Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 345.02 Million |

| Market Size (2031) | USD 463.99 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

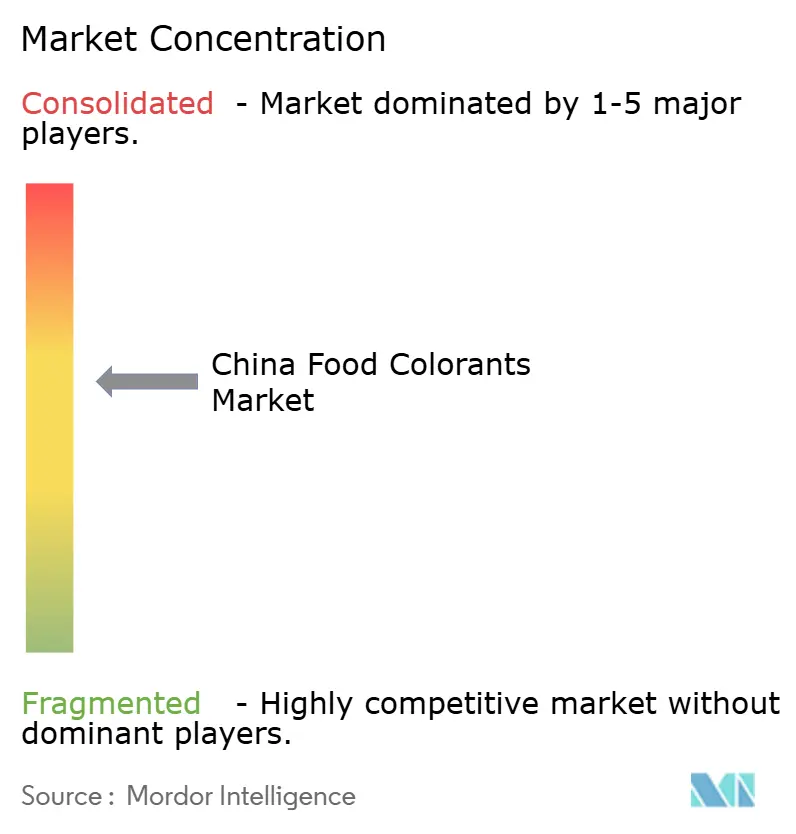

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Food Colorants Market Analysis by Mordor Intelligence

China Food Colorants Market size in 2026 is estimated at USD 345.02 million, growing from 2025 value of USD 325.12 million with 2031 projections showing USD 463.99 million, growing at 6.12% CAGR over 2026-2031. Rapid urbanization and increasingly busy lifestyles are fueling demand for processed, convenience, and ready-to-eat foods. This trend emphasizes the need for consistent and visually appealing products to convey freshness and flavor in a competitive packaged-food market. Simultaneously, growing consumer awareness of health and ingredients is prompting manufacturers to shift from synthetic additives to natural, plant-based, or clean-label color solutions that maintain performance under industrial processing conditions. This transition is further supported by regulatory developments, including China's standardization of plant-based coloring foods and broader food safety policies, which define acceptable coloring ingredients and encourage advancements in the stability and functionality of naturally derived pigments.

Key Report Takeaways

- By product type, Synthetic Color controlled 56.03% of the China food colorants market share in 2025, whereas Natural Color is forecast to expand at an 8.52% CAGR through 2031.

- By color, Red shades captured 33.00% revenue in 2025, while Blue pigments are projected to rise at a 8.78% CAGR to 2031.

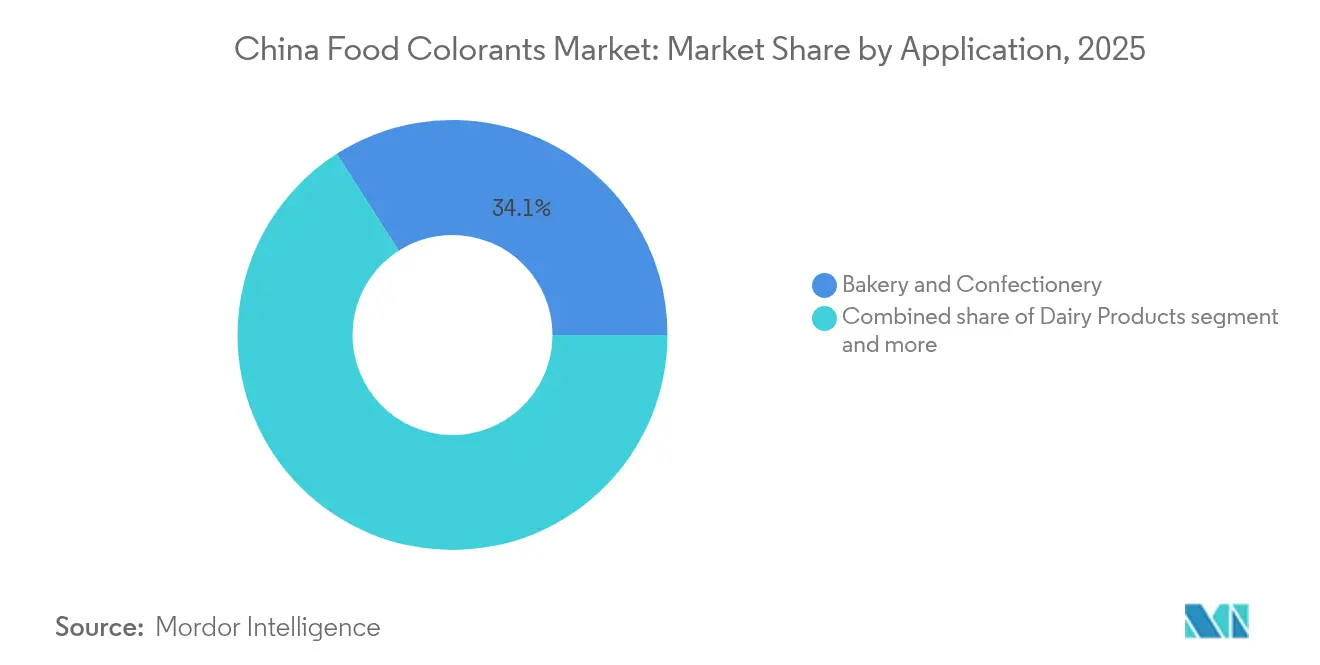

- By application, Bakery and Confectionery led with 34.05% of 2025 sales, yet Beverages are poised for an 8.19% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Food Colorants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for processed, convenience and ready-to-eat foods | +1.2% | National, with concentration in Tier-1 and Tier-2 cities (Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu) | Medium term (2-4 years) |

| Increasing demand for organic and clean-label ingredients | +1.6% | National, with early adoption in coastal provinces (Zhejiang, Jiangsu, Guangdong) | Long term (≥ 4 years) |

| Growth in dairy, and meat/seafood applications for aesthetic appeal | +0.9% | National, with spillover to dairy-producing regions (Inner Mongolia, Heilongjiang) | Medium term (2-4 years) |

| Regulatory tailwinds expanding natural color approvals | +0.8% | National, enforced by NMPA and provincial food safety bureaus | Short term (≤ 2 years) |

| Rising popularity of vegan and plant-based products | +0.7% | Tier-1 cities with early spillover to Tier-2 urban centers | Medium term (2-4 years) |

| Technological advancements in colorant extraction | +0.6% | Concentrated in Zhejiang, Yunnan, Jiangsu production hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for processed, convenience and ready-to-eat foods

The increasing consumption of processed, convenience, and ready-to-eat foods in China is a significant driver of the food colorants market. As urban lifestyles grow busier and dual-income households become more common, consumers are turning to packaged snacks, instant meals, chilled ready dishes, and ready-to-drink beverages. These products rely on colorants for flavor signaling and enhancing shelf appeal. Food manufacturers use colorants to standardize product appearance across large-scale production, mask natural ingredient variability, and ensure products appear fresh and appealing even after extended storage and distribution. The expansion of modern retail formats, convenience stores, and online grocery platforms further emphasizes the importance of visually appealing packaging and product colors, as many purchases are made quickly and impulsively. In this context, both synthetic and natural colorants are experiencing increased demand, while premium convenience products, such as better-for-you snacks and functional ready meals, are driving opportunities for clean-label, plant-based color solutions.

Increasing demand for organic and clean-label ingredients

The growing demand for organic and clean-label ingredients is a key driver of the China Food Colorants Market, as consumers increasingly focus on ingredient transparency and naturalness. Clean-label expectations are encouraging brands to replace synthetic dyes with colorants derived from fruits, vegetables, plants, and algae, which can be described in simple and recognizable terms. This trend is further supported by regulatory developments, such as China’s new standard for plant-based coloring foods. This regulation classifies many natural colorants as food ingredients rather than additives, promoting transparent labeling practices. The broader green food movement highlights the scale of this preference. According to the China Green Food Development Center, sales of certified green food in China reached approximately CNY 609.78 billion in 2024, demonstrating consumers' willingness to invest in safer and more sustainable products [1]Source: China Green Food Development Center (CGFDC), "Green food domestic sales value in China", greenfood.org.cn. As food and beverage manufacturers adapt to these trends, the demand for natural and organic color solutions continues to rise, benefiting suppliers of clean-label food colorants.

Growth in dairy, and meat/seafood applications for aesthetic appeal.

Growth in dairy and meat/seafood applications is a significant driver for China’s food colorants market, as these categories increasingly depend on visual appeal to convey freshness, flavor, and quality to consumers. In the dairy segment, colorants are extensively used in products such as flavored milks, yogurts, drinking yogurts, ice creams, and cheese snacks. These colorants help create consistent and appealing shades that align with fruit or dessert flavors while also aiding in the differentiation of premium products in competitive retail environments. The scale of the dairy industry further enhances this impact. According to the National Bureau of Statistics of China, cow’s milk output reached approximately 40.8 million metric tons in 2024, providing a substantial and growing foundation for colorant usage in value-added dairy products [2]Source: National Bureau of Statistics of China, "Cow's milk production volume in China", stats.gov.cn. As manufacturers introduce more indulgent and functional dairy offerings, often aimed at children and young adults, the demand for stable and vibrant colors that can withstand heat treatment and cold-chain distribution continues to increase.

Regulatory tailwinds expanding natural color approvals

Regulatory developments are increasingly facilitating the growth of natural food colorants in China, particularly with the introduction of the industry standard QB/T 6500‑2024 Coloring Food Ingredients for the Food Industry. Effective from May 1, 2025, this standard requires that coloring food ingredients be derived from fruits, vegetables, plants, or algae commonly consumed as food and processed solely through physical methods, excluding synthetic solvents and artificial colorants. By classifying these preparations as food ingredients rather than additives, the regulation promotes cleaner and more transparent label declarations. This clarification addresses previous ambiguities regarding natural claims and provides both domestic and multinational manufacturers with a clear framework for developing and marketing plant-based color solutions. Consequently, the new standard serves as a structural driver of demand for natural colorants, encouraging a shift away from synthetic alternatives and accelerating investments in compliant extraction, processing, and application capabilities within the Chinese food colorants market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of natural colorants | -0.5% | National, with acute pressure in price-sensitive segments (snacks, cereals) | Medium term (2-4 years) |

| Limited color palette / shade range with natural colorants | -0.3% | National, affecting specialty applications (metallic, black, neon shades) | Long term (≥ 4 years) |

| Climate-driven crop supply volatility | -0.4% | Regional, concentrated in Yunnan (spirulina), Xinjiang (paprika), Inner Mongolia (safflower) | Short term (≤ 2 years) |

| Limited innovation pace in synthetic colorants | -0.2% | National, with spillover to export-dependent producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of natural colorants

The high cost of natural colorants serves as a significant restraint on the China Food Colorants Market. Plant-based pigments, such as anthocyanins, carotenoids, and spirulina extracts, require more complex cultivation, extraction, and purification processes compared to synthetic dyes, leading to higher production costs. Additionally, natural colorants often exhibit lower tinting strength and narrower stability ranges, necessitating higher dosages or advanced formulation technologies to achieve comparable visual effects. These factors result in natural colorants being more expensive per functional unit in many applications, particularly in cost-sensitive mass-market products. Consequently, some food and beverage manufacturers in China are hesitant to fully transition from synthetic to natural alternatives, which slows the adoption of clean-label products despite strong consumer demand and regulatory support.

Limited color palette / shade range with natural colorants

The high cost of natural colorants serves as a significant restraint on the China Food Colorants Market. Plant-based pigments, such as anthocyanins, carotenoids, and spirulina extracts, require more complex cultivation, extraction, and purification processes compared to synthetic dyes, leading to higher production costs. Additionally, natural colorants often exhibit lower tinting strength and narrower stability ranges, necessitating higher dosages or advanced formulation technologies to achieve comparable visual effects. These factors result in natural colorants being more expensive per functional unit in many applications, particularly in cost-sensitive mass-market products. Consequently, some food and beverage manufacturers in China are hesitant to fully transition from synthetic to natural alternatives, which slows the adoption of clean-label products despite strong consumer demand and regulatory support.

Segment Analysis

Growing demand for processed, convenience and ready-to-eat foods

Synthetic colorants hold the largest share of the China Food Colorants Market, driven by their long-standing use, cost-effectiveness, and technical stability across diverse applications. In 2025, these products accounted for 56.03% of the market, reflecting their significant presence in high-volume segments such as beverages, snacks, and confectionery. Their strong tinting strength and lower dosage requirements remain attractive to manufacturers aiming to optimize formulation costs. Additionally, established production infrastructure and robust supply chains further support their dominant position. However, this leadership is increasingly under pressure due to heightened regulatory scrutiny and growing concerns about consumer health. Consequently, while synthetic colors are expected to remain important in the short term, their market share is anticipated to decline as natural alternatives gradually gain traction.

Natural colors represent the fastest-growing segment in the China Food Colorants Market, with a projected CAGR of approximately 8.52% between 2026 and 2031. This growth is fueled by rising demand for clean-label, plant-based, and minimally processed ingredients, particularly in beverages, dairy, and confectionery. Regulatory initiatives, such as China’s emphasis on plant-based coloring foods, are accelerating adoption by clarifying standards and encouraging reformulation away from synthetic options. Simultaneously, advancements in extraction and stabilization technologies are enhancing the performance and shelf life of natural pigments, making them more viable for challenging applications. As these solutions become increasingly competitive in terms of cost and functionality, they are progressively eroding the market share of synthetic colorants.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Color: Blue Hues Surge on Beverage Innovation

Red colorants hold the largest share of the China Food Colorants Market, accounting for 33.00% of the total market value in 2025. This dominance is attributed to their extensive use in categories such as meat products, processed seafood, confectionery, and fruit-flavored beverages, where red and reddish-brown tones enhance visual appeal. Both synthetic red colorants and natural options, such as anthocyanins and beet-based pigments, contribute to this leadership, offering manufacturers flexibility across various price points and labeling preferences. The established role of red shades in traditional Chinese cuisine, festive products, and premium gifting items further supports their widespread adoption. Additionally, ongoing product launches in red-colored candies and bakery fillings are expected to sustain significant baseline demand. While other color segments are gaining traction, red colorants are projected to remain the cornerstone of the market in the medium term.

Blue colorants represent the fastest-growing segment in the China Food Colorants Market, with a projected CAGR of approximately 8.78% from 2026 to 2031, the highest among all color categories. This growth is primarily driven by the increasing adoption of spirulina-derived phycocyanin, a plant-based, label-friendly alternative to traditional synthetic blue pigments. Beverage manufacturers are leveraging these natural blue colorants to achieve striking visual differentiation while aligning with clean-label trends. The shift away from titanium dioxide and certain synthetic pigments, due to safety concerns and consumer perception, is further encouraging the exploration of new blue color systems in beverages and confectionery. Advances in the stability and processing tolerance of phycocyanin are expanding its application potential across various product categories.

By Application: Beverages Accelerate on RTD and Functional Formats

The bakery and confectionery segment currently holds the largest share in the China Food Colorants Market, accounting for 34.05% of market value in 2025. This dominance is attributed to the extensive use of colorants in products such as cakes, pastries, filled breads, sugar confectionery, and chocolate decorations, where visual appeal significantly influences consumer purchasing decisions. The segment encompasses both industrially produced packaged goods and a substantial out-of-home bakery channel, driving high-volume demand for a wide range of reds, yellows, and mixed shades. In July 2024, China submitted a draft National Food Safety Standard for Cakes and Bread to the WTO (G/SPS/N/CHN/1304), indicating increased regulatory scrutiny of ingredients, including colorants . This regulatory development is expected to encourage manufacturers to adopt stricter compliance measures and potentially shift toward more natural or standardized coloring systems over time.

The beverages segment is the fastest-growing application area for food colorants, with usage projected to grow at a CAGR of approximately 8.19% between 2026 and 2031. This growth is driven by the expanding range of ready-to-drink (RTD) teas, functional drinks, energy beverages, and carbonated soft drinks, which rely on vibrant colors for product differentiation and flavor signaling. Brand owners are increasingly reformulating their products to incorporate natural and plant-based colorants, particularly in premium and health-focused beverages, contributing to value growth. Ingredients such as spirulina-derived blues and anthocyanin-based reds are being adopted to create more complex shades in both clear and opaque drink formulations. Additionally, rising disposable incomes in urban areas and the growing popularity of café-style and bubble-tea concepts are boosting demand for visually appealing beverages that require advanced color systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China's food colorants market is heavily concentrated along the eastern coastal belt, with Zhejiang, Jiangsu, and Guangdong serving as key manufacturing and trading hubs. These provinces benefit from dense clusters of food and beverage processors, export-oriented ingredient manufacturers, and well-developed logistics networks. This combination ensures consistent demand for both natural and synthetic color systems. Additionally, proximity to major ports such as Ningbo, Shanghai, and Shenzhen facilitates the import of raw materials and the export of finished products, further solidifying their dominance in national production and distribution. Local governments in these regions actively support value-added food and specialty chemical industries, encouraging investments in colorant production capacity and application laboratory

Inland provinces like Sichuan and Henan are increasingly gaining prominence in synthetic colorant production, particularly for azo dyes and other bulk commodity pigments. These regions offer lower labor and land costs, along with established chemical industrial parks that provide utilities and shared treatment infrastructure tailored to dye and intermediate manufacturing. This shift diversifies China's supply base away from coastal areas while maintaining competitive production costs for downstream users in snacks, bakery, and instant foods. However, stricter environmental and safety compliance requirements are prompting inland producers to upgrade their processes and invest in cleaner technologies. This trend is gradually raising the technological entry barriers, favoring larger, well-capitalized synthetic colorant manufacturers capable of meeting national standards and catering to branded customers.

On the demand side, Tier-1 cities such as Beijing, Shanghai, Guangzhou, and Shenzhen continue to drive end-use consumption and premium product launches in the food colorants market. These metropolitan areas, characterized by high disposable incomes, dense modern retail networks, and advanced foodservice channels, support the early adoption of clean-label, natural, and visually differentiated products that rely on advanced color systems. However, Tier-2 and Tier-3 cities are now experiencing faster growth, driven by the expansion of e-commerce platforms and social-commerce channels. These developments are increasing access to premium snacks, beverages, and bakery items beyond the coastal megacities. As a result, national brands and multinational manufacturers are focusing on securing long-term, high-specification colorant supplies, often favoring vertically integrated producers with control over pigment cultivation or key intermediates.

Competitive Landscape

China’s food colorants market is highly fragmented, with numerous regional manufacturers supplying both synthetic dyes and emerging natural pigments across various provinces. Many small and mid-sized firms focus on commodity azo dyes and standard blends, competing primarily on price and proximity to local food processors. This competitive environment exerts significant price pressure in lower-specification segments and complicates efforts by downstream brands to ensure consistent quality and regulatory compliance across suppliers. However, domestic players with advanced Research and Development (R&D) capabilities and regulatory expertise are beginning to stand out by offering cleaner production processes and customized color solutions. As a result, factors such as scale, technical service, and reliability are becoming increasingly important alongside basic production capacity.

Multinational ingredient companies, including DSM-Firmenich, Dohler, and Givaudan, are addressing the market's fragmentation by expanding their local presence in China. These companies are establishing application laboratories and powder-blending facilities near major food and beverage hubs, enabling the co-development of formulations tailored to Chinese preferences for taste, color, and processing conditions. These facilities facilitate rapid prototyping for applications in beverages, bakery, confectionery, and dairy, helping brand owners accelerate product launches and reformulations toward natural and clean-label solutions.

In addition, multinational players are investing in or partnering for local extraction, concentration, and distribution of plant-based pigments to reduce dependence on imported intermediates. This integrated approach helps stabilize input costs, enhances batch-to-batch consistency, and ensures compliance with evolving Chinese standards for coloring foods and additives. Over time, the combination of technical service capabilities and partial vertical integration is expected to strengthen the competitive position of multinational companies in the higher-value segments of China’s fragmented food colorants market.

China Food Colorants Industry Leaders

-

Givaudan S.A.

-

DSM-Firmenich AG

-

Sensient Technologies Corporation

-

Dohler GmbH

-

Kalsec Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: IFF has opened an innovation center in Shanghai. The 16,000 square-meter facility, named the Shanghai Creative Center, is the company's largest in Asia. The center is designed to support the development of innovative solutions across IFF's portfolio in China and the Greater Asia market.

- March 2024: BASF participated in the Food Ingredients China (FIC) 2024 trade show held at the National Exhibition and Convention Center in Shanghai. The company remains committed to providing high-quality, safe, and sustainable ingredients that address the changing demands of consumers.

China Food Colorants Market Report Scope

The China Food Colorants Market is segmented by Type into Natural Color and Synthetic Color. The market is segmented by Application into Beverages, Dairy & Frozen products, Bakery, Meat and Seafood, Confectionery, and Others.

By Product Type

| Natural Color | Anthocyanins |

| Carotenoids | |

| Curcumin | |

| Carmine | |

| Spirulina | |

| Other Types | |

| Synthetic Color |

By Color

| Blue |

| Green |

| Red |

| Yellow |

| Purple |

| Orange |

| Pink |

| Others |

By Application

| Bakery and Confectionery |

| Dairy Products |

| Snacks and Cereals |

| Beverages |

| Others |

| By Product Type | Natural Color | Anthocyanins |

| Carotenoids | ||

| Curcumin | ||

| Carmine | ||

| Spirulina | ||

| Other Types | ||

| Synthetic Color | ||

| By Color | Blue | |

| Green | ||

| Red | ||

| Yellow | ||

| Purple | ||

| Orange | ||

| Pink | ||

| Others | ||

| By Application | Bakery and Confectionery | |

| Dairy Products | ||

| Snacks and Cereals | ||

| Beverages | ||

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What growth rate is forecast for the China food colorants market between 2026 and 2031?

The market is expected to register a 6.12% CAGR, climbing from USD 345.02 million in 2026 to USD 463.99 million in 2031.

Which pigment type is growing fastest in China’s food sector?

Spirulina-derived blue pigments are projected to post the highest CAGR at 8.78% through 2031 as beverage brands search for label-friendly blues.

How will new Chinese regulations affect natural colorant suppliers?

GB 2760-2024 and the Coloring Food Ingredients standard require solvent-free extraction and full traceability, allowing certified vendors to charge price premiums while pushing non-compliant plants toward exit or consolidation.

Which regions host the bulk of China’s pigment production?

Zhejiang, Jiangsu, and Guangdong provinces house roughly 54.62% of capacity, benefitting from export ports, integrated ingredient clusters, and early regulatory audits.