Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

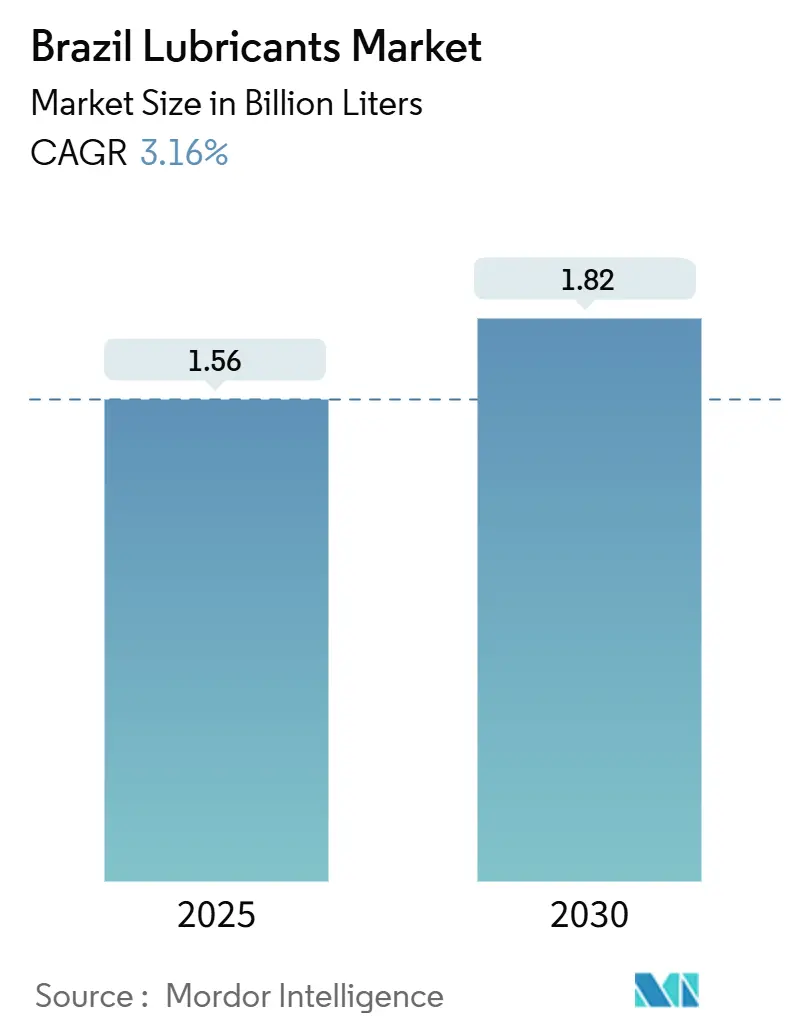

| Market Volume (2025) | 1.56 Billion liters |

| Market Volume (2030) | 1.82 Billion liters |

| Growth Rate (2025 - 2030) | 3.16% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Lubricants Market Analysis by Mordor Intelligence

The Brazil Lubricants Market size is estimated at 1.56 billion liters in 2025, and is expected to reach 1.82 billion liters by 2030, at a CAGR of 3.16% during the forecast period (2025-2030). This sizable domestic base underscores Brazil’s role as Latin America’s largest lubricants consumer. Rising vehicle registrations, a broad re-industrialization push, and steady pre-salt exploration sustain volume expansion even as electric mobility gains share. Refinery upgrades led by Petrobras are expected to increase Group II base-oil production, reducing import reliance and supporting premium formulations. Meanwhile, tightening emission rules and the adoption of predictive maintenance are shifting demand toward synthetic blends that deliver extended drain intervals. Competitive strategies now revolve around vertical integration, technical partnerships, and distribution reach as illicit trade and crude-price swings pressure margins. Companies that align portfolios with flex-fuel engines, heavy equipment uptime, and offshore drilling needs are positioned to capture the next leg of growth in the Brazil lubricants market.

Key Report Takeaways

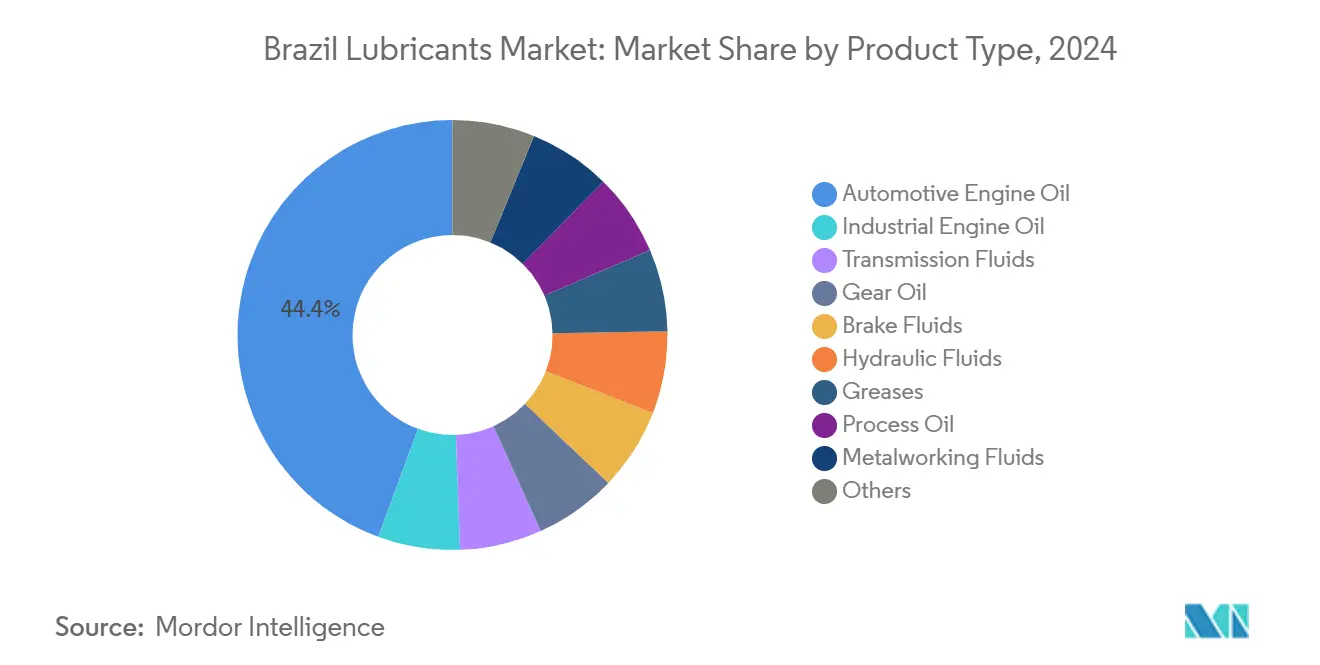

- By product type, automotive engine oil led with 44.38% revenue share in 2024; grease is projected to expand at a 4.88% CAGR through 2030.

- By end-user industry, the automotive segment held 56.76% of the Brazilian lubricants market share in 2024, while industrial uses are forecast to register the highest CAGR of 5.04% from 2024 to 2030.

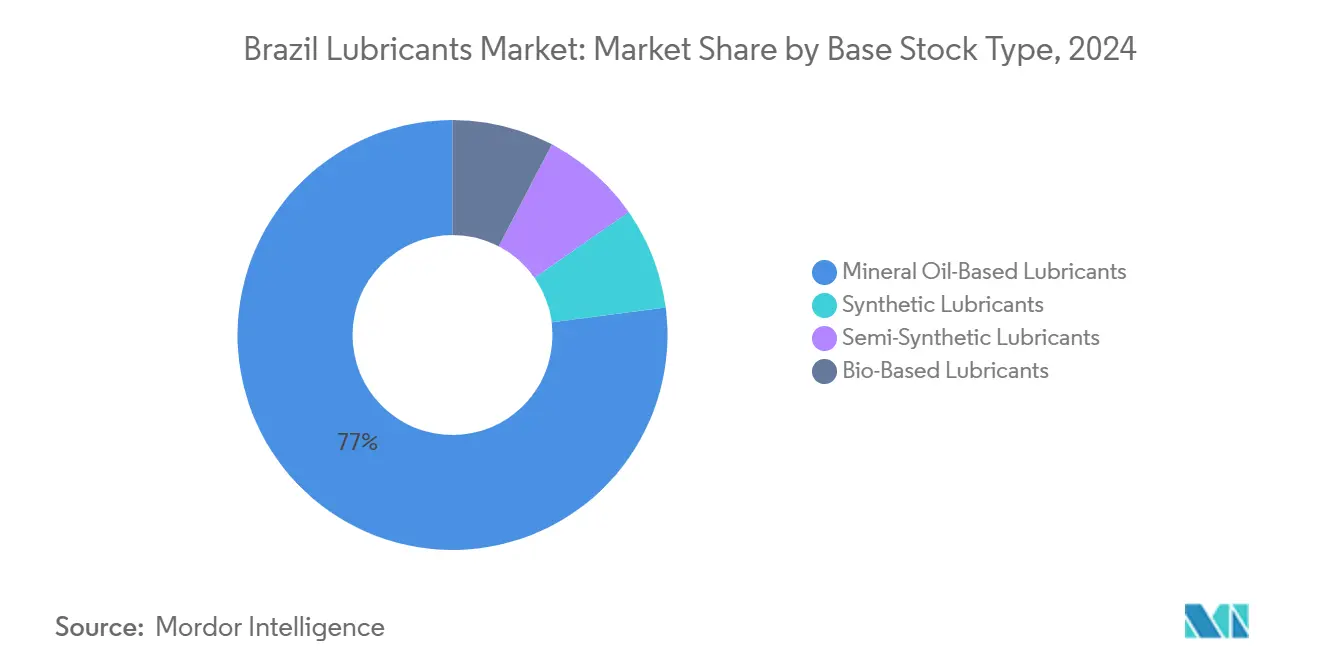

- By base stock type, mineral formulations accounted for 77.04% share of the Brazil lubricants market size in 2024, and synthetics are advancing at a 4.71% CAGR through 2030.

Brazil Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle parc expansion and after-market growth | +0.8% | São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Industrial capex recovery from re-industrialization programs | +0.7% | Southeast, South, expanding Northeast | Long term (≥ 4 years) |

| Stricter emission norms spurring premium lubricants | +0.4% | National metro areas | Medium term (2-4 years) |

| Pre-salt exploration and production boom raising marine and drilling fluid demand | +0.3% | Coastal Santos and Campos basins | Long term (≥ 4 years) |

| Ethanol-process integration boosting specialty lubes | +0.2% | Center-West and Southeast sugarcane belt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vehicle Parc Expansion and After Market Growth

Light- and heavy-duty registrations continue to rise, lifting fuel use. An aging fleet, more than 60% of passenger cars are over 10 years old, requires shorter oil-change intervals, which favor higher-margin workshop sales. Fleet operators are adopting predictive maintenance, which extends drain intervals while demanding synthetic blends that protect engines under mixed ethanol and gasoline cycles. E-commerce logistics activity intensifies the use of heavy-duty trucks, reinforcing the consumption of API CK-4 formulations. The spread of flex-fuel engines, already standard in 85% of new cars, drives the need for corrosion-resistant additives, expanding premium niches in the Brazil lubricants market.

Industrial Capex Recovery from Re Industrialization Programs

The USD 60 billion Made in Brazil initiative funds new capacity in autos, machinery, and chemicals, reviving demand for hydraulic fluids, gear oils, and metalworking fluids. Utilization gains at automotive assembly plants increase the consumption of high-speed spindle oils, which enable precision machining. Planned 13,200 MW of flexible generation by 2027 escalates the need for turbine and transformer oils that meet strict dielectric specs[1]Energy Research Office, “EPE EN Início,” EPE.GOV.BR. Vale’s mine expansions in Minas Gerais and Pará sustain heavy-duty hydraulic-fluid volume, while sugar-energy complexes drive process-oil uptake. These trends underpin the fastest growth rate among end-users, reinforcing industrial pull on the Brazil lubricants market.

Stricter Emission Norms Spurring Premium Lubricants

Phase L8 of the PROCONVE program aligns with Euro 6 and requires low-viscosity, low-SAPS oils that safeguard diesel particulate filters. Truck fleets are shifting toward API FA-4 10W-30 synthetics to balance fuel economy with uptime, thereby expanding mid-tier synthetic demand. Additive houses, such as Chevron Oronite, deepen Brazilian technical hubs through distribution deals with ICONIC, thereby accelerating local qualification cycles. Premiumization spreads to two-wheeler oils as urban delivery riders seek higher-temperature stability in congested traffic. The regulatory push lifts average selling prices, supporting value growth in the Brazil lubricants market.

Pre Salt Exploration and Production Boom Raising Marine and Drilling Fluid Demand

Pre-salt output already accounts for a major portion of national crude and targets 5 million bpd by 2027, elevating demand for EAL-compliant marine gear oils and synthetic drilling fluids able to withstand 10,000 psi conditions. Additional FPSO units in the Santos Basin drive year-round orders for hydraulic fluids and specialty greases that resist saltwater corrosion. Petrobras collaborates with Vale on 24% renewable bunker fuels, prompting lubricant suppliers to validate the compatibility of their products with bio-content blends. Technical entry barriers favor multinationals with global offshore references, supporting margin resilience within this high-value slice of the Brazil lubricants market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude and base-oil price swings | -0.5% | Import-dependent regions | Short term (≤ 2 years) |

| EV penetration cutting engine oil volume | -0.3% | Large urban centers | Long term (≥ 4 years) |

| Illicit or tax-evasion lube trade eroding formal sales | -0.4% | Border and informal zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude and Base Oil Price Swings

Spot Group II imports from the United States expose local blenders to currency swings, squeezing their margins when the real exchange rate weakens. Boaventura’s Group II stream will improve supply security by 2027, yet covers only part of the total need. Small producers lacking scale face steep minimum-order commitments, prompting consolidation toward firms with procurement leverage. Frequent list-price updates strain customer loyalty, while inventory hedging ties up working capital that could be used to fund product development in the Brazilian lubricants market.

EV Penetration Cutting Engine Oil Volume

Pure battery cars displace engine oil demand entirely, though hybrid uptake tempers the near-term decline. Urban bus and last-mile delivery electrification cuts heavy-duty volumes where per-unit consumption is highest. Suppliers diversify into e-gear oils and dielectric coolants, but these emerging lines remain relatively small in terms of liters compared to legacy products. Managing stranded blending assets becomes a strategic imperative within the Brazil lubricants market.

Segment Analysis

By Product Type Engine Oils Lead Despite Grease Acceleration

Automotive engine oils accounted for 44.38% of the total volume in 2024, underscoring the enduring importance of passenger and commercial vehicle maintenance within the Brazilian lubricants market. Grease, although a smaller line, posts the fastest 4.88% CAGR through 2030 as mining and farming equipment fleets scale in harsh environments. Transmission fluids gain from rising automatic gearbox penetration, while hydraulic fluids remain staples in construction and mining. Metalworking fluids see selective growth in high-speed machining segments tied to advanced manufacturing plants.

Heavy-duty engine oils for power generation and marine propulsion provide steady, if specialized, demand where uptime trumps initial price. Oil consumption is linked to tire and petrochemical output, while turbine oil orders align with gas-fired capacity additions. Transformer oils benefit from grid investments in high-voltage corridors. Collectively, this diversified mix supports resilience in the Brazilian lubricants market, even as the engine oil share edges down over time.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User Industry Industrial Sector Drives Growth Acceleration

The automotive sector maintained a 56.76% share in 2024. Industrial applications, however, are expected to record the highest 5.04% CAGR through 2030, as manufacturing, mining, and power assets scale. Construction and agriculture continue to drive demand for hydraulic fluids, while offshore operators specify high-performance marine oils.

Commercial vehicles consume more liters per unit than passenger cars, anchoring volume despite the risks of electrification. Two-wheelers require cost-sensitive, yet emission-compliant, oils for the delivery and ride-hailing sectors. Aerospace remains a niche yet technically demanding field, with Embraer’s supply chain creating a domestic demand for aviation-grade products. This end-user shift underpins an evolving revenue mix within the Brazil lubricants market.

By Base Stock Type Synthetic Growth Challenges Mineral Dominance

Mineral formulations maintained a 77.04% share in 2024, while synthetic lines expanded at a 4.71% CAGR as operators sought longer drainages and emission compliance. Semi-synthetic blends offer a cost-effective solution for fleets transitioning to higher performance levels. Bio-based lubes trail in volume but gain research and development attention thanks to local fatty-acid feedstocks that deliver promising tribology results.

Domestic Group II output under Petrobras’ RefTOP program lowers cost barriers, accelerating the synthetic shift in industrial and premium passenger segments. Fleets prioritize total cost of ownership, favoring synthetics that cut downtime. Research from Brazilian universities validates oxidative stability improvements in modified vegetable-oil bases, hinting at future local sourcing opportunities for the Brazil lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

São Paulo and Rio de Janeiro anchor the country’s largest consumption cluster, integrating automotive manufacturing, petrochemicals, and services that demand premium formulations. Minas Gerais contributes a sizable volume of grease and gear oil from Vale-operated mines, which run heavy mobile equipment year-round. The South achieves steady growth through agricultural mechanization and the development of export-oriented automotive assembly lines.

The Northeast posts above-average growth as new refineries, wind farms, and port logistics expand offshore supply chains. Rising FPSO traffic triggers marine-lube requirements along the Bahia and Ceará coasts[2]Energy Research Office, “PDE 2027,” EPE.GOV.BR . Center-West remains an agricultural powerhouse, where tractor hydraulic fluids and specialty oils for ethanol plants are in high demand. Extensive road distances reward distributors with integrated storage, rail, and truck fleets, exemplified by Vibra’s 44 million-liter tank network that underpins national reach.

Border regions pose leakage risks as smugglers exploit regulatory gaps, allowing illicit products to be pushed into interior states. Companies with compliance programs and electronic invoicing can protect their market share. Overall, geographic diversity both complicates logistics and creates multiple demand pockets that stabilize overall growth in the Brazil lubricants market.

Competitive Landscape

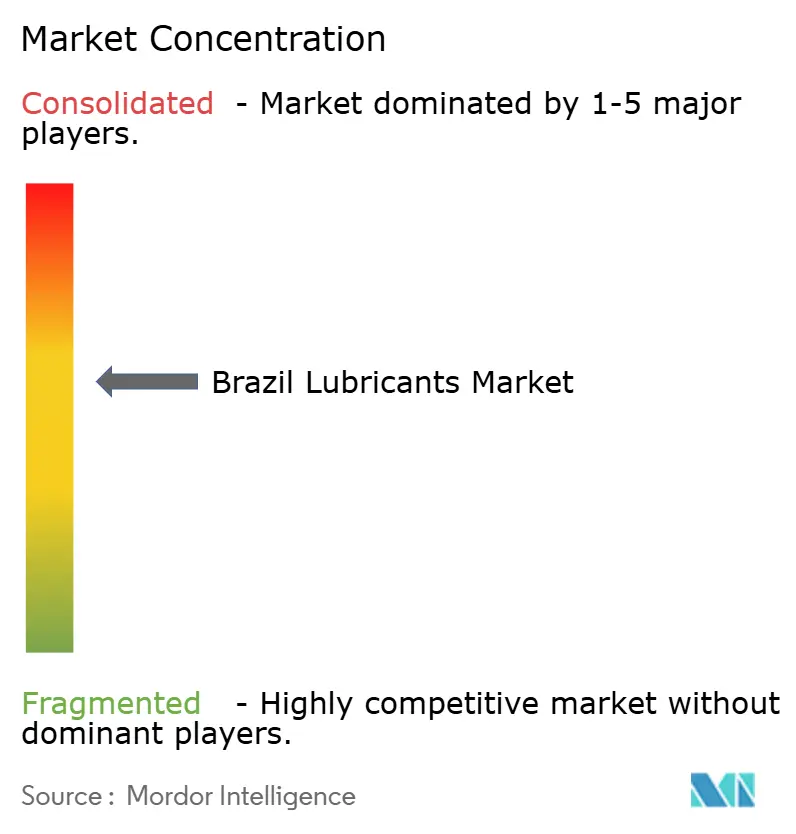

The Brazil Lubricants Market is moderately fragmented. Petrobras Distribuidora (Lubrax), ICONIC Lubrificantes (Chevron–Ipiranga), and Shell vie for leadership, each maintaining multi-channel networks that reach service stations, quick-lube centers, and OEM dealerships. Portfolio sustainability is another battleground. Petrobras began pilot production of cellulosic-content fuels in early 2025, supplying low-carbon base stocks for eco-label lubricants. ICONIC launched biobased hydraulic fluids verified under ANP’s RenovaCalc pathway, and Shell tests re-refined blends with OEM partners. As OEM emission targets tighten, the supplier's ability to certify cradle-to-gate footprints will likely determine future channel partnerships, reinforcing the premium segment but compressing margins in conventional volumes.

Brazil Lubricants Industry Leaders

-

Petrobras

-

Shell plc

-

ExxonMobil Corporation (Cosan)

-

Chevron Corporation (Iconic)

-

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: German lubricant manufacturer FUCHS has committed BRL 220 million to a new Sorocaba production complex, aiming to double its market share in Brazil and expand its supply across Latin America.

- November 2024: Vibra Energia acquired the Lubrax factory in Duque de Caxias, increasing the annual capacity of lubricants by 53.3% and deepening its vertical integration.

Brazil Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected volume for the Brazil lubricants market in 2030?

Forecasts indicate 1.82 billion liters by 2030, up from 1.56 billion liters in 2025.

How fast is the market expected to grow?

The compounded annual growth rate is estimated to be 3.16% from 2025 to 2030.

Which product type leads consumption?

Automotive engine oils held 44.38% of the 2024 volume, remaining the largest category.

Which end-user segment is growing fastest?

Industrial applications are set to post a 5.04% CAGR through 2030.

How will electric vehicles affect lubricant demand?

EV adoption trims engine oil volume but improves opportunities in e-gear oils and thermal fluids.

Page last updated on: