Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

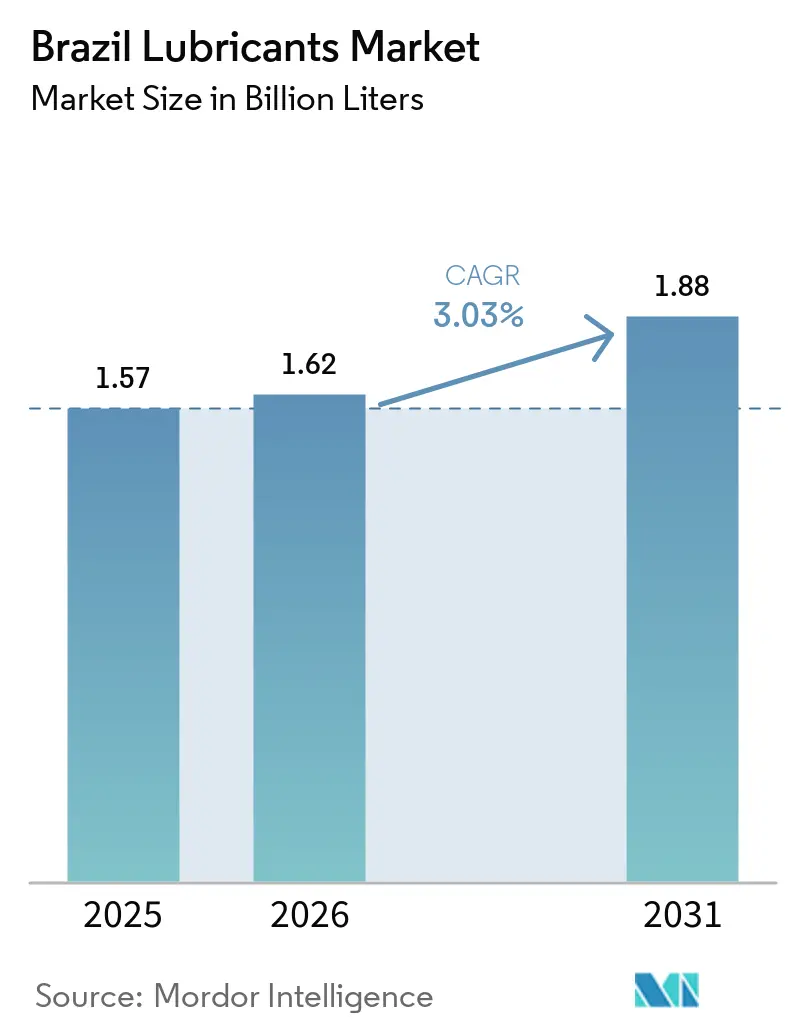

| Base Year Market Size (2025) | 1.57 Billion liters |

| Market Volume (2026) | 1.62 Billion liters |

| Market Volume (2031) | 1.88 Billion liters |

| Growth Rate (2026 - 2031) | 3.03% CAGR |

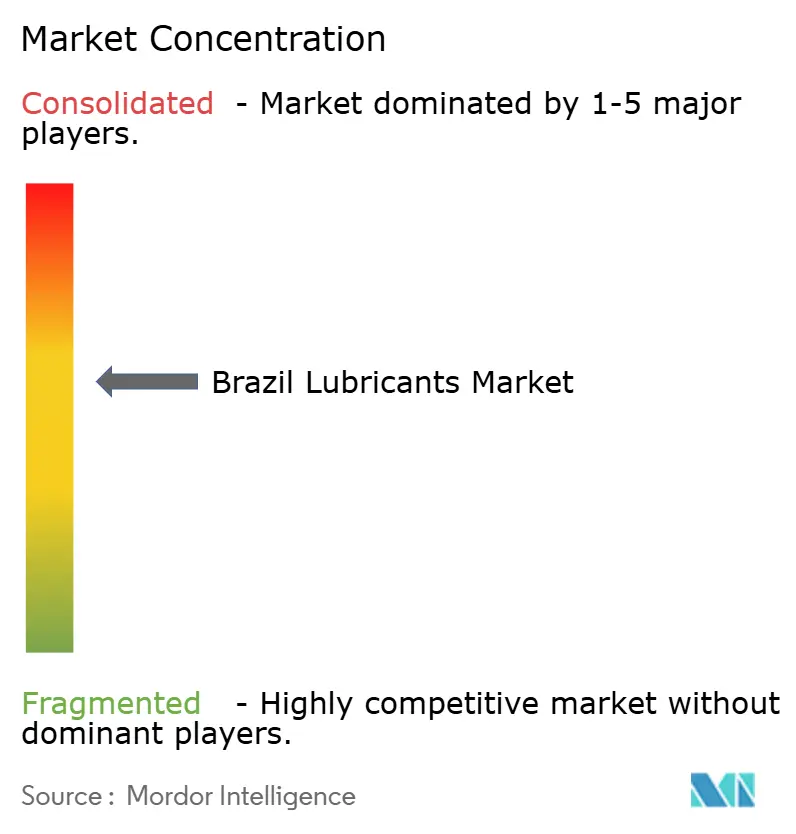

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Lubricants Market Analysis by Mordor Intelligence

The Brazil Lubricants Market size is projected to be 1.57 Billion liters in 2025, 1.62 Billion liters in 2026, and reach 1.88 Billion liters by 2031, growing at a CAGR of 3.03% from 2026 to 2031. Increasing industrial output, stricter sustainability regulations, and renewed infrastructure investments are driving demand for high-performance, lower-viscosity, and biodegradable formulations. Specialty greases for mining, steel, and construction equipment are experiencing growing demand as these industries expand capacity and aim for extended maintenance intervals. Base oil supply imbalances, caused by European refinery closures, are increasing import reliance, prompting Petrobras and private refiners to enhance Group II production capacity and invest in re-refining processes. Additionally, tariff-related delays in battery-electric vehicle adoption are slowing the transition to dedicated e-fluids, leading blenders to focus on dual-use formulations suitable for both internal combustion and hybrid powertrains. Competitive pressures are intensifying as domestic players like Vibra Energia and Iconic Lubrificantes increase blending capacity, while global companies invest in local research and development as well as digital fluid-monitoring solutions.

Key Report Takeaways

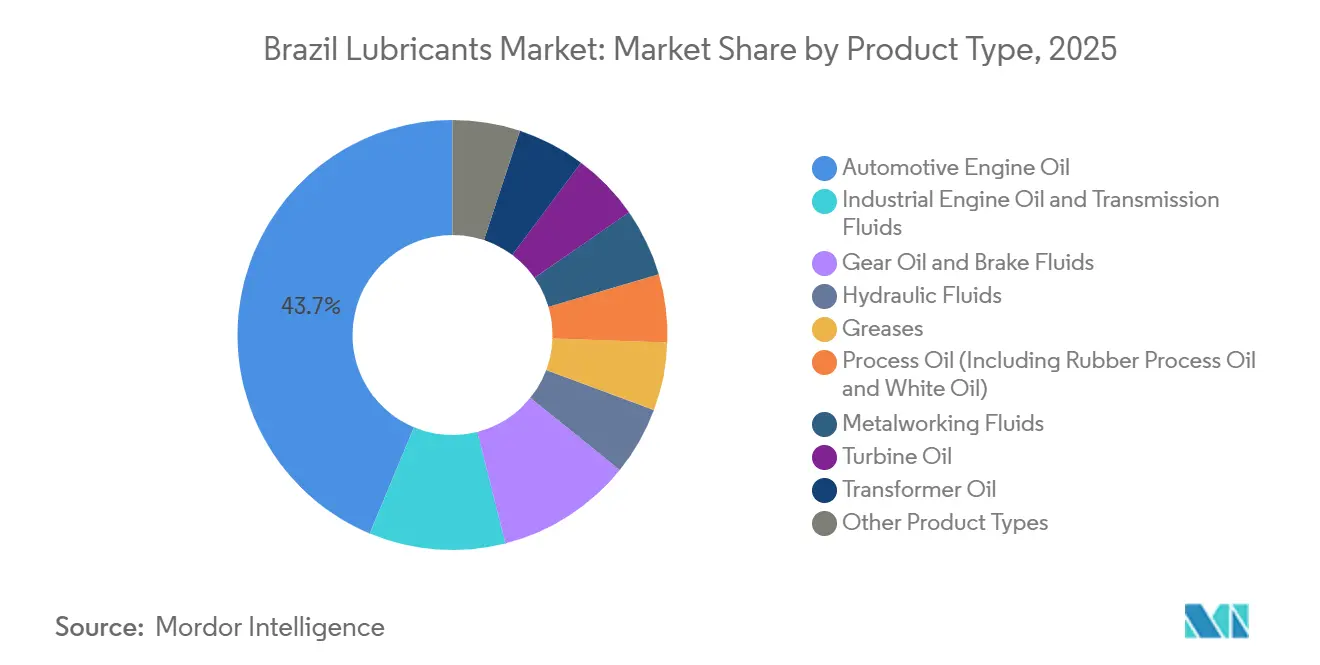

- By product type, automotive engine oil led with 43.72% of the Brazil lubricants market share in 2025, while greases are advancing at a 4.69% CAGR through 2031.

- By base stock type, mineral oil-based lubricants captured 76.32% of the Brazil lubricants market share in 2025, whereas bio-based lubricants are projected to expand at a 4.55% CAGR through 2031.

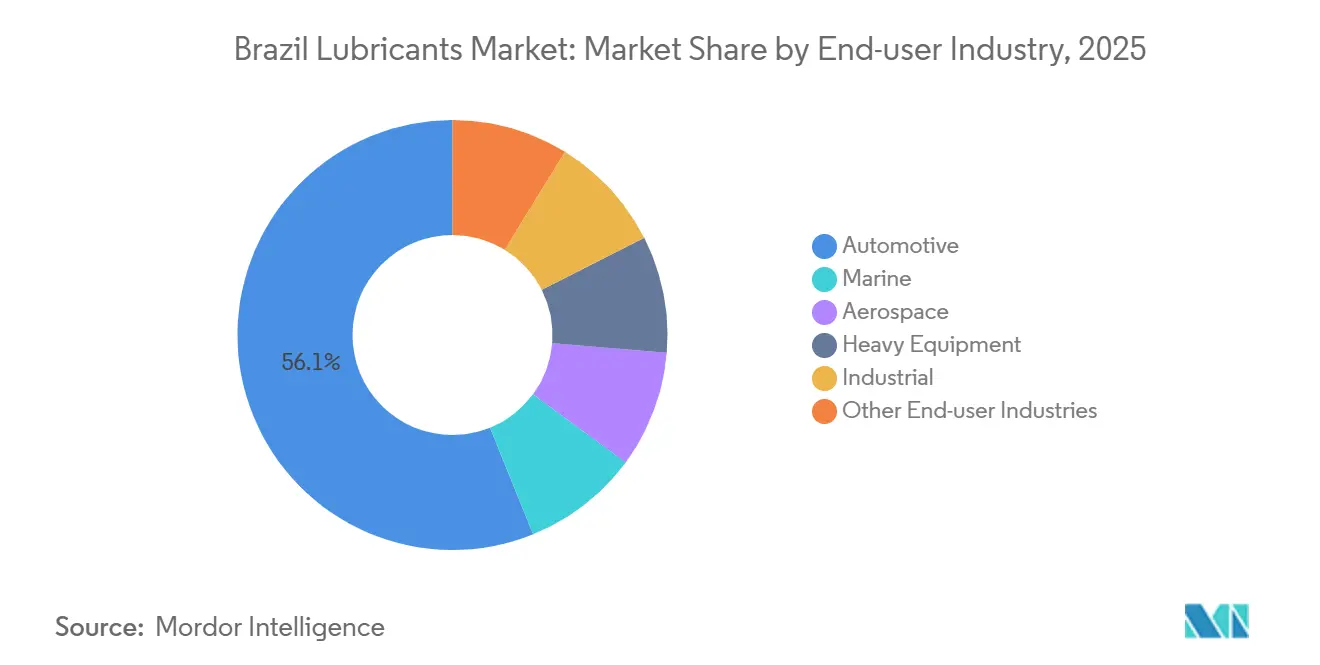

- By end-user industry, automotive accounted for 56.12% of the Brazil lubricants market share in 2025, while the industrial segment is poised to grow at a 4.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing PMI rebound lifting metalworking fluids | +0.6% | National, concentrated in São Paulo, Minas Gerais, and Rio Grande do Sul industrial corridors | Medium term (2-4 years) |

| Electric vehicle-specific e-fluids and thermal-management oils | +0.4% | National, with early adoption in São Paulo, Rio de Janeiro metropolitan fleets | Long term (≥ 4 years) |

| Offshore wind and green hydrogen turbine-fluid demand | +0.2% | Coastal states, including Rio Grande do Sul, Bahia, Ceará, and pilot hydrogen hubs | Long term (≥ 4 years) |

| European Union Batteries Regulation fostering electrolyte know-how | +0.3% | National, particularly São Paulo chemical clusters and automotive OEM supply chains | Medium term (2-4 years) |

| CSRD-driven uptake of re-refined base oils | +0.5% | National, led by multinational subsidiaries and export-oriented manufacturers in Southeast Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Manufacturing PMI Rebound Lifting Metalworking Fluids

Industrial production rose by 1.8% month-on-month in January 2026, maintaining the upward trend that began in mid-2025 as interest rates stabilized and the PMI returned to positive growth. Metalworking fluids are seeing significant gains as automakers and machinery manufacturers increase production to fulfill export contracts and restock inventories. TotalEnergies provides water-based Folia coolants that reduce consumption[1]TotalEnergies, “Folia Metalworking Fluids,” totalenergies.com , while PETRONAS’s IoT-enabled Fluid-i platform extends service life to 12,000 hours, cutting disposal costs. The demand for synthetic and semi-synthetic coolants is growing due to the need for improved chip evacuation in higher-speed CNC machining and tighter tolerances, which is also driving up average selling prices. Automotive production reached 2.64 million units in 2025 and is forecasted to rise to 2.74 million units in 2026, further supporting lubricant demand.

Electric Vehicle-Specific E-Fluids and Thermal-Management Oils

Electrified vehicle sales climbed to 73,000 units in 2025, representing a 60.8% increase and raising their production share to 11.2%. Raízen introduced Shell Helix Ultra Professional AG 0W-20, designed for hybrids requiring lower viscosity and extended drain intervals, utilizing PurePlus gas-to-liquid technology. However, the federal tariff increase to 35% on imported EVs, effective July 2026, is slowing consumer adoption. Lubricant manufacturers are addressing this by developing dual-use fluids compatible with both ICE and hybrid drivetrains, ensuring flexibility as domestic battery-pack assembly expands.

Offshore Wind and Green Hydrogen Turbine-Fluid Demand

Pilot offshore wind projects along the southern and northeastern coasts, along with green hydrogen hubs at industrial ports, are driving demand for turbine oils that can withstand salt exposure and wide temperature variations. Shell Marine, distributed exclusively by Bunker One under a 2024 agreement, offers biodegradable GTL-based turbine oils with oxidation stability exceeding 10,000 hours. Additionally, electrolyzer compressors in hydrogen plants require contamination-free lubricants. While initial volumes are being imported from Europe, domestic blenders are negotiating additive partnerships to localize supply chains.

European Union Batteries Regulation Fostering Electrolyte Know-How

The EU Batteries Regulation is encouraging Brazilian investments in battery-grade chemicals, which is boosting demand for ultra-clean process oils and specialty greases used in cell assembly lines. Chevron Oronite’s Mauá additives plant is well-positioned to supply friction modifiers tailored for battery-cooling fluids. With Anfavea members committing BRL 140 billion through 2030 for electrified vehicle programs, electrolyte-compatible lubricants are emerging as a complementary product category that leverages existing distribution networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European refinery closures tightening base-oil supply | -0.5% | National, affecting all blenders dependent on imported Group II/III base stocks | Short term (≤ 2 years) |

| Upcoming PFAS ban threatening high-temp greases | -0.3% | National, concentrated in aviation, steel, and mining sectors using specialty greases | Medium term (2-4 years) |

| EV-subsidy withdrawal distorting specialty-fluid mix | -0.4% | National, with acute impact in São Paulo and Rio de Janeiro metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

European Refinery Closures Tightening Base-Oil Supply

Base-oil imports totaled 68,000 tons in December 2025, with Group III oils representing a four-year high of 21%. Reduced refinery throughput in Europe is extending supply chains and increasing freight costs, while domestic production at Petrobras’ Reduc plant continues to decline. The planned Group II capacity expansion at Boaventura is not expected to be operational until 2028. Consequently, blenders are negotiating longer-term contracts and evaluating re-refined alternatives, although the transition is slowed by the need for customer validation.

Upcoming PFAS Ban Threatening High-Temperature Greases

An OECD study published in June 2025 revealed that PFAS-containing greases dominate critical high-temperature applications. Brazil’s new chemical inventory law indicates that domestic restrictions may follow Europe’s regulatory framework. As a precaution, industries such as mills, airlines, and mining operations are reviewing their inventories of PFAS greases in anticipation of potential bans. Suppliers are testing fluorine-free alternatives; however, these products face performance challenges above 200 °C, and aviation certification processes, which can take over three years, add further complexity to the transition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Greases Outpace Engine Oils

Automotive engine oil held 43.72% of the Brazil lubricants market share in 2025. However, greases are projected to grow at a 4.69% CAGR through 2031, driven by demand from heavy machinery and mineral extraction industries. Specialty greases that can withstand high loads, water washout, and extreme heat are essential in steel mills and open-pit mines, where operational uptime is critical. TotalEnergies’ CERAN calcium-sulfonate range reduces consumption by four times compared to lithium-based alternatives, lowering lubrication-related downtime costs for steel producers. Additionally, construction and agricultural machinery are adopting long-life greases that extend relubrication intervals and reduce labor costs, expanding the market share of greases in Brazil's lubricants market.

Hydraulic fluids, metalworking coolants, and turbine oils are also experiencing growth as industrial production recovers. PETRONAS’ Fluid-i monitoring platform enables 12,000-hour hydraulic oil drain intervals, while water-based metalworking fluids assist automakers in meeting plant-level emissions regulations. Turbine oil demand is supported by grid upgrades and the addition of gas-fired power capacity, which require oxidation-stable Group II and Group III synthetic oils. Although brake, process, and transformer oils remain niche products, specialty variants like biodegradable transformer fluids are gaining traction in safety-critical applications such as substations.

By Base Stock Type: Bio-Based Gains Traction

Mineral oil-based lubricants accounted for 76.32% of volumes in 2025, reflecting cost advantages and widespread OEM approvals. Semi-synthetic lubricants, which combine mineral and PAO stocks, balance cost efficiency with fuel economy benefits, making them popular among commercial vehicle fleets. Fully synthetic lubricants, offering oxidation stability exceeding 10,000 hours, remain positioned in the premium segment. Bio-based lubricants are projected to grow at a 4.55% CAGR through 2031, supported by feedstocks such as soybean and sugarcane. Sustainability-focused agribusinesses are increasingly adopting biodegradable hydraulic oils to meet scope-3 emissions targets and avoid soil contamination penalties.

However, price remains a challenge, as vegetable-oil formulations can cost 30% more than mineral-based alternatives and face oxidative stability limitations at high temperatures. Innovations in feedstock and scaling efforts, such as Petrobras’ re-refined base-oil program and Shell/Bunker One’s marine biodegradable product line, are helping to reduce cost disparities. If CSRD reporting requirements expand to include local firms, the adoption of bio-based lubricants could accelerate, making them a strategically significant segment of the Brazil lubricants market.

By End-user Industry: Industrial Segment Drives Growth

The automotive industry accounted for 56.12% of lubricant volumes in 2025, while the industrial segment is expected to grow at a 4.87% CAGR through 2031. Passenger car fleets prefer 5W-30 and 0W-20 multigrade oils for fuel efficiency, while commercial trucks are adopting API CK-4 compliant 15W-40 and 10W-30 blends to meet Euro VI standards, set to be implemented in Brazil by 2027. Two-wheelers represent a high-frequency drain opportunity for lubricant blenders targeting urban delivery operators.

Industrial users, including power generation, metallurgy, mining, and process industries, are the fastest-growing end-user group in the Brazil lubricants market. Gas turbines require oxidation-stable ISO 32 oils that meet GE Frame 7 and Siemens SGT-800 specifications, while steel producers rely on specialty greases resistant to scale and water ingress. Mining operations in Pará and Minas Gerais specify calcium-sulfonate greases with a 200 kgf weld-load capacity to minimize unplanned equipment downtime. Additionally, textile and food processing industries demand NSF-H1-approved white oils to prevent product contamination, further expanding the specialty lubricant market in Brazil.

Geography Analysis

The Southeast region remains the largest contributor to the Brazil lubricants market, driven by São Paulo’s concentration of OEMs, tier-1 suppliers, and energy infrastructure. Key facilities such as Vibra’s 500-million-liter Lubrax plant and FUCHS’ 50,000 tons Sorocaba facility ensure efficient last-mile delivery and strong brand visibility. Rio de Janeiro supports marine lubricant demand through offshore oil fields and hosts Petrobras’ base-oil assets, while Minas Gerais’ iron ore and steel industries drive demand for greases and hydraulic oils.

In the South, agribusiness in Rio Grande do Sul and Paraná supports demand for biodegradable hydraulic oils, while automotive parts plants in Santa Catarina require metal-forming fluids. Early offshore wind and hydrogen projects along the Atlantic coast, though currently small, signal long-term diversification opportunities, particularly for turbine oils.

The Northeast region’s demand is anchored by Bahia’s petrochemical hub and Pernambuco’s Suape complex, which require process oils and marine lubricants. Wind farms in Ceará and Rio Grande do Norte increase grease demand for yaw and pitch bearings. In the Center-West, agribusiness in Goiás and Mato Grosso drives demand for tractor and combine fluids. The North region, dominated by mining operations in Pará and low-density logistics corridors, accounts for the remaining market share. Infrastructure developments, including ports, highways, and rail corridors, are expected to gradually redistribute lubricant demand, although the Southeast will remain the market’s focal point.

Competitive Landscape

The top five suppliers, Iconic Lubrificantes, Shell plc, Exxon Mobil, Petrobras, and TotalEnergies, collectively held an estimated 66% market share in 2025, indicating moderate market concentration. Iconic Lubrificantes leverages dual branding through Ipiranga and Texaco[2]Iconic Lubrificantes, “Corporate Presentation 2026,” iconiclubrificantes.com.br. Raízen integrates Shell’s branding with a 280,000-kL blending plant and 7,900 retail sites, capturing premium synthetic and marine lubricant niches.

International players are expanding their local presence. FUCHS is investing BRL 220 million in a carbon-neutral Sorocaba plant, which will be five times larger than its current facility, aiming to double its market share by 2030. Usiquímica, the exclusive Valvoline licensee, has acquired YPF Lubrificantes and plans to triple its Diadema capacity by 2026, targeting a 3% national market share. Technology platforms like PETRONAS’ Fluid-i and Shell’s LubeAnalyst integrate predictive maintenance into customer operations, transforming product supply into data-driven service contracts. On the feedstock side, Petrobras and Lwart are localizing Group II and re-refined base oil supplies, mitigating import volatility and enhancing ESG compliance for multinational firms under CSRD reporting.

White-space growth revolves around e-fluids, bio-based formulations, and circular-economy base oils. While EV adoption remains limited due to tariffs, Anfavea’s BRL 140 billion investment pipeline suggests future scale, benefiting early adopters of low-viscosity dielectric fluids. Bio-based lubricant penetration remains below 5%, but Brazil’s soybean and sugarcane feedstocks provide a cost advantage as OEM approvals expand. Re-refined base oils are projected to replace up to 30% of virgin imports by 2031, contingent on Petrobras’ and Lwart’s planned expansions, reshaping cost structures and competitive dynamics in the Brazil lubricants market.

Brazil Lubricants Industry Leaders

Petrobras

Shell plc

Exxon Mobil Corporation (Cosan)

BP p.l.c.

ICONIC Lubrificantes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vibra, Brazil's largest fuel distributor, launched a new brand, Vibra Base Oil, marking its entry into the base oil market. The initial product portfolio focused on Group II base oils, sourced through a partnership with a U.S.-based refiner and producer of Group II base oils.

- May 2025: FUCHS invested over BRL 220 million (USD 39 million) to construct a new lubricant blending plant in Sorocaba, Brazil. This investment was expected to strengthen the company's position in the lubricant market and enhance supply capabilities in Latin America.

Brazil Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The Brazil lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

How large is the Brazil lubricant market?

The Brazil lubricant market stands at 1.62 billion liters in 2026 and is projected reach 1.88 billion liters by 2031.

Which product type is growing the quickest through 2031?

Greases lead with a 4.69% CAGR through 2031, thanks to rising equipment uptime requirements in mining, steel, and construction.

What share did mineral oil-based lubricants hold in 2025?

Mineral oil-based lubricants represented 76.32% of the 2025 volume.

Why are re-refined base oils gaining attention?

They cut CO₂ emissions up to 50% versus virgin stocks and help multinationals comply with CSRD scope-3 reporting, prompting Petrobras and Lwart to expand domestic capacity.

Page last updated on: