Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

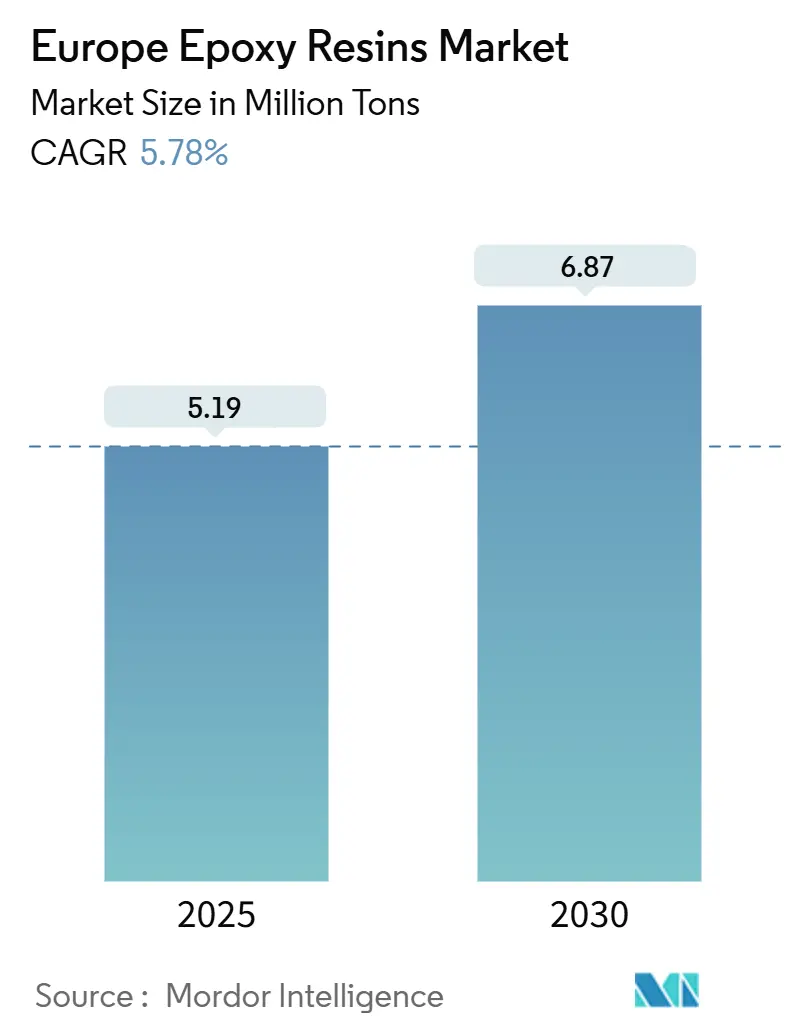

| Market Volume (2025) | 5.19 Million tons |

| Market Volume (2030) | 6.87 Million tons |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Epoxy Resins Market Analysis by Mordor Intelligence

The Europe Epoxy Resins Market size is estimated at 5.19 million tons in 2025, and is expected to reach 6.87 million tons by 2030, at a CAGR of 5.78% during the forecast period (2025-2030). The expansion reflects stronger demand from wind-energy blade production, construction-sector renovation programs, and electric-vehicle lightweighting, even as tighter regulation of bisphenol A and epichlorohydrin chemistry, as well as new anti-dumping duties, reshape raw-material flows. Paints and coatings maintain leadership thanks to the Energy Performance of Buildings Directive, while Germany anchors regional growth on the back of automotive composites and federal subsidies for gigawatt-scale semiconductor fabs. The tariff wall introduced in February 2025 against Chinese, Taiwanese, and Thai imports has already allowed regional resin producers to lift prices, although the permanent shutdown of Ineos Phenol’s Gladbeck phenol unit exposes a structural feedstock gap. Formulators continue to trial bisphenol F, novolac, and bio-based routes to hedge against looming endocrine-disruption restrictions while preserving compatibility with existing curing agents.

Key Report Takeaways

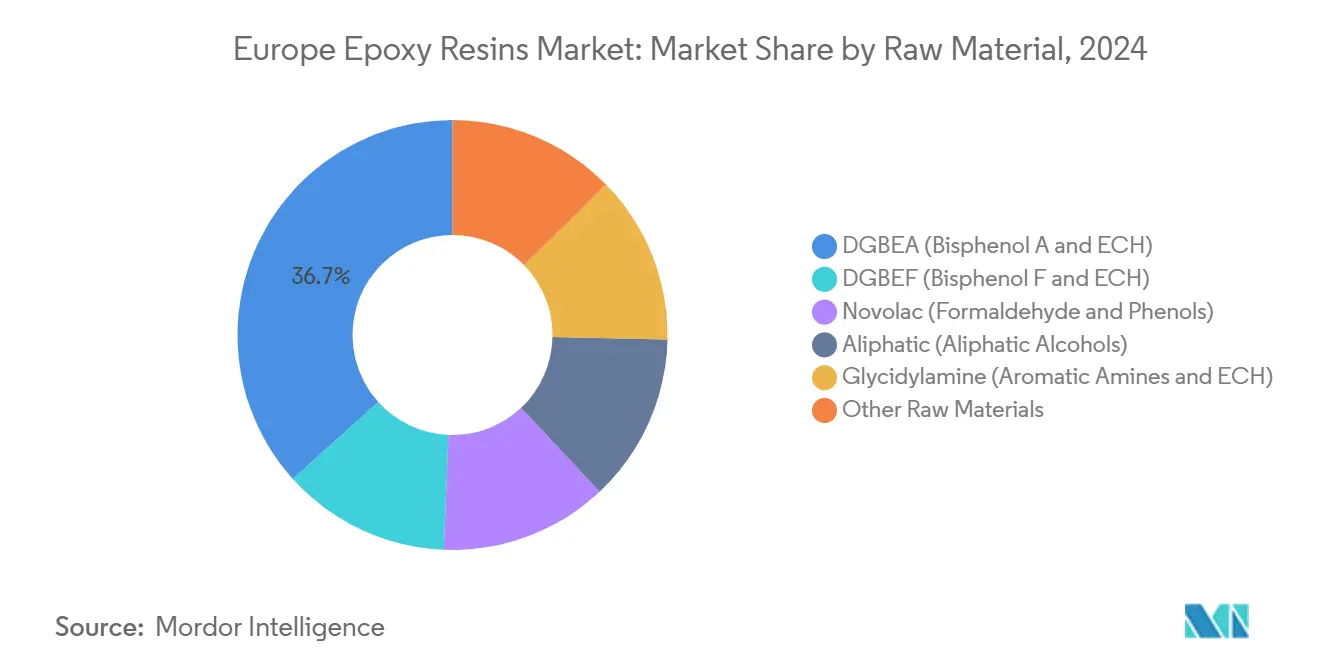

- By raw material, DGBEA (Bisphenol A and ECH) held 36.67% of Europe epoxy resin market share in 2024 and it is expected to record the fastest growth at 6.38% CAGR to 2030.

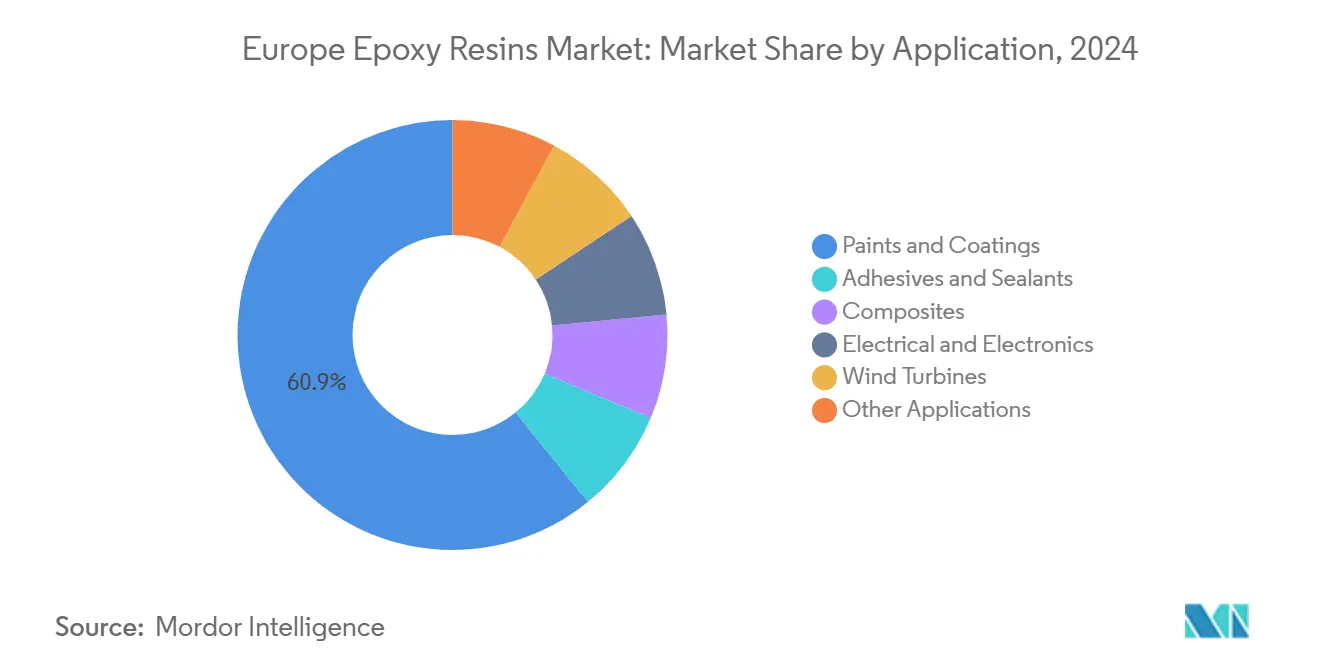

- By application, paints and coatings accounted for a 60.86% share in 2024, and this is expected to grow at a CAGR of 6.24% during the forecast period (2025-2030).

- By geography, Germany captured 30.23% of the market volume in 2024 and is expected to expand at a 6.18% CAGR through 2030.

Europe Epoxy Resins Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in wind-energy blade demand | +1.2% | Germany, Spain, Nordic region, North Sea | Long term (≥4 years) |

| Lightweight automotive composites push | +0.9% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Expansion of electronics and electricals manufacturing | +0.4% | Germany, France, Italy | Medium term (2-4 years) |

| Rebound in protective construction coatings | +1.5% | Germany, France, Spain, Italy, United Kingdom | Short term (≤2 years) |

| EU Renovation Wave subsidies for epoxy floors | +0.8% | Germany, France, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Wind-Energy Blade Demand

Europe aims to achieve 510 GW of installed wind capacity by 2030; however, the International Energy Agency forecasts the continent will reach only 370 GW, resulting in a 28% gap that is lengthening project lead times. Blade production consumes up to 10 tons of epoxy per multi-MW unit, driving resin consumption across Denmark, Spain, and Italy, where Vestas and Siemens Gamesa run blade plants. Vestas earmarked EUR 531 million for green R&D in 2024, with EUR 20.5 million allocated to CETEC, a consortium comprising Olin and Stena Recycling, which aims to demonstrate the chemical recycling of end-of-life blades by 2026[1]Vestas Wind Systems, “Annual Report 2024,” vestas.com. Success would create a circular feedstock pool and alleviate pressures on virgin resin demand. Offshore wind growth in the North Sea continues to drive demand for marine coatings and subsea grout applications, which also rely on epoxy chemistry.

Lightweight Automotive Composites Push

Airbus increased A350 output to 10 aircraft per month in 2024, and the model uses epoxy-matrix composites for 52% of its structure. Hexcel responded with new prepreg lines in France and Austria, supporting a 12.5% sales rise in Q4 2024. On the road, battery packs add 400-500 kg to electric vehicles, prompting OEMs to switch from steel to carbon-fiber epoxy body panels, which reduce mass by up to 50%. Ricardo projects rising composite content in European light vehicles through 2030, while Toray and Syensqo have expanded carbon-fiber capacity to meet demand.

Expansion of Electronics and Electricals Manufacturing

The EU Chips Act allocates EUR 43 billion to double regional semiconductor capacity by 2030, with Intel’s Magdeburg fab and TSMC’s Dresden plant alone expected to require several kilotons of ultra-pure novolac and cycloaliphatic resins. Although Europe’s PCB sector shrank to 2.3% of global output by 2022, the growth in advanced packaging partly offsets the decline. The European Semiconductor Strategy now seeks PFAS-free materials, prompting formulators to adopt bio-based epoxy alternatives.

Rebound in Protective Construction Coatings

Revisions to the Energy Performance of Buildings Directive require the disclosure of life-cycle global warming potential for new buildings from 2028, directing specifiers to use long-life epoxy coatings that amortize the embodied carbon. The Construction Products Regulation 2024/3110 added digital product passports that favor suppliers with verified environmental data. Waterborne dispersions already hold 55% of Europe’s industrial coatings demand, while powder systems show the fastest growth as they meet volatile-organic-compound caps.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA and ECH regulatory scrutiny | -0.6% | European Union | Short term (≤2 years) |

| Crude-linked raw-material price volatility | -0.5% | Germany, Italy, France | Short term (≤2 years) |

| Bio-based resin substitution threat | -0.3% | Nordic region, Germany | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

BPA and ECH Regulatory Scrutiny

Regulation 2024/3190 bans bisphenol A in food-contact materials from 2025, leaving only narrow derogations for large storage tanks and polysulfone membranes. Parallel CLP amendments add Carcinogen 1B and Skin Sensitizer 1A tags to popular accelerators, raising compliance costs by up to 12% for mid-tier producers[2]European Chemicals Agency, “CLP Amendments 2024,” echa.europa.eu. The new labels also extend reformulation lead times as products pass customer requalification. Sanctions under Council Regulation 2024/745 further restrict data sharing with certain Russian entities, complicating joint research and development on specialty grades.

Crude-Linked Raw-Material Price Volatility

Epichlorohydrin and bisphenol A mirror crude-oil swings with a time lag, squeezing margins when benzene and propylene spike faster than quarterly price-adjustment clauses. The British Plastics Federation recorded only 3-5% price increases for epoxy between March and May 2024, despite steeper jumps in competing resin chemistries. Ineos Phenol’s shutdown in Gladbeck eliminates 240,000 tons of phenol capacity and highlights Europe’s feedstock cost disadvantage relative to integrated Middle East complexes. Sluggish cracker utilization—around 75%—and aging assets compound the issue.

Segment Analysis

By Raw Material – Regulatory Crosswinds Reposition Mainstream Feedstocks

DGBEA retained 36.67% of Europe epoxy resin market share in 2024 and is trending at a 6.38% CAGR to 2030, yet its reliance on bisphenol A exposes formulators to regulatory risk that is triggering a pivot toward bisphenol-F and novolac alternatives. Novolac resins deliver crosslink densities 30–40% above DGBEA, raising glass-transition temperatures beyond 150°C and making them indispensable for semiconductor encapsulation once Intel’s Magdeburg and TSMC’s Dresden lines commence operation in 2027. Europe epoxy resin market size for novolac grades is therefore set to expand more quickly than the baseline. Glycidylamine systems remain the benchmark for aerospace prepregs due to their glass-transition temperatures above 200°C, which meet Airbus A350 service requirements. Meanwhile, cycloaliphatic and aliphatic grades address ultraviolet stability in decorative finishes and LED encapsulation. REACH fees and data-sharing obligations have encouraged consolidation, giving vertically integrated majors an edge as they can amortize compliance costs across broader volumes.

Formulators are also validating bio-based epichlorohydrin from glycerol. While commercial supply is limited, a successful scale-up would reduce chlorine use and improve carbon footprints. Ongoing trials suggest performance parity in flooring and electrical potting, but cost parity requires larger Asian capacities or European on-purpose plants. Until then, most producers hedge by blending bio-content with conventional feedstocks to balance mechanical performance and pricing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application – Coatings Dominate as Construction Revival Gains Traction

Paints and coatings commanded 60.86% of Europe epoxy resin market size in 2024 and show a 6.24% CAGR through 2030 as building-energy codes favor long-life protective layers. Waterborne dispersions already meet the Industrial Emissions Directive's solvent limits, while powder coatings post the fastest gains due to their zero VOCs. Marine coatings for offshore wind foundations and LNG carriers rely on epoxy primers that survive decades of immersion, ensuring steady pull-through in Northern Europe shipyards.

Adhesives and sealants with reactive chemistries are overtaking mechanical fasteners in the body-in-white assembly process. Composites applications, including wind turbine blades, vehicles, and sporting goods, represent the highest unit growth potential. Europe epoxy resin market share for wind-energy blades is forecast to climb as turbine lengths increase and blade recycling initiatives unlock secondary raw materials. Electronics demand is mixed: the migration of printed-circuit-board production to Asia offsets gains from advanced packaging, but novolac encapsulants for EU fab projects provide a niche growth pocket that stabilizes volumes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany held 30.23% of Europe epoxy resin market size in 2024 and is expanding at a 6.18% CAGR to 2030. Growth aligns with EUR 18.6 billion in federal retrofit subsidies, electric-vehicle composite uptake, and the upcoming Intel fab, which will utilize multi-kiloton quantities of ultra-pure novolac resin. Yet the Gladbeck phenol shutdown heightens exposure to imported feedstocks and underscores energy-cost disadvantages.

Spain installed 30.8 GW of wind capacity in 2024 and aims to reach 62 GW by 2030, driving blade-resin growth through Siemens Gamesa and Vestas plants. France’s MaPrimeRénov pays homeowners to install epoxy-based floors and moisture barriers, while Italy hosts Vestas’ Taranto offshore blade line. Each market benefits from Renovation Wave grants, lifting short-term volumes in coatings and flooring.

Nordic countries punch above their population weight due to offshore wind and marine coatings activity centered around Denmark and Norway. The United Kingdom’s construction PMI dipped below 50 in December 2024, but the local composites sector remains buoyed by aerospace and niche automotive brands. Central and Eastern Europe gain share as lower labor costs attract downstream molding operations, and Czech producer Spolchemie upgrades epichlorohydrin units to compete on energy efficiency SPOLCHEMIE.CZ. The February 2025 anti-dumping duties covering 70,000 tons of Asian imports have tightened supply, allowing European producers to lift prices by 5–7% while South Korean suppliers capitalize on their duty-free status.

Competitive Landscape

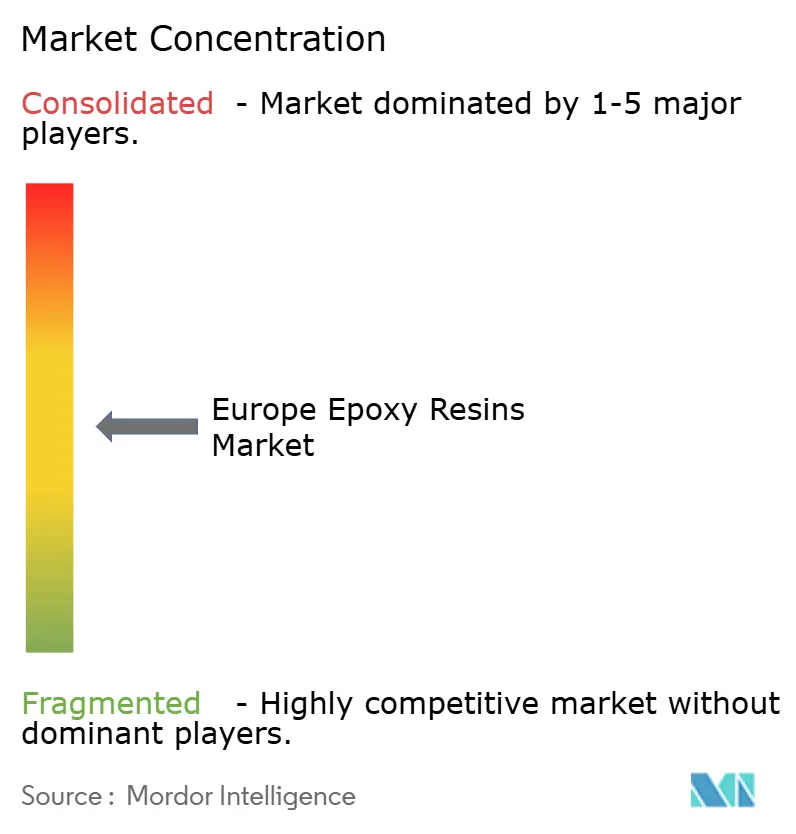

The Europe Epoxy Resins market possesses moderate concentration. Integrated players span chlorine, epichlorohydrin, bisphenol, and formulated resin stages, enabling them to buffer feedstock volatility and regulatory costs. Capacity rationalization is evident in Ineos Phenol’s exit, which removes a critical phenol stream but may improve margins for surviving producers. The investment focus has shifted toward bio-based and circular solutions. Asian competition persists despite duties. Chinese, Thai, and Taiwanese volumes face tariffs up to 40.8%, but South Korean suppliers exploit their exemption to expand their share through competitive pricing and technical service packages.

Europe Epoxy Resins Industry Leaders

-

Covestro AG

-

Huntsman International LLC

-

Olin Corporation

-

BASF

-

Westlake Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Westlake Corporation announced that Westlake Epoxy plans to launch several new products at the European Coatings Show (ECS) 2025 in Germany. The company will introduce the EpoVIVE portfolio of epoxy resins with a lower carbon footprint.

- March 2025: BASF and Sika jointly developed a new amine building block for curing epoxy resins, commercially available under BASF’s Baxxodur EC 151 brand. This new development is suitable for flooring applications, including production plants, storage and assembly halls, as well as parking decks.

Europe Epoxy Resins Market Report Scope

Epoxy resins are reinforced polymer composites derived from petroleum sources, resulting from a reactive process involving epoxide units. Epoxide and another molecule with two hydroxyl groups are copolymerized to produce epoxy resin. It is mostly used in applications such as paints and varnishes, adhesives, and composites.

The Europe epoxy resin market is segmented by raw material and application. By raw material, the market is segmented into DGBEA, DGBEF, Novolac, Aliphatic, Glycidylamine, and other raw materials. By application, the market is segmented into paints and coatings, adhesives and sealants, composites, electrical and electronics, and other applications. The report also covers the market size and forecasts for epoxy resins in 5 countries across the European region.

For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Raw Material

| DGBEA (Bisphenol A and ECH) |

| DGBEF (Bisphenol F and ECH) |

| Novolac (Formaldehyde and Phenols) |

| Aliphatic (Aliphatic Alcohols) |

| Glycidylamine (Aromatic Amines and ECH) |

| Other Raw Materials |

By Application

| Paints and Coatings |

| Adhesives and Sealants |

| Composites |

| Electrical and Electronics |

| Wind Turbines |

| Other Applications |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| NORDIC Countries |

| Rest of Europe |

| By Raw Material | DGBEA (Bisphenol A and ECH) |

| DGBEF (Bisphenol F and ECH) | |

| Novolac (Formaldehyde and Phenols) | |

| Aliphatic (Aliphatic Alcohols) | |

| Glycidylamine (Aromatic Amines and ECH) | |

| Other Raw Materials | |

| By Application | Paints and Coatings |

| Adhesives and Sealants | |

| Composites | |

| Electrical and Electronics | |

| Wind Turbines | |

| Other Applications | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe epoxy resin market in 2025?

The market reached 5.19 million tons in 2025 and is forecast to rise to 6.87 million tons by 2030.

What is the expected compound annual growth rate for epoxy resins in Europe to 2030?

The market is set to expand at a 5.78% CAGR over 2025-2030.

Which application segment uses the most epoxy resin in Europe?

Paints and coatings lead with 60.86% of 2024 volume and a 6.24% CAGR outlook.

Why is Germany the largest national market for epoxy resin?

Germany combines strong construction retrofit funding, electric-vehicle composite adoption, and semiconductor investments, giving it 30.23% share in 2024.

How are EU regulations affecting bisphenol A use in epoxy resins?

Regulation 2024/3190 bans bisphenol A in food-contact materials from 2025, forcing formulators to shift toward bisphenol-F, novolac, and bio-based resins.

Page last updated on: