Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

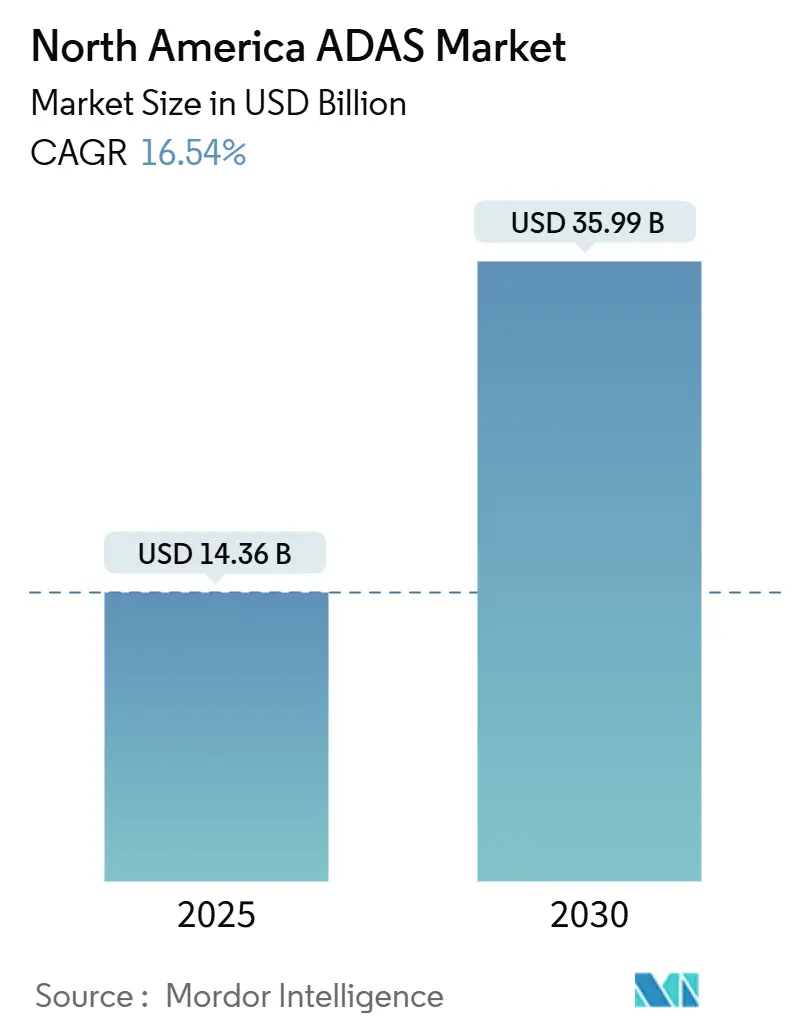

| Market Size (2025) | USD 14.36 Billion |

| Market Size (2030) | USD 35.99 Billion |

| Growth Rate (2025 - 2030) | 16.54% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America ADAS Market Analysis by Mordor Intelligence

The North America ADAS Market size is estimated at USD 14.36 billion in 2025, and is expected to reach USD 35.99 billion by 2030, at a CAGR of 16.54% during the forecast period (2025-2030). Underscoring a swift shift toward advanced safety and automation features across passenger and commercial vehicles. Intensifying federal safety rules, notably the National Highway Traffic Safety Administration’s requirement that all light vehicles incorporate automatic emergency braking by September 2029, is the largest catalyst for near-term demand growth.[1]“Federal Motor Vehicle Safety Standard No. 127,” National Highway Traffic Safety Administration, nhtsa.gov.

Key Report Takeaways

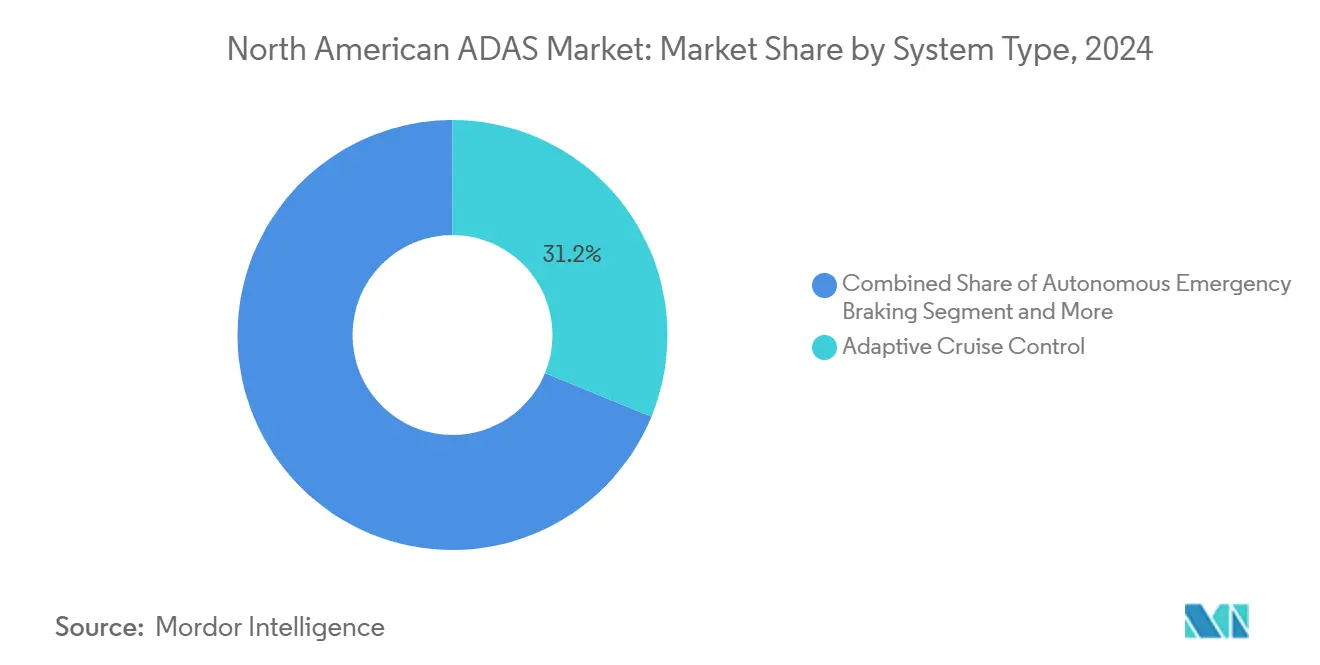

- By system type, adaptive cruise control held a 31.17% revenue share of the North American ADAS market in 2024, whereas traffic sign recognition is projected to expand at a 25.78% CAGR through 2030.

- By sensor technology, radar led with 33.74% North American ADAS market share in 2024 while LiDAR is poised for the fastest 23.14% CAGR to 2030.

- By vehicle type, passenger cars commanded 68.71% of the North American ADAS market size in 2024, yet two-wheelers are forecast to grow at an 18.78% CAGR through 2030.

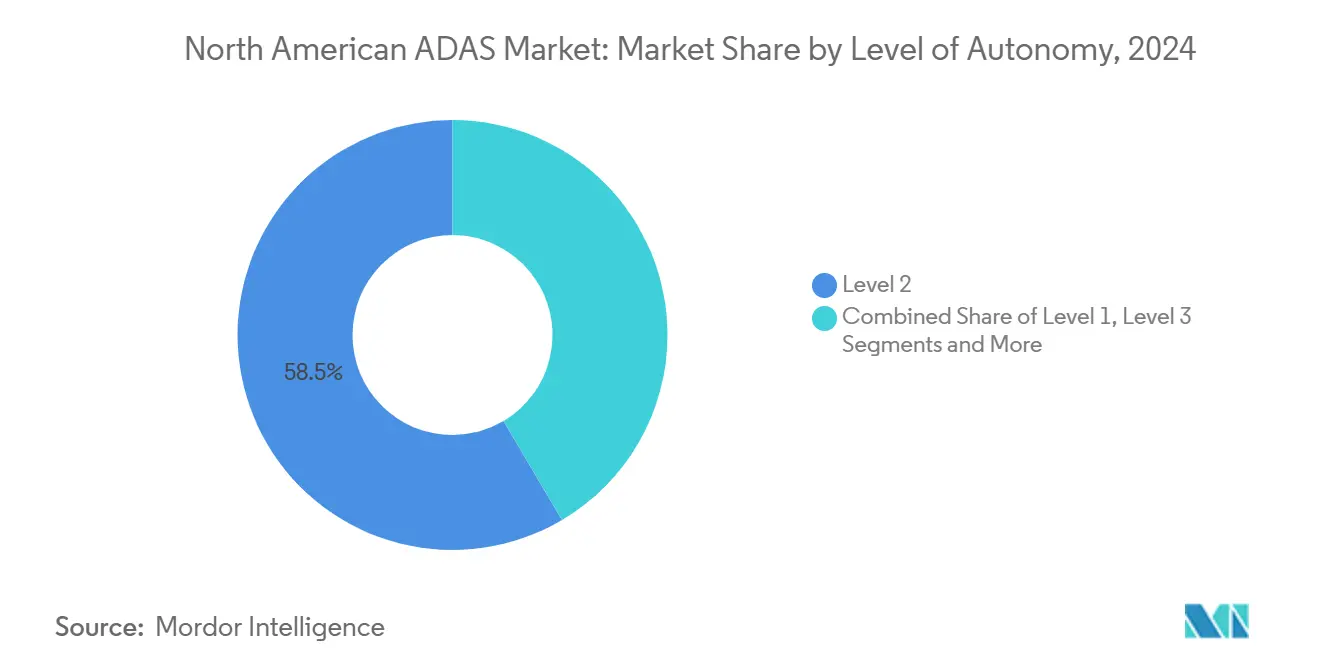

- By level of autonomy, Level 2 systems represented 58.45% of the 2024 installed base, whereas Level 4 solutions show the highest 22.14% CAGR outlook.

- By sales channel, OEM-fitted solutions accounted for 81.32% of 2024 revenue; aftermarket retrofit kits are still projected to post 21.11% CAGR through 2030.

- By country, the United States led with 76.45% revenue share of the North American ADAS market in 2024 and is projected to grow at a 17.54% CAGR through 2030.

North America ADAS Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-mandated AEB and FCW standards | +4.2% | United States primary, Canada delayed adoption | Medium term (2-4 years) |

| Declining radar / camera sensor prices | +3.1% | North America | Short term (≤ 2 years) |

| OEM software-defined platform upgrades | +2.8% | North America | Medium term (2-4 years) |

| HD-mapped highway and V2X corridors expansion | +2.3% | United States corridors, limited Canada | Long term (≥ 4 years) |

| Insurance premium discounts for ADAS-equipped vehicles | +1.9% | United States and Canada | Long term (≥ 4 years) |

| After-market retrofit kits for commercial fleets | +1.1% | North America commercial segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-mandated AEB & FCW standards

Federal rulemaking compels OEMs to integrate automatic emergency braking that functions at highway speeds and detects pedestrians in low-light situations, driving material increases in sensor count per vehicle, and accelerating platform refresh cycles. Tier 1 suppliers are bundling camera, radar, and growing LiDAR modalities into single-calculator fusion stacks that meet the new test protocol without inflating the bill-of-materials beyond target price points. U.S. prescriptions contrast with Transport Canada’s outcome-based stance that offers flexibility but stalls region-wide harmonization. Compliance work pulls forward software spending, boosts validation mileage, and compresses launch timelines into the 2029 deadline window.

Declining radar / camera sensor prices

Volume production and wafer-level packaging have cut 77 GHz radar module costs by more than 30% between 2022 and 2024, widening eligibility for safety suites on entry trims. Camera ASPs follow a similar curve because pixel density has risen while manufacturing yields improve. Due to solid-state designs, LiDAR, historically priced above USD 1,000, is now available below USD 500; Hesai shipped over 501,000 units in 2024, a 134.2% jump year on year, reflecting how cost deflation fuels exponential uptake[2]“2024 Annual Report,” Hesai Group, hesai.com. The affordability shift accelerates the standardization of multi-sensor fusion across compact sedans, SUVs, and even two-wheelers.

OEM software-defined platform upgrades

Automakers deploy centralized compute and zonal EE architectures that separate hardware from feature functionality, enabling continuous ADAS evolution via over-the-air updates. Volkswagen Group’s alliance with Valeo and Mobileye equips MQB derivatives with 360-degree perception and Level 2+ hands-free operations, all delivered through cloud-backed software bundles[3]“Next-Generation MQB ADAS Collaboration,” Volkswagen Group, media.vw.com. Bosch and Cariad target Level 3 mass production by 2025, supported by one thousand engineers working on computer vision pipelines. The approach allows monetization of feature unlocks during vehicle ownership.

Insurance premium discounts for ADAS-equipped vehicles

LexisNexis research across 11 million vehicles shows meaningful reductions in bodily injury and collision claim frequency where at least core ADAS features are active. Actuarial validation allows insurers to structure granular discounts that nudge adoption among cost-conscious buyers. However, higher repair complexity pushes up claim severity, producing a nuanced overall loss-cost impact. Specialist collision centers are investing in calibration bays, driving a parallel services market that offsets increases in component pricing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High LiDAR & sensor-suite costs | -2.7% | North America and Global | Medium term (2-4 years) |

| Regulatory patchwork | -1.8% | United States and Canada differences | Short term (≤ 2 years) |

| Shortage of certified calibration technicians | -1.4% | North America service networks | Medium term (2-4 years) |

| Cyber-security risks in OTA ADAS updates | -0.9% | Connected vehicle markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High LiDAR & sensor-suite costs

Even with sharp declines, a full forward-looking tri-sensing stack can still exceed USD 800 on compact vehicles, discouraging OEMs from broad deployment in cost-competitive segments. Passenger-car LiDAR trails radar-camera fusion in total installations, leaving Level 3 functions confined to premium nameplates. Suppliers are developing chip-on-board photonics and scanning-mirror eliminations to bring sub-USD 500 solutions to market, yet production yields remain volatile.

Regulatory patchwork across the NAFTA region

The timelines for the U.S. Federal Motor Vehicle Safety Standard are precise, whereas Transport Canada’s outcome-based draft allows open interpretation, and Mexico has yet to publish binding AEB mandates. Divergent homologation documents force OEMs to tailor validation protocols, duplicating engineering spends. Suppliers must maintain multiple feature toggles in software to meet distinct compliance targets, delaying single-SKU scale economies.

Segment Analysis

By System Type: Traffic Sign Recognition Drives Innovation

Traffic sign recognition surged 25.78% CAGR through 2030 as infrastructure-to-vehicle data streams enhance on-board classification accuracy. The feature underpins higher-level automation by feeding real-time speed-limit and warning information into trajectory planning engines. Adaptive cruise control, which commanded the largest 31.17% revenue block in 2024, benefits from long-range radar maturity and insurer endorsement. The North American ADAS market size attributed to adaptive cruise control is projected to scale in lockstep with the 2029 federal AEB cut-in, reinforcing its foundational role. Autonomous emergency braking, Lane Keep Assist, and driver monitoring system installations expand as cost-down camera modules and standardized ECU footprints simplify integration.

Software-defined vehicle strategies encourage OEMs to bundle incremental functions after sale, letting drivers unlock blind-spot detection or automated parking over a subscription. The North American ADAS market continues to favor modular feature packaging because buyers can tailor spend against perceived risk profiles. Night-vision and adaptive front-lighting remain premium, yet falling infrared sensor costs foreshadow trickle-down migration. Overall, the system-type hierarchy demonstrates how cross-feature synergies accelerate payback on core compute investment while maintaining consumer pricing flexibility.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sensor Technology: LiDAR Emergence Reshapes Competitive Dynamics

Radar retained a 33.74% share in 2024, due to resilience in adverse weather and commodity pricing that enables dual and tri-radar front ends on mid-tier cars. Still, LiDAR’s expected 23.14% CAGR signals an inflection as solid-state models integrate with NVIDIA DRIVE Orin to support automated emergency steering and robust object classification out to 250 meters. The North American ADAS market size attributed to LiDAR is on a steep trajectory as Mercedes-Benz and Volvo commit to feature-complete stacks on next-generation EV platforms.

Camera technology remains indispensable for lane-level semantics and traffic light detection, with volume shipments aligning with 8-megapixel resolution adoption. Ultrasonic sensors cover sub-5-meter blind spots for park assist, while V2X modules multiply in connected corridor states to extend situational awareness beyond line of sight. Sensor fusion algorithms deliver redundancy, and Magna’s Collective Perception constructs networked environmental twins to smooth handoffs between modalities. Supplier competition increasingly revolves around chipset roadmaps and perception software, overshadowing discrete hardware performance metrics.

By Vehicle Type: Two-Wheeler Innovation Accelerates Market Expansion

Passenger cars constituted 68.71% of 2024 volume, reflecting their regulatory prioritization and broad consumer base, yet two-wheelers will outpace all other segments at an 18.78% CAGR through 2030. Continental’s radar-assisted rider aid, entering series production on performance motorcycles, extends the North American ADAS market penetration into a previously underserved mobility segment. Light commercial vehicles gain traction as fleet operators chase lower liability exposure through standard lane departure warnings and collision avoidance.

Medium and heavy commercial vehicles integrate camera-mirror replacements and automated braking to meet North American Council for Freight Efficiency safety recommendations. Scania and Waabi’s generative AI approach to long-haul autonomy showcases data-driven dispatch, promising major fuel and uptime savings once regulatory clarity emerges. Overall, vehicle-type sub-segmentation underscores that penetration curves reflect unique use cases, cost envelopes, and risk tolerances rather than technology maturity alone.

By Level of Autonomy: Level 4 Development Accelerates Despite Regulatory Hurdles

Level 2 functions such as lane centering and adaptive cruise dominated with 58.45% share in 2024 because they align with driver oversight norms and insurance frameworks. The North American ADAS market anticipates Level 3 deployments led by Mercedes-Benz Drive Pilot, though state-by-state approval limits coverage areas. Level 4 prototypes demonstrate the highest growth runway at 22.14% CAGR, buoyed by commercial vehicle applications where hub-to-hub autonomy sidesteps dense urban complexity.

SAE Level 5 remains in R&D due to human-machine interface, legal liability, and fail-operational requirements that exceed current compute and cost envelopes. North American ADAS industry participants concentrate on scalable Level 2+ to Level 4 architectures so over-the-air feature rollout can monetize maturing perception stacks while infrastructure and policy advance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: Aftermarket Retrofit Gains Momentum Despite OEM Integration

OEM-factory installs represented 81.32% revenue in 2024 as automakers increasingly view ADAS as cornerstone brand equity. Their dominance is reinforced by Mobileye’s 2024 decision to shutter its aftermarket unit and pivot fully to embedded compute solutions that streamline homologation. Still, the retrofit segment’s 21.11% CAGR through 2030 reflects persistent demand among fleets with decade-long asset cycles.

Specialist installers overcome calibration challenges by adopting AI-driven documentation that flags OEM-specific torque specs and camera aiming positions; Mitchell and Protech’s partnership exemplifies this trend. Continental broadened aftermarket portfolios to include multifunction cameras with pre-aligned shrouds that cut set-up time by 40%. The North American ADAS market will therefore remain multi-channel, with retrofit kits addressing the legacy fleet while OEM pipelines supply the fast-growing new-vehicle pool.

Geography Analysis

The United States held 76.45% of regional demand in 2024 and is forecast to grow at 17.54% CAGR through 2030 as federal mandates lock in deployment targets and USD 60 million in V2X corridor grants create early-mover network effects. The North American ADAS market resonates strongly with U.S. buyers because the regulatory countdown to 2029 compels every mainstream OEM to include at least basic AEB and FCW on all trims. Complementary state subsidies for connected infrastructure, such as Texas Department of Transportation’s I-45 work-zone project, further accelerate adoption.

Canada accounts for a smaller but strategically relevant slice, defined by its consultative, outcome-based regulatory posture. The approach gives OEMs latitude on technical pathways yet extends uncertainty around program launch timing. Provincial insurance frameworks are beginning to experiment with ADAS-linked premium reductions, a factor that could lift local penetration once federal guidelines crystallize. The North American ADAS market size uptick in Canada depends on how quickly Transport Canada moves from consultation to binding rulemaking.

The rest of North America, encompassing Mexico and regional assembly centers, benefits from spill-over manufacturing and technology transfer. Luminar’s Guanajuato facility anchors LiDAR production for global supply, illustrating Mexico’s role in advanced component logistics. Cross-border supply chains let OEMs source calibrated sensor modules while exploiting cost advantages. Adoption curves lag the United States because binding mandates remain pending, yet as localized content rules under USMCA harmonize sourcing, suppliers anticipate synchronized feature rollouts across the broader trade zone.

Competitive Landscape

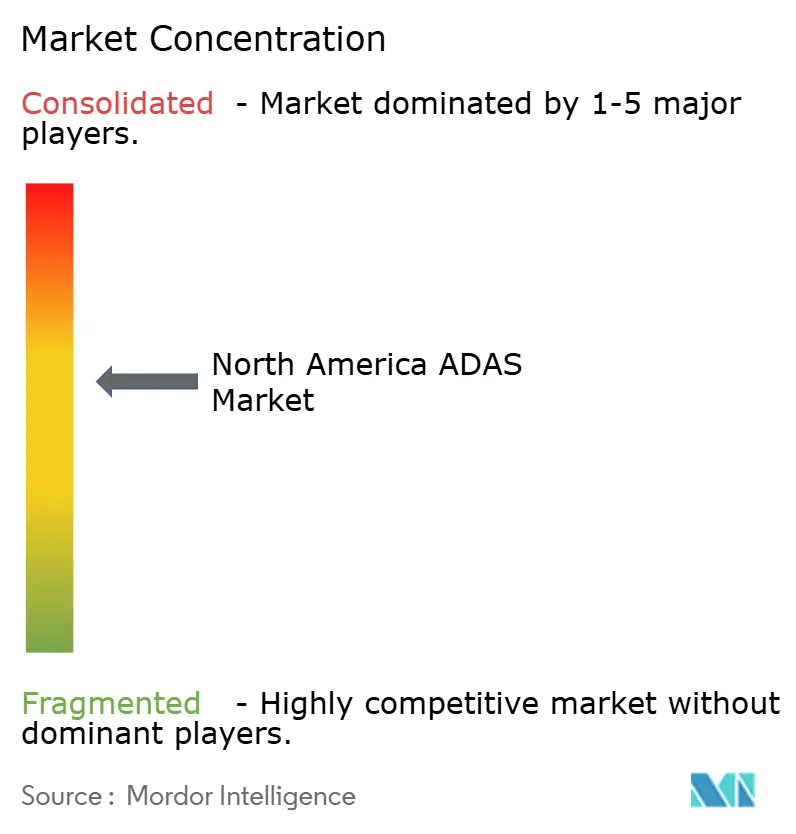

The North American ADAS market remains moderately consolidated, with the top five suppliers capturing an estimated more than half of the combined revenue in 2024. Bosch, Continental, and ZF leverage manufacturing scale, hardware breadth, and deep OEM ties to stay embedded on future platforms while redirecting R&D spending toward perception software and centralized compute. Bosch’s co-development of generative AI with Microsoft for automated driving exemplifies its bid to transition from component to full-stack solution provider.

Technology specialists like Luminar, Hesai, and Innovusion anchor differentiation around long-range LiDAR and proprietary chips, partnering with tier-ones for system integration. NVIDIA’s Drive platform, now paired with Magna hardware, gives traditional suppliers a commercial-ready AI backbone from Level 2+ to Level 4, accelerating time to market. Qualcomm’s 2025 acquisition of Autotalks bundles C-V2X and DSRC compatibility into Snapdragon Digital Chassis, signaling semiconductor ascendancy in vehicular domains.

Emerging white-space opportunities include two-wheeler ADAS, aftermarket calibration services, and data-driven insurance models. Start-ups chasing these niches face lower competitive intensity yet must navigate stringent safety validation. Overall, supplier success hinges on bundling perception, compute, and continuous software support rather than isolated hardware metrics, a shift that redefines traditional automotive value pools.

North America ADAS Industry Leaders

-

Continental AG

-

Aptiv Plc

-

MobilEye

-

Robert Bosch GmbH

-

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Qualcomm acquired Autotalks to enhance V2X communication solutions and strengthen its Snapdragon Digital Chassis product portfolio.

- April 2025: Continental launched its Aumovio brand as part of its automotive spin-off, focusing on software-defined vehicles and modern mobility solutions.

- March 2025: Volkswagen Group, Valeo, and Mobileye announced collaboration to enhance Level 2+ automation in MQB-based vehicles, featuring 360-degree sensor arrays and over-the-air update capabilities. This partnership streamlines procurement processes while enabling advanced driver assistance features across Volkswagen's vehicle portfolio.

- March 2025: Magna partnered with NVIDIA to integrate the DRIVE AGX platform into next-generation automotive technologies, supporting L2+ to L4 active safety solutions. The collaboration aims to redefine vehicle intelligence and autonomy, with a demonstration platform expected in Q4 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North American advanced driver assistance systems (ADAS) market as the revenue generated by active safety hardware (radar, cameras, LiDAR, ultrasonic sensors, micro-controllers) and the embedded software that governs them when factory fitted or professionally retrofitted into passenger cars as well as light, medium, and heavy commercial vehicles operating in the United States, Canada, and Mexico.

Scope exclusion: stand-alone infotainment units, pure telematics devices, and pilot-scale robo-taxi platforms remain outside this revenue pool.

Segmentation Overview

- By System Type

- Adaptive Cruise Control

- Autonomous Emergency Braking

- Lane Keeping Assist

- Lane Departure Warning

- Blind-Spot Detection

- Driver Monitoring / Drowsiness Alert

- Night Vision

- Adaptive Front-lighting

- Traffic Sign Recognition

- By Sensor Technology

- Radar

- Camera

- LiDAR

- Ultrasonic

- Infra-red

- V2X Modules

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Two-Wheelers (Motorcycles)

- By Level of Autonomy (SAE)

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

- By Sales Channel

- OEM-fitted

- After-market Retrofit

- By Country

- United States

- Canada

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with vehicle-safety engineers, sensor manufacturers, dealership groups, and insurance telematics specialists across North America. Their insights on pricing spreads, retrofit viability, and likely timelines for the forthcoming AEB mandate helped us close information gaps and align assumptions with field reality.

Desk Research

We began with open data from NHTSA crash causation files, Transport Canada road-safety statistics, and OICA vehicle production. We then layered in customs records, Society of Automotive Engineers sensor papers, and peer-reviewed cost curves for CMOS image sensors. Our analysts next reviewed company 10-Ks, select investor decks, and news articles in Dow Jones Factiva, while D&B Hoovers supplied verified financial splits for leading Tier-1 suppliers, letting us benchmark sensor average selling prices and OEM adoption rates. The sources listed here are only illustrative; many additional public and subscription databases were used for data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down build began with 2024 vehicle production and in-service parc, followed by ADAS fitment ratios by SAE level multiplied with sensor-mix average prices. Selective bottom-up checks using supplier roll-ups and channel feedback corrected outliers. Key variables include annual light-vehicle output, LiDAR cost deflation, federal AEB mandate milestones, premium electric-vehicle penetration, and average miles driven; these feed a multivariate regression that projects demand through 2030. Gap handling for sparse bottom-up inputs uses weighted averages of comparable vehicle classes and price brackets.

Data Validation & Update Cycle

Before sign-off, Mordor Intelligence reviewers run variance screens against recall rates, insurance loss data, and import shipment counts. Reports refresh every twelve months, and interim updates are issued when material policy or technology shifts occur.

Why Our North America ADAS Baseline Stands Reliable

Published ADAS numbers often differ because providers slice the market by dissimilar component mixes, price curves, or refresh schedules, leaving clients puzzled. Our disciplined scope, annual refresh cadence, and dual filter of production volumes plus fitment ratios yield a balanced figure, while others may bundle driver-monitoring infotainment chips, assume steep sensor price erosion, or omit retrofit channels, pushing their totals higher or lower.

This comparison shows our estimate sitting midway and firmly anchored to transparent variables, giving strategists a dependable baseline for critical planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.36 bn (2024) | Mordor Intelligence | - |

| USD 15.40 bn (2024) | Regional Consultancy A | Includes domain control units and camera-software bundles |

| USD 11.14 bn (2024) | Global Consultancy B | Focuses on radar and cameras only, excludes retrofit revenue |

| USD 10.80 bn (2023) | Trade Journal C | Uses conservative fitment rates and omits Mexico volumes |

This comparison shows our estimate sitting midway and firmly anchored to transparent variables, giving strategists a dependable baseline for critical planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the North American ADAS market?

The market was valued at USD 14.36 billion in 2024 and is forecast to reach USD 35.99 billion by 2030.

What compound annual growth rate (CAGR) is projected for North American ADAS sales between 2025 and 2030?

Revenue is expected to rise at a 16.54% CAGR during the 2025-2030 period.

Which ADAS technology segment is forecast to expand fastest through 2030?

Traffic sign recognition leads with a 25.78% CAGR, reflecting its pivotal role in higher-level automation and compliance needs.

How will federal regulations influence ADAS demand in the United States?

The National Highway Traffic Safety Administration requires automatic emergency braking on all new light vehicles by September 2029, driving a compliance-led surge in sensor and software adoption.

Are OEM-fitted or aftermarket ADAS systems more prevalent in North America?

Factory-installed systems dominate with 81.32% share in 2024, though aftermarket retrofit kits for fleets still post a strong 21.11% CAGR through 2030.

Which sensor type currently holds the largest share of the North American ADAS market?

Radar leads with 33.74% share in 2024, favored for its robustness across weather conditions and cost efficiency.

Page last updated on: