Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

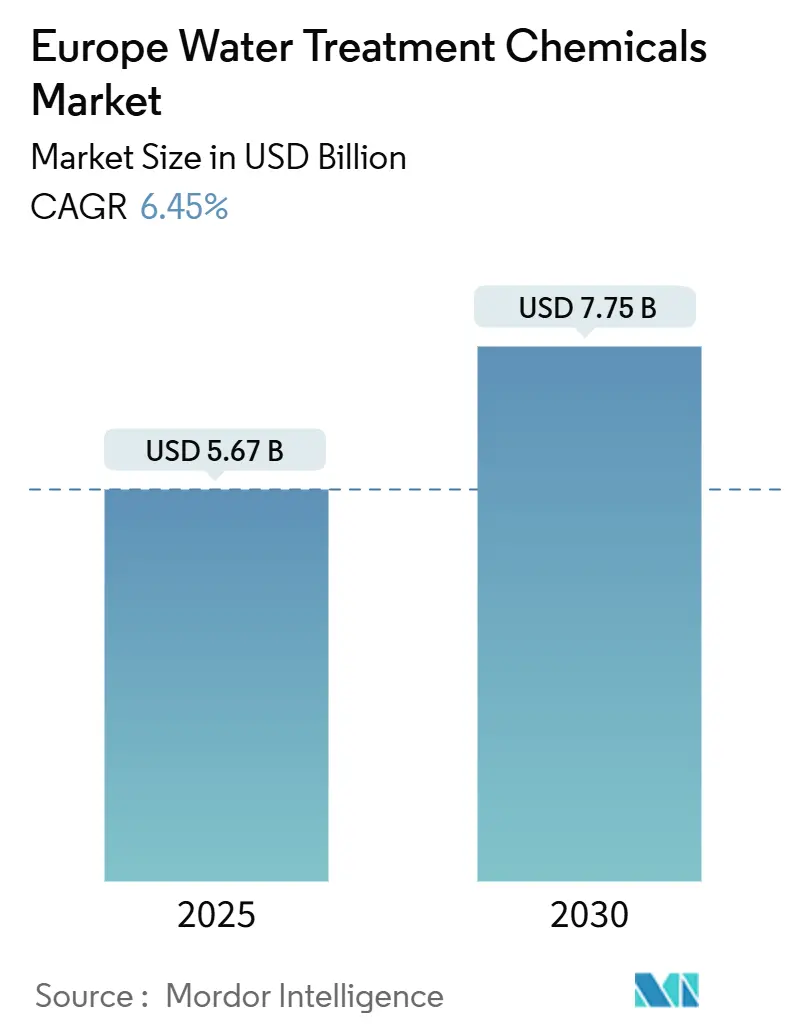

| Market Size (2025) | USD 5.67 Billion |

| Market Size (2030) | USD 7.75 Billion |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

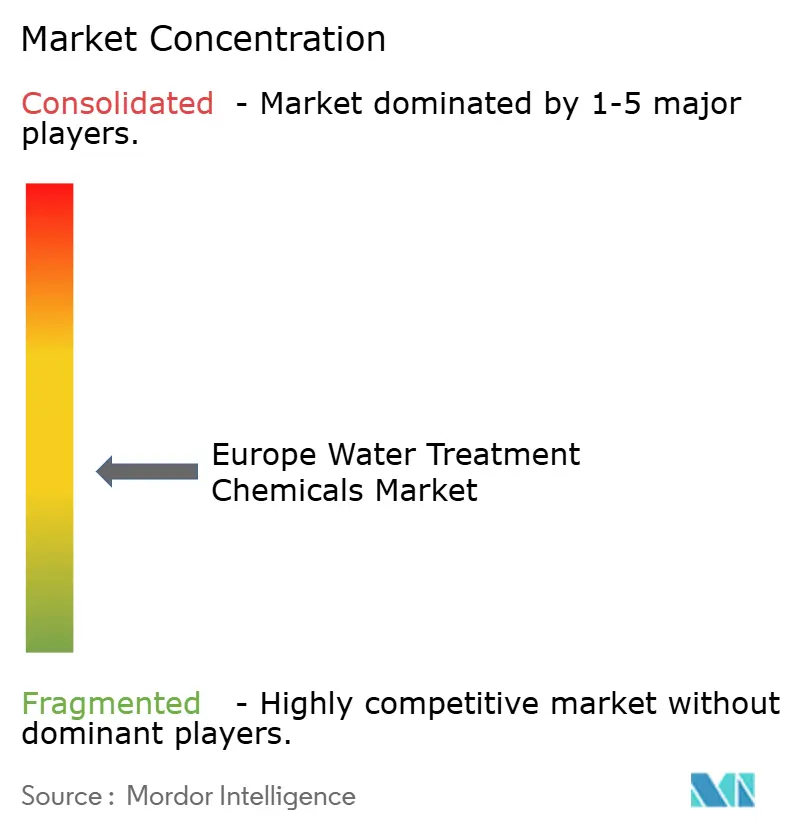

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Water Treatment Chemicals Market Analysis by Mordor Intelligence

The European Water Treatment Chemicals Market size is estimated at USD 5.67 billion in 2025, and is expected to reach USD 7.75 billion by 2030, at a CAGR of 6.45% during the forecast period (2025-2030). Rising penalties for discharge non-compliance, industrial decarbonization that multiplies process-water loops, and multibillion-euro municipal upgrade programs simultaneously expand addressable demand across utilities and heavy industry. Germany retains the largest national revenue base, yet the Nordic countries add volume the fastest as PFAS, phosphorus recovery, and micropollutant mandates roll out. Segment momentum is already shifting from legacy corrosion and scale inhibitor consumption toward coagulants and flocculants needed for tertiary and quaternary treatment, while ultra-pure water requirements in green-hydrogen electrolysers unlock a new high-purity chemical niche.

Key Report Takeaways

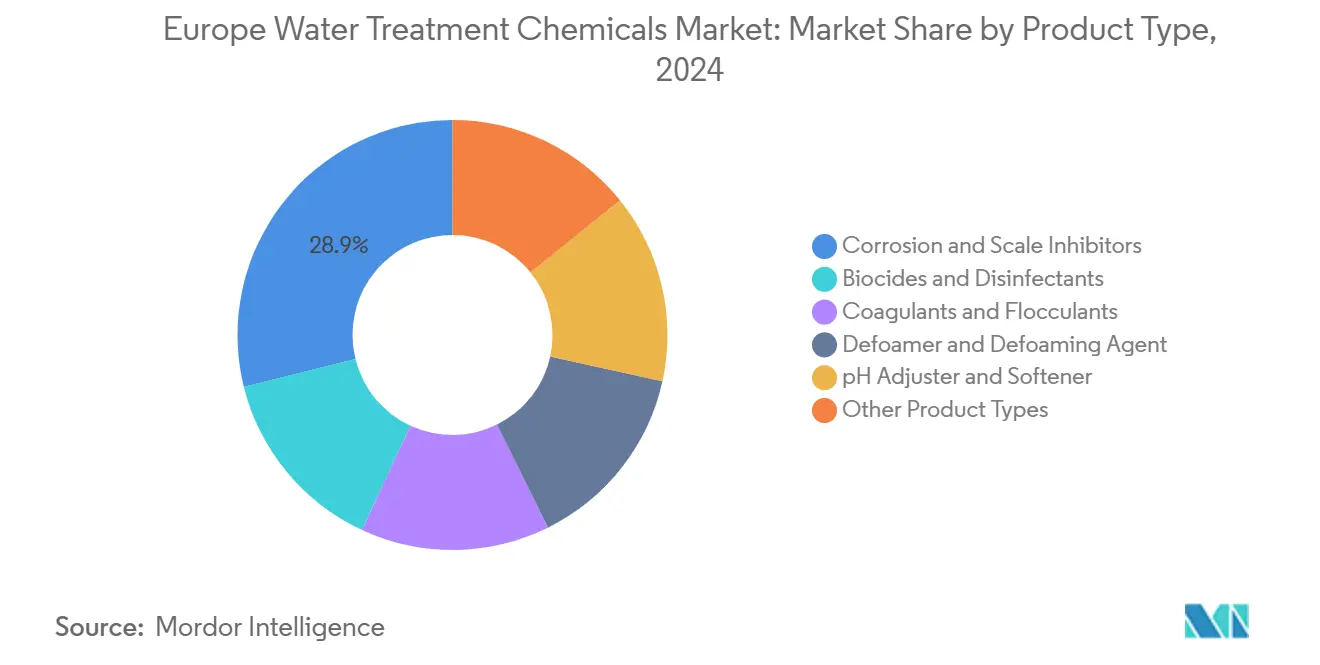

- By product type, corrosion and scale inhibitors led the European water treatment chemicals market with a 28.87% share in 2024. Coagulants and flocculants are projected to grow at a 7.34% CAGR through 2030.

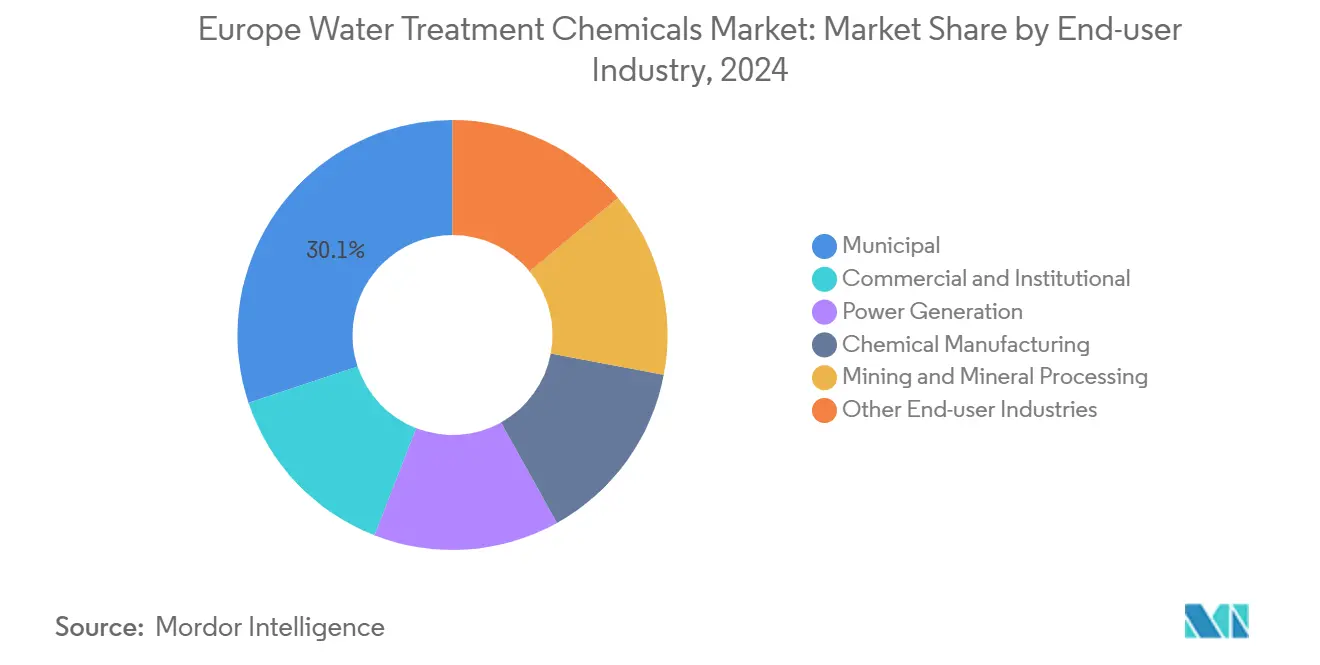

- By end-user, municipal utilities held a 30.12% share of the European water treatment chemicals market in 2024 and are projected to advance at a 7.12% CAGR through 2030.

- By geography, Germany accounted for 28.89% of regional revenue in 2024, while the Nordic countries registered the steepest growth rate of 7.67% through 2030.

Europe Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU discharge and reuse regulations | +1.2% | Belgium, Netherlands, Cyprus | Medium term (2-4 years) |

| EU Water Framework Directive enforcement and penalties | +1.0% | Germany, France, Spain | Short term (≤2 years) |

| Industrial decarbonization boosting process-water demand | +0.9% | Germany, France, Nordic region | Long term (≥4 years) |

| Municipal infrastructure upgrades (AMP8, Cohesion Fund) | +1.3% | UK, Germany, Spain | Medium term (2-4 years) |

| Ultra-pure water for green-hydrogen electrolysers | +0.8% | Germany, Spain, Nordic offshore wind | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Discharge and Reuse Regulations

In 2024, EU infringement actions against Belgium, Cyprus, and the Netherlands introduced daily fines for non-compliance with designated sensitive areas, prompting the rapid retrofitting of tertiary phosphorus removal stages that consume 20–40 mg/L of aluminum or iron coagulants[1]European Commission, “Infringement Procedures Urban Wastewater Treatment Directive,” EC.EUROPA.EU. In a bid to enhance water quality for the Paris Olympics, a project allocated a significant portion of its budget solely to coagulants. Directive 2024/1083 broadens the tertiary mandate to every agglomeration with a population equivalent of more than 10,000 by 2035, doubling the number of facilities that must dose polyaluminum chloride or ferric salts. National agencies, such as Germany’s Umweltbundesamt and Spain’s river-basin authorities, enforce Water Framework targets, thereby accelerating long-term contracts for performance-guaranteed chemical supply.

EU Water Framework Directive Enforcement and Penalties

Germany allocated grants to enhance various plants, with a focus on removing nutrients and micropollutants. Meanwhile, Directive 2024/1203 categorizes illegal discharges as criminal offenses, with potential imprisonment. In response, utilities are securing multi-year contracts with suppliers to ensure the quality of effluent. In Spain, authorities levied fines in 2024, but violations dropped, thanks to the use of real-time phosphorus analyzers for automated coagulant dosing. The upcoming 2027 review is anticipated to halve nitrogen caps, boosting the demand for supplemental carbon sources and pH adjusters throughout Europe.

Industrial Decarbonization Boosting Process-Water Demand

Closed-loop cooling and heat-recovery retrofits increase the risk of scaling and fouling because higher cycles of concentration intensify mineral precipitation. Belgium’s EVEREST lime project lifted antiscalant and biocide usage after boosting water recycling. The Clean Industrial Deal commits heavy industry to reducing CO₂ emissions, forcing steel, cement, and chemicals players to install water recirculation systems that require additional corrosion inhibitors at elevated temperatures. Poland’s industrial sector recorded an increase in corrosion inhibitor purchases in 2024. Bio-based polyaspartate inhibitors are experiencing rapid growth, driven by Kemira’s expansion in sustainable product sales.

Municipal Infrastructure Upgrades (AMP8, Cohesion Fund)

The United Kingdom’s AMP8 plan allocates budgets to treatment chemicals. Anglian Water is installing tertiary phosphorus-removal projects that specify polyaluminum chloride for its lower sludge yield in cold weather. Germany’s KfW grants reimburse capital invested in quaternary pharmaceutical removal, but utilities must pre-treat with coagulants to protect activated-carbon beds. Spain’s drought-resilience program funds desalination and reuse, spurring a dedicated antiscalant and biocide micro-segment.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hazardous nature and handling of hydrazine derivatives | -0.4% | Germany, UK, France | Short term (≤2 years) |

| Raw-material price volatility (alum, caustic, acrylamide) | -0.5% | Pan-European | Medium term (2-4 years) |

| Extended-Producer-Responsibility costs for quaternary treatment | -0.3% | Germany, Netherlands, France | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hazardous Nature and Handling of Hydrazine Derivatives

Utilities, facing the Category 1B carcinogen classification of hydrazine under ECHA rules, are compelled to implement closed-loop dosing, vapor containment, and real-time leak detection. These measures inflate capital costs significantly. In 2024, Germany logged numerous incidents of exposure. As insurance premiums surge, smaller operators are gravitating towards pricier yet safer alternatives, such as carbohydrazide or tannin scavengers. Despite the shift, high-pressure boilers operating above 100 bar continue to rely on hydrazine for swift oxygen removal, underscoring the challenges of a complete transition in power and district heating networks.

Raw-Material Price Volatility (Alum, Caustic, Acrylamide)

From 2022 to 2024, caustic soda prices nosedived significantly. Despite this, a substantial portion of chlor-alkali capacity remains heavily reliant on gas, leaving it vulnerable to energy market shocks. In 2024, aluminum sulfate prices mirrored an uptick in ingot prices, squeezing coagulant supplier margins. Fluctuations in acrylamide prices compel flocculant vendors to renegotiate municipal contracts frequently. SNF revealed that in 2024, raw materials constituted a higher percentage of their cost of goods sold compared to 2022. As a result, utilities are increasingly favoring suppliers with backward integration or robust hedging strategies.

Segment Analysis

By Product Type: Coagulant-Driven Growth Outpaces Legacy Inhibitors

Coagulants and flocculants start from a smaller 2024 base but outpace the broader European water treatment chemicals market at a 7.34% CAGR through 2030, as Directive 2024/1083 doubles the number of facilities that must remove phosphorus to 10 mg/L. Stockholm’s Henriksdal plant reduced sludge and improved capture by switching to polyaluminum chloride, a trend now spreading across cold-climate utilities. Ferric salts gain share in coastal desalination pretreatment due to their superior removal of organics, as evidenced by the Barcelona Llobregat project, which documented a lower membrane-fouling rate after adopting ferric sulfate. Defoamers, pH adjusters, and disinfectants serve narrower niches but grow steadily in food-contact and paper-recycling loops. Corrosion and scale inhibitors are still the largest segment of the European water treatment chemicals market in 2024, accounting for 28.87%. However, nuclear shutdowns and phosphonate restrictions are expected to depress growth, partially offset by inhibitor packages tailored for hydrogen electrolysers. Phosphonate-free polyaspartate blends launched by LANXESS illustrate industry adaptation even at a 10% efficacy trade-off[2]LANXESS, “Polyaspartate Reformulation Product Bulletin 2024,” LANXESS.COM.

Second-order dynamics reveal differential regulatory exposure. The EU Biocidal Products Regulation extended approval timelines for new disinfectants to 36 months, delaying revenue from novel actives. Conversely, niche oxygen scavengers such as erythorbate accelerate in district-heating circuits tolerant of slower kinetics. The European water treatment chemicals market, therefore, tilts toward formulations with demonstrable compliance advantages, even when price premiums reach double digits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Municipal Budgets Anchor Volume and Growth

Municipal utilities account for 30.12% of the 2024 value and are also the fastest-expanding end-user, advancing at a 7.12% CAGR through 2030, driven by AMP8 and Cohesion Fund projects. Thames Water has set aside substantial funds to tackle combined sewer overflow, employing high-charge polymers to minimize solids carryover. German municipalities, which consume large quantities of aluminum-based coagulants annually, still operate below Nordic standards, indicating substantial room for improvement. As coal and nuclear retirements lessen the need for boiler treatments, power generation's share diminishes. Eurostat highlighted a decline in European utility-scale thermal generation from 2022 to 2024, leading to a reduction in spending on inhibitors and biocides. In the chemical sector, BASF’s Ludwigshafen complex invested significantly in corrosion inhibitors and regenerants, supporting its numerous closed-loop operations. Mining operations, like LKAB’s Kiruna mine, utilize high-molecular-weight flocculants for tailings to achieve high solids content. To counter rising tariffs, commercial and institutional sites are increasingly adopting on-site reuse systems, driving demand for monochloramine and peroxyacetic regimes, both approved for food contact.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2024, Germany, buoyed by a federal nutrient-removal program and Berlin’s rollout of fourth-stage ozonation, accounted for 28.89% of total revenue. Export-oriented suppliers in Germany, capitalizing on compliance upgrades in Eastern Europe, exported chemicals and equipment, with Poland and Romania absorbing a notable portion of this. Additionally, as industrial decarbonization gains momentum, the EVEREST project has notably increased antiscalant usage following its recirculation retrofits.

Despite being outside EU regulations, the United Kingdom has pledged substantial funding to AMP8, significantly boosting the trans-Channel chemical trade. Notably, Feralco’s Dutch facility has secured a new multi-year contract, supplying a significant portion of Southern Water’s polyaluminum chloride needs. Meanwhile, France, having invested heavily to clean the Seine ahead of the 2024 Olympics, grapples with an upgrade backlog spanning thousands of municipal plants. In a related stride, Veolia has achieved growth in its European chemical-management services by integrating cloud-connected dosing systems into contracts in France and Spain.

Italy and Spain, which had previously lagged, are now accelerating their tertiary education uptake. Spain's ambitious initiative on desalination and reuse is in dire need of antiscalants, especially those tailored for the high-silica feeds of the Mediterranean. Meanwhile, Italy's Po River basin has set a stringent phosphorus limit across hundreds of plants, unveiling a lucrative market for coagulants. The Nordic nations are witnessing the sharpest growth, boasting a 7.67% CAGR projected through 2030. Stockholm is enforcing PFAS removal using a combination of powdered activated carbon and coagulants, Helsinki is pioneering phosphorus recovery through struvite, and Oslo is harnessing ozonation for pharmaceutical removal. Elsewhere in Europe, nations are reaping the benefits of accession-driven funding. Romania, with its ambitious upgrade scheme targeting numerous plants, currently lacks domestic chemical capacity, paving the way for lucrative import opportunities.

Competitive Landscape

The European water treatment chemicals market is moderately fragmented. Private equity validated the profit resilience of chemical service contracts when Platinum Equity acquired Solenis. Specialists such as Herco Wassertechnik focus on boron-selective resins that can meet electrolyser specifications, which command premiums. Technology bifurcation widens: advanced utilities adopt cloud-controlled dosing, which penalizes suppliers unable to integrate digitally, whereas smaller municipalities still award contracts based on unit price.

Europe Water Treatment Chemicals Industry Leaders

Kemira

Kurita Water Industries Ltd.

Ecolab

Solenis

Veolia

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Kemira received board approval for a new activated-carbon reactivation plant in Helsingborg, Sweden, a low double-digit million-euro investment that supports Nordic demand for PFAS and micropollutant removal.

- July 2025: Kemira committed USD 23 million to add an aluminum chlorohydrate production line at its Tarragona, Spain, site, with start-up expected in 2028 to satisfy EMEA demand for high-performance coagulants.

Europe Water Treatment Chemicals Market Report Scope

Water treatment chemicals are substances used to make water suitable for various end-use applications, including drinking, cooking, irrigation, and industrial purposes. The chemicals help eliminate hazardous substances from water, including sand, minerals, bacteria, viruses, and other contaminants. The European water treatment chemicals market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into biocides and disinfectants, coagulants and flocculants, corrosion and scale inhibitors, defoamers and defoaming agents, pH adjusters and softeners, and other product types. By end-user industry, the market is segmented into commercial and institutional, power generation, chemical manufacturing, mining and mineral processing, municipal, and other end-user industries. The report also covers the market size and forecasts for European water treatment chemicals in seven regional countries. The market sizing and forecasts are provided for each segment based on value (USD).

By Product Type

| Biocides and Disinfectants |

| Coagulants and Flocculants |

| Corrosion and Scale Inhibitors |

| Defoamer and Defoaming Agent |

| pH Adjuster and Softener |

| Other Product Types |

By End-user Industry

| Commercial and Institutional |

| Power Generation |

| Chemical Manufacturing |

| Mining and Mineral Processing |

| Municipal |

| Other End-user Industries |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Rest of Europe |

| By Product Type | Biocides and Disinfectants |

| Coagulants and Flocculants | |

| Corrosion and Scale Inhibitors | |

| Defoamer and Defoaming Agent | |

| pH Adjuster and Softener | |

| Other Product Types | |

| By End-user Industry | Commercial and Institutional |

| Power Generation | |

| Chemical Manufacturing | |

| Mining and Mineral Processing | |

| Municipal | |

| Other End-user Industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the European water treatment chemicals market in 2025?

The European water treatment chemicals market size is expected to reach USD 5.67 billion in 2025.

What is the expected CAGR for water treatment chemicals demand in Europe to 2030?

Demand is projected to rise at a 6.45% CAGR, taking value to USD 7.75 billion by 2030.

Which product type is growing fastest across European utilities?

Coagulants and flocculants lead growth at a 7.34% CAGR because tertiary phosphorus removal becomes mandatory.

Why are municipal utilities the biggest buyers of treatment chemicals?

AMP8 and EU Cohesion Fund upgrades drive sustained chemical procurement, resulting in a 30.12% share and a 7.12% CAGR, the highest among all.

Which country records the sharpest market growth through 2030?

Nordic countries post the highest 7.67% CAGR due to stricter PFAS and phosphorus mandates that lift chemical volumes.