Wearable Adhesive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

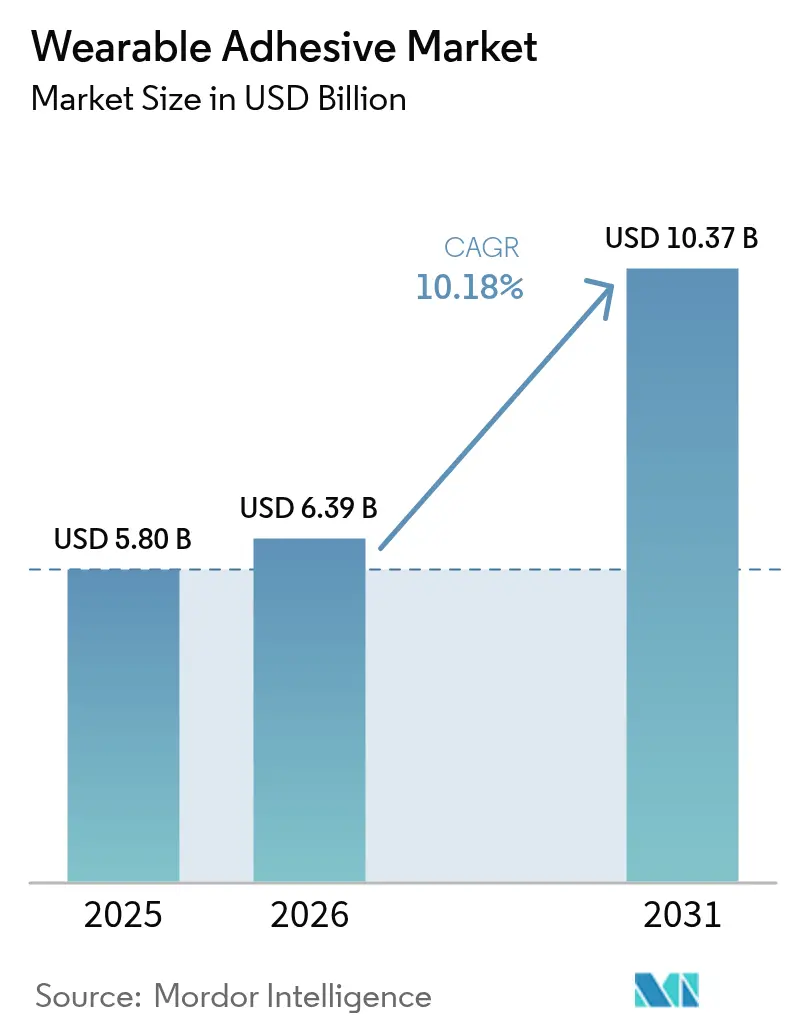

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 10.37 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

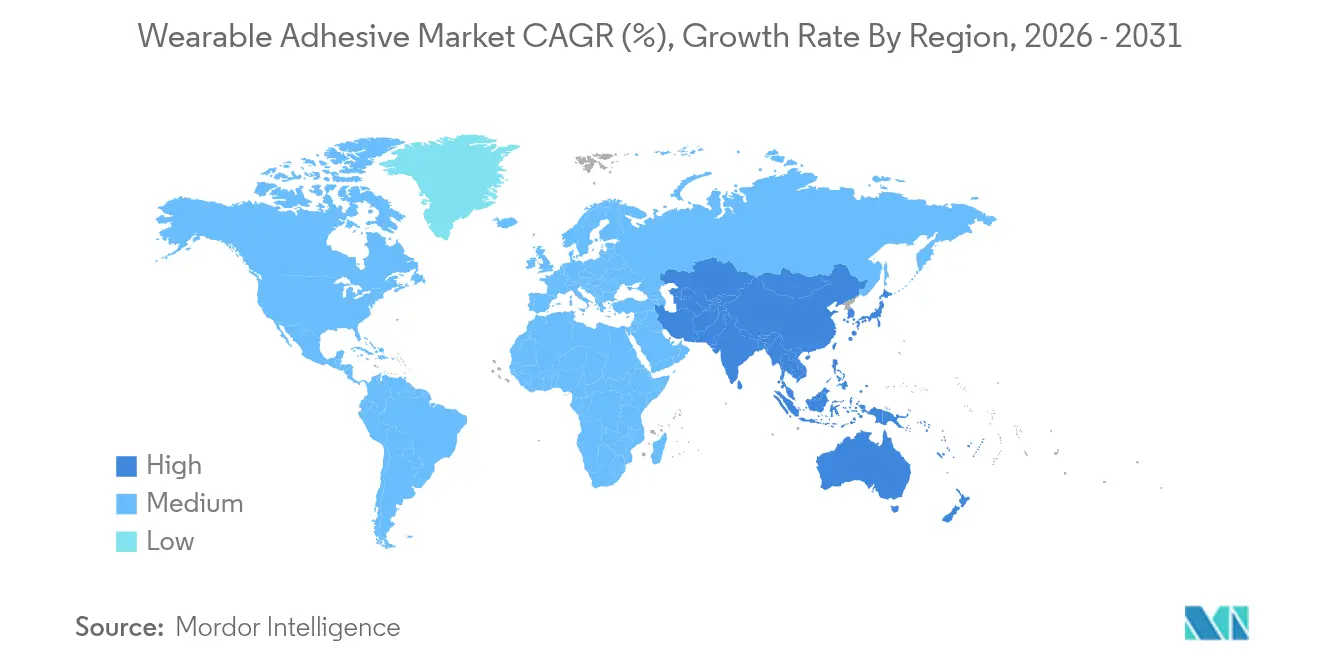

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable Adhesive Market Analysis by Mordor Intelligence

The wearable adhesive market size is expected to grow from USD 5.80 billion in 2025 to USD 6.39 billion in 2026 and is forecast to reach USD 10.37 billion by 2031 at 10.18% CAGR over 2026-2031. Growth is underpinned by three simultaneous shifts: health-care digitalization that expands remote monitoring programs, steady gains in industrial and defense biometrics, and rapid chemistry innovation that lowers skin-reaction risk while lengthening wear life. North America leads with 37.8% revenue share in 2024, but Asia-Pacific is the fastest-expanding geography at a 10.9% CAGR as Chinese medical-device production scales toward a USD 210 billion domestic market by 2025. Segment momentum is most visible in hydrogel formulations, therapeutic drug-delivery patches, and home-care settings, each growing more than the headline pace.

Key Report Takeaways

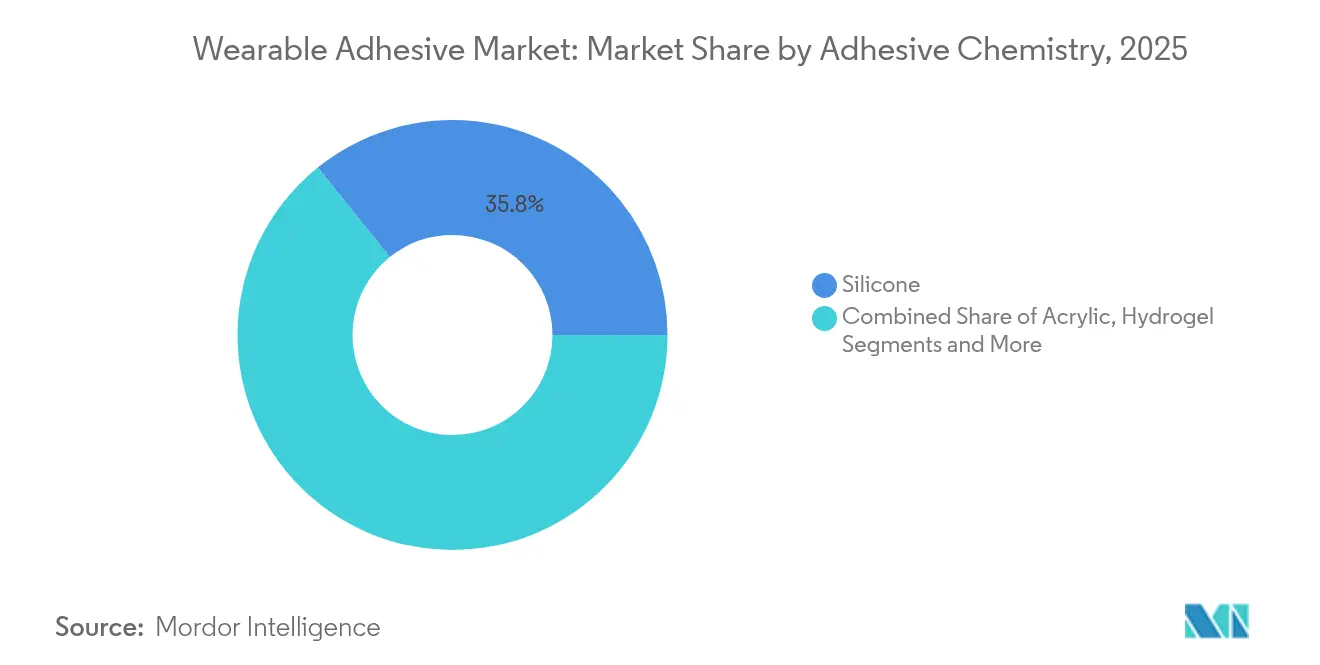

- By adhesive chemistry, silicone held 35.78% of the wearable adhesive market share in 2025; hydrogel is projected to grow at 11.02% CAGR through 2031.

- By product type, diagnostic and monitoring patches led with 40.85% revenue share in 2025, while therapeutic patches are forecast to expand at a 11.46% CAGR to 2031.

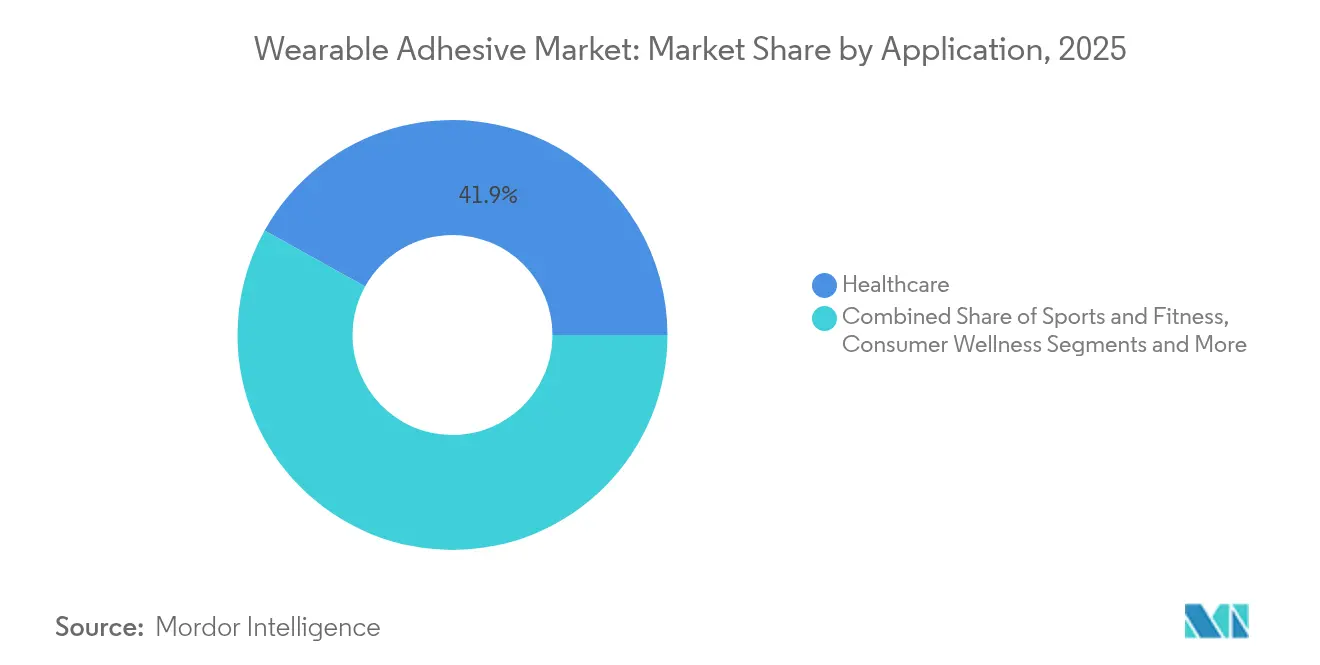

- By application, healthcare accounted for 41.92% of the wearable adhesive market size in 2025; industrial and military applications register the fastest 11.12% CAGR.

- By end-user, hospitals held 37.54% share of the wearable adhesive market in 2025, whereas home-care is advancing at a 10.21% CAGR to 2031.

- By geography, North America retained 37.22% share of the wearable adhesive market in 2025; Asia-Pacific is growing at a 10.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wearable Adhesive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of wearable medical and fitness devices | +2.8% | Global (early North America, EU) | Medium term (2-4 years) |

| Advances in skin-friendly adhesive chemistries | +2.1% | Global core, emerging markets spill-over | Long term (≥ 4 years) |

| Expansion of home-based remote patient monitoring programs | +1.9% | North America and EU, scaling in APAC | Short term (≤ 2 years) |

| Industrial and defense uptake of biometric patches | +1.4% | US and EU defense, emerging APAC | Medium term (2-4 years) |

| Regulatory push toward reusable devices | +1.2% | FDA/CE areas, global cascade | Long term (≥ 4 years) |

| Rise of minimally invasive microneedle patches | +1.0% | Advanced health-care markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Wearable Medical and Fitness Devices

The FDA’s March 2024 clearance of Dexcom Stelo, the first over-the-counter continuous glucose monitor, unlocked a new end-user pool of 25 million U.S. adults with Type 2 diabetes and in turn catalyzed adhesive-volume growth across retail channels[1]U.S. FDA, “Medical Device Biocompatibility Guidance,” fda.gov . Venture funding signals similar momentum: Biolinq raised USD 58 million in April 2024 to scale precision multi-analyte biosensors that hinge on long-wear skin adhesives. Longer sensor life is now feasible; Dexcom’s G7 platform reaches 15.5 days of reliable adhesion, reducing replacement frequency and widening consumer appeal. Each of these milestones expands the wearable adhesive market beyond clinical silos and embeds patches in everyday wellness management.

Advances in Skin-Friendly Adhesive Chemistries

Peer-reviewed data in Contact Dermatitis flagged isobornyl acrylate (IBOA) as an allergy trigger in certain CGM users, prompting industry-wide reformulations. Dymax answered with an IBOA-free and TPO-free 2000-MW series that still meets ISO 10993 requirements for skin contact. MIT researchers added a hydrogel barrier that averts fibrosis and allows months-long implantation without immune rejection. Such breakthroughs widen the wearable adhesive market by easing regulatory hurdles tied to adverse skin events.

Expansion of Home-Based Remote Patient Monitoring Programs

North American payers reimburse more home-based monitoring, and EU regulators similarly prioritize out-of-hospital care; both trends rely on reliable skin-contact interfaces. Caltech’s iCares “smart bandage” reads wound biomarkers in real time, empowering clinicians to intervene remotely. Emotional-state patches from Penn State now track cortisol fluctuations, underscoring the expanding telemetry breadth. As device complexity rises, adhesive longevity and repositionability become differentiators, lifting the wearable adhesive market adoption curve in consumer dwellings.

Industrial and Defense Uptake of Biometric Patches

DARPA’s BEST program funds self-powered bandages that alert combat medics to infection risk, advancing a use-case where adhesive durability under sweat, dust, and motion is mission-critical. KAIST’s sweat-resistant EMG sensors preserve signal quality in high-humidity factory floors, illustrating industrial cross-over potential. Such specialized environments reward adhesives that marry high bond strength with painless removal, lifting average selling prices and segment margins inside the wearable adhesive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin irritation and sensitivity leading to product recalls | -1.8% | Global, highly regulated markets | Short term (≤ 2 years) |

| Long-wear adhesion versus painless removal trade-off | -1.2% | Global, pronounced in aging users | Medium term (2-4 years) |

| Environmental concerns over silicone/acrylate waste | -0.9% | EU and North America first movers | Long term (≥ 4 years) |

| Fragile supply chain for hydrogel polymers | -0.7% | Global, APAC production hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skin Irritation and Sensitivity Leading to Product Recalls

The FDA’s MAUDE database lists rising dermatitis complaints against adhesive-based wearables; iRhythm’s Zio Monitor and Abbott’s FreeStyle Libre 3 both faced warnings or recalls tied to chemical burns or inaccurate readings. Pediatric burn cases triggered a Megadyne electrode correction, showing that one-formula-fits-all designs fall short of vulnerable-skin needs. These events temporarily cap the wearable adhesive market size, spark reformulation costs, and fuel a regulatory climate that favors proactive biocompatibility proof.

Long-Wear Adhesion Versus Painless Removal Trade-Off

Avery Dennison technical notes confirm that increasing tack for seven-day wear commonly raises epidermal trauma on removal. Silicone systems reduce trauma yet can lift under sweat or motion, while acrylics stick hard but irritate thin skin. Swiss supplier artimelt proposes silicone-free low-trauma blends that aim to square this circle. Until a universally gentle yet high-strength adhesive matures, this physics dilemma restrains certain high-dwell applications and tempers some wearable adhesive market forecasts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Chemistry: Silicone Leadership Faces Hydrogel Innovation

Silicone held 35.78% of the wearable adhesive market in 2025 owing to hypoallergenic profiles, repositionability, and proven ISO 10993 records. NuSil and Elkem locked in health-care contracts by optimizing viscosity ranges for roll-to-roll coating lines. Hydrogel chemistries, although only 23.8% today, accelerate at an 11.02% CAGR as they wick perspiration and maintain electrical contact over long new work shifts. The wearable adhesive market size for hydrogel patches will likely surpass USD 3.18 billion before 2031 if current momentum persists. Hybrid siloxane-hydrogel matrices emerge as a middle path, especially for flexible printed-circuit assemblies that need both breathability and conductivity.

Second-order innovation targets conductivity and self-healing. Frontiers in Chemistry documented polyvinyl-alcohol hydrogels that restore bond integrity after mechanical damage and allow real-time ECG capture. Recyclable lipoic-acid adhesives from UC Berkeley extend sustainability narratives and could cut medical waste once performance data mature. Such green attributes may soon influence procurement scores, nudging the wearable adhesive market toward circular models.

By Product Type: Diagnostic Dominance Yields to Therapeutic Innovation

Continuous glucose monitors, ECG patches, and fertility trackers established a 40.85% foothold, anchoring diagnostic leadership within the wearable adhesive market. The sector standard for adhesion rose in April 2025 when Dexcom’s G7 extension hit a 15-day wear record. Yet therapeutic patches sprint faster at a 11.46% CAGR, powered by microneedle drug-delivery arrays that bypass first-pass metabolism. The wearable adhesive market size for this sub-class already exceeds USD 842.6 million and enjoys premium pricing because adhesion performance doubles as a drug-delivery safety metric.

Transdermal neuromodulation and pain-management devices reinforce the trend; their need for consistent skin impedance makes adhesive selection a critical clinical parameter. FDA guidance issued in 2024 specifically calls out 72-hour post-application peel tests for drug-in-adhesive systems, raising technical barriers for newcomers. Smart wound dressings fuse both product worlds by integrating moisture sensors with antimicrobial release, offering a long runway for differentiation.

By Application: Healthcare Foundation Expands to Industrial Frontiers

Clinical use still anchors 41.92% of 2025 demand. Hospitals rely on predictable adhesion removal cycles that fit into protocol windows, giving silicone suppliers a volume cushion. However, emerging industrial and defense deployments grow 11.12% yearly and introduce harsh-environment requirements that elevate average selling price in the wearable adhesive market. Sweat-proof EMG strips optimize factory-floor ergonomics, while military field patches must survive sand, water, and vibration.

Consumer wellness devices, propelled by OTC regulatory wins, blur category lines. As users self-install devices without clinician oversight, suppliers now bundle pre-application skin-prep kits and latex-free options, adding ancillary revenue and complexity to the wearable adhesive market.

By End-User: Hospital Concentration Shifts Toward Home-Care Decentralization

Hospitals commanded 37.54% of revenue in 2025 due to bulk procurement and integrated EMR compatibility that favors top-tier suppliers. Multi-site clinical trials often start here, ensuring adhesives meet IRB safety thresholds. Yet the 10.21% CAGR in home-care transforms distribution logic: e-commerce refill packs and pharmacist-dispensed accessories rise in tandem. Clinics and ambulatory surgery centers act as tipping points, piloting small-batch novel adhesives before payers green-light broader reimbursement.

Device makers now run parallel peel-test protocols—one replicating controlled hospital climates and another mimicking variable home humidity—to optimize skus. These shifts broaden the wearable adhesive market beyond institutional walls and illuminate service gaps such as telehealth hotline support for skin issues.

Geography Analysis

Regulatory clarity keeps North America on top with 37.22% share. The FDA’s 2024 update on biological evaluation of medical devices gave early-mover benefits to suppliers already using IBOA-free chemistries. The region also hosts many of the clinical trials validating 10-day plus wear claims, embedding a virtuous cycle of data and reimbursement alignment.

Asia-Pacific logs the quickest 10.55% CAGR as China’s Five-Year Plan funds domestic device innovation and local adhesive coating lines. India’s new mandatory registration scheme, effective late-2023, filters sub-par imports and nudges reputable suppliers into joint ventures that expand the wearable adhesive market footprint.

Europe grows steadily, but its Green Deal pushes recyclability and solvents reduction, prompting R&D pivots toward water-based systems that may modestly lift unit costs.

Competitive Landscape

The wearable adhesive market shows moderate concentration. Avery Dennison’s medical unit grew 3.61% in Q4 2024 and now holds about 4.03% revenue share, outperforming larger diversified peers. 3M’s healthcare spin-off, Solventum, with USD 8.2 billion revenue, clusters advanced wound-care tapes and biosensor adhesives under one focused banner, thereby intensifying rivalry. H.B. Fuller’s December 2024 twin acquisitions of Medifill and GEM diversified its cyanoacrylate toolbox, creating cross-selling opportunities in wound-closure films.

Technology competition emphasizes allergen-free performance. Dymax launched IBOA-free portfolios early, gaining trials with top-five CGM manufacturers. DELO entered medical electronics in January 2024, bringing know-how from automotive micro-LED bonding to stretchable PCB adhesives, a move that may disrupt incumbent silicone players. VTT’s roll-to-roll printed-electronics partnership showcases manufacturing scale that could shave cost per patch and amplify volumes in the wearable adhesive market.

Strategic alliances now incorporate carbon-capture chemistry; Henkel and Celanese are piloting CO2-based methanol feedstocks for water-based adhesives, aligning with EU Scope-3 targets. DuPont’s Donatelle acquisition layers injection-molding skill on top of its silicone platform, smoothing vertical integration and accelerating design-for-manufacture cycles for new patch concepts[3]DuPont Investor News, “Donatelle Plastics Acquisition,” dupont.com.

Wearable Adhesive Industry Leaders

Koninklijke Philips N.V.

MC10 Inc.

3M

Avery Dennison Medical

Nitto Denko Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dexcom won FDA clearance for the G7 15-Day CGM, delivering 15.5-day wear life at 8.0% MARD accuracy.

- December 2024: H.B. Fuller acquired Medifill Ltd. and signed for GEM S.r.l. to boost cyanoacrylate wound-closure offerings.

- November 2024: Henkel and Celanese launched a CCU partnership turning captured CO2 into methanol feedstock for water-based adhesives.

- July 2024: Avery Dennison opened a Medical Wearable Adhesives Learning Center to support device developers.

Global Wearable Adhesive Market Report Scope

Sticking a wearable device to the skin can be very tricky. That’s why it’s very important to have a good adhesive to hold the device together or adhere the device to the wearer’s skin. The adhesive can be used to stick various types of medical devices into a patients skin to collect data about the patient well being or to monitor patient's activity.

| Silicone |

| Acrylic |

| Hydrogel |

| Hydrocolloid |

| Others |

| Diagnostic / Monitoring Patches | Continuous Glucose Monitor (CGM) |

| ECG / Cardiac Patch | |

| Temperature Patch | |

| Therapeutic Patches | Microneedle Drug-delivery |

| TENS / Neuromodulation Patch | |

| Transdermal Drug-in-Adhesive Patch | |

| Wound-care Dressings | Advanced Hydrocolloid |

| Antimicrobial Foam | |

| Smart Bandages |

| Healthcare |

| Sports and Fitness |

| Industrial and Military |

| Consumer Wellness |

| Hospitals |

| Clinics |

| Home-care Settings |

| Ambulatory Surgical Centers |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Adhesive Chemistry | Silicone | ||

| Acrylic | |||

| Hydrogel | |||

| Hydrocolloid | |||

| Others | |||

| By Product Type | Diagnostic / Monitoring Patches | Continuous Glucose Monitor (CGM) | |

| ECG / Cardiac Patch | |||

| Temperature Patch | |||

| Therapeutic Patches | Microneedle Drug-delivery | ||

| TENS / Neuromodulation Patch | |||

| Transdermal Drug-in-Adhesive Patch | |||

| Wound-care Dressings | Advanced Hydrocolloid | ||

| Antimicrobial Foam | |||

| Smart Bandages | |||

| By Application | Healthcare | ||

| Sports and Fitness | |||

| Industrial and Military | |||

| Consumer Wellness | |||

| By End-user | Hospitals | ||

| Clinics | |||

| Home-care Settings | |||

| Ambulatory Surgical Centers | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the wearable adhesive market and how fast is it growing?

The market is valued at USD 6.39 billion in 2026 and is forecast to reach USD 10.37 billion by 2031, reflecting a 10.18% CAGR over 2026-2031.

Which adhesive chemistry leads the market today?

Silicone-based formulations hold the largest 35.78% share because they balance biocompatibility, gentle removal, and proven regulatory history.

Why are hydrogel adhesives receiving so much attention?

Hydrogels manage sweat and moisture better than other chemistries and therefore post the fastest 11.02% CAGR, especially in long-wear glucose monitors and smart bandages.

How significant is home-care adoption compared with hospitals?

Hospitals still command 37.54% of 2025 revenues, yet home-care settings are expanding briskly at a 10.21% CAGR as payers reimburse remote monitoring and patients favor in-home management.

Which region will add the most new revenue through 2031?

Asia-Pacific, led by China’s USD 210 billion medical-device build-out, is growing at 10.55% CAGR and is set to contribute the largest incremental dollar gains.

What is the main technical challenge holding back even faster growth?

Balancing long-wear adhesion with painless removal remains a core hurdle; stronger tack often raises skin-trauma risk, spurring ongoing R&D into low-trauma chemistries.

Page last updated on: