Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

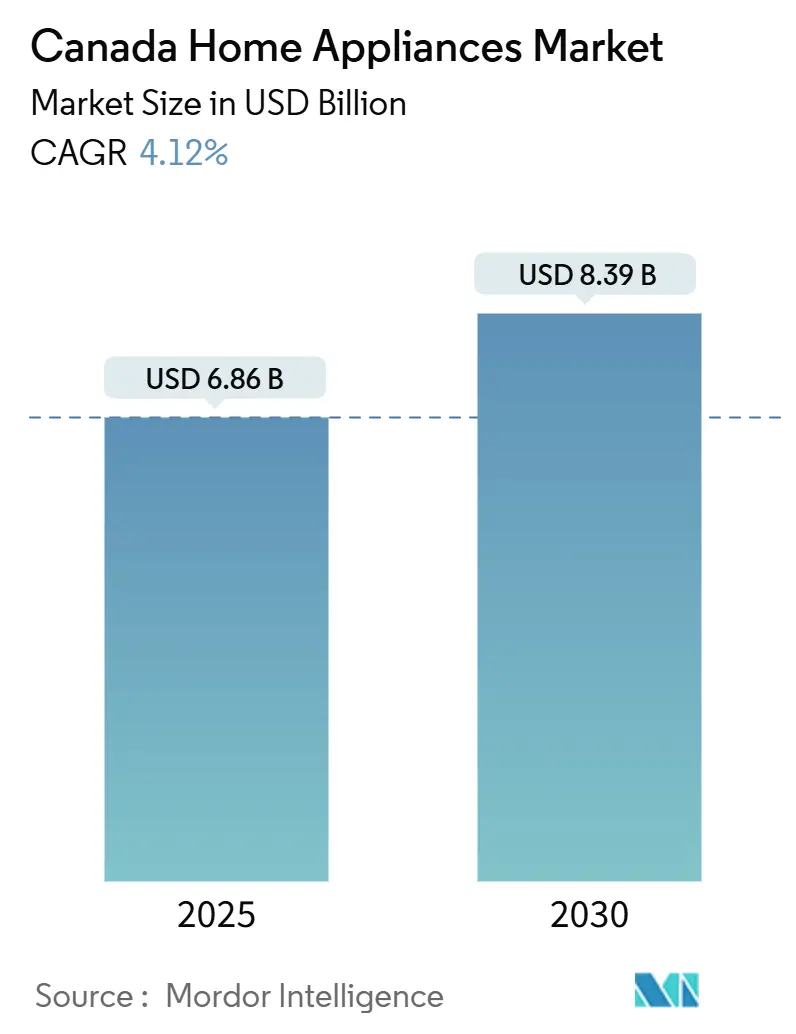

| Market Size (2025) | USD 6.86 Billion |

| Market Size (2030) | USD 8.39 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Home Appliances Market Analysis by Mordor Intelligence

The Canada home appliances market size stands at USD 6.86 billion in 2025 and is forecast to reach USD 8.39 billion by 2030, reflecting a 4.12% CAGR over the period. Immigration-led household formation, energy-efficiency rebate programs, and rapid smart-technology adoption combine to keep demand resilient even as macroeconomic conditions fluctuate. Appliance prices fell 1.2% in 2024, cushioning consumers from broader inflation and stimulating replacement purchases. Retail e-commerce sales grew 6.8% the same year, underscoring a structural shift toward online channels for both major and small appliances[1]Statistics Canada, “Retail E-commerce Sales,” statcan.gc.ca. Federal and provincial rebates worth up to CAD 12,000 per household accelerate the uptake of Energy Star-certified models, while manufacturer financing and subscription plans lower ownership barriers. Geographic concentration remains pronounced, with Ontario leading but Alberta expanding fastest as energy-sector prosperity and interprovincial migration lift disposable incomes.

Key Report Takeaways

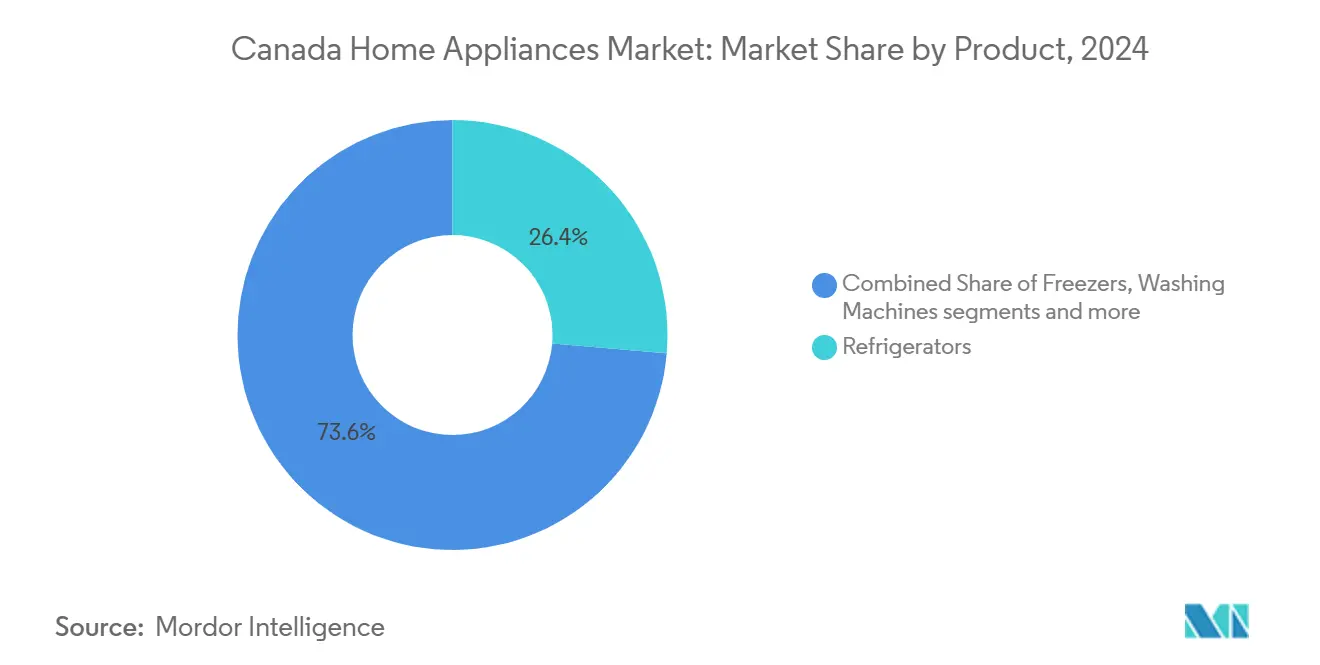

- By product category, refrigerators led with 26.36% of Canada's home appliances market share in 2024, while air fryers advanced at the highest 4.57% CAGR through 2030.

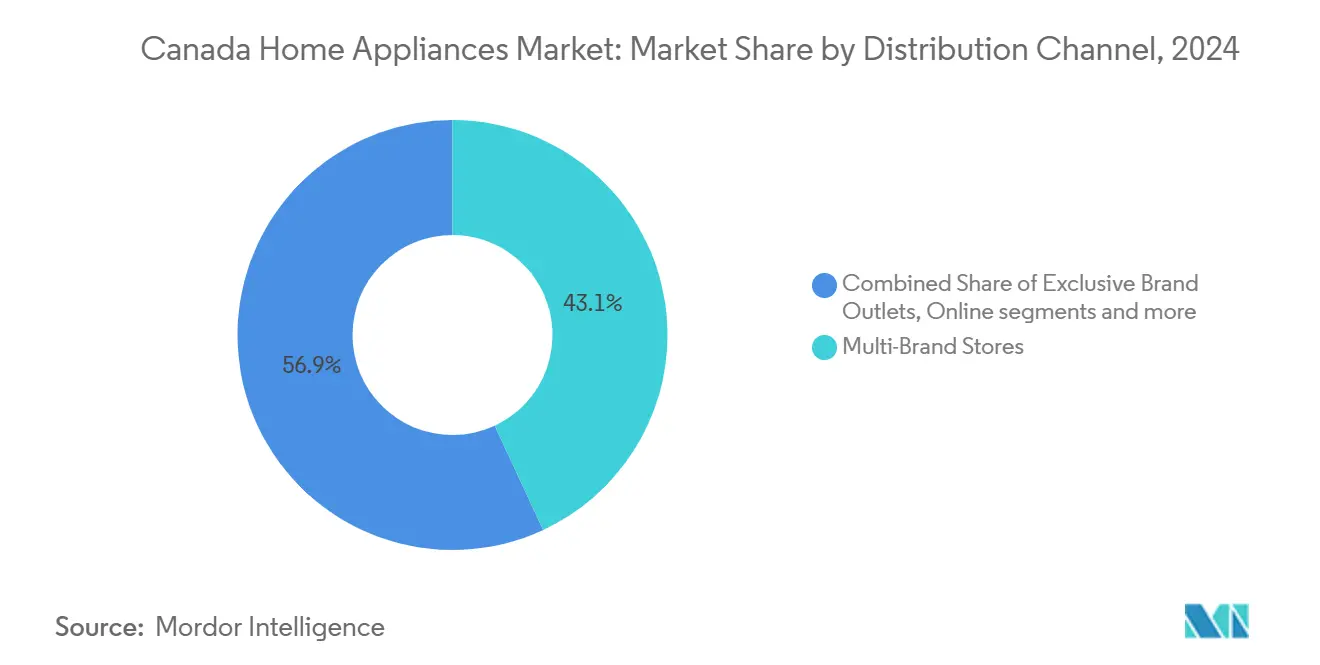

- By distribution channel, multi-brand stores held 43.07% share of the Canada home appliances market size in 2024, whereas online retailing is projected to expand at a 5.30% CAGR to 2030.

- By geography, Ontario accounted for 38.43% of the Canada home appliances market in 2024, and Alberta is forecast to grow at a 4.29% CAGR through 2030.

Canada Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & urban migration | +0.8% | Ontario, British Columbia, Alberta | Medium term (2–4 years) |

| Federal & provincial energy-efficiency rebates | +1.2% | National (higher in Ontario, Quebec) | Short term (≤ 2 years) |

| Expansion of e-commerce retailing | +0.9% | National, urban centers | Medium term (2–4 years) |

| Rapid smart-home device adoption | +0.7% | Ontario, British Columbia | Long term (≥ 4 years) |

| Immigration-led household formation surge | +1.1% | Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| OEM financing & subscription models | +0.5% | National, urban-focused | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Urban Migration

Income gains in energy-rich Alberta and tech-focused British Columbia translate into greater purchasing power for premium refrigerators, washers, and built-in cooking suites. Urban migration concentrates demand in high-density housing where consumers favor compact, multifunctional, and smart-enabled models that optimize limited space. Housing market recovery in major metropolitan areas triggers appliance purchases tied to new construction and renovation cycles[2]Canada Mortgage and Housing Corporation, “Housing Market Outlook,” cmhc-schl.gc.ca. Interprovincial in-migration to Alberta amplifies this effect by adding younger households with above-average disposable incomes. Across Toronto and Vancouver, condominium dwellers increasingly select counter-depth refrigerators and ventless dryers designed for smaller footprints.

Federal & Provincial Energy-Efficiency Rebates

Canada Greener Homes Grant and parallel provincial schemes deliver cash incentives up to CAD 12,000 per household, advancing replacement timelines for washers, dishwashers, and heat-pump dryers[3]Natural Resources Canada, “Canada Greener Homes Grant,” nrcan.gc.ca. Retailers report sales spikes during rebate windows as shoppers bundle multiple qualifying purchases to maximize benefits. Energy Star certification becomes a primary filter in online searches, steering share toward brands with robust high-efficiency portfolios. The rebate landscape also strengthens demand for induction cooktops and inverter refrigerators that meet stringent consumption thresholds. Manufacturers capitalize by marketing lifetime utility savings alongside up-front rebate amounts to justify premium pricing.

Expansion of E-commerce Retailing

Online penetration rises on the back of enhanced last-mile logistics, white-glove installation services, and virtual product demos that replicate in-store consultations. Durable-goods e-commerce outpaced overall retail in 2024, highlighting consumer confidence in large-ticket online transactions. Market leaders integrate AI-powered recommendation engines to guide SKU selection and cross-sell extended warranties and subscription filters. Manufacturer direct-to-consumer storefronts reduce distribution costs and capture first-party data critical for iterative product design. Seasonal assortment resets—Best Buy Canada refreshed 40% of its small-appliance lineup for the 2024 holidays—keep online catalogues aligned with evolving trends.

Rapid Smart-Home Device Adoption

Connected refrigerators, AI ovens, and voice-controlled washers gain traction as Wi-Fi coverage and smart-speaker usage proliferate. Samsung’s Bespoke AI appliances debuted in 2024 with machine-learning-driven energy optimization, attracting tech-savvy households seeking convenience and cost savings. Predictive maintenance alerts minimize downtime, extending product lifecycles and reducing long-run ownership costs. Integration with utility-time-of-use schedules aligns appliance operation with lower electricity rates, appealing to budget-conscious consumers facing rising power bills. As interoperability standards mature, cross-brand ecosystems enable centralized control through single interfaces, simplifying adoption hurdles for late-majority buyers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain cost inflation | -0.9% | National | Short term (≤ 2 years) |

| High market saturation & long replacement cycles | -1.3% | Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Rising electricity prices | -0.6% | Ontario, Alberta | Medium term (2–4 years) |

| Repair culture & right-to-repair legislation | -0.4% | Quebec leading, expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Cost Inflation

Persistent freight surcharges and semiconductor shortages extend lead times for smart refrigerators and laundry pairs beyond six months at specialty retailers[4]Coast Appliances, “Product Availability and Lead Times,” coastappliances.ca. Manufacturers respond with selective price hikes, squeezing affordability for budget segments. Higher parts prices inflate repair costs, yet some consumers delay purchases, hoping for discounts once inventories normalize. Companies diversify sourcing and near-shore subassembly to mitigate volatility, but the strategic shift raises capital expenditures in the short term. Retailers hedge through larger safety-stock orders, increasing working capital requirements.

High Market Saturation & Long Replacement Cycles

Refrigerator and washer penetration rates exceed 95% in Ontario and Quebec, limiting organic unit growth to replacement demand. Average major-appliance lifespans of 12–15 years delay repeat purchases, especially when inflation makes consumers price-sensitive. Consequently, brands pivot to smart add-ons and aesthetic customization to trigger mid-cycle upgrades. Saturation intensifies competition, prompting heavier promotion, trade-in schemes, and bundled warranties to capture share without deep discounting. Growth concentrates in emerging categories such as countertop ovens and robotic vacuums, where household penetration remains below 40%.

Segment Analysis

By Product – Major Appliances Anchor Value, Small Appliances Propel Growth

Refrigerators accounted for 26.36% of the Canada home appliances market size in 2024 and continue to dominate replacement spending due to their essential status and high ticket prices. Meanwhile, air fryers post a 4.57% CAGR, exemplifying how health-centric cooking trends reshape small-appliance baskets. Energy-efficient laundry pairs and dishwashers capture rebate-driven demand, while smart ovens gain share by integrating recipe libraries and voice commands. The Canada home appliances market benefits from advanced AI features that personalize cooling zones or adapt wash cycles to fabric loads, raising premium-segment average selling prices. Compact, multifunctional appliances resonate with urban consumers constrained by kitchen space, encouraging purchase of 2-in-1 washer-dryer combos and countertop convection units. Manufacturers invest in aesthetic modularity, enabling color-panel swaps that prolong perceived product relevance without full replacement. As a result, incremental accessory sales emerge as a secondary revenue stream alongside core unit shipments.

Small-appliance categories thrive on fast innovation cycles and lower replacement barriers, allowing brands to test niche features such as auto-dose coffee makers or app-controlled kettles. Canadian households exhibit above-average ownership of specialty food preparation devices, an outcome linked to multicultural culinary habits. Subscription filter programs for water pitchers and vacuum robots deepen customer lock-in, offsetting the lower upfront price of small units. Overall, major appliances secure recurring revenue through extended warranties, while small appliances generate repeat sales via frequent launches. Both dynamics support sustained growth even in a maturing Canada home appliances market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel – Omnichannel Strategies Redefine Shopper Journeys

Multi-brand big-box stores captured 43.07% of the Canada home appliances market in 2024, leveraging scale to negotiate supplier terms and aggregate assortments that satisfy comparison shoppers. In-store displays increasingly emphasize connected experiences, offering interactive demos of smart fridges or voice-enabled dishwashers. Retailers deploy data-driven planograms to optimize floor space, while store-pickup models shorten fulfilment for online orders of air purifiers and countertop grills. At the same time, online sales advance at a 5.30% CAGR, lifted by improved white-glove delivery and installations that once limited e-commerce adoption for large items. Virtual consultations using augmented reality help consumers visualize appliances in situ, reducing return rates and boosting conversion for premium SKUs.

Manufacturers escalate direct-to-consumer efforts, bundling exclusive colourways or early-access launches to drive traffic to branded sites. The omnichannel Canada home appliances market allows shoppers to toggle seamlessly between research, purchase, and after-sales service, aligning with rising expectations for frictionless experiences. Retailers integrate loyalty programs across channels, rewarding purchases of both a USD 2,000 refrigerator and a USD 150 blender within the same ecosystem. Warehouse clubs and independent dealers continue to serve rural pockets but invest in click-and-collect to remain competitive. As fulfillment efficiencies improve, online channels will claim a growing slice of the Canada home appliances market size, although physical showrooms will retain relevance for tactile evaluation of texture and build quality.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Ontario remains the focal point of the Canada home appliances market, accounting for 38.43% share in 2024, supported by dense population clusters in the Greater Toronto Area and robust provincial rebates of up to CAD 12,000 that stimulate accelerated replacement cycles. Retail infrastructure is sophisticated, with flagship experience centers from Samsung, LG, and Whirlpool showcasing smart-home ecosystems and bundled financing plans. E-commerce penetration is highest here owing to logistics density and consumer comfort with online transactions, reinforcing omnichannel dominance.

Alberta is the growth standout, projected to post a 4.29% CAGR through 2030 as energy-sector incomes lift discretionary spending and interprovincial migrants swell household counts. Calgary and Edmonton drive volume through new-build housing and renovation of aging suburban stock. Younger demographics gravitate toward smart, energy-efficient appliances that deliver connectivity and long-term cost savings. Retailers curate assortments heavy on premium French-door refrigerators, induction ranges, and large-capacity washers to match income profiles.

Quebec presents distinct operating parameters shaped by right-to-repair legislation and French-language labeling rules. Bill 29 mandates parts availability, encouraging repair culture that lengthens replacement timelines but increases demand for OEM spare parts. Market consolidation—Groupe Amiel’s 2025 acquisition of Les Spécialistes de l’électroménager—signals maturation and efficiencies across distribution. British Columbia mirrors Ontario’s urban density but exhibits heightened environmental consciousness, boosting penetration of heat-pump dryers and induction cooktops. Prairie and Atlantic provinces adopt a steady replacement rhythm tied to macroeconomic stability, whereas Northern Territories remain a niche constrained by logistics costs and off-grid energy considerations.

Competitive Landscape

The Canada home appliances market features moderate fragmentation, with the top five multinational brands accounting for roughly half of unit sales. Whirlpool, LG, and Samsung leverage global R&D scale, deep retail partnerships, and increasingly aggressive financing offers to protect share in mature product lines. Samsung’s Bespoke AI suite, launched in 2024, underscores the strategic pivot toward personalized, software-rich platforms that lock users into proprietary ecosystems. LG’s ThinQ integration and carbon-neutrality roadmap differentiate on sustainability, meeting regulatory and consumer demands for lower footprints. Whirlpool focuses on mass-premium positioning with fingerprint-resistant finishes and self-cleaning oven technologies.

Supply-chain resilience investments, including near-shoring component production, aim to mitigate freight inflation and component shortages. Meanwhile, domestic mid-tier brands exploit market niches in French-language packaging and region-specific after-sales service, especially in Quebec. Small-appliance specialists such as Breville and SharkNinja gain traction through rapid innovation cycles and direct-to-consumer marketing that bypasses traditional retail gatekeepers. Subscription models for water filters and vacuum consumables create annuity revenue streams, cushioning price competition in core appliance categories. Mergers among independent retailers—Distinctive Appliances’ 2025 purchase of Corbeil—seek scale advantages to negotiate better supplier terms and fund omnichannel capabilities.

Canada Home Appliances Industry Leaders

-

Whirlpool Corporation

-

Electrolux AB

-

Samsung Electronics

-

LG Electronics

-

Electrolux AB

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Groupe Amiel completed the acquisition of Les Spécialistes de l’électroménager for an undisclosed amount, expanding its Quebec market presence and consolidating regional distribution capabilities. The deal adds 12 retail locations, giving Amiel denser coverage in Greater Montreal and Quebec City. Management expects operational synergies in logistics and marketing to sharpen price competitiveness against national chains.

- April 2025: Distinctive Appliances acquired Corbeil Électrique in a CAD 45 million transaction, creating Quebec’s largest independent appliance retail network with 28 combined locations. Corbeil’s strong brand relationships and premium assortment complement Distinctive’s volume-driven model. The merged entity targets CAD 8 million in annual cost savings through unified procurement and shared back-office systems.

- July 2024: LG Electronics unveiled its 2024 Canadian lineup with ThinQ AI across refrigerators, washers, and dishwashers, and announced a CAD 25 million investment to expand Toronto-area service infrastructure. The company reported 15% year-over-year growth in Canadian smart-appliance sales. Expanded service coverage supports faster installations and repairs, reinforcing LG’s premium positioning.

- April 2024: Samsung Electronics launched its Bespoke AI appliance lineup in Canada, featuring machine-learning algorithms for energy optimization and personalized user experiences. Promotional 0% financing for 24 months and trade-in credits up to CAD 1,500 strengthened early adoption. The rollout positions Samsung at the forefront of Canada’s fast-growing smart-appliance niche.

Canada Home Appliances Market Report Scope

Home appliances are machines designed to aid in various household tasks, including cooking, cleaning, and food preservation. These appliances can be broadly classified into three categories, namely major appliances, small appliances, and consumer electronics.

The Canadian home appliance market is segmented by major appliances, small appliances, and distribution channel. By major appliances, the market is segmented into refrigerators, freezers, dishwashing machines, washing machines, and cookers and ovens. By small appliances, the market is segmented into vacuum cleaners, small kitchen appliances, hair clippers, irons, toasters, grills and roasters, hair dryers, and other small appliances. By distribution channel, the market is segmented into multi-brand stores, exclusive stores, online, and other distribution channels. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Prairie Provinces (SK & MB) |

| Atlantic Canada |

| Territories |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Ontario | |

| Québec | ||

| British Columbia | ||

| Alberta | ||

| Prairie Provinces (SK & MB) | ||

| Atlantic Canada | ||

| Territories | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the value of the Canada home appliances market in 2025?

It is USD 6.86 billion, with a projected rise to USD 8.39 billion by 2030.

Which province shows the fastest growth in appliance demand?

Alberta leads with a forecast 4.29% CAGR to 2030, fueled by energy-sector incomes and migration inflows.

How large is the e-commerce channel in Canadian appliance sales?

Online retail holds a growing share and is expanding at a 5.30% CAGR, reflecting consumer comfort with large-ticket purchases delivered to home.

Which product category commands the largest share?

Refrigerators remain the top category, representing 26.36% of national revenue in 2024.

What incentives exist for energy-efficient appliance purchases?

Federal and provincial rebate programs offer up to CAD 12,000 per household, accelerating replacement of older models.

How are manufacturers lowering upfront costs for premium appliances?

Zero-interest financing up to 24 months and emerging subscription programs bundle payments, maintenance, and upgrade options, making high-end models more affordable.

Page last updated on: