Market Overview

| Study Period | 2019 - 2030 |

|---|---|

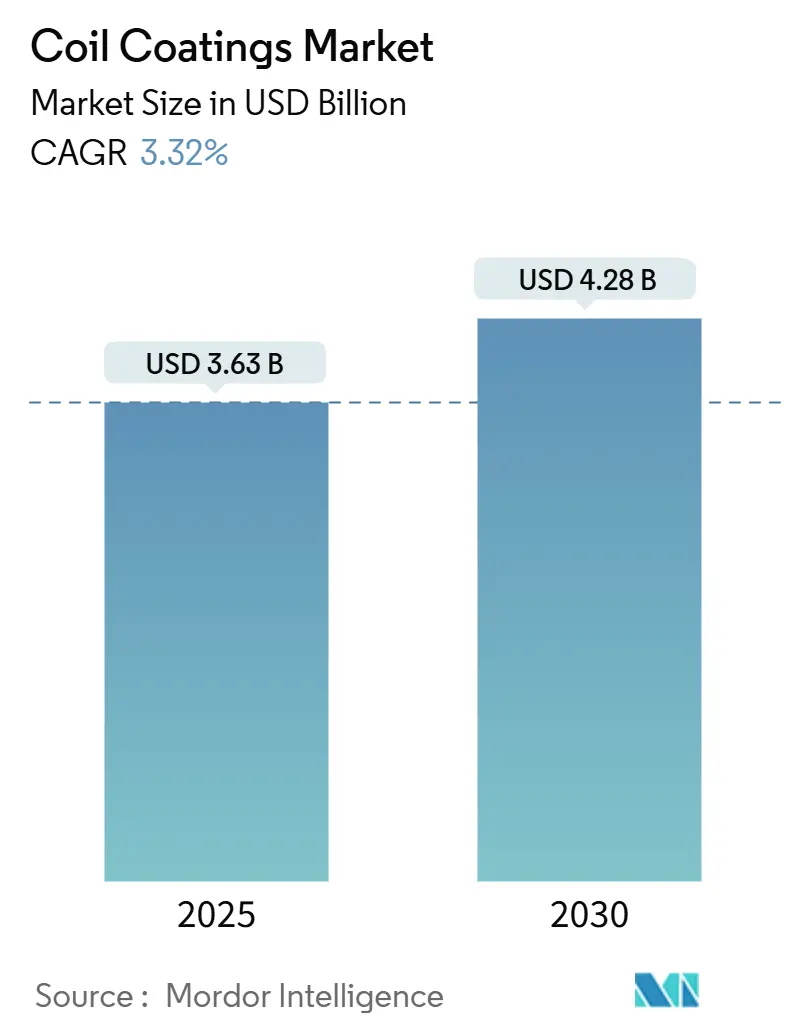

| Market Size (2025) | USD 3.63 Billion |

| Market Size (2030) | USD 4.28 Billion |

| Growth Rate (2025 - 2030) | 3.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Coil Coatings Market Analysis by Mordor Intelligence

The Coil Coatings Market size is estimated at USD 3.63 billion in 2025, and is expected to reach USD 4.28 billion by 2030, at a CAGR of 3.32% during the forecast period (2025-2030). Steady construction spending, an upswing in appliance production, and tightening environmental rules anchor this trajectory, even as substrate competition and raw-material volatility moderate headline growth. Demand concentrates in roll-formed steel and aluminum sheets because pre-finishing offers faster installation, uniform quality, and lower lifetime cost than post-fabrication painting. Investments aimed at modular buildings, solar metal framing, and premium home appliances lift volumes in mature regions, while Asia-Pacific’s large manufacturing base keeps the coil coatings market firmly centered in the region. Across segments, polyester chemistries dominate, PVDF (Polyvinylidene Fluoride) gathers momentum in high-end exteriors, and the shift to PFAS-free fluoropolymers is reshaping innovation pipelines.

Key Report Takeaways

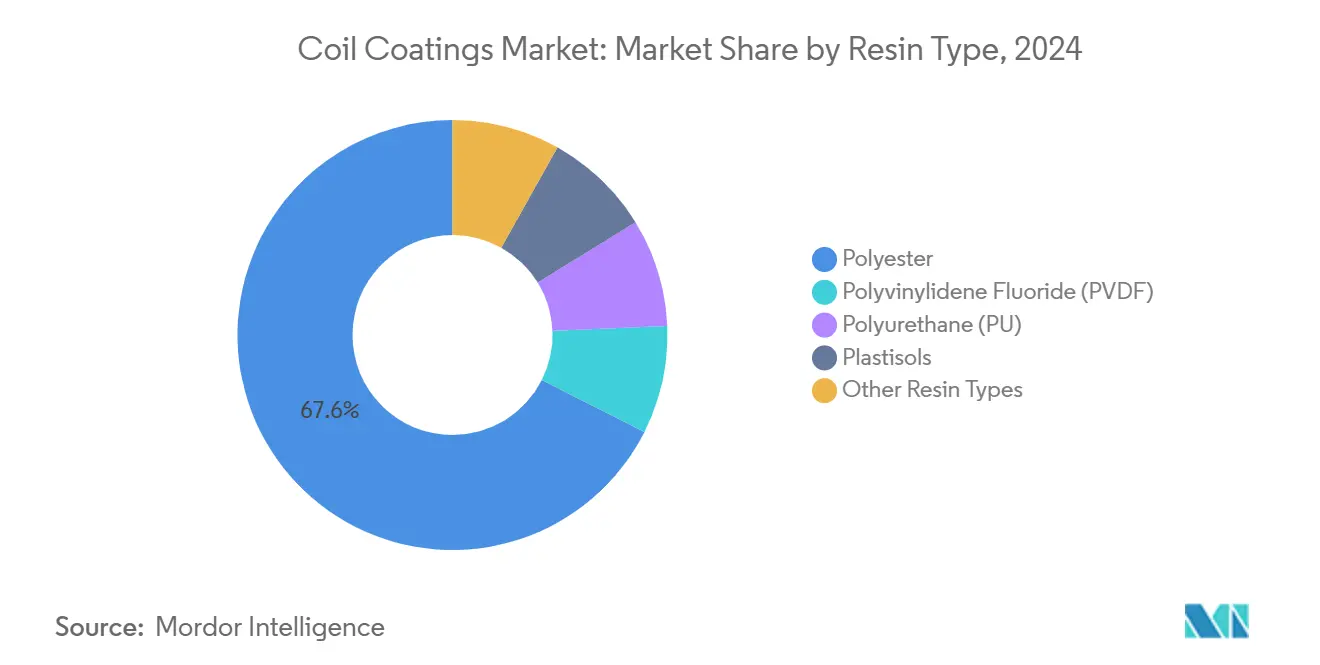

- By resin type, polyester held 67.56% of the Coil Coatings market share in 2024; PVDF is projected to deliver a 3.68% CAGR through 2030.

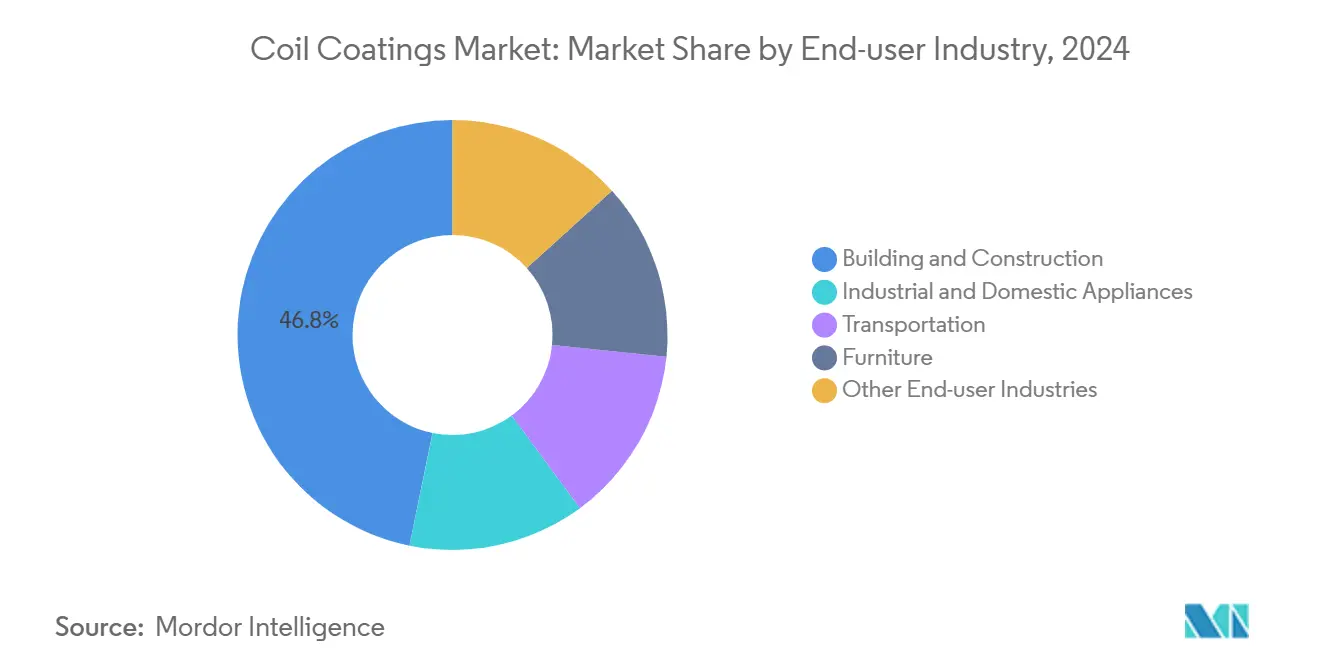

- By end-user industry, building and construction captured 46.78% of the Coil Coatings market size in 2024, while transportation is forecast to expand at a 3.56% CAGR between 2025 and 2030.

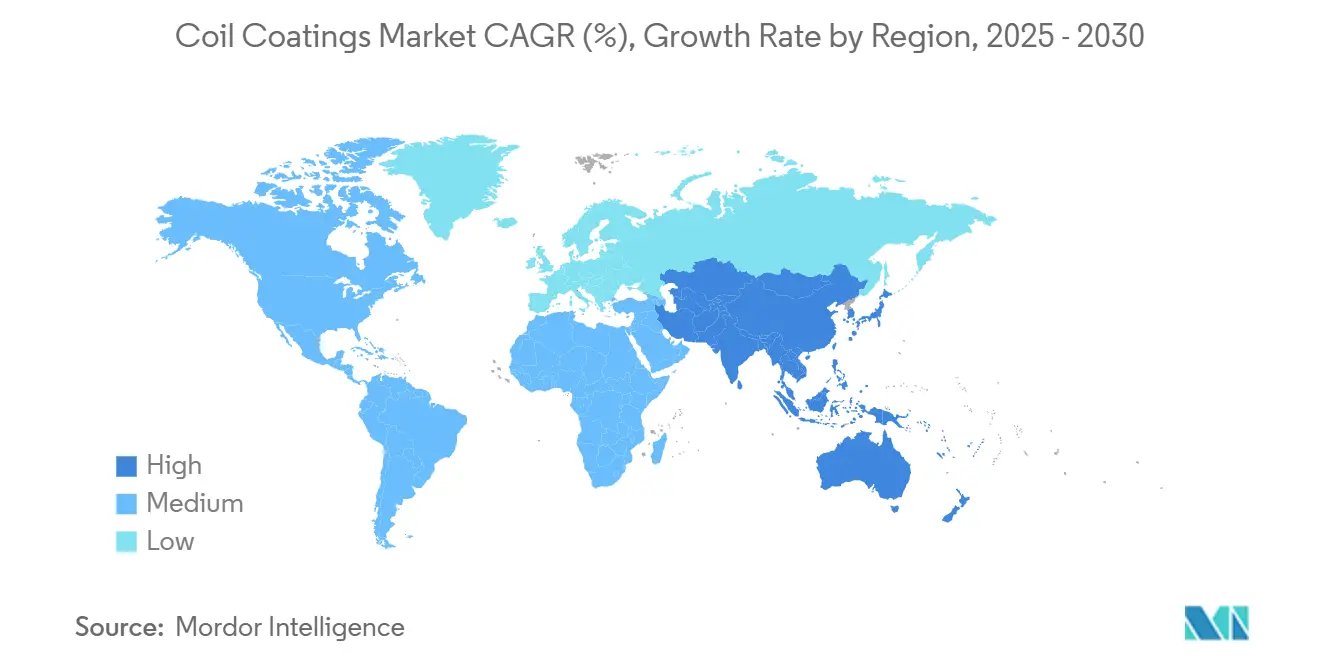

- By geography, Asia-Pacific commanded 50.35% of the coil coatings market size in 2024 and is advancing at a 3.78% CAGR through 2030.

Global Coil Coatings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction Steel Demand Upswing | +0.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Energy-efficient Appliances Expansion | +0.6% | Global, concentrated in APAC manufacturing hubs | Long term (≥ 4 years) |

| Stricter VOC and Carbon Regulations | +0.5% | North America & EU primary, expanding to APAC | Short term (≤ 2 years) |

| Shift toward High-Durability Exterior Panels | +0.4% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Agrivoltaic Metal Framing Boom | +0.3% | Global, early adoption in EU, US, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Steel Demand Upswing

Recovering construction steel orders drive greater use of pre-coated coil because builders can eliminate on-site painting delays, mitigate weather risks, and lower labor costs. The World Steel Association signals a 2025 rebound in global steel demand, with non-residential and infrastructure spending pushing volumes in the United States, China, and India[1]World Steel Association, “Short Range Outlook 2025,” worldsteel.org. Governments channel stimulus into bridges, schools, and renewable-energy projects, favoring corrosion-resistant coil-coated panels. Modular construction firms increasingly specify factory-finished sheets to standardize quality and compress project timelines. Polyester and PVDF coatings with 20- to 30-year warranties support this momentum by lowering total maintenance expense. These factors underpin a significant share of future coil coatings market growth.

Energy-efficient Appliances Expansion

Appliance OEMs (original equipment manufacturers) specify coil coatings to satisfy thermal performance and design demands. Heat-pump outdoor units require finishes that survive freeze-thaw cycles while retaining heat-transfer efficiency, a need highlighted by the United States Department of Energy’s incentive programs. Korean manufacturers Samsung and LG are scaling premium built-in product lines worth USD 64.5 billion globally, with color-matched, scratch-resistant coatings acting as brand differentiators. Engineers must ensure chemical compatibility as refrigeration moves to low-GWP (Global Warming Potential) refrigerants; advanced polyester-silicone hybrids provide the necessary barrier. Luxury real-estate trends toward integrated kitchens elevate aesthetic expectations, pressuring suppliers to offer deep-hue, high-gloss coil options. These dynamics create durable demand pockets inside the coil coatings market.

Stricter VOC and Carbon Regulations

Regulators tighten allowable solvent emissions, forcing plants to adopt waterborne, high-solids, or powder formulations. The U.S. EPA National Emission Standards for Hazardous Air Pollutants (NESHAP) cut permissible VOC levels for coil coating lines, prompting capital upgrades and formulation revisions. In Europe, Best Available Techniques documents set a benchmark of 0.73–0.84 g/m² VOC output for continuous lines, catalyzing investments in regenerative thermal oxidizers and new coating chemistries. Manufacturers with low-VOC portfolios gain procurement preference from OEMs looking to decarbonize scope 3 footprints. Powder coil coating, though currently limited by curing-temperature constraints, is gaining R&D attention because it could eliminate solvent use. Therefore, Compliance pressure underpins risk mitigation and fresh sales opportunities across the coil coatings market.

Shift toward High-Durability Exterior Panels

Climate resilience priorities escalate performance specs for façades and roofs, lifting PVDF demand thanks to its UV and color-retention superiority. Cool-roof formulations incorporating infrared-reflective pigments reduce building energy loads, aligning with green-building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method). Architects increasingly request metallic and pearlescent finishes, stimulating advances in mica-based pigment systems that withstand thermal cycling without chalking. Regions prone to hurricanes or wildfires adopt impact-resistant and non-combustible metal panels, requiring robust topcoats compliant with ASTM E84 and FM 4473 standards. The result is a steady mix shift toward high-performance chemistries that sustain premium price points.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Titanium Dioxide and Resin Prices | -0.4% | Global, with supply chain concentrated in China | Short term (≤ 2 years) |

| Plastic and Composite Material Substitution | -0.3% | North America & EU leading, spreading to APAC | Medium term (2-4 years) |

| PFAS-free Fluoropolymer Reformulations | -0.2% | Global, regulatory-driven in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Titanium Dioxide and Resin Prices

Titanium dioxide (TiO₂) markets experienced rapid price oscillations throughout 2024 as Chinese output cuts, power shortages, and environmental inspections collided with uneven demand from coatings, plastics, and paper. Because white and pastel coil colors rely heavily on TiO₂, quarter-to-quarter swings erode margins or trigger pass-through clauses that unsettle customers. Polyesters and acrylic resins follow upstream petrochemical cycles, so feedstock disruptions in Asia can ripple across global supply chains within weeks. Producers hedge by expanding multi-sourcing, raising safety stocks, or blending alternative pigments, yet these tactics inflate working capital and complicate formulation stability.

Plastic and Composite Material Substitution

In certain façades, vehicle body panels, and consumer goods, engineered plastics challenge coated metal based on weight savings and design flexibility. Danish firm Primo A/S supplies composite cladding profiles that tout corrosion immunity and point-of-sale customization. DuPont’s Zytel and Delrin families enable metal replacement in automotive brackets and housings, delivering mass reduction critical to electric-vehicle range goals[2]DuPont, “Engineering Polymers for Lightweighting,” dupont.com. Although high material cost and recycling hurdles limit polymer encroachment to niche or luxury segments, every incremental substitution trims the serviceable tonnage for the coil coatings industry over the mid-term.

Segment Analysis

By Resin Type: Polyester Dominance Faces PVDF Challenge

Polyester chemistries represented 67.56% of 2024 revenue thanks to low unit cost, broad color gamut, and compatibility with a spectrum of primers and backers. Recent investments in high-solids and weather-resistant hybrids strengthen their foothold in mid-range building and appliance programs. The coil coatings market size for polyester products eclipses USD 2 billion today, underpinning line utilization across Asia’s contract coaters. Although smaller in volume, PVDF grades post a 3.68% CAGR to 2030 as architects prioritize 30-year warranties and deep-tone aesthetics in large commercial façades. The coil coatings market share grabbed by PVDF is further fueled by cool-roof codes in hot climates that specify minimum solar-reflectance values.

Transitioning to PFAS-free fluoropolymers has initiated an intense R&D (research and development) race. NOF Metal Coatings Group unveiled pilot batches that match traditional weathering metrics, signaling viable pathways to regulation-proof premium topcoats. Sherwin-Williams’ RadGuard radiation-cure line illustrates another innovation vector: UV-triggered polymerization that trims natural-gas usage and raises line speed, appealing to coaters eager to curb carbon footprints. As customers judge bids not only on cost but also on embodied carbon and recyclability, resin suppliers with credible environmental data stand to gain wallet share across the coil coatings market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user Industry: Construction Leadership Amid Transportation Growth

Building and construction applications accounted for 46.78% of 2024 billings, covering roofing, siding, rainwater systems, and façade elements. Demand pivots around speed-to-site advantages—pre-coated sheets arrive ready to install—slashing labor and weather delays. Government infrastructure packages in the United States, Canada, and India keep pipeline visibility strong through 2027. Meanwhile, although only a mid-single-digit slice now, transportation advances at a 3.56% CAGR as automakers substitute painted blanks with coil-coated aluminum, streamlining stamping, and eliminating primer ovens. The coil coatings market size linked to EV battery casings and lightweight commercial trailers is gaining strategic importance for tier-one suppliers.

Electrification raises thermal-management and corrosion-resistance bars, prompting specification of silicone-modified polyesters and zinc-rich primers. The United States Department of Energy funds pilot lines exploring integrated insulation layers that could embed dielectric properties directly into coil-coated battery boxes. Appliance replacement cycles continue to deliver steady, margin-friendly volumes, particularly in premium stainless-look and matte finishes that replicate powder-coated aesthetics. Furniture and miscellaneous sectors remain specialized but profitable, tapping low-gloss polyurethanes for abrasion-resistant storage cabinets and signage.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific held 50.35% of global revenue in 2024 and is on track for a 3.78% CAGR to 2030 despite pockets of steel oversupply. China’s stimulus-backed rail and EV charging buildout cushions domestic demand, while export-oriented coil lines feed appliance clusters across ASEAN. Japan leverages long-term supply deals with ocean-going shipyards and home-grown appliance majors to sustain premium PVDF demand, whereas South Korea’s appliance giants outsource additional tonnage to Vietnamese toll coaters to optimize logistics for export markets. India’s smart-city schemes and rural electrification spur orders for galvanized roofing and agrivoltaic structures, though price sensitivity favors local polyester formulations.

North America remains technology-focused, emphasizing regulatory compliance and durability over sheer growth. The coil coatings market size in the United States benefits from a remodeling boom and tax incentives for energy-efficient roofs. Stricter VOC caps from the South Coast Air Quality Management District accelerate high-solids adoption and drive capital upgrades among West Coast lines. Canada’s colder climate elevates insulation panels coated with flexible polyurethanes designed to withstand freeze-thaw cycles, while Mexico’s proximity to United States OEMs secures appliance backlog stability under USMCA (United States-Mexico-Canada Agreement) trade provisions.

Europe’s mature landscape values sustainability badges and traceability. Carbon-border adjustments and extended producer-responsibility schemes push mills and coaters to document cradle-to-gate emissions, rewarding suppliers with verified EPDs. Germany’s refurbishment grants promote cool-roof retrofits that favor PVDF, France’s agrivoltaic subsidies accelerate demand for corrosion-resistant framing, and the Nordics continue to specify matte polyesters for standing-seam metal roofs in residential constructions. South America and the Middle East & Africa contribute modest volumes but outsize potential; Brazil’s coastal resorts mandate anti-salt-spray coatings, while Gulf logistics hubs commission color-fast warehouse cladding amid extreme UV exposure. The overall geography spread insulates the coil coatings market against single-region shocks.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Coil Coatings market is fragmented. Supply security and technical service are decisive tender criteria. Major OEMs mandate on-site audits, accelerated weathering tests, and digital color formulation libraries. Smaller entrants without global field-service teams struggle to break specification locks. Nevertheless, white-space opportunities persist in PFAS-free fluoropolymers, high-recycled-content backers, and radiation-cure platforms that halve energy draw. Partnerships with line-equipment makers and chemical pretreatment specialists can unlock turnkey packages for emerging-market coaters eyeing compliance parity, reinforcing competitive moats for integrated suppliers inside the coil coatings market.

Coil Coatings Industry Leaders

-

Beckers Group

-

Akzo Nobel N.V.

-

PPG Industries, Inc.

-

The Sherwin-Williams Company

-

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2024: Beckers Group announced the opening of its FutureLab in Liverpool, United Kingdom. This facility is designed to drive the development of next-generation coil coatings. The new building effectively doubles the capacity of the company's long-term development department, strengthening its efforts to produce more sustainable coatings.

- August 2024: AkzoNobel Coil Coatings announced the launch of FIDURA, a versatile coil coating system tailored for the construction sector. FIDURA is designed for diverse applications, including roofing, walls, facades/cladding, rainwater systems, garage doors, and roller shutters.

Global Coil Coatings Market Report Scope

Coil coatings are used for aluminum and steel coils or sheets and applied on automated lines. The coated metal coil or sheet is subsequently supplied to equipment manufacturers to be formed into a range of ready-painted parts. The coil coatings market is segmented based on resin type, end-user industry, and geography. The market is segmented by resin type into polyester, polyvinylidene fluorides (PVDF), polyurethane (PU), plastisols, and other resin types. The market is segmented into building and construction, industrial and domestic appliances, transportation, furniture, and other end-user industries by end-user industry. The report offers market size and forecasts for 15 countries across major regions. For each segment, market sizing and forecasts are based on revenue (USD) for all the above segments.

By Resin Type

| Polyester |

| Polyvinylidene Fluoride (PVDF) |

| Polyurethane (PU) |

| Plastisols |

| Other Resin Types |

By End-user Industry

| Building and Construction |

| Industrial and Domestic Appliances |

| Transportation |

| Furniture |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Polyester | |

| Polyvinylidene Fluoride (PVDF) | ||

| Polyurethane (PU) | ||

| Plastisols | ||

| Other Resin Types | ||

| By End-user Industry | Building and Construction | |

| Industrial and Domestic Appliances | ||

| Transportation | ||

| Furniture | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Coil Coatings market in 2025?

The coil coatings market size stands at USD 3.63 billion in 2025.

What is the expected CAGR for coil-applied finishes through 2030?

Revenue is projected to advance at a 3.32% CAGR over 2025-2030.

Which resin dominates sales today?

Polyester formulations hold 67.56% share owing to cost efficiency and versatile performance.

Why is PVDF gaining momentum?

PVDF grows fastest at 3.68% CAGR because it meets long-term color-retention and cool-roof requirements in commercial façades.

Which region leads demand?

Asia-Pacific leads with 50.35% of global revenue thanks to its large appliance, automotive, and construction base.

Page last updated on: