Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

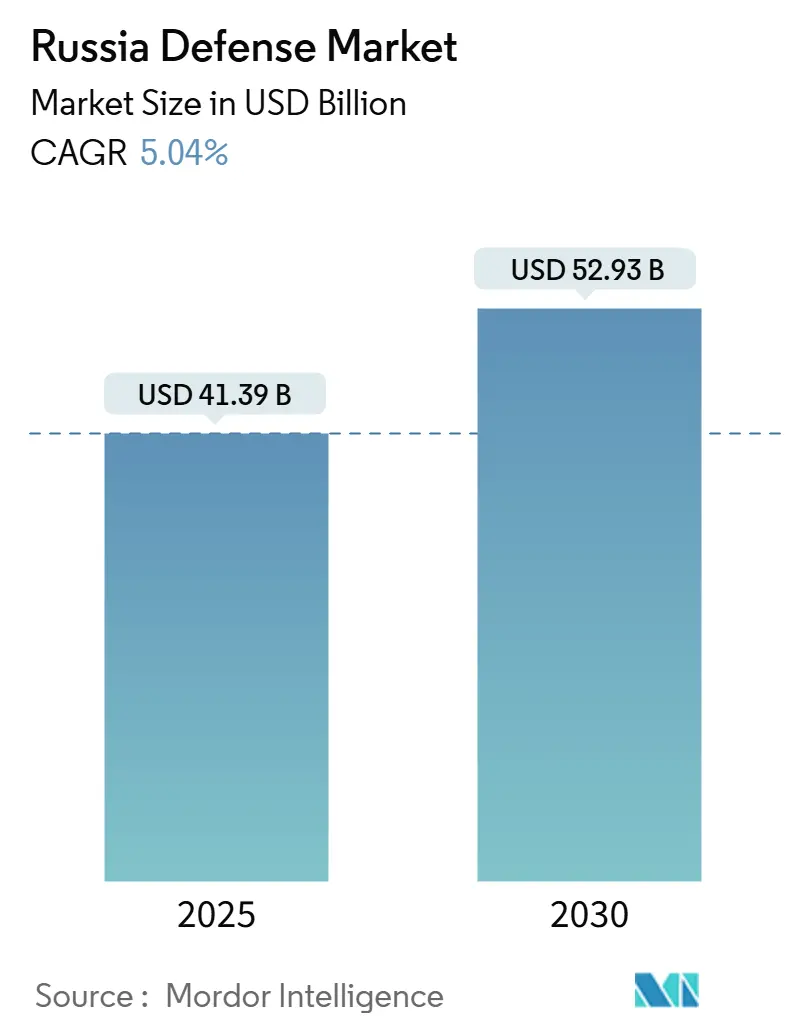

| Market Size (2025) | USD 41.39 Billion |

| Market Size (2030) | USD 52.93 Billion |

| Growth Rate (2025 - 2030) | 5.04% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Defense Market Analysis by Mordor Intelligence

The Russia defense market size was valued at USD 41.39 billion in 2025 and is forecasted to rise to USD 52.93 billion by 2030, reflecting a 5.04% CAGR. Combat losses in Ukraine, Western sanctions, and an ambitious 13.5 trillion ruble defense budget for 2025 (USD 145 billion) combine to drive a mobilization economy that prioritizes output volume over platform novelty. Ammunition production targets have tripled, air-defense deployments now ring core industrial zones, and state conglomerates redirect resources from exports to domestic re-armament. Simultaneously, a 300,000-person labor gap, double-digit inflation, and restricted access to advanced semiconductors erode purchasing power and slow innovation. Strategic opportunities nevertheless exist in unmanned combat systems, counter-drone technologies, and modular armor kits as commanders seek affordable precision effects at scale.

Key Report Takeaways

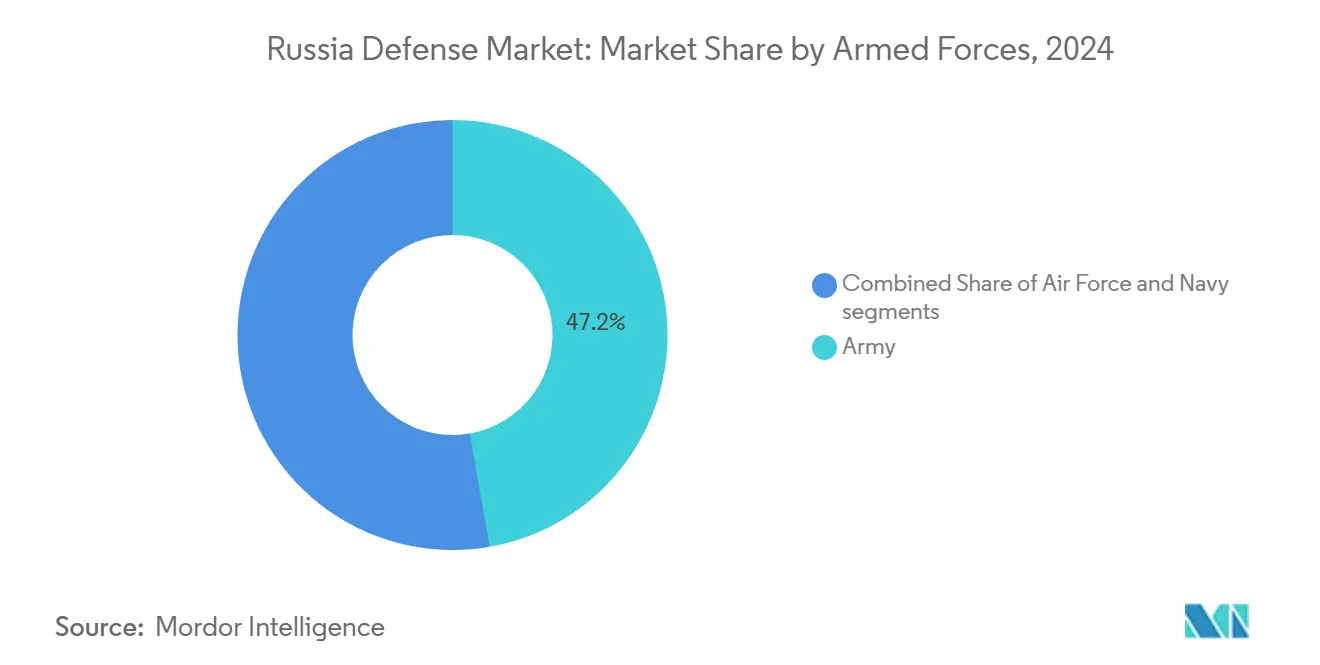

- By armed forces, the Army captured 47.24% of Russia defense market share in 2024, while the air force segment is advancing at a 6.72% CAGR through 2030.

- By type, weapons and ammunition led with 30.11% share of the Russia defense market size in 2024, while the unmanned systems segment is projected to expand at a 7.45% CAGR to 2030.

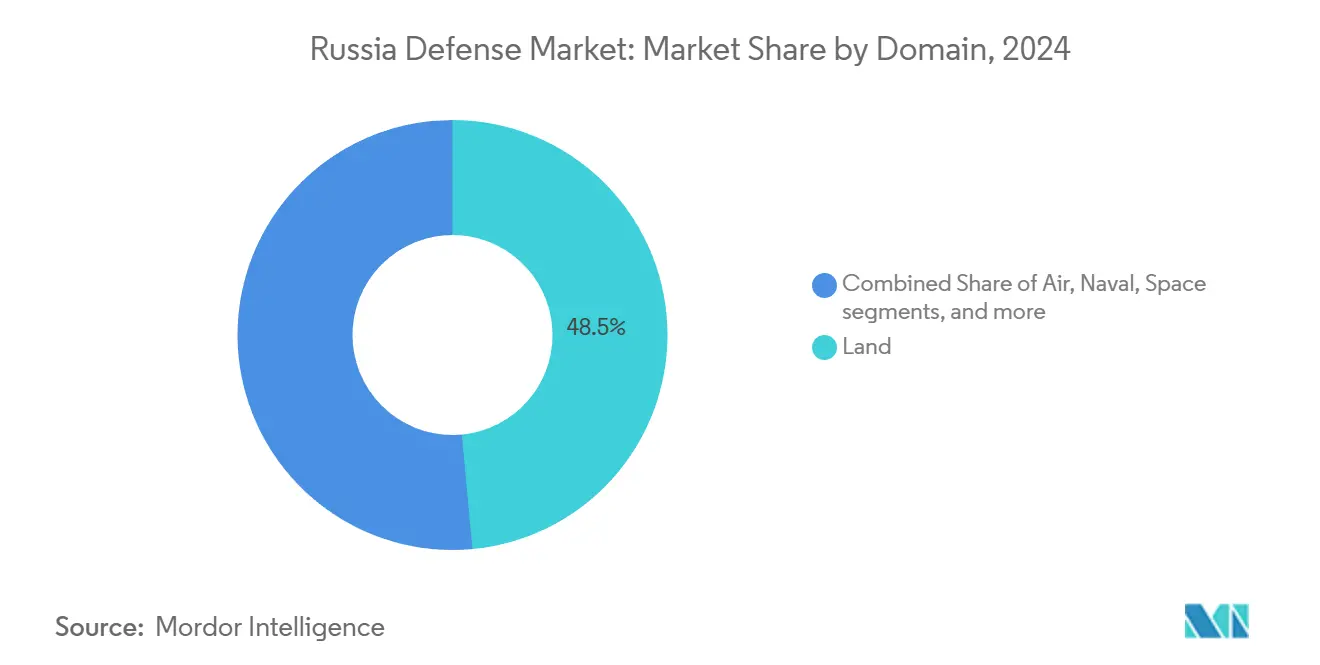

- By domain, the land segment accounted for 48.27% of Russia defense market size in 2024, and the air domain is growing fastest at a 6.21% CAGR.

- By procurement nature, indigenous production dominated the Russia defense market with a 78.86% share in 2024 and is forecasted to grow at a 5.88% CAGR.

Russia Defense Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated ammunition and munitions replenishment requirements | +1.8% | Urals industrial belt (Sverdlovsk, Chelyabinsk, Perm oblasts) | Short term (≤ 2 years) |

| Rising investment in integrated air and missile defense systems | +1.2% | Moscow, St. Petersburg, Crimea, Kaliningrad | Medium term (2-4 years) |

| Rapid recapitalization of ground combat platforms | +1.0% | Nizhny Tagil, Omsk, Kurgan armored-vehicle plants | Short term (≤ 2 years) |

| State-led defense industrial mobilization and capacity expansion | +1.5% | Tatarstan, Nizhny Novgorod, Rostov-on-Don | Medium term (2-4 years) |

| Import substitution and domesticization of critical defense components | +0.8% | Moscow, St. Petersburg design bureaus, Urals facilities | Long term (≥ 4 years) |

| Increased adoption of cost-effective unmanned and loitering munition systems | +0.9% | Donbas and southern Ukraine operational zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Ammunition and Munitions Replenishment Requirements

Artillery-centric combat has driven shell demand from an estimated 10 million rounds fired in 2022–2023 to annual production goals nearing 4 million rounds by 2026. Factories in Sverdlovsk and Chelyabinsk now run three shifts and reactivated Soviet-era lines to supply Grad rockets, mortar bombs, and anti-tank guided missiles (ATGMs). Quality control cycles are shorter, resulting in higher dud rates, yet commanders accept this trade-off to maintain volume. Tactical Missiles Corporation boosts Kalibr cruise-missile output despite turbofan shortages, while Urals plants focus on 152-millimeter shells. The ammunition surge remains central to offensive doctrine, underpinning the Russia defense market’s near-term growth trajectory.

Rising Investment In Integrated Air and Missile Defense Systems

UAV strikes on refineries and airbases more than 1,000 kilometers from the front have elevated domestic air defense to an existential priority. Almaz-Antey fielded the first S-500 batteries around Moscow in 2024, complementing 60 operational S-400 battalions. Resources originally earmarked for exports are redirected to reinforce St. Petersburg, Crimea, and Kaliningrad. Electronic-warfare (EW) assets such as Murmansk-BN and Krasukha-4 form outer layers that jam communications and airborne radars.[1]Patrick Tucker, “Russia Deploys Murmansk-BN Electronic Warfare System,” Defense One, defenseone.com Counter-drone procurement lags, however, leaving gaps filled by improvised RF jammers and shotgun teams. Together, these programs fuel the Russia defense market as air-space security becomes a budget imperative.

State-Led Defense Industrial Mobilization and Capacity Expansion

The Kremlin condensed a decade of modernization into two years by mandating wartime operating tempos across strategic plants. Uralvagonzavod increased T-90M tank production to over 200 units in 2024 by utilizing simplified assembly lines. United Shipbuilding Corporation launched the Yasen-M submarine Perm in March 2025, maintaining a pace of one boat every 18 months despite sanctions on precision machinery. Russian Helicopters sustained Ka-52M and Mi-28NM deliveries by cannibalizing export lots. Second-tier suppliers, such as Shvabe, scaled thermal sights, and RTI Systems, doubled the production of radar components. This surge redirects engineers from civil programs, yet it anchors the Russia defense market over the medium term.

Increased Adoption Of Cost-Effective Unmanned And Loitering Munition Systems

Low-cost precision platforms now deliver effects once reserved for manned aviation. Zala Aero’s Lancet loitering munition costs about USD 35,000 yet neutralizes howitzers worth millions. Geran-2 one-way attack drones, reverse-engineered from Iranian designs, achieve a monthly production rate of over 1,000 units. Kronstadt’s Orion MALE UAV entered full-rate output in 2024, offering persistent ISR without pilot risk. Early operator training deficits led to high attrition in 2022; however, dedicated UAV battalions and encrypted data links have since improved sortie rates. These developments expand the Russia defense market by combining affordability with sustained lethality.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor and engineering talent constraints in defense manufacturing | -0.7% | Moscow, St. Petersburg design bureaus, Urals plants | Medium term (2-4 years) |

| Supply chain disruptions in advanced electronics and micro-components | -0.9% | Nationwide dependence on Chinese imports | Long term (≥ 4 years) |

| Fiscal pressures affecting long-term defense capital expenditure | -0.6% | National budget-allocation tensions | Medium term (2-4 years) |

| Modernization limitations linked to legacy platform dependence | -0.5% | Urals tank plants, Severodvinsk shipyards, legacy aircraft works | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor and Engineering Talent Constraints In Defense Manufacturing

Defense firms advertised more than 300,000 vacancies by mid-2024, covering CNC machinists, avionics technicians, and software engineers. Mobilization drafted many specialists, leaving design bureaus operating at 60-70% capacity. Salary hikes of 30% merely reshuffled scarce talent regionally. Vocational schools require up to three years to produce competent technicians, which is often misaligned with near-term production spikes. The emigration of IT professionals further drains expertise, while older Soviet-trained staff stay beyond retirement, creating knowledge-transfer bottlenecks that cap Russia's defense market efficiency.

Supply Chain Disruptions In Advanced Electronics and Micro-Components

Export controls eliminated Western semiconductors and precision machine tools, pushing Russian firms toward Chinese parts that add cost and uncertainty.[2]Financial Times Reporters, “Sanctions Force Russia to Rely on Chinese Chips,” Financial Times, ft.com Domestic foundries cannot produce chips below 28 nanometers, limiting the performance of fire-control computers and avionics. Thermal imagers once sourced from Thales are now relying on lower-resolution domestic alternatives, while gaps in machine tools slow down turbine blade fabrication. Programs such as Zircon and Su-57 face recurring delays and design compromises. These shortages impose a structural drag on the Russia defense market outlook beyond 2028.

Segment Analysis

By Armed Forces: Army Dominance Masks Air Force Acceleration

The Army retained 47.24% of 2024 spending within the Russia defense market and continues to absorb the bulk of ammunition, armor, and field-repair budgets. Air Force allocations, although smaller, are increasing at a 6.72% CAGR as helicopter losses spur the procurement of Ka-52M and Mi-28NM, and Su-34M deliveries refresh strike capacity.[3]Reuters Staff, “Russia Su-34M Deliveries,” Reuters, reuters.com Naval programs advance more slowly due to complex shipyard cycles and propulsion bottlenecks, despite the Arkhangelsk submarine's entry into service in 2024.

Ground forces dominate the Russia defense market in terms of consumables, logistics vehicles, and in-theater electronics. Meanwhile, the Air Force maintains strategic relevance by integrating layered S-500 defenses and sustaining frontline fighter aviation. Navy budgets hinge on Sevmash's ability to maintain a nuclear-submarine production line and Zelenodolsk's frigate output, both of which are sensitive to turbine supplies. Together, these patterns reveal a posture optimized for land warfare yet increasingly aware that air control multiplies ground effectiveness.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Unmanned Systems Surge Reshapes Procurement Mix

Weapons and ammunition held 30.11% of the Russia defense market share in 2024, buoyed by 1.3 million shells produced and plans to triple capacity. Unmanned systems drive growth at a 7.45% CAGR, as the Lancet and Geran-2 platforms deliver precision at economies of scale unattainable with cruise missiles. Vehicles, notably the T-90M tanks, maintain a steady output of over 200 units per year. C4ISR and electronic-warfare demand rise in parallel; Murmansk-BN systems now create theater-wide denial bubbles, while Krasukha-4 jammers shield key infrastructure.

Persistent shortfalls in night-vision sensors and secure communications underscore the limits of import substitution. Nonetheless, UAV integration at the battalion level, plus Orion MALE UAVs providing theater surveillance, cements unmanned systems as a structural pillar of the Russia defense market.

By Domain: Land Primacy Gives Way To Air Defense Urgency

Land operations consumed 48.27% of the 2024 value, mirroring artillery exchanges and armored thrusts along the 1,000-kilometer front. Air spending outpaces all other domains at a 6.21% CAGR, driven by S-400 redeployments, S-500 rollouts, and rotary-wing fleet renewal. Naval allocations rise modestly as Yasen-M submarines maintain a steady drumbeat, while lower-cost corvette programs encounter engine delays.

Air domain ascendance within the Russia defense market reflects not only the defense of strategic cities but also a broader doctrine favoring standoff strikes that conserve high-value aircraft. Land budgets are pivoting toward counter-battery radars and modular armor, rather than new tank lines, illustrating a shift from massed steel to survivability.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Procurement Nature: Indigenous Production Dominates Amid Import Substitution

Indigenous production accounted for 78.86% of spending in 2024 and is set to grow at a 5.88% CAGR, reflecting necessity as much as strategy. Import channels for avionics, sensors, and propulsion were collapsed, redirecting billions of dollars to domestic supply chains. Success stories include Shvabe’s thermal sights and United Engine Corporation’s AL-31F turbofans. Yet, 90% of defense electronics still trace back to Chinese intermediaries, underlining future risks.

Foreign procurement remains limited to components that are unavailable domestically, often necessitating longer lead times and higher costs. The Russia defense market thus grows around entrenched verticals, such as armor, artillery, and helicopters, while advanced subsystems remain hostage to external dependencies.

Geography Analysis

Russia consolidates defense production across three Soviet-era corridors. The Urals belt dominates in ammunition and armor: Uralvagonzavod in Nizhny Tagil builds over 200 T-90M tanks annually, and Sverdlovsk plants target 4 million shells annually. The Volga cluster hosts Kazan Aviation Plant, which assembles Tu-160M bombers, and Sokol Aircraft Plant, which overhauls Su-34 fighters.

Northwest yards drive naval power. Sevmash in Severodvinsk launched the Yasen-M submarine Perm in March 2025 and commissioned Arkhangelsk in December 2024.[4]Naval News Staff, “Russia Launches Yasen-M Submarine Perm,” Naval News, navalnews.com Admiralty Shipyards in St. Petersburg builds Lada-class submarines, while Kaliningrad’s Zelenodolsk yard manages Project 22350 frigates, though propulsion shortages stretch timelines.

Far Eastern Komsomolsk-on-Amur produces Su-35 and Su-57 fighters for Pacific aviation, leveraging its proximity to Asian supply routes. However, the distance from European suppliers raises logistics costs. Rostov-on-Don’s Rostvertol plant completes Mi-28NM helicopters, but labor shortages across Moscow and Saint Petersburg compel overtime and rehiring of retirees. The dispersion safeguards assets from border threats yet complicates supply chain coordination within the Russia defense market.

Competitive Landscape

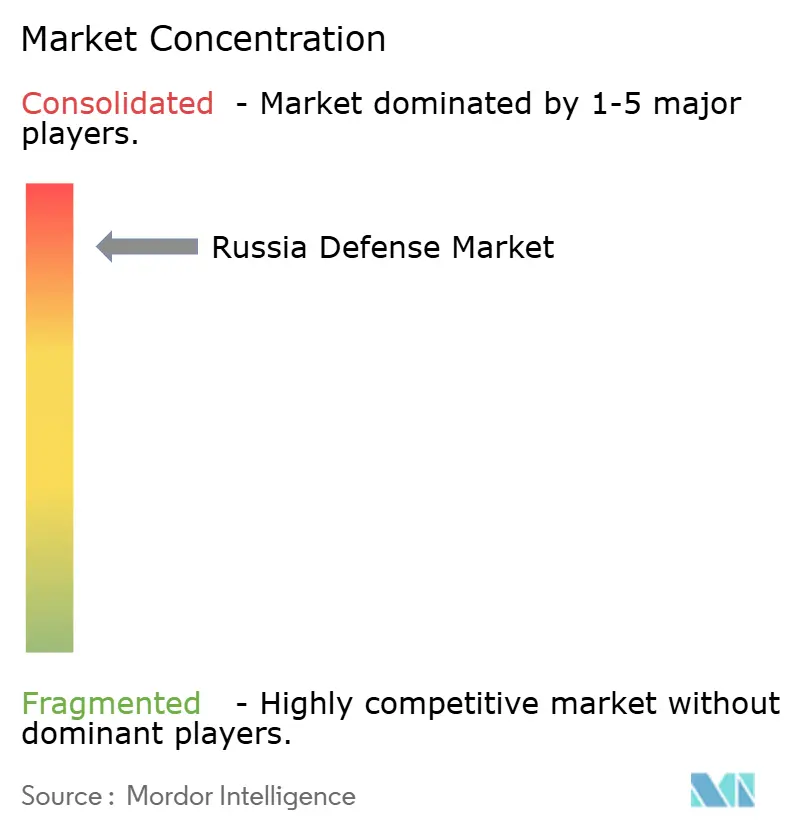

Almaz-Antey Air and Space Defence Corporation, United Aircraft Corporation, United Shipbuilding Corporation, 'Russian Helicopters' JSC, and Kalashnikov Concern JSC control a significant share of production, confirming a highly concentrated Russian defense market. United Shipbuilding Corporation monopolizes naval construction, and United Engine Corporation anchors propulsion.

Strategic emphasis favors proven designs over R&D: Uralvagonzavod scales T-90M throughput instead of fielding the T-14 Armata; Tactical Missiles Corporation extends Kalibr serial runs rather than fast-tracking next-gen hypersonics. Niche firms such as Kronstadt Group thrive by supplying Orion and Sirius UAVs free of foreign intellectual property, while Shvabe accelerates domestic optics to replace sanctioned imports.

Patent filings and lab budgets declined after 2022 as resources channeled into volume production. Testing cycles are shortened, risking quality lapses, yet Kremlin oversight ensures funding continuity. The Russia defense industry thus functions less as a competitive arena and more as a mobilization enterprise that prizes scale, vertical integration, and resilience to sanctions.

Russia Defense Industry Leaders

-

Almaz-Antey Air and Space Defence Corporation

-

United Aircraft Corporation

-

United Shipbuilding Corporation

-

Kalashnikov Concern JSC

-

'Russian Helicopters' JSC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Russia's fifth-generation Su-57 stealth fighter completed its first test flight using the advanced Izdeliye 177 engine.

- June 2025: Russia announced that it would deliver the two remaining squadrons of S-400 surface-to-air missile systems to India by 2026-2027.

- May 2022: Uralvagonzavod, part of the UVZ concern of the Rostec State Corporation, solemnly dispatched a train of T-90M "Proryv" tanks to the Russian MoD.

Russia Defense Market Report Scope

The Russian defense market encompasses all aspects of military vehicles, armaments, and other equipment procurements, as well as upgrade and modernization plans. The report also provides insights into the country's budget allocation and spending in the past, present, and forecast periods.

The Russian defense market is segmented by armed forces (air force, army, and navy), type (personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems), domain (land, air, naval, space, and cyber and electromagnetic spectrum), and procurement nature (indigenous production, and foreign procurement). The report offers market size and forecast for all the above segments in terms of value (USD billion).

By Armed Forces

| Air Force |

| Army |

| Navy |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Russia defense market in 2025?

The Russia defense market size stands at USD 41.39 billion in 2025.

What is the expected growth rate for Russian defense spending through 2030?

Spending is projected to grow at a 5.04% CAGR, lifting total value to USD 52.93 billion by 2030.

Which segment is expanding fastest within Russian defense procurement?

Unmanned Systems lead with a 7.45% CAGR driven by Lancet and Geran-2 drone production.

Which armed service receives the largest share of Russia’s defense budget?

The Army holds 47.24% of total outlays, reflecting ground combat’s centrality.

What is the role of indigenous production in Russia’s defense supply chain?

Indigenous production accounts for 78.86% of procurement and is expanding as import options dwindle.

Page last updated on: