Regulation as a Market Divider

The EU Artificial Intelligence Act has moved from policy draft to business reality. What began as a regional compliance exercise is now reshaping global Artificial Intelligence strategy, forcing companies to decide whether to treat governance as a burden or a differentiator.

For CEOs and boards, the question is no longer if compliance is required but how to align it with growth.

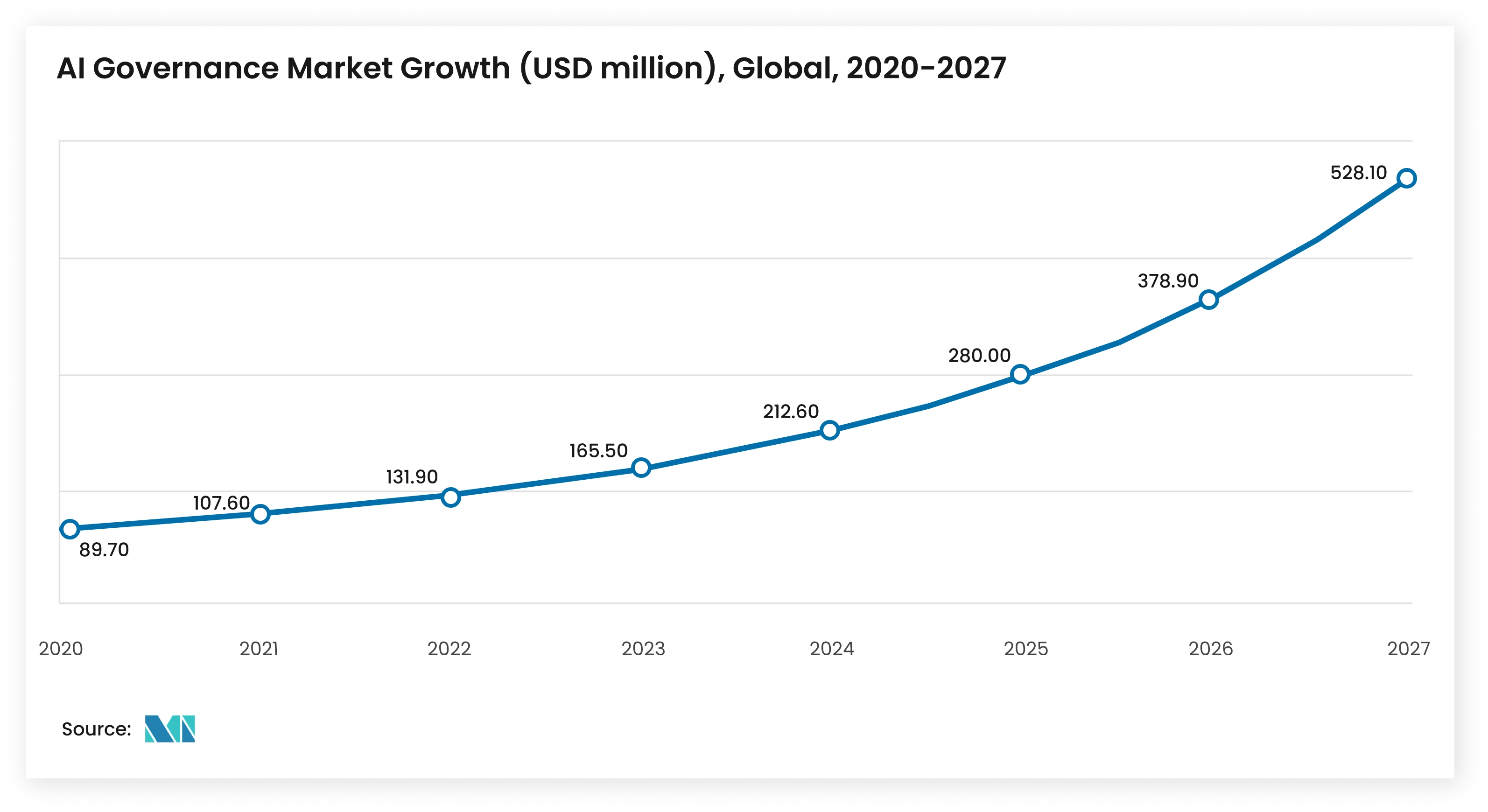

The Global AI Governance market is estimated at USD 0.34 billion in 2025 and is projected to grow at 28.80% CAGR, touching USD 1.21 billion by 2030. This acceleration underscores a structural shift: regulation is not slowing the Artificial Intelligence economy; it is building its infrastructure of trust.

The Inflection Point: When Regulation Becomes Strategy

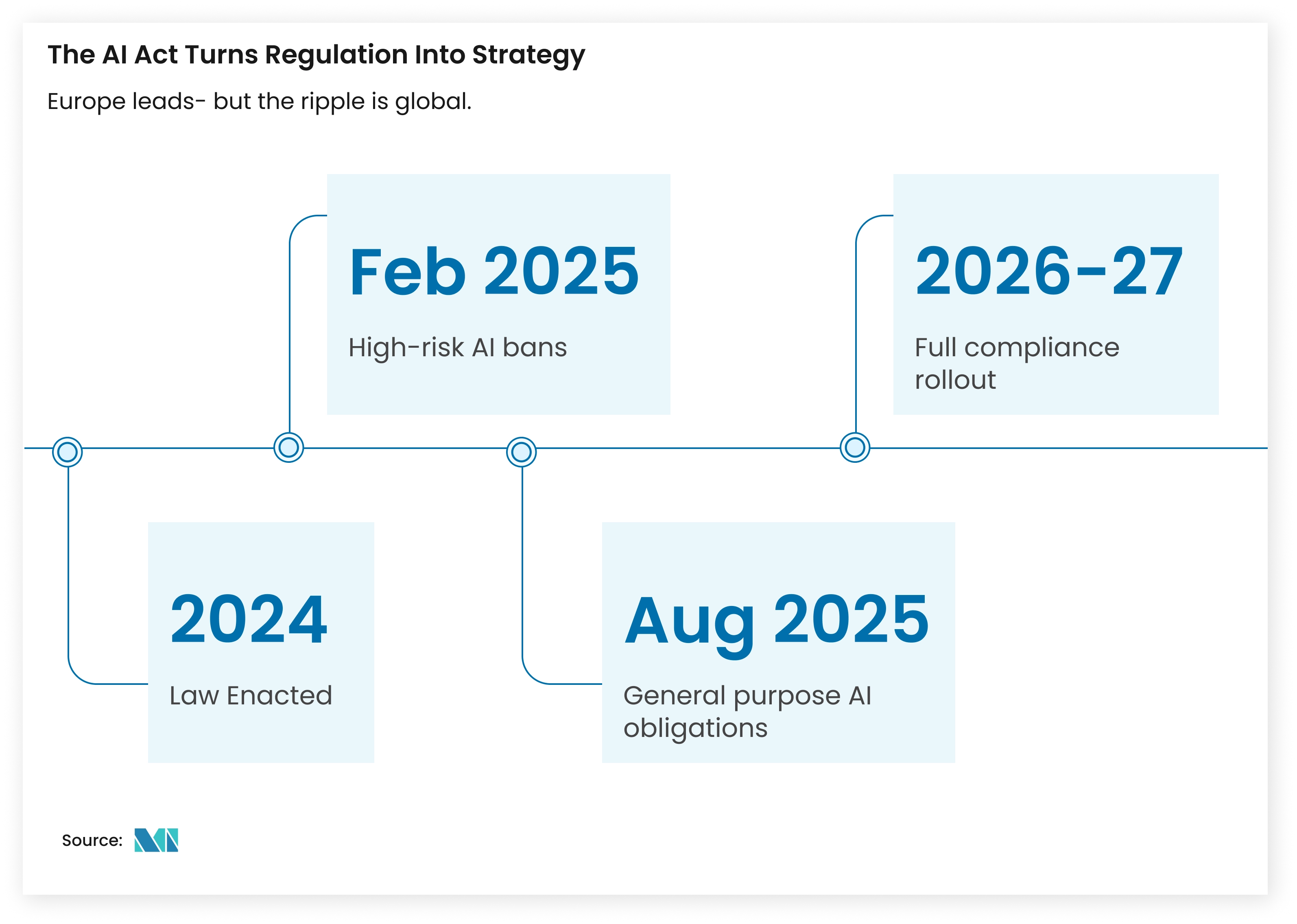

The EU AI Act came into force on 1 August 2024, marking the beginning of its phased implementation across the European Union. But the real action lies ahead.

| Date | Key Milestone |

| 2 February 2025 | Prohibited systems (e.g., social scoring, real-time biometric ID) banned |

| 2 August 2025 | Obligations for general-purpose AI (GPAI) models begin |

| 2026–27 | High-risk sector compliance deadlines |

Source: EU AI Act

Although the law is EU-centric, its impact is global. Firms outside Europe that deploy, import, or service EU customers will feel the ripple. What was once “just” a regulatory cost is becoming a strategic axis: trust, scale, and market access.

The Boardroom Frictions Defining AI Strategy

Executives are confronting three interlocking tensions that will define how AI investments evolve.

| Strategic Tension | Fast-Mover Approach | Laggard Risk |

| Speed vs Certainty | Embed governance during development, not after. | Market entry delays and costly retrofits. |

| Control vs Collaboration | Build shared compliance frameworks with partners. | Isolated audit burden, vendor dependency. |

| Cost vs Advantage | Treat governance maturity as proof of operational excellence. | Pure cost-center approach, margin pressure. |

Source: Mordor Intelligence

A. Clarity vs. Speed

Firms face a choice: pause innovation until policy uncertainty resolves, or push ahead and retrofit controls.

B. Control vs. Collaboration

The EU AI Act’s “provider/deployer” liability model means that every API, dataset, and partner model must be traced. Large-scale industrials (aircraft, automated systems) are forming compliance consortia to share audit burden and data lineage responsibilities.

C. Compliance vs. Competitiveness

If governance is seen purely as cost, product cycles slow; if ignored, brand and regulatory risk rise. Leading firms are starting to view governance maturity itself as a form of operational maturity and a signal to customers, partners, and investors.

Market Evidence: How Governance Is Becoming a Differentiator

The shift from compliance burden to competitive advantage is already visible in measurable data and strategic behavior across industries.

1. A Market for Trust

AI governance is emerging as one of the fastest-growing service ecosystems in Europe. Consulting and audit services are projected to expand from USD 371.04 billion in 2025 to USD 469.28 billion by 2030, driven by financial institutions and industrial firms seeking verifiable AI systems.

2. The Preparedness Gap

This demand is running far ahead of supply. According to a 2024 survey of European financial executives found that 90% of institutions use AI, but only 9% feel equipped to meet the AI Act’s standards.

3. Early Leadership Signals

- Regulatory Partnerships: The Bank of England’s 2024 collaboration with technology providers to define AI governance frameworks highlights how regulators are favoring proactive, cooperative engagement.

- Transparency Reporting: Firms publishing explainability and fairness reports in 2024 saw stronger procurement outcomes in finance and healthcare.

- Institutional Momentum: Large European enterprises with embedded governance frameworks now report faster product approval cycles and improved investor sentiment.

- Capital Market Validation: Firms with public AI governance disclosures achieved average market-cap gains of 4–5 % within two quarters.

4. Sector Divergence

- Governance leadership is not evenly distributed.

- Regulated sectors, finance, healthcare, manufacturing, are scaling faster because the path to compliance is clearer.

- Meanwhile, unregulated verticals are lagging, widening the gap in trust-based competitiveness.

How Global Leaders Are Re-Architecting for the AI Act

| Sector | Key Players | Strategic Adaptation | Market Signal |

| Technology | Microsoft, Google, Meta | Building cloud-based governance platforms and transparency dashboards for EU deployments. | Compliance-by-design becomes a developer advantage. |

| Industrial & Manufacturing | Siemens, ABB, Bosch | Embedding audit trails in predictive-maintenance systems. | Governance equals reliability in B2B sales. |

| Financial Services | Major European Banks | Aligning AI frameworks with Basel and AML principles. | Regulatory leadership becomes capital advantage. |

| Healthcare & Life Sciences | Philips, Roche, Siemens Healthineers | Tracking diagnostic AI lineage to meet medical-device standards. | Data provenance redefined as patient safety. |

| Automotive & Mobility | Volkswagen, Volvo, Mercedes-Benz | Certifying autonomous-system models for EU safety criteria. | Trusted automation becomes brand premium. |

Source: Mordor Intelligence

The Next 12 Months: What Will Separate Fast-Followers from Leaders

What to watch for in the immediate horizon, not as predictions, but as strategic markers:

- Regulatory Convergence Acceleration: The Brussels Effect is expanding. Similar AI governance frameworks emerging in Singapore, Canada, and select US jurisdictions create global standardization opportunities for early adopters.

- Trust Infrastructure Competition: The real competitive battleground is shifting to traceability, audit capabilities, and transparency documentation, not just model accuracy. Firms building these capabilities now gain sustainable advantages.

- Sector Performance Divergence: Regulated industries (financial services, healthcare, manufacturing) are adopting AI governance faster than less-regulated sectors, creating widening competitive gaps.

- Capital Market Integration: AI governance capabilities are becoming visible metrics in enterprise evaluation, similar to ESG frameworks. Institutional investors increasingly require governance documentation for AI-dependent business models.

Executives are moving from asking “Can we comply?” to “How do we lead through compliance?”

Executive Takeaways

- Governance is now the license to scale in AI-driven industries.

- Procurement and investors increasingly reward transparency over speed.

- The EU AI Act is shaping a trust-based economy, not just a compliance landscape.

Closing Reflection

The Act doesn’t decide who can innovate. It decides who can be trusted to. As AI becomes the backbone of global operations, compliance will evolve from a legal metric to a leadership trait. The companies that master both innovation and integrity will likely own the future of intelligent systems.

Want deeper insights on how AI Act compliance and regulation are transforming global AI strategy? Explore our latest AI Governance Market Report.