Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

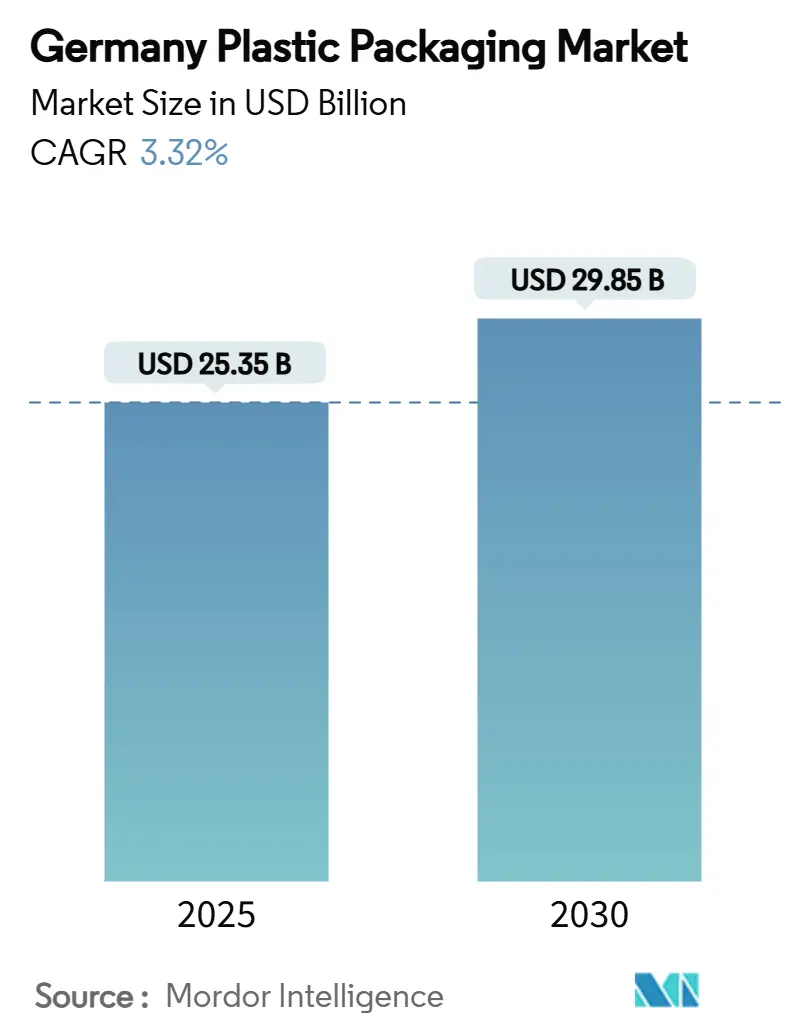

| Market Size (2025) | USD 25.35 Billion |

| Market Size (2030) | USD 29.85 Billion |

| Growth Rate (2025 - 2030) | 3.32% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Plastic Packaging Market Analysis by Mordor Intelligence

The Germany plastic packaging market size stood at USD 25.35 billion in 2025 and is on course to reach USD 29.85 billion by 2030, advancing at a steady 3.32% CAGR. The expansion reflects the sector’s ongoing transition toward circular-economy design principles while absorbing higher energy costs and stringent regulatory demands. Food packaging remains the anchor for volume, accounting for 39.32% of 2024 revenues, yet cosmetics and personal care is the pace-setter with a 5.58% CAGR through 2030. Flexible formats consolidate their lead as e-commerce, lightweight logistics and mono-material adoption intensify. In rigid solutions, PET benefits from Germany’s deposit system and high recycling rates, whereas polypropylene compounds gain traction in automotive light-weighting programs. Despite a 4.3% decline in domestic converter turnover during 2024, the Germany plastic packaging market continues to demonstrate resilience through high collection rates, rapid material innovation and deep industrial integration.

Key Report Takeaways

- By packaging type, flexible formats held 54.1% of Germany plastic packaging market share in 2024, while rigid solutions are forecast to post the fastest expansion at a 4.61% CAGR to 2030.

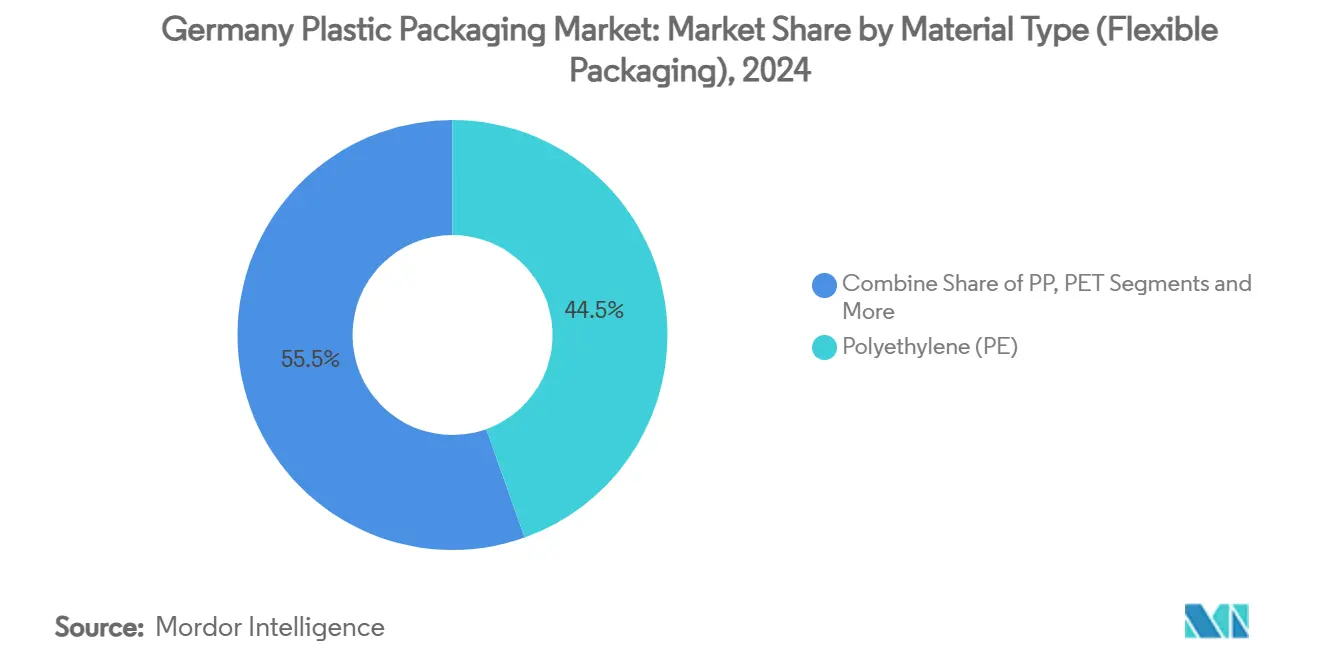

- By material type, polyethylene led with 44.54% share of flexible revenues in 2024; specialty films and emerging polymers are projected to grow at 6.87% CAGR through 2030.

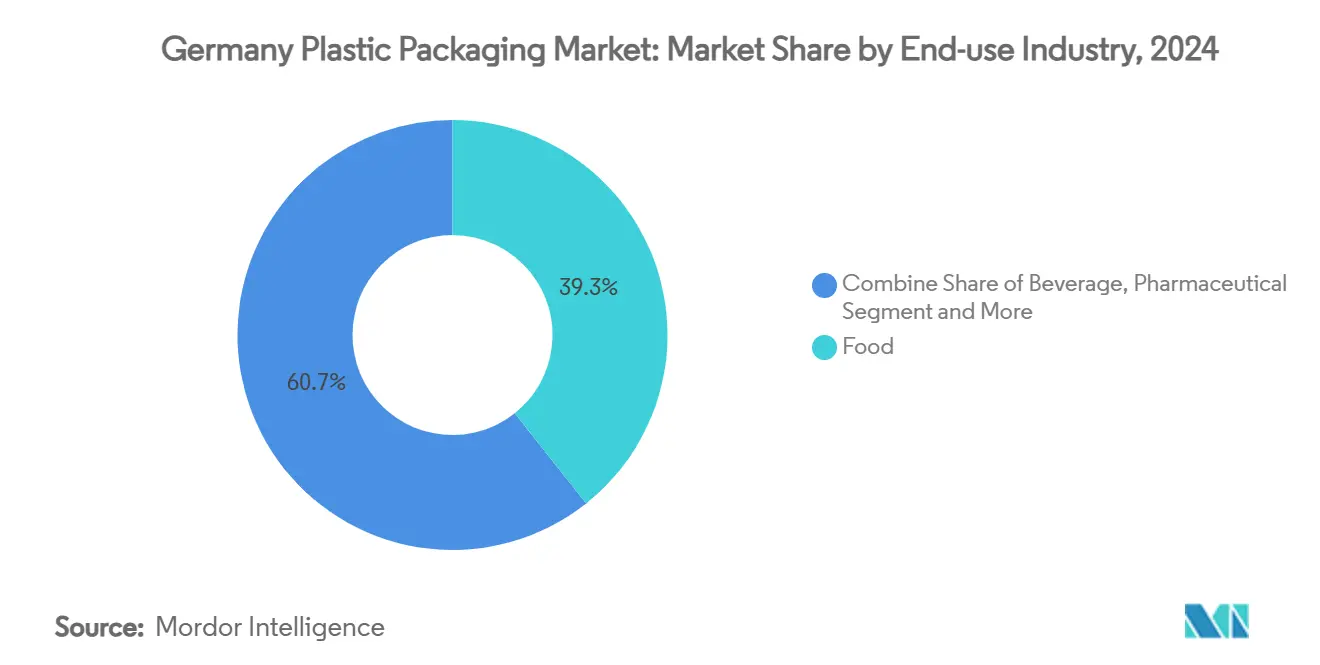

- By end-use industry, food retained 39.32% share of the Germany plastic packaging market size in 2024, whereas cosmetics and personal care exhibits the highest 5.58% CAGR to 2030.

- By distribution channel, direct sales controlled 68.56% share in 2024, while indirect routes are forecast to rise at 4.78% CAGR on the back of digital procurement platforms.

Germany Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Producer Responsibility mandates | +0.8% | National with EU spill-over | Medium term (2-4 years) |

| E-commerce boom and parcel mailers | +0.6% | National, urban focus | Short term (≤ 2 years) |

| Automotive & industrial lightweighting | +0.5% | National with export links | Long term (≥ 4 years) |

| Mehrweg PET refill quotas | +0.4% | National | Medium term (2-4 years) |

| Convenience-ready meal culture | +0.3% | National | Short term (≤ 2 years) |

| Cold-chain biologics pipeline | +0.2% | National, EU alignment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility mandates driving recyclable mono-material demand

Germany’s Packaging Act tightens recyclability rules, prompting brand owners to shift from complex laminates toward single-polymer structures. The Central Agency Packaging Register (ZSVR) released updated minimum standards in 2024 that attach higher compliance fees to multi-layer packs, channeling investment into mono-material polyethylene and polypropylene barrier solutions. Mondi and Fressnapf’s recyclable mono-material pet-food pouch exemplifies how regulatory pressure is translating into large-scale commercial roll-outs. [1]Mondi Group, “Mono-material pouches for dry pet food revealed by Mondi and Fressnapf,” mondigroup.com The approach also helps procurement teams score higher on retailer sustainability scorecards, turning compliance into a market differentiator.

E-commerce boom in Germany fueling lightweight flexible parcel mailers

Online retail keeps growing even as volumes fluctuate, pushing parcel operators to trim packing weight. DS Smith estimates 791 million plastic shipping bags were deployed in German fashion logistics during 2024 with unit demand projected to rise 42% to 2030.[2] DS Smith, “Kunststoffverpackungen im deutschen Online-Fashionhandel,” dssmith.com Flexible mailers reduce dimensional weight fees and carbon emissions, making them the default choice for apparel and small electronics. Amazon’s pledge to phase out plastics in its own fulfillment operations pressures third-party sellers to follow, accelerating the shift toward mono-material recyclables.

Automotive & industrial lightweighting shifting from metal to rigid plastics

The German Association of Plastics Converters highlights that replacing 300 kg of metal with 100 kg of engineering plastics delivers fuel-saving and CO₂ benefits, a message amplified by rising electric-vehicle output in Stuttgart and Wolfsburg. Polypropylene compound demand for automotive interiors is projected to climb from USD 1.31 billion in 2025 to USD 1.93 billion by 2034. OEM-supplier collaborations such as Audi’s circular-plastics pilot with the Karlsruhe Institute of Technology illustrate how design-for-recycling is entering the drivetrain and battery housing arena.

Mehrweg PET refill quotas accelerating rPET preform and bottle usage

Germany collects 93% of its PET beverage containers via the deposit system, creating Europe’s largest feedstock pool for recycled PET. [3]European Environment Agency, “Germany Municipal and Packaging Waste Factsheet 2025,” eea.europa.eu Average recycled content in bottles already stands at 24% and will reach the EU-mandated 30% by 2030. LyondellBasell’s Mo ReTec-1 chemical-recycling unit in Cologne will process difficult household waste equal to 1.2 million citizens’ output, closing the gap between rPET demand and supply. Brand owners consequently lock in long-term rPET sourcing contracts to secure compliance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proposed EUR 0.80/kg plastics tax | -0.7% | National | Short term (≤ 2 years) |

| Retailer-led fiber shift | -0.5% | National with EU links | Medium term (2-4 years) |

| High German electricity costs | -0.4% | National | Short term (≤ 2 years) |

| Limited food-grade rPCR supply | -0.3% | National with EU supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proposed EUR 0.80/kg German plastics tax inflating virgin resin prices

The Single-Use Plastics Fund Act that entered force in January 2025 levies EUR 0.80 on every kilogram of non-recycled plastic packaging. The Federal Environment Agency estimates annual collections near EUR 1.4 billion, a direct hit on converters working with virgin polymer streams umweltbundesamt.de. The measure sharpens the financial case for recycled content but also squeezes margins where food-grade rPET or rPP supply remains tight. Coupled with a 265% spike in industrial electricity tariffs since 2022, several mid-sized extruders have paused expansion plans.

Retailer-led fiber shift shrinking plastic shelf share

Supermarket groups Aldi, REWE and Lidl are removing single-use plastics from fresh produce aisles, replacing them with paper wraps or loose displays. REWE aims for fully recyclable own-brand packs by 2025 and a 20% cut in overall plastic tonnage, pushing suppliers to redesign packs or risk de-listing rewe-group-nachhaltigkeitsbericht.de. Functional limits persist for high-barrier dairy and meat applications, yet the optical reduction of visible plastics on shelf affects consumer perception and purchasing decisions.

Segment Analysis

By Material Type: Polyethylene drives flexible innovation

Polyethylene retained 44.54% share of flexible revenues in 2024, underpinned by cost efficiency, high seal integrity and mature recycling streams. The Germany plastic packaging market size for polyethylene formats stood at USD 11.3 billion in 2025 and continues to edge upward as converters roll out mono-material pouches with EVOH-free oxygen barriers. Emerging films such as recyclable polyolefin-based paper-touch laminates are expanding at 6.87% CAGR, indicating sustained R&D investment in lightweight, high-barrier structures that unlock producer responsibility fee rebates.

Other rigid resins tell a similar story. PET captured 33.36% share of rigid revenues thanks to the deposit-return system, while polypropylene outpaces other rigid substrates with a 5.76% CAGR through 2030. Polypropylene’s dimensional stability and heat resistance suit it for ready-meal trays and EV battery casings, reinforcing its demand in both consumer and industrial verticals. Conversely PVC and polystyrene continue to lose traction under recycling-related policy headwinds.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Flexible solutions propel the market

Flexible solutions held 54.1% share of 2024 revenues, validating their role as the workhorse of the Germany plastic packaging market. Stand-up pouches, pre-zipped bags and form-fill-seal webs deliver material savings of up to 70% compared with rigid tubs, a decisive advantage for brand owners paying modulated eco-fees. The segment’s 4.61% CAGR through 2030 eclipses rigid formats because flexible lines require lower capital and operate at faster change-over speeds, helping converters absorb fluctuating run sizes linked to e-commerce.

Rigid containers remain indispensable for carbonated beverages, cosmetics jars and pharma applications requiring dimensional stability. PET bottles achieve 93% take-back and high optical clarity, preventing contamination of food-grade rPET loops. Meanwhile, SCHOTT Pharma’s cardboard-based syringe wallet demonstrates how even high-value medical devices are testing fiber-slash-plastic hybrids to align with hospital waste-segregation protocols.

By End-use Industry: Food dominates while cosmetics accelerates

Food retained 39.32% of 2024 demand and will remain the backbone of the Germany plastic packaging market. Shelf-stable confectionery, snack multipacks and fresh produce liners rely on high-performance sealant layers that balance moisture control with recyclability. Dairy processors trial clear, retortable polypropylene cups that eliminate aluminium lids to lower cost and streamline sorting.

Cosmetics and personal care is the fastest climber at 5.58% CAGR. Premium skin-care brands leverage barrier laminate tubes with over 62% PCR content, a concept embraced by Bulldog men’s grooming in 2025, saving 8.5 t of virgin plastic annually. Pharma packaging also grows steadily due to biologics, cold-chain requirements and stricter child-resistant mandates, pushing multilayer blister designers to test PP-based foil replacements amenable to mechanical recycling streams.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channels: Direct engagement remains pivotal

Direct contracts between converters and brand owners secured 68.56% share in 2024. Co-engineering of pack structures, shelf-life validation and line trials demand tight collaboration that distributors often cannot provide. In addition, large FMCG groups negotiate multi-year supply accords to guarantee volumes of certified post-consumer resin.

Indirect channels are modernizing rapidly. Specialized online marketplaces now bundle standard mailers, labels and stretch films for SMEs at click-to-ship speed, fuelling a 4.78% CAGR. Converters see the route as a hedge against demand cycles in core accounts, although quality control and technical service remain challenges when physical proximity diminishes.

Geography Analysis

Germany’s status as Europe’s largest economy underpins the Germany plastic packaging market, supported by a dense network of polymer producers, converters and recyclers. Plastics Europe reported that domestic polymer output rose 4.5% in Q1 2025, lifting industry revenue to EUR 6.5 billion. North Rhine-Westphalia hosts major crackers and the new Mo ReTec-1 chemical-recycling plant, securing feedstock loops for western clusters. Bavaria and Baden-Württemberg, home to premium auto brands, generate concentrated demand for injection-moulded logistics trays and battery casings.

Logistics-driven site selection remains critical. Converters pair extrusion and printing assets near large food processors in Lower Saxony to enable just-in-time deliveries. Cross-border flows with the Benelux ensure a steady supply of ethylene, while export demand for German machinery supports tooling suppliers in the Black Forest region.

Energy price volatility, however, could influence regional competitiveness. Plants in eastern states weigh investment decisions against higher grid fees and workforce availability. Policy-aligned subsidies for chemical-recycling projects and renewable-energy PPAs may tilt future capacity additions toward areas offering reliable green-electricity sourcing.

Competitive Landscape

The Germany plastic packaging market features fragmentation. Top players span global multinationals and highly specialized mid-caps. Amcor, Constantia Flexibles, Gerresheimer, Mondi and Berry Global collectively dominate high-barrier flexibles, healthcare vials and PET preforms. The April 2025 Amcor-Berry merger created a USD 27 billion revenue leader with USD 650 million synergy targets by FY 2028, reshaping procurement scale.

Strategic plays gravitate toward circular integration. Mondi’s planned EUR 634 million purchase of Schumacher Packaging widens its corrugated footprint and accelerates fibre-plastic hybrid development. LyondellBasell’s investment in advanced recycling safeguards resin availability while lowering Scope 3 footprints for downstream packagers. Mid-sized extrusion coaters invest in AI-enabled optical sorters and digital print presses to offer small-batch, design-to-print services.

Innovation races centre on mono-material laminate patents, oxygen-scavenging additives compatible with PE, and RFID-enabled smart labels that provide pack-level traceability. Start-ups focusing on enzymatic recycling and bio-based PHA films are securing pilot lines inside established converters’ R&D hubs, signalling that collaborative open-innovation models are becoming the norm.

Germany Plastic Packaging Industry Leaders

-

Amcor Plc

-

Mondi Group

-

Huhtamaki Oyj

-

Sealed Air Corporation

-

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: SÜDPACK MEDICA doubled clean-room pouch capacity at its French facility to reinforce supply security for German pharma customers.

- June 2025: Amcor trimmed material usage in Bulldog skin-care tubes by 16.67%, integrating 62% PCR without compromising barrier performance.

- April 2025: Amcor completed its all-stock merger with Berry Global, projecting USD 650 million annual synergies and 12% EPS accretion in FY 2026.

- January 2025: Germany enforced the Single-Use Plastics Fund Act, imposing EUR 0.80/kg levies on non-recycled packaging with first payments in 2025.

Germany Plastic Packaging Market Report Scope

Plastic packaging is a part of the multi-faceted system for providing products, from the point of manufacture to the consumption end. Its principal purpose is to guard and ensure safe and secure product delivery in flawless and perfect condition to the end-user (manufacturer of product or consumer). Its role in a circular economy is to sustain the value of a product as long as required and to help remove product waste.

The Germany Plastic Packaging Market is segmented by packaging type (rigid plastic, flexible plastic), end-user industry (food, beverage, healthcare, personal care, and household, and other end-user), and products (bottles and jars, cans, pouches, trays and containers, films and wraps, and other product types).

The market sizes and forecasts are in terms of value (USD million) for all the above segments.

By Material Type

| Rigid Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |

| Other Rigid Plastic | |

| Flexible Plastic | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Polyvinyl Chloride (PVC) | |

| Ethylene-Vinyl Alcohol (EVOH) | |

| Other Flexible Plastic |

By Packaging Type

| Rigid Plastic Packaging | Bottles and Jars |

| Trays and Clamshells | |

| Pallets and Crates | |

| Other Rigid Plastic Packaging | |

| Flexible Plastic Packaging | Pouches |

| Bags and Sacks | |

| Films and Wraps | |

| Other Flexible Plastic Packaging |

By End-use Industry

| Food | Confectionery and Snacks |

| Breads and Cereals | |

| Fresh Produce | |

| Dairy based products | |

| Other Food Products | |

| Beverage | Bottled Water |

| Juices and Nectars | |

| Dairy Based Beverages | |

| Carbonated Soft Drinks | |

| Other Beverages | |

| Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial | |

| Pet Food and Animal Care | |

| Other End-use Industry |

By Distribution Channels

| Direct Sales Channels |

| Indirect Sales Channels |

| By Material Type | Rigid Plastic | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride (PVC) | ||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||

| Other Rigid Plastic | ||

| Flexible Plastic | Polyethylene (PE) | |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Ethylene-Vinyl Alcohol (EVOH) | ||

| Other Flexible Plastic | ||

| By Packaging Type | Rigid Plastic Packaging | Bottles and Jars |

| Trays and Clamshells | ||

| Pallets and Crates | ||

| Other Rigid Plastic Packaging | ||

| Flexible Plastic Packaging | Pouches | |

| Bags and Sacks | ||

| Films and Wraps | ||

| Other Flexible Plastic Packaging | ||

| By End-use Industry | Food | Confectionery and Snacks |

| Breads and Cereals | ||

| Fresh Produce | ||

| Dairy based products | ||

| Other Food Products | ||

| Beverage | Bottled Water | |

| Juices and Nectars | ||

| Dairy Based Beverages | ||

| Carbonated Soft Drinks | ||

| Other Beverages | ||

| Pharmaceutical | ||

| Cosmetics and Personal Care | ||

| Industrial | ||

| Pet Food and Animal Care | ||

| Other End-use Industry | ||

| By Distribution Channels | Direct Sales Channels | |

| Indirect Sales Channels | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Germany plastic packaging market?

The market is valued at USD 25.35 billion in 2025 and is projected to touch USD 29.85 billion by 2030.

Which segment holds the largest Germany plastic packaging market share?

Flexible formats lead with 54.1% share as of 2024, driven by e-commerce parcel mailers and lightweight pouches.

How fast is the cosmetics and personal care segment growing?

It is expanding at a 5.58% CAGR through 2030, the fastest among all end-use industries.

What impact does the German plastics tax have on converters?

The EUR 0.80/kg levy on non-recycled packaging raises raw-material costs and compresses margins, particularly for converters with limited access to food-grade recyclate.

Why is polyethylene dominant in flexible applications?

Polyethylene offers cost-effective sealing, established recycling streams and compatibility with mono-material barrier technologies, holding 44.54% of flexible revenues.

How are leading companies responding to sustainability mandates?

Strategies include mergers for scale, such as Amcor-Berry, investments in chemical-recycling plants, and the launch of mono-material or fibre-hybrid pack formats that satisfy recyclability criteria.

Page last updated on: