Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

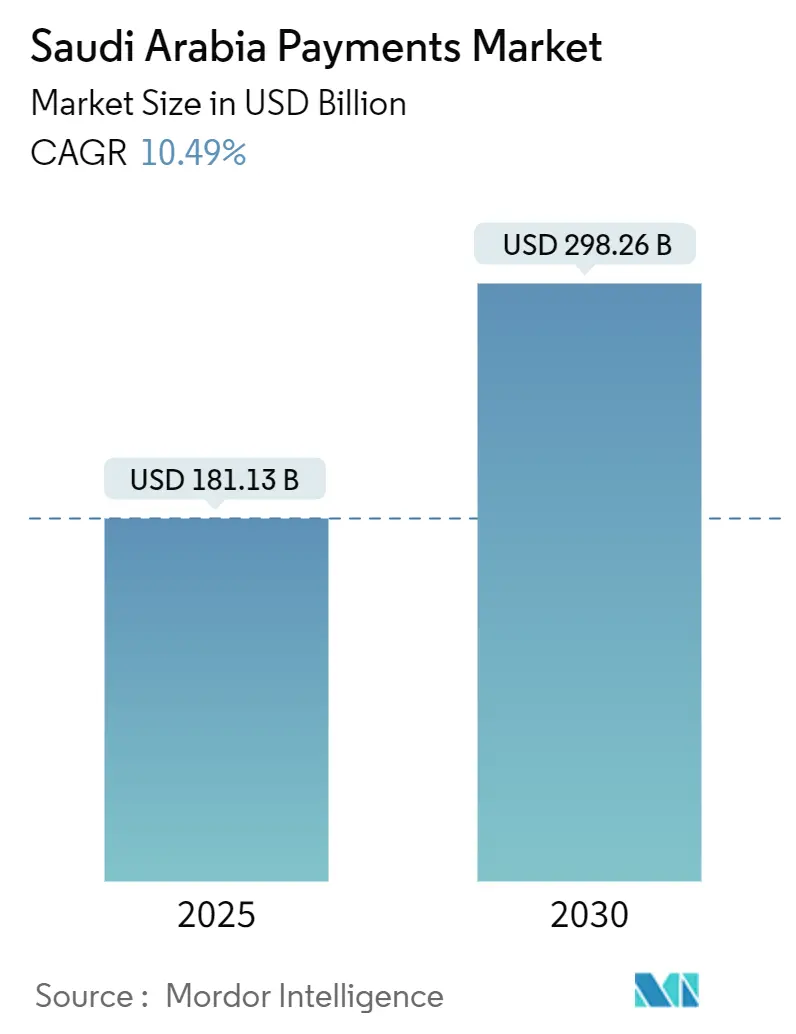

| Market Size (2025) | USD 181.13 Billion |

| Market Size (2030) | USD 298.26 Billion |

| Growth Rate (2025 - 2030) | 10.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Payments Market Analysis by Mordor Intelligence

The Saudi Arabia payments market reached a market size of USD 181.13 billion in 2025 and is projected to expand to USD 298.26 billion by 2030, reflecting a robust 10.49% CAGR during the forecast period. Vision 2030’s cash-less objectives, real-time settlement rails, and open-banking standards continued to accelerate digital transaction volumes while encouraging competitive differentiation across service layers. Point-of-sale volumes still dominated value, yet e-commerce growth, account-to-account (A2A) rails, and tokenized pilgrim wallets elevated online channels. Regulatory clarity around payment initiation, central-bank-digital-currency (CBDC) pilots, and youth-driven buy-now-pay-later (BNPL) adoption further stimulated the Saudi Arabia payments market, positioning it as the Gulf’s most dynamic digital finance hub.[1]Adam Jones, “Redefining Digital Financial Services in Saudi Arabia,” Mastercard Perspectives, mastercard.comIntensifying cross-border trade, industrial digitization in Eastern Province, and religious tourism innovations created adjacent revenue pools that incumbent banks and fintech startups raced to capture.

Key Report Takeaways

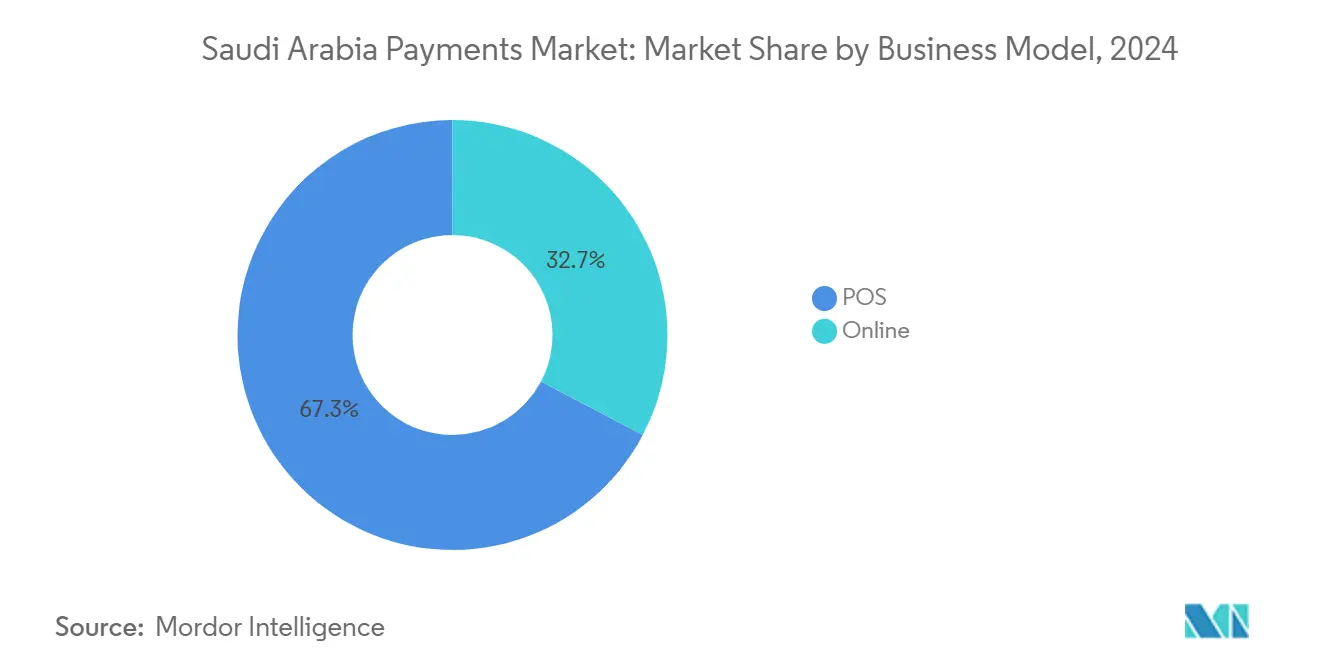

- By mode of payment, point-of-sale transactions held 67.30% of the Saudi Arabia payments market share in 2024, whereas online payments are advancing at an 11.67% CAGR to 2030.

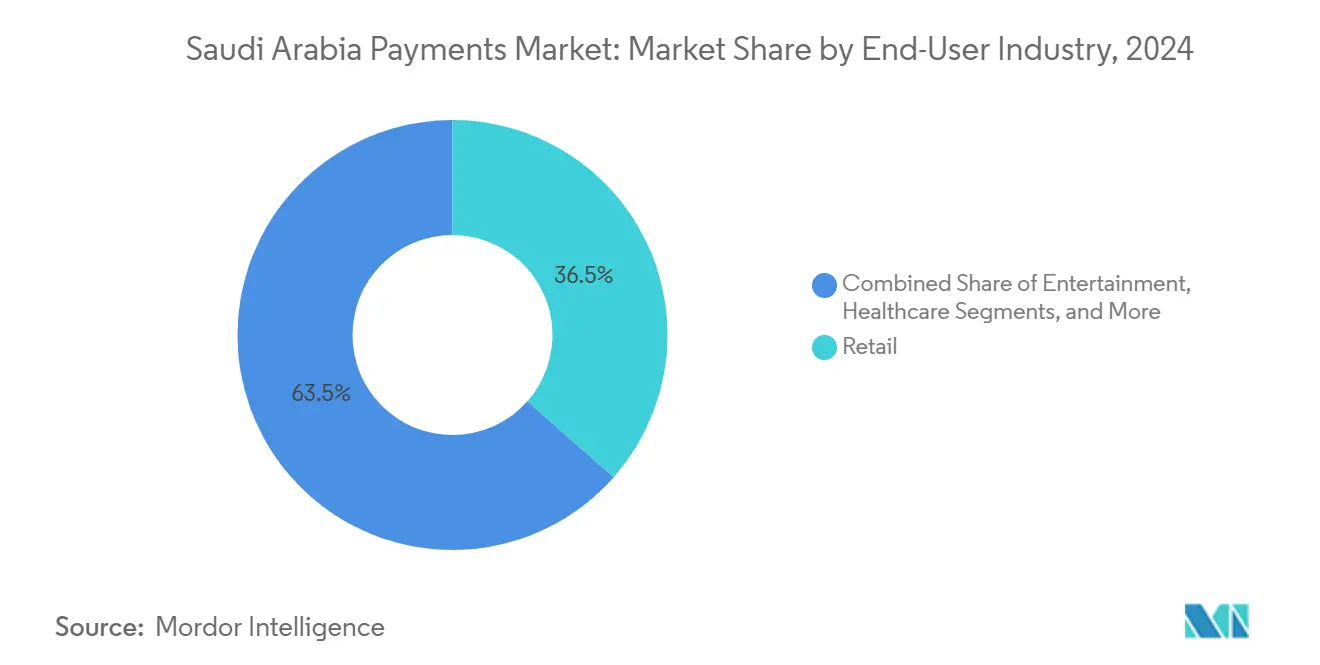

- By end-user industry, retail commanded 36.50% share of the Saudi Arabia payments market size in 2024, while entertainment is forecast to expand at an 11.98% CAGR through 2030.

- By geography, Riyadh contributed 35.34% of 2024 transaction value, while Eastern Province is projected to grow at an 11.36% CAGR between 2025-2030.

Saudi Arabia Payments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating e-commerce penetration | +2.1% | National | Medium term (2-4 years) |

| Cashless 2030 targets and instant payments | +2.8% | National | Long term (≥ 4 years) |

| Open-banking framework rollout | +1.7% | National / GCC | Medium term (2-4 years) |

| BNPL surge among youth | +1.9% | Urban centers | Short term (≤ 2 years) |

| Tokenized pilgrim wearables | +0.8% | Makkah and Madinah | Short term (≤ 2 years) |

| Digital Riyal pilots | +1.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cashless 2030 Targets and Instant Payments Infrastructure

SARIE processed transactions worth SAR 2.5 trillion in 2024, delivering sub-second settlement between banks and lowering liquidity costs, which reinforced confidence in the Saudi Arabia payments market.[2]Saudi Central Bank, “Implementation Progress of SARIE & AFAQ,” sama.gov.sa AFAQ complemented SARIE by handling high-volume, low-value government and utility transfers, letting agencies automate disbursements at minimal marginal cost. Private firms leveraged the dual rail architecture to deploy just-in-time supplier payouts, unlocking working-capital efficiencies in manufacturing and petrochemicals. Banks integrated SARIE APIs into corporate cash-management portals, which compressed receivable cycles for exporters shipping to Asian buyers. The real-time rails therefore served as a platform for new revenue streams-from instant payroll to micro-savings products-while building resilience against cross-border correspondent-bank fees.

BNPL Surge Among Youth

Tamara achieved unicorn status at a USD 1 billion valuation in 2024 after raising USD 340 million, illustrating how alternative credit addressed historic gaps in revolving credit access for the Kingdom’s under-35 majority. Tabby shifted its regional headquarters to Riyadh and reached a USD 3.3 billion valuation, signaling the pull of the Saudi Arabia payments market for BNPL pioneers. Summer 2024 BNPL volumes tripled year-on-year as merchants observed a 30% rise in average order values, sparking adoption by offline grocers, electronics chains, and automotive parts retailers.[3]Staff Writer, “Summer 2024 Sees a Boom in Digital Payments,” checkout.com Regulatory sandboxes allowed rapid product iteration while ensuring consumer-protection caps on late-fees, bolstering trust. Fintech lenders simultaneously embedded Sharia-compliant financing logic, widening acceptance among conservative shoppers.

Open-Banking Framework Rollout

Phase 2 of SAMA’s open-banking plan introduced Payment Initiation Services in 2024, permitting licensed third parties to pull funds directly from customer accounts and bypass card networks. Participating banks reported a 15% drop in checkout abandonment on merchant sites that switched to direct-debit rails, highlighting the cost and latency advantages. Fintech newcomers packaged account aggregation with budgeting, payroll, and automated VAT reconciliation, deepening client stickiness. Alignment with international API standards facilitated partnerships with EU and Singaporean providers eager to export technology to the Saudi Arabia payments market. Early adopters witnessed a 25% lift in daily active users across digital channels, confirming open-banking’s role in sustaining engagement beyond basic balance queries.

Tokenized Pilgrim Wearables

Nusuk deployed contactless bracelets for 2 million Hajj pilgrims in 2024, enabling 85% of on-site retail transactions to clear digitally, freeing visitors from cash handling and exchange-rate uncertainties. The wearables used near-field communication linked to multi-currency wallets, settling in real time over SARIE rails. Retailers inside the holy sites saw a 20% reduction in queue times, improving crowd management and compliance with safety protocols. Post-event analytics allowed merchants to tailor inventory for Umrah seasons, illustrating data monetization potential. The initiative showcased how specialized vertical solutions can scale nationally and abroad, reinforcing the competitive appeal of the Saudi Arabia payments market to event-economy innovators.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High merchant MDR for cross-border cards | -1.4% | National / border cities | Medium term (2-4 years) |

| Cyber-fraud and data-privacy fears | -0.9% | National | Short term (≤ 2 years) |

| Patchy rural acceptance infrastructure | -1.1% | Rural and secondary cities | Long term (≥ 4 years) |

| Consumer inertia among >55 demographic | -0.7% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Merchant MDR for Cross-Border Cards

Average fees ranging from 6-12% on international card payments squeezed exporter margins and deterred small retailers from serving overseas tourists. Multi-leg correspondent-bank chains introduced double-FX spreads and delayed settlement, compounding cash-flow constraints. The Saudi Arabia payments market saw fintech entrants pitch corridor-specific solutions that netted 20-40 bps savings by routing remittances through regional hubs. SAMA’s bilateral CBDC experiments with UAE signaled intent to dismantle these cost layers, although production timelines extended beyond 2027. Meanwhile, e-commerce merchants increasingly promoted A2A pay-by-link options for GCC shoppers, circumventing card rails and shifting chargeback risk to issuers.

Cyber-Fraud and Data-Privacy Fears

Payment-related fraud losses totaled USD 140 million in 2024, fueling a 7.52% CAGR cybersecurity spend that reached USD 2.4 billion. Data-localization mandates forced global processors to deploy in-country nodes, raising capex yet enhancing incident-response speeds. Heightened anti-money-laundering checks slowed onboarding for high-risk merchants such as crypto brokers, tempering digital uptake. Consumer surveys highlighted phishing as the top fear, prompting both banks and fintechs to roll out biometric-login, tokenized PAN, and AI-powered anomaly detection. Sustained fraud-education campaigns remain vital to nurturing confidence in the Saudi Arabia payments market.

Segment Analysis

By Mode of Payment: Digital Channels Redefine Value Creation

Point-of-sale terminals retained 67.30% share in 2024, underscoring the lingering weight of physical commerce within the Saudi Arabia payments market. However, online payments recorded an 11.67% CAGR forecast through 2030 and are capturing incremental value from rapid e-commerce penetration, which grew 9.4% in Q3 2024 alone. The structural pivot reflects changing consumer behavior, deeper logistics reach, and superior mobile-wallet experiences. Retailers embedded mada, Apple Pay, Google Pay, and STC Pay buttons at checkout, minimizing friction. The integration of SARIE APIs into gateway stacks trimmed acquiring fees by up to 30 bps for high-ticket electronics merchants.

A2A transactions gained further traction as corporates adopted real-time salary disbursements, boosting worker liquidity. Digital wallets-such as urpay, which served 5 million customers-extended reach to 180 countries through Mastercard Move rails, consolidating foreign-currency remittances into the Saudi Arabia payments market. Cash-on-delivery contracted as logistics firms bundled QR-code pay-on-arrival options, bringing rural buyers into the formal ecosystem. Contactless penetration surged above 94% of card transactions in urban centers, reflecting pandemic-period behavioral shifts that persisted into 2025. Merchants deployed value-added modules-installments, e-invoicing, e-receipt archiving-to differentiate beyond price, evidencing maturation of service-layer competition.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Entertainment Outpaces Retail

Retail payments controlled 36.50% of 2024 transaction value, supported by hypermarkets, convenience stores, and mall clusters that rapidly integrated omni-channel checkout journeys. Yet entertainment transactions are projected to grow at an 11.98% CAGR to 2030 as Vision 2030 investments pour into cinemas, theme parks, and esports arenas. PayOne’s 2025 agreement with SaudiCo equipped hospitality operators with fully reconciled payment stacks, reducing chargebacks by 15% and elevating guest satisfaction. Sports venues adopted facial-recognition ticketing linked to stored-value wallets, enhancing stadium throughput while capturing granular fan-spend analytics.

Healthcare digitization accelerated after Bupa Arabia’s no-pre-approval network served 200 000 members by March 2025, demonstrating frictionless settlement potential in insurance claims. Telemedicine platforms integrated tokenized billing that auto-releases payment upon doctor verification, averting disputed charges. Education providers embraced subscription-style tuition plans billed via open-banking rails, smoothing cashflow for households. The Saudi Arabia payments market therefore diversified from retail dependence toward experience-centric verticals that reward contextual, embedded payment flows. Providers able to tailor sector-specific risk, settlement, and compliance modules secured stickier revenue-reinforcing the competitive premium on specialization.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Riyadh accounted for 35.34% of 2024 transaction value, anchored by government payrolls, corporate treasuries, and a concentration of fintech headquarters. The capital’s high smartphone penetration continued to foster early adoption of biometric and IoT payments. Eastern Province’s 11.36% CAGR outlook between 2025-2030 stemmed from petrochemical diversification, port-linked free-trade zones, and cross-border commerce with Bahrain and Kuwait, which together elevated high-value B2B flows that now settle in real time via SARIE. Investors funneled USD 330 billion into industrial and logistics megaprojects, driving demand for treasury, procurement-financing, and supplier-payment automation.

Makkah’s unique religious-tourism economy accelerated digital-wallet penetration through Nusuk’s contactless solution, which processed 85% of retail spend inside holy sites during the 2024 Hajj season. Visa-on-arrival pilgrims used multi-currency wallets, cutting FX leakage and queuing. Secondary cities such as Tabuk, Abha, and Al-Ahsa lagged infrastructure readiness yet benefited from mobile-network rollouts and agent-bank programs that seeded QR acceptance in convenience stores. The Rest-of-Saudi cohort nevertheless represented a vital inclusion frontier: 4.2 million migrant workers remitted wages each month, suggesting a material untapped slice of the Saudi Arabia payments market awaiting low-cost wallet-to-wallet corridors.

Competitive Landscape

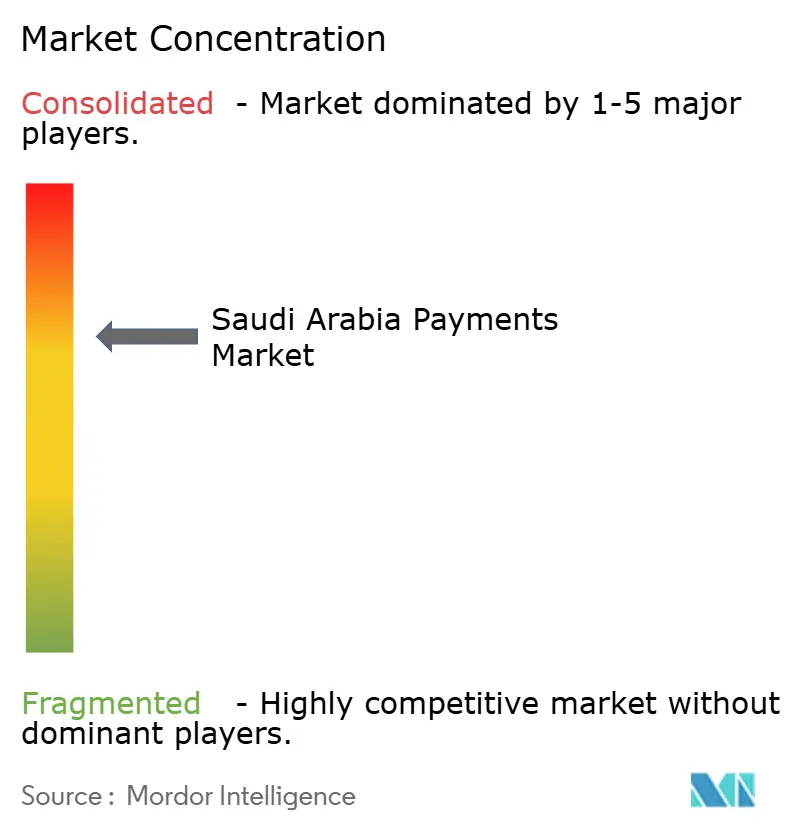

The Saudi Arabia payments market displayed a moderate concentration level, with mada rails underpinning every card transaction but competition flourishing in overlay services. Geidea captured 75% of the national ATM fleet and equipped 150 000 merchants with omnichannel gateways, illustrating scale advantages in hardware-as-a-service. International schemes deepened roots: Visa opened an Innovation Center in Riyadh in 2024, while Mastercard launched local processing infrastructure to meet data-residency mandates. Meanwhile, STC Pay leveraged its 10-million-user base to spin off stc Bank, securing SAMA approval in January 2025 with SAR 2.5 billion capitalization and broadening competition into digital banking.

Strategic alliances multiplied. Telr partnered with Bank AlJazira in February 2025 to bundle BNPL, fraud, and e-invoice modules for SME merchants. Al Rajhi Bank integrated its Makafaa rewards scheme into 60 000 Salla e-stores, pushing closed-loop loyalty across the Saudi Arabia payments market. Cross-border corridors remained white space: UnionPay’s July 2024 tie-up with Saudi Awwal Bank aimed to lure Asian tourists by expanding acceptance, while banks contemplated blockchain-based corridors to slash sender fees. Competitive intensity therefore shifted from basic acquiring to data analytics, embedded finance, and ecosystem partnerships, signaling a marketplace where technological agility outranked legacy scale.

Saudi Arabia Payments Industry Leaders

-

Saudi Payments Company (mada network)

-

STC Bank (STC Pay Wallet)

-

Visa Inc.

-

Mastercard Inc.

-

Hyperpay Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: STC Bank commenced digital banking operations after SAMA approval, building on STC Pay’s wallet network.

- January 2025: Google Pay launched nationwide through mada integration, expanding wallet choice for Android users.

- February 2025: Telr and Bank AlJazira teamed up to deliver an end-to-end payment suite featuring BNPL and e-invoicing.

- February 2025: Al Rajhi Bank partnered with Salla to extend Makafaa loyalty across 60 000 online stores.

Saudi Arabia Payments Market Report Scope

The payments market is segmented by two modes of payment - POS and e-commerce. E-commerce payments include online purchases of goods and services, such as purchases on e-commerce websites and online booking of travel and accommodation. However, it does not include online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for POS, all transactions that occur at the physical point of sale are included in the market scope. It includes traditional in-store transactions and all face-to-face transactions, regardless of where they take place. Cash is also considered for both cases (cash-on-delivery for e-commerce sales).

The Saudi Arabian payments market is segmented by mode of payment (point of sale (card payments, digital wallet, cash, and others), online sale (card payments, digital wallet, and others)), and end-user industry (retail, entertainment, healthcare, hospitality, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Payment Mode

| Point-of-Sale (POS) | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other Point- of-Sale (POS) Payment Modes | |

| Online (E-commerce and In-app) | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sale Payment Modes |

By End-User Industry

| Retail |

| Entertainment |

| Healthcare |

| Hospitality |

| Other End-User Industries |

| By Payment Mode | Point-of-Sale (POS) | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point- of-Sale (POS) Payment Modes | ||

| Online (E-commerce and In-app) | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sale Payment Modes | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Healthcare | ||

| Hospitality | ||

| Other End-User Industries | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large was the Saudi Arabia payments market in 2025?

How large was the Saudi Arabia payments market in 2025?

What CAGR is forecast for transaction value through 2030?

Aggregate value is projected to rise at a 10.49% CAGR, taking total volume to USD 298.26 billion by 2030

Which payment segment is growing fastest?

Online payments are forecast to post an 11.67% CAGR as e-commerce penetration deepens and A2A rails bypass card fees.

Why is Eastern Province considered a high-growth region?

Industrial digitization, port-centric trade, and cross-border links to Bahrain and Kuwait are driving an 11.36% CAGR outlook.

How is BNPL reshaping consumer spending?

BNPL providers like Tamara and Tabby enable flexible checkouts, boosting average order values and widening credit access for the under-35 demographic.

What role do SARIE and AFAQ play in market development?

They provide instant and batch settlement rails, cut liquidity costs, and underpin new use-cases such as instant payroll and pilgrim wallets.

Page last updated on: