Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

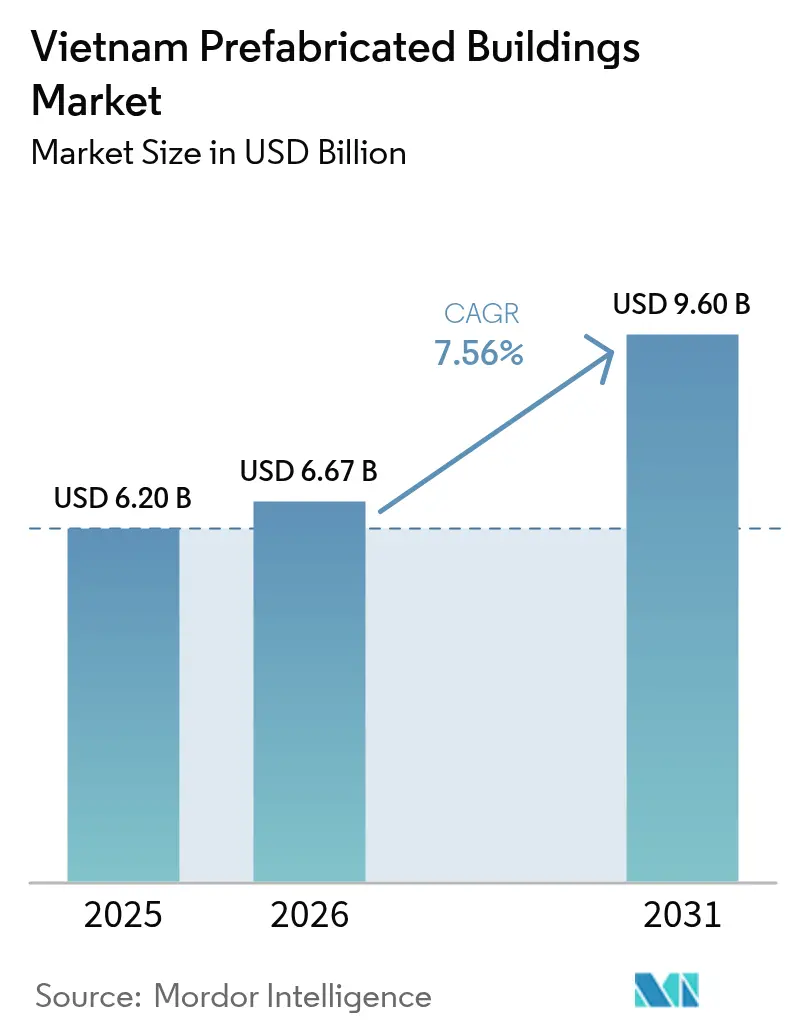

| Base Year Market Size (2025) | USD 6.20 Billion |

| Market Size (2026) | USD 6.67 Billion |

| Market Size (2031) | USD 9.60 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Prefabricated Buildings Market Analysis by Mordor Intelligence

The Vietnam prefabricated buildings market size was valued at USD 6.20 billion in 2025 and estimated to grow from USD 6.67 billion in 2026 to reach USD 9.6 billion by 2031, at a CAGR of 7.56% during the forecast period (2026-2031). Government social-housing programs, rising foreign direct investment (FDI) in industrial parks, and time-critical coastal tourism projects together underpin this solid growth trajectory. Rapid factory relocations from China, a 7% real GDP expansion in 2024, and the “One Million Social Homes 2025-2035” scheme have accelerated demand for ready-to-install modules that shorten project cycles. Pressure on contractors’ margins from volatile steel prices is partly offset by green-credit incentives that lower financing costs for low-carbon modular buildings. Expanding worker dormitory requirements around Bac Ninh, Hai Phong, and Ho Chi Minh City further anchor medium-term opportunities for Vietnam's prefabricated buildings market participants.

Key Report Takeaways

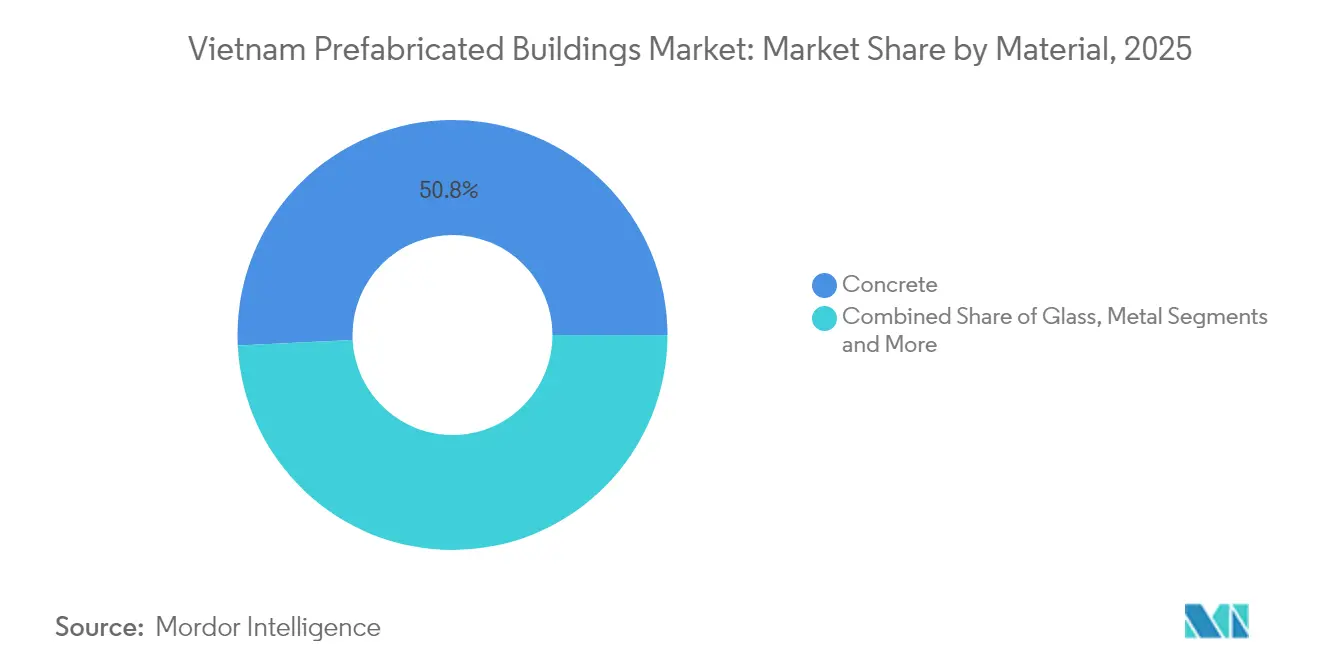

- By material, concrete led with 50.78% Vietnam prefabricated buildings market share in 2025, while timber is projected to post the fastest 8.28% CAGR through 2031.

- By application, residential projects captured 50.62% revenue share in 2025; commercial buildings are set to advance at an 7.95% CAGR to 2031.

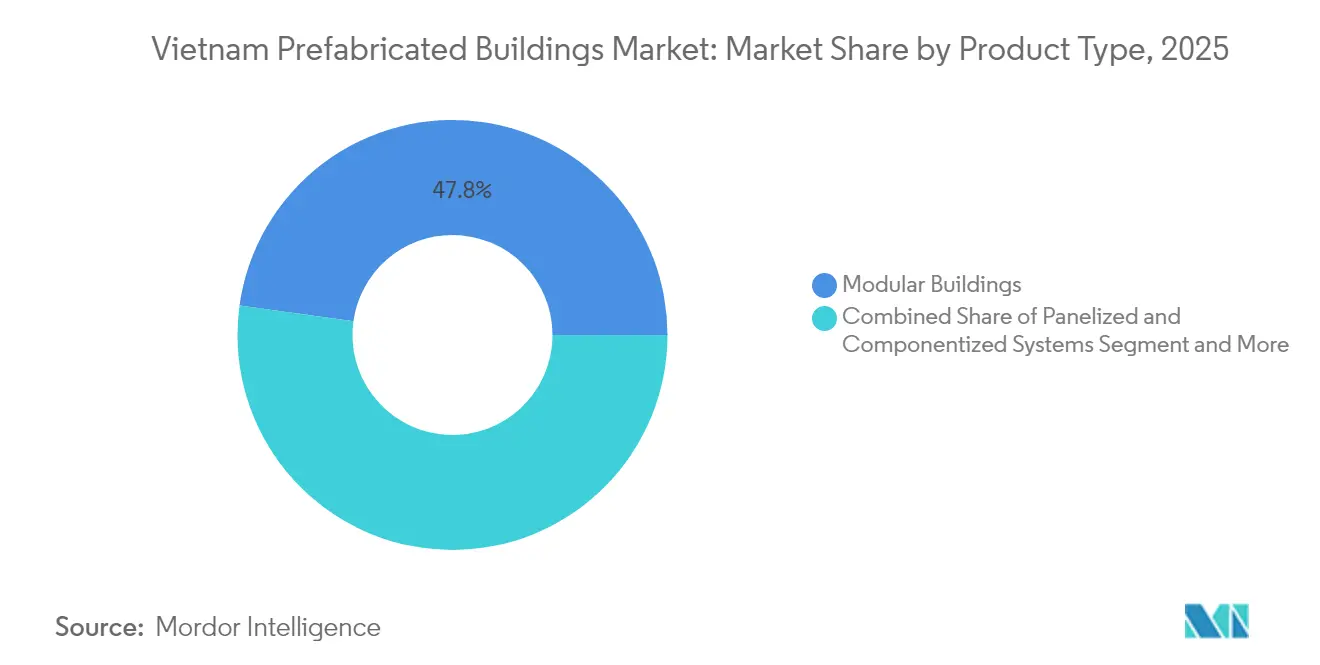

- By product type, modular construction commanded 47.81% share of the Vietnam prefabricated buildings market size in 2025, and panelized systems are forecast to expand at an 8.19% CAGR through 2031.

- By key cities, Ho Chi Minh City held 21.12% share in 2025, whereas Da Nang is expected to grow at the highest 8.44% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government “One Million Social Homes 2025-2035” scheme unlocking prefab tenders | +1.2% | National: Ho Chi Minh City, Hanoi, key industrial provinces | Medium term (2-4 years) |

| FDI-led industrial-park dormitories needing rapid deployment | +0.9% | Bac Ninh, Hai Phong, Ho Chi Minh City | Short term (≤ 2 years) |

| Coastal resort boom compressing construction timelines | +0.8% | Da Nang, Phu Quoc, coastal provinces | Medium term (2-4 years) |

| Skilled-labor shortages spurring off-site productivity gains | +0.7% | National, acute in large cities | Long term (≥ 4 years) |

| Green-credit incentives for low-carbon modular buildings | +0.6% | National, green economic zones | Medium term (2-4 years) |

| Offshore-wind service hubs adopting floatel modules | +0.4% | Coastal wind zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government “One Million Social Homes 2025-2035” scheme unlocking prefab tenders

The social-housing initiative is Vietnam’s single largest demand trigger for modular systems. It has already delivered 117 schemes totaling 85,275 units and launched another 159 projects aimed at 135,563 units that must be handed over by end-2025. Resolution 155/NQ-CP fast-tracks permitting and creates a national housing fund, so contractors with factory-built modules hold an execution edge. Provincial variation remains wide—Nghệ An has exceeded housing targets while Hà Tĩnh lags—yet uniform pressure to meet ministry targets keeps Vietnam's prefabricated buildings market momentum high. The program also overlaps with worker dormitory needs in industrial parks, compounding its pull on prefab capacity.

FDI-led industrial-park dormitories needing rapid deployment

FDI inflows totaled USD 38.23 billion in 2024, with USD 25.58 billion flowing into processing and manufacturing projects that demand on-site accommodation. Logistics parks such as BW-ESR’s 112,000 m² Nam Son Hap Linh and 162,000 m² Yen Phong hubs illustrate how multinational tenants specify fast-assembly dorms. Tight production ramp-up schedules mean factory-fabricated rooms are preferred over conventional masonry, putting another growth stream into the Vietnam prefabricated buildings market. Provinces courting investors with tax breaks intensify this timing imperative and make modular units the practical solution for labor housing[1]Ministry of Planning and Investment, “FDI Performance 2024,” mpi.gov.vn.

Coastal resort boom compressing construction timelines

Mega schemes such as Vingroup’s USD 11 billion Cần Giờ coastal city and Sun Group’s USD 512 million Aspira Tower highlight how developers must open properties before the high tourist season. Prefab guestrooms and service blocks achieve consistent quality while shaving months off build cycles, a decisive advantage when monsoons restrict site work. Cat Ba Central Bay’s USD 500 million eco-tourism complex is adopting off-site modules to meet strict environmental benchmarks and deadline-driven booking schedules. As coastal visitor numbers climb, the Vietnam prefabricated buildings market will gain fresh orders from hospitality groups looking to cut timeline risk.

Skilled-labor shortages spurring off-site productivity gains

A 7% GDP jump in 2024 stretched Vietnam’s construction workforce thin, with industrial output up 8.4% and drawing trades away from building sites. Factory-controlled assembly lets fewer skilled technicians deliver more structural output, reducing on-site labor days. Directive 03/CT-BXD’s stricter safety rules further favor controlled plant environments. Trần Đức’s new 126,000 m² Net Zero Carbon plant shows how companies pivot to high-efficiency production lines, reinforcing prefab’s role in closing the labor gap across the Vietnam prefabricated buildings industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel prices are squeezing contractor margins | -0.9% | Nationwide, steel-heavy builds | Short term (≤ 2 years) |

| Fragmented provincial building codes are delaying type approval | -0.8% | Nationwide, varies by province | Medium term (2-4 years) |

| Cultural preference for masonry homes in urban centers | -0.6% | Major cities, traditional districts | Long term (≥ 4 years) |

| Limited domestic CLT/glulam capacity amid export pull | -0.5% | Nationwide, timber projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile steel prices are squeezing contractor margins

A surge in green-steel investments and external shocks like the EU Carbon Border Adjustment Mechanism have sent Vietnamese steel prices on a roller-coaster ride. Prefab firms, locked into fixed-price contracts built on heavy steel frames, absorb much of the fluctuation, eroding profit. While tax incentives ease some pressure, unpredictable input costs remain a near-term brake on Vietnam's prefabricated buildings market expansion.

Fragmented provincial building codes are delaying type approval

Prefabricated products must often secure separate approvals in each province, extending lead times and raising compliance costs. Circular 02/2025/TT-BXD seeks uniformity, but uneven enforcement keeps investors cautious. BIM mandates in Thanh Hoa starting in 2025 add yet another layer of digital requirements. Until harmonization improves, the Vietnam prefabricated buildings market faces slower roll-outs, especially for nationwide housing models[2]Ministry of Construction, “Circular 02/2025/TT-BXD,” moc.gov.vn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete remains dominant while timber races ahead

Concrete commanded a 50.78% Vietnam prefabricated buildings market share in 2025, sustained by well-established precast supply chains and cultural familiarity with solid structures. Precast wall panels and hollow-core slabs underpin social-housing and industrial contracts, letting developers keep costs predictable. Timber, although smaller, is the fastest-growing material with an 8.28% CAGR through 2031, propelled by carbon-reduction targets and wider acceptance of engineered wood products in mid-rise projects. Manufacturers such as Trần Đức are investing in automated lines for cross-laminated and glulam components, aiming to capture green-credit demand. Metal systems continue to find traction in logistics parks, while hybrid composite modules emerge in luxury coastal resorts that emphasize glass façades and corrosion resistance.

The shift toward sustainable inputs reflects Vietnam’s pledge to reach net-zero by 2050 and to trim building-sector emissions 9-27% by 2030. Contractors blending concrete cores with timber interiors offer a cost-effective bridge between familiarity and sustainability, positioning them for future tenders under Resolution 122/NQ-CP. As the supply of domestically produced CLT widens, the Vietnam prefabricated buildings market size for wood-based frames is projected to expand steadily, helping diversify away from steel-heavy methods sensitive to global price swings.

By Application: Residential leads but commercial accelerates

Residential projects held a 50.62% share of the Vietnam prefabricated buildings market in 2025, anchored by the government’s social-housing pipeline that alone accounts for more than 627,000 planned units. Low-rise modular blocks allow provincial authorities to hand over keys within 12-14 months, far faster than traditional masonry. Yet commercial structures, spanning factories, warehouses, and retail formats, are advancing at an 7.95% CAGR, the highest among applications, as FDI projects stipulate quick turnarounds. Dormitory complexes often blur residential and commercial boundaries, but their recurring volume makes them significant order books for prefab manufacturers.

Healthcare, education, and hospitality represent smaller slices yet support diversification. High-rise apartment developers in Ho Chi Minh City are piloting pod-type bathrooms and utility shafts to de-risk interior fit-out time. That approach signals growing acceptance of partial prefabrication, which could eventually lift the Vietnam prefabricated buildings market size further if consumer attitudes toward fully modular homes improve.

By Product Type: Modular units on top; panelized systems gain speed

Modular buildings represented a 47.81% Vietnam prefabricated buildings market share in 2025. Their plug-and-play nature fits public-sector schedules that demand turnkey delivery. Whole-room modules reduced social-housing site work by up to 40 days per floor, giving contractors the decisive advantage on penalty-tight contracts. Panelized and componentized solutions, however, are forecast to grow at an 8.19% CAGR to 2031 as developers seek design flexibility without forfeiting off-site efficiencies. Firms like ATAD and BMB Steel deliver pre-engineered frames that designers can clad or partition on-site, striking a balance between customization and speed.

Hybrid systems, incorporating steel cores with prefabricated bathroom pods, gain attention in higher-rise commercial towers where full volumetric stacking is structurally impractical. As BIM adoption spreads, manufacturers can further integrate panel production with digital models, minimizing rework and material waste across the Vietnam prefabricated buildings industry.

Geography Analysis

Ho Chi Minh City anchors demand, holding a 21.12% share in 2025 as multinational manufacturers and local conglomerates concentrate expansion there. Massive projects like Vingroup’s coastal township rely on volumetric room stacks and precast façades to compress schedule and satisfy green benchmarks. The city’s extensive logistics network further supports just-in-time module delivery, reinforcing its dominance in the Vietnam prefabricated buildings market.

Hanoi maintains the second-largest slice, capitalizing on governmental funding streams and institutional projects that increasingly enforce BIM and green-certification requirements. Its position as policy nerve center accelerates regulatory clarity for off-site construction, nudging private developers toward modular solutions. Although traditional masonry remains culturally preferred in high-income neighborhoods, pilot prefabricated schools and clinics showcase cost and safety advantages, gradually shifting perception.

Da Nang is on track to be the fastest-growing metro with an 8.44% CAGR to 2031, powered by tourism-driven hotels, port upgrades targeting up to 29 million tons of cargo by 2030, and supportive municipal policies. Resorts along My Khe beach now specify volumetric villas to open ahead of peak season, and floatel makers eye the port for offshore-wind staging. Elsewhere, industrial corridors in Bac Ninh, Hai Phong, and Nghệ An see steady module demand for dormitories as foreign electronics assemblers ramp up capacity. With expressways shortening transit, prefab hubs in Binh Duong and Dong Nai can serve these northern sites, expanding the Vietnam prefabricated buildings market footprint across virtually every province.

Competitive Landscape

The Vietnam prefabricated buildings industry is moderately fragmented, with several steel-structure specialists playing a significant role in large-scale tenders. Companies like ATAD Steel Structure Corp., Zamil Steel Buildings Vietnam, and BMB Steel utilize extensive fabrication yards and hold international quality certifications, enabling them to secure contracts for factories, warehouses, and airport hangars. PEB Steel, for instance, operates seven plants with substantial production capacity, allowing for shorter lead times and competitive unit costs.

Strategic focus is shifting towards sustainability and digital innovation. Trần Đức is investing USD 300 million in a Net Zero prefab complex powered by renewable energy and optimized for wooden modules, aiming to benefit from future green-credit incentives. Dai Dung Metallic has achieved LEED GOLD v4 certification, setting an environmental benchmark increasingly prioritized in public tender evaluations. Foreign companies are exploring joint ventures, collaborating with local partners for land and permits while introducing advanced volumetric technology.

Emerging service niches, such as offshore-wind floatels, are witnessing growing competition, with no dominant domestic player yet. Companies combining marine engineering expertise with modular construction capabilities have the potential to secure high-value projects. Additionally, provincial BIM mandates are encouraging firms to adopt integrated design-to-production software, raising technological standards and challenging smaller workshops. While competition remains robust, the adoption of green and digital standards is expected to drive opportunities in Vietnam's prefabricated buildings market.

Vietnam Prefabricated Buildings Industry Leaders

ATAD Steel Structure Corp.

Zamil Steel Buildings Vietnam

BMB Steel

Dai Dung Metallic Structure

Hoa Binh Construction Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Trần Đức Corporation broke ground on a 126,000 m² Net Zero Carbon prefab factory in Binh Duong with targeted USD 300 million yearly revenue by 2029.

- June 2025: Nam Định launched a USD 4 billion green-steel plant expected to supply 16,000 jobs and future prefab demand.

- April 2025: Vingroup started the USD 11 billion Cần Giờ coastal urban area applying prefabricated components at scale.

- April 2025: Government approved USD 136.3 billion Power Plan VIII focusing on rooftop solar integration compatible with modular roofs.

Vietnam Prefabricated Buildings Market Report Scope

Modular building solutions are becoming more popular among big housing companies because they reduce waste, speed up construction, save money, are good for the environment, and are flexible. The report covers the growing trends and projects in prefab building markets like commercial construction, residential construction, and industrial construction. The report also covers the industry by the type of material used, like concrete, timber, glass, metal, and other types. It also analyzes the key players and the competitive landscape in the Vietnamese prefabricated building market. The impact of COVID-19 has also been included in the study. The report offers market size and forecasts for the Vietnam prefabricated buildings industry market in value (USD billion) for all the above segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key Cities

| Ho Chi Minh City |

| Hanoi |

| Danang |

| Rest of Vietnam |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key Cities | Ho Chi Minh City |

| Hanoi | |

| Danang | |

| Rest of Vietnam |

Key Questions Answered in the Report

What is the current value of the Vietnam prefabricated buildings market?

It was valued at USD 6.67 billion in 2026 and is forecast to grow steadily through 2031.

Which material leads Vietnam’s prefab sector?

Precast concrete held a 50.78% share in 2025, supported by mature local supply chains.

Why is Da Nang the fastest-growing city for prefab demand?

Rapid tourism projects and port upgrades push its market to an expected 8.44% CAGR to 2031.

How do government green-credit incentives benefit prefab builders?

Qualifying modular projects receive 2% loan subsidies and tax holidays, improving project economics.

Which product type is expanding fastest?

Panelized systems are set to grow at an 8.19% CAGR thanks to their design flexibility.

What restrains wider residential adoption of prefab homes?

Urban buyers still prefer masonry for perceived permanence, slowing the uptake of modular housing.

Page last updated on: