF Ceramic Coatings for EV Rotors

Volkswagen specified WC-Co HVOF coatings on ID-series rear rotors to achieve a 180,000 km service life, reducing warranty reserves by EUR 42 per vehicle while incurring only EUR 28 in additional processing costs. Stellantis and Renault issued parallel specifications, creating a forecasted demand for 4.8 million coated rotors annually by 2026. Aerospace-optimized HVOF cells handle 15-20 rotors per hour, yet automotive economics need 40 units per hour, so new high-throughput lines are emerging in Spain and Poland, where labor costs run 35% lower than Germany. Tight run-out tolerances under 0.05 mm also force iron foundries to invest in post-casting machining, shifting some rotor supply to precision forgers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trivalent hard-chrome and PVD substitutes | −0.8% | Germany, France, UK, Italy | Medium term (2-4 years) |

| High capex of robot-integrated spray cells | −0.5% | Pan-European, focus on Western Europe | Short term (≤ 2 years) |

| Supply tightness of YSZ and rare-earth oxides | −0.6% | Pan-European | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emergence of Trivalent Hard-Chrome and PVD Alternatives

EU REACH restrictions on hexavalent chromium accelerated the adoption of trivalent baths that plate at 25 µm per hour, 68% quicker than HVOF chromium-carbide, enabling same-day hydraulic-rod turnaround. Safran Landing Systems qualified arc-PVD CrN on A320 cylinders, matching fatigue life while removing the 0.15 mm grinding step. PVD chambers coat 40 rods per shift, compared to 12 for thermal spray, reducing labor costs from EUR 18 to EUR 6 per part. Thermal spray still excels in thick rebuilds of 2-5 mm but loses ground in thin-film jobs under 150 µm, a segment where Bosch and ZF adopted PVD TiAlN on fuel-injector needles in 2024.

High Capex of Robot-Integrated Spray Cells

A robot-integrated thermal spray cell costs EUR 800,000 to EUR 1.2 million, including robots, HVOF systems, enclosures, filtration, and sensors. Bodycote budgeted EUR 22 million for 18 new cells in 2024 with a 24-month payback that assumes 75% utilization—levels small regional shops rarely hit. Financing is tougher for mid-tier firms because banks require 30% equity, and lease terms reach 6.5% interest, driving all-in capital cost to 9.2%. Capacity growth therefore clusters among the 15 largest coating houses, while 180 smaller shops stay manual and compete on labor rates.

Segment Analysis

By Product Type: Equipment Accelerates as Automation Spreads

Coatings contributed 77.13% of 2024 revenue, but pricing softened by 4% due to Eastern European job shops undercutting Western rivals. Ceramic powders, led by YSZ and chromium carbide, constituted 58% of the feedstock spend, while polymer powders remained a 3% niche for FDA-approved polyetheretherketone implants. Dust-collection systems benefit from the 2024 tightening of particulate limits to 5 mg/Nm³, which increases the average filter cost to EUR 140,000 per cell. Equipment revenue in the Europe thermal spray market will grow at a 3.95% CAGR through 2030, faster than overall market expansion, as shops upgrade to robot-integrated lines that embed AI path correction.

The installed base of 1,800 cells underpins a steady aftermarket for guns, nozzles, and feeders, which account for 28% of equipment sales. Oerlikon and GTV released modular torches that cut nozzle swap time to 15 minutes, improving uptime for high-mix aerospace lines.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Process Type: Combustion Retains the Throughput Edge

Combustion methods captured 72.11% of the Europe thermal spray market share in 2024 and are projected to outpace electric processes with a 4.12% CAGR through 2030. HVOF velocities of 800-1,200 m/s generate dense, low-porosity coatings that automotive and hydraulic users specify for wear parts. Volkswagen’s rotor program shows the advantage: HVOF deposits 4.5 kg/h and finishes a rotor in 7 minutes, versus 12 minutes for plasma spray. Propane-oxygen fuel costs only EUR 12 per kilogram, less than half the expense of argon-hydrogen in plasma environments.

Electric processes, such as atmospheric plasma spray, advance 3.2% annually, which is indispensable for abradable turbine coatings that must maintain 18%-22% porosity; however, HVOF would densify them too much. Cold spray, now accounting for 4% of segment revenue, is used in battery-enclosure and electronics cooling applications because it avoids melt-induced oxidation; however, its ductile-metal limitation caps its potential at approximately 8% of total demand. Cost remains a decisive factor, keeping combustion in front for high-volume parts.

By End-User Industry: Aerospace Stays on Top, Electronics Surges

Aerospace contributed 34.99% of 2024 revenue, consuming 420 t of thermal-barrier and abradable coatings across European MRO hangars. Electronics is the fastest riser at a 3.96% CAGR because EV inverters require copper-diamond layers with a thermal conductivity of 400 W/mK, which is quadruple that of alumina’s 25 W/mK. Industrial gas turbines account for 16% of demand, with Siemens Energy retrofits extending inspection intervals to 24,000 hours. The automotive industry holds 14% and is shifting from 300-µm cylinder-bore coatings to 80-µm brake-rotor layers, reducing material revenue per vehicle by 62% despite higher unit volumes.

Medical devices are clustered in Germany and France, where Zimmer Biomet and Stryker apply HA to hip and knee implants, achieving a 96.8% survivorship rate. Oil & gas, energy, steel, textile, and printing together make up the remainder, each with specialized wear and corrosion needs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany is projected to log a 4.06% CAGR, the fastest in the region, on the back of Volkswagen’s cold-spray battery enclosures and MTU Aero Engines’ YSZ-coated geared-turbofan parts. Its 340 cells represent 28% of the European total, serving clustered automotive and aerospace supply chains that consumed 95 t of HVOF powder in 2024. Regulatory updates on real-time particulate monitoring favor automated cells, reinforcing the lead of Bodycote and Oerlikon.

The Rest of Europe held 33.37% of the Europe thermal spray market size in 2024, buoyed by Poland’s labor-cost edge and Turkey’s turbine demand. Poland delivers 1.8 million brake rotors annually to Stellantis and Volkswagen, reducing lead times from five days to 36 hours. Turkey coats pipeline-compressor turbines but pays 12% more for YSZ because it lacks EU subsidies on raw materials. Russia’s market shrank by 18% in 2024 due to sanctions that limit imports of HVOF equipment.

The United Kingdom and France each command 11-13% shares. Rolls-Royce invested £12 million in Derby vacuum-plasma cells to coat UltraFan blades in-house, reducing the per-blade cost by 18% and shortening the development cycle by six weeks. France’s Safran sites used 32 t of YSZ in 2024, but a 22% electricity-price spike eroded plasma margins, prompting migration of lower-value work to Czech vendors. The Nordics market share is anchored by marine and power-plant refurbishment but constrained by a base of 85 cells.

Competitive Landscape

The Europe Thermal Spray market is moderately consolidated. Oerlikon’s 2024 purchase of AM Coating signals confidence that additive-manufactured parts will need hybrid spray finishing, an area that smaller players cannot match. Equipment makers Lincoln Electric, GTV, and Flame Spray Technologies are promoting modular gun designs with 15-minute nozzle swaps, targeting aerospace lines that process up to 18 formulations weekly. Vertical integration gains favor in the automotive industry; Volkswagen’s in-house Salzgitter line has already diverted EUR 18 million in annual work from external applicators.

Europe Thermal Spray Industry Leaders

Saint-Gobain

Hoganas AB

Linde Plc

Bodycote

OC Oerlikon Management AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Scotland-based ATL Turbine Services expanded its technological capabilities by investing in the Surface Two thermal spray system from OC Oerlikon Management AG, enabling the delivery of high-performance, precision-engineered coating solutions for turbine components across the aerospace, energy, and industrial sectors.

- December 2024: Kymera International, a specialty materials company based in the United States, acquired Coating Center Castrop GmbH (CCC), a thermal spray and precision machining specialist in Germany, for the aerospace, marine propulsion, pharmaceutical, and general industrial markets.

Europe Thermal Spray Market Report Scope

Thermal spray is an industrial coating process that utilizes high-velocity heat to melt or soften materials, then sprays them onto a surface, creating a protective or functional layer. This technique applies metallic, ceramic, or polymer coatings to enhance properties like wear resistance, corrosion protection, and thermal insulation, often used to restore worn components or add new surface properties.

The Europe Thermal Spray market is segmented by product type, process type, end-user industry, and geography. By product type, the market is segmented into coatings, thermal-spray equipment, and materials. By process type, the market is segmented into combustion and electric energy. By end-user industry, the market is segmented into aerospace, industrial gas turbines, automotive, electronics, oil and gas, medical devices, energy and power, steelmaking, textiles, and printing and paper. The report also covers the market size and forecasts for the thermal spray market in six countries across the European region. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

By Product Type

| Coatings | |||

| Materials | Coating Materials | Powders | Ceramics |

| Metals | |||

| Polymer | |||

| Other Coating Materials | |||

| Wires/Rods | |||

| Other Materials | |||

| Thermal-Spray Equipment | Thermal Spray Coating System | ||

| Dust Collection Equipment | |||

| Spray Gun and Nozzle | |||

| Feeder Equipment | |||

| Spare Parts | |||

| Noise-reducing Enclosure | |||

| Other Thermal Spray Equipment | |||

By Process Type

| Combustion |

| Electric Energy |

By End-user Industry

| Aerospace |

| Industrial Gas Turbines |

| Automotive |

| Electronics |

| Oil and Gas |

| Medical Devices |

| Energy and Power |

| Steel Making |

| Textile |

| Printing and Paper |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDICS Countries |

| Russia |

| Rest of Europe |

| By Product Type | Coatings | |||

| Materials | Coating Materials | Powders | Ceramics | |

| Metals | ||||

| Polymer | ||||

| Other Coating Materials | ||||

| Wires/Rods | ||||

| Other Materials | ||||

| Thermal-Spray Equipment | Thermal Spray Coating System | |||

| Dust Collection Equipment | ||||

| Spray Gun and Nozzle | ||||

| Feeder Equipment | ||||

| Spare Parts | ||||

| Noise-reducing Enclosure | ||||

| Other Thermal Spray Equipment | ||||

| By Process Type | Combustion | |||

| Electric Energy | ||||

| By End-user Industry | Aerospace | |||

| Industrial Gas Turbines | ||||

| Automotive | ||||

| Electronics | ||||

| Oil and Gas | ||||

| Medical Devices | ||||

| Energy and Power | ||||

| Steel Making | ||||

| Textile | ||||

| Printing and Paper | ||||

| By Geography | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| NORDICS Countries | ||||

| Russia | ||||

| Rest of Europe | ||||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe thermal spray market in 2025?

The Europe thermal spray market size stands at USD 3.28 billion in 2025 and is projected to reach USD 3.96 billion by 2030.

Which product category grows fastest?

Equipment leads with a 3.95% CAGR because coating houses are investing in robot-integrated cells and AI controls.

Why do combustion processes dominate over plasma?

HVOF and other combustion methods deposit material 15%-25% faster and cost less in fuel, making them the preferred choice for high-volume parts.

What is driving electronics demand for thermal spray?

EV power-module substrates need copper-diamond coatings that dissipate heat at 400 W/mK, far above alumina’s capacity, boosting electronics-sector uptake.

How are rare-earth quotas impacting European suppliers?

China’s export restrictions added 18% to YSZ powder prices and stretched lead times to 14 weeks, prompting European firms to qualify ceria- and magnesia-stabilized zirconia.