Vertebral Compression Fracture Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

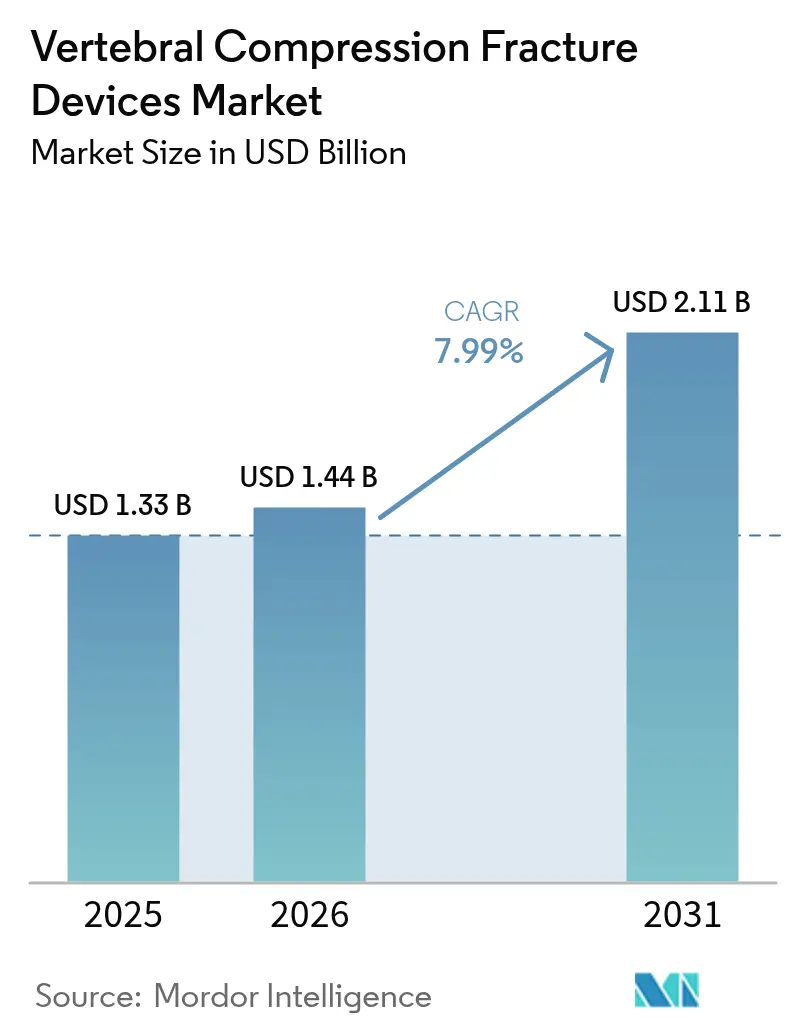

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

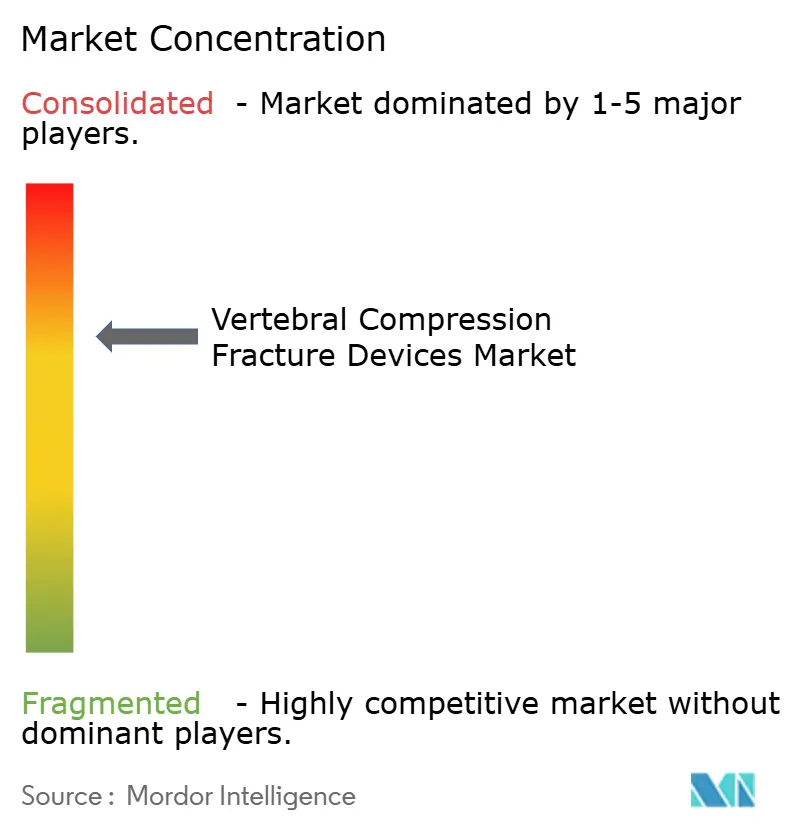

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertebral Compression Fracture Devices Market Analysis by Mordor Intelligence

Vertebral compression fracture devices market size in 2026 is estimated at USD 1.44 billion, growing from 2025 value of USD 1.33 billion with 2031 projections showing USD 2.11 billion, growing at 7.99% CAGR over 2026-2031. Population aging, rapid uptake of minimally invasive spinal interventions and a decisive industry shift toward outpatient venues are the primary engines behind this growth trajectory. Demand is further amplified by robust clinical data validating balloon kyphoplasty, AI-assisted navigation that lowers cement-leak risk, and wider reimbursement for ambulatory surgical centers (ASCs) under evolving value-based care mandates.[1]Food and Drug Administration, “Medical Devices; Quality System Regulation Amendments,” federalregister.govCompetitive activity remains intense: market leaders are consolidating portfolios, as evidenced by Globus Medical’s move into pain management through its Nevro acquisition, while regulators streamline approvals via harmonized Quality System Regulation amendments at the FDA.

Key Report Takeaways

- By product type, balloon kyphoplasty devices held 44.02% of vertebral compression fracture devices market share in 2025; expandable intravertebral implants are poised for the fastest 11.19% CAGR to 2031.

- By material, PMMA bone cement accounted for 55.98% share of the vertebral compression fracture devices market size in 2025, whereas bio-active and bioresorbable cements are tracking a 12.49% CAGR.

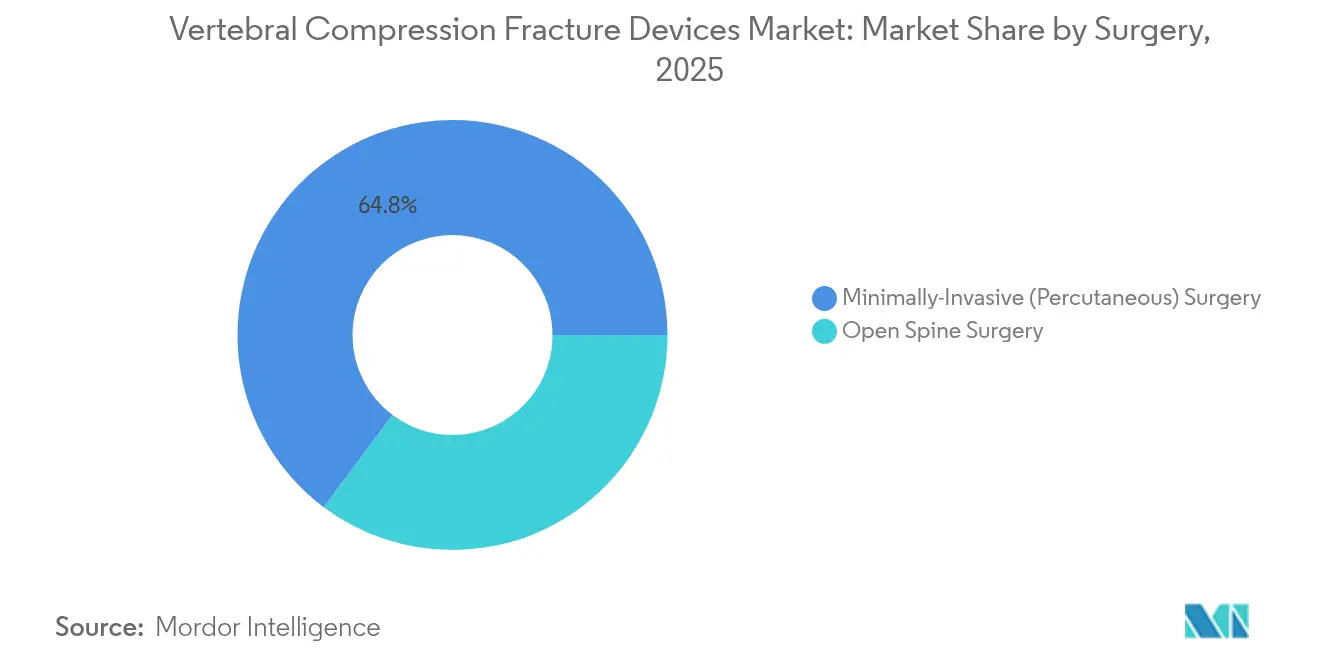

- By surgery, minimally invasive percutaneous procedures captured 64.78% revenue share in 2025 and are projected to advance at a 12.54% CAGR through 2031.

- By end user, hospitals led with 52.45% of vertebral compression fracture devices market size in 2025, but ambulatory surgical centers are the fastest riser at 11.03% CAGR.

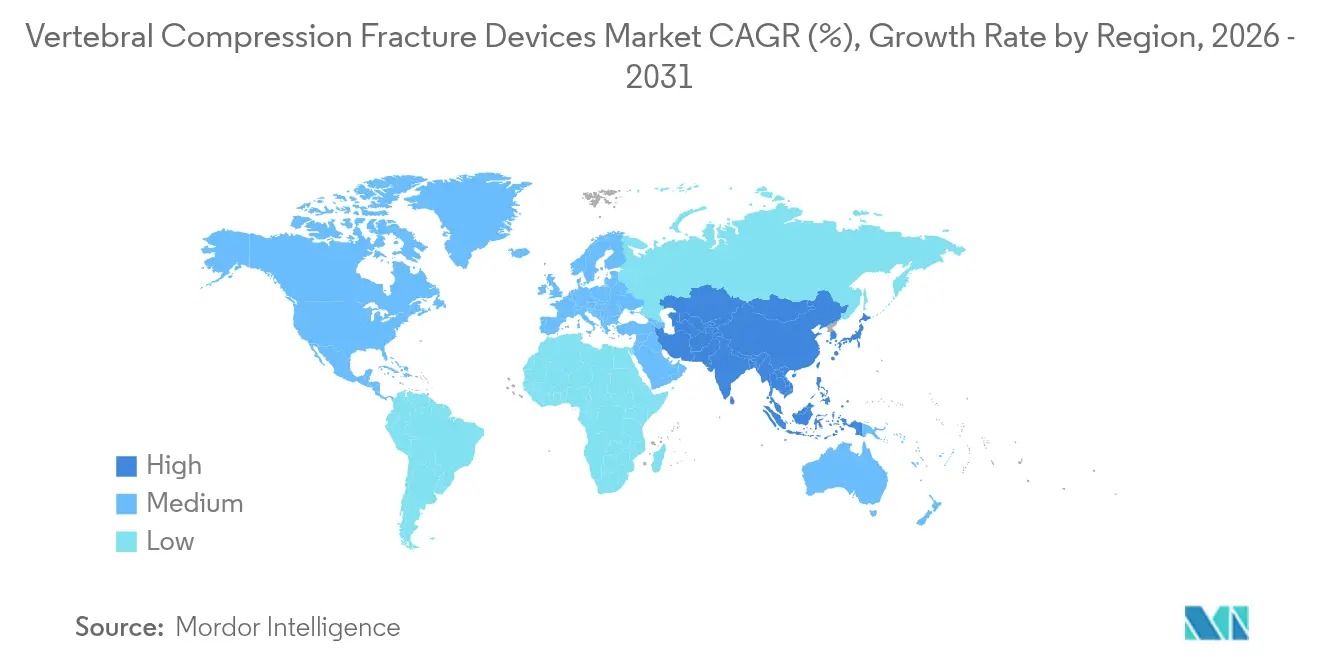

- By geography, North America commanded 38.90% vertebral compression fracture devices market share in 2025; Asia-Pacific is expanding quickest at a 10.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vertebral Compression Fracture Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoporosis-linked VCFs | +2.1% | Global, aging clusters | Long term (≥ 4 years) |

| Growing adoption of minimally invasive surgery | +1.8% | North America & EU lead, APAC follows | Medium term (2-4 years) |

| Increasing healthcare spend in emerging markets | +1.4% | Asia-Pacific core, MEA spill-over | Long term (≥ 4 years) |

| Robust clinical evidence for balloon kyphoplasty | +1.2% | Global | Short term (≤ 2 years) |

| Reimbursement shift toward ASC venues | +0.9% | Primarily North America, selective EU | Medium term (2-4 years) |

| AI-guided navigation lowering cement leakage | +0.6% | High-income regions first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of osteoporosis-linked VCFs

Global osteoporosis is forecast to affect 263.2 million people by 2034, exposing a much larger cohort to vertebral compression fractures. National studies echo the trend—12.2% fracture prevalence in urban Vietnam and heightened risk among Korean postmenopausal women.[2]Hoa T. Nguyen, “Prevalence, Incidence of and Risk Factors for Vertebral Fracture in the Community: The Vietnam Osteoporosis Study,” Nature, nature.com Even as age-standardized rates ease, absolute fracture counts climb because populations are aging, a pattern confirmed by international burden analyses. Screening gaps exacerbate the issue: only 25.7% of elderly Japanese spinal patients receive pre-operative bone mineral density tests, indicating untapped need for devices that stabilize fragile vertebrae.[3]Kenta Yamamoto, “Survey on Actual Management of Osteoporosis With the Japanese Medical Data Vision Database in Elderly Patients Undergoing Spinal Fusion,” Journal of Clinical Medicine, mdpi.comThese factors ensure sustained demand for the vertebral compression fracture devices market.

Growing adoption of minimally invasive spinal procedures

Medicare data show ASC procedures cost less than hospital outpatient departments while delivering equivalent safety, a clear incentive for providers. Vertebral augmentation reduces median stays to 2.4 days compared with 10.8 days for conservative management, trimming direct costs to USD 4,737 versus USD 7,250. Same-day discharge protocols, stress-tested during COVID-19, achieved 100% success across 164 minimally invasive cases Precision keeps improving: a novel 2D navigation system reached 0.54 mm accuracy in spine models. Together these data points underline why clinicians increasingly prefer minimally invasive options, accelerating the vertebral compression fracture devices market.

Increasing healthcare expenditure in emerging markets

Asia-Pacific nations allocate larger portions of GDP to health services, widening access to spinal technologies. In India, patients aged ≥ 70 realized substantial quality-of-life gains after vertebral procedures. Thai cost-utility models favor minimally invasive lumbar fusion over posterior methods on lifetime costs. Latin America explores value-based frameworks as clinicians study the feasibility of minimally invasive spine surgery in low-income settings. These spending patterns fuel future uptake across the vertebral compression fracture devices market.

Robust clinical evidence validating balloon kyphoplasty

Ten-year longitudinal research showed pain scores dropping from 7.9 to 2.2 and ODI disability plunging from 30.4 to 10.7 after balloon kyphoplasty. The multicenter EVOLVE study on 354 Medicare-eligible patients delivered comparable three-month improvements. Timing matters: interventions within four weeks of fracture yield stronger pain relief and kyphotic angle correction. Cement ratios optimized at 0.4-0.6 further reduce leakage. These outcomes reinforce physician confidence and expand the vertebral compression fracture devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-surgical complications (cement leakage, embolism) | -1.3% | Global, higher in low-volume centers | Short term (≤ 2 years) |

| Stringent regulatory & reimbursement hurdles | -1.1% | Region dependent | Medium term (2-4 years) |

| Price erosion of commoditized PMMA cements | -0.8% | More pronounced in emerging markets | Long term (≥ 4 years) |

| Limited long-term proof for bio-active cements | -0.6% | Premium segment worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-surgical complications (cement leakage, embolism)

Meta-analysis shows leakage in 46.2% of kyphoplasty cases, despite being the safest among augmentation options. Rare but severe sequelae include right-atrial perforation with pericardial tamponade and pulmonary cement embolism presenting as acute dyspnea. PMMA polymerization temperatures exceeding 70 °C can induce thermal necrosis at the bone interface. Modified cements and aspiration techniques drop leakage to 13% but require training and capital. These risks may curb near-term growth in the vertebral compression fracture devices market.

Stringent regulatory & reimbursement hurdles

The FDA’s 2026 Quality System Regulation integrates ISO 13485 standards, representing a compliance lift for resource-constrained manufacturers. Local Coverage Determinations demand granular functional-outcome documentation, and spinal spheres now fall under Class III PMA oversight. Global market entry is slowed by disparate approval paths, collectively tempering momentum in the vertebral compression fracture devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Expandable Implants Drive Innovation

Balloon kyphoplasty secured 44.02% of vertebral compression fracture devices market share in 2025 due to payer familiarity, straightforward workflows, and ample clinical proof. Expandable intravertebral implants, however, are growing at an 11.19% CAGR and challenge the incumbent modality by restoring vertebral height more effectively, as demonstrated in randomized trials of the SpineJack system. Conventional vertebroplasty retains market presence because of its lower cost and quick learning curve in resource-limited settings. Niche segments such as radio-frequency augmentation and vesselplasty solve complex anatomic challenges, expanding surgeon toolkits within the vertebral compression fracture devices market.

Engineering advances in expandable implants distribute endplate loads evenly, improving long-term biomechanics. The SPICO study confirmed shorter hospital stays and faster work resumption despite higher upfront device costs. Ancillary bone-cement delivery systems are also proliferating as surgeons prioritize precision; the Tripod-Fix device’s retractable arms nearly eliminated leakage in early clinical use. New entrants must now pair hardware with integrated navigation software to gain traction in the vertebral compression fracture devices market.

By Material: Bio-Active Cements Challenge PMMA Dominance

PMMA continues to dominate with 55.98% share of vertebral compression fracture devices market size due to cost advantages and decades-long surgical familiarity. Yet bio-active and bioresorbable cements are accelerating at 12.49% CAGR because clinicians aim for osteointegration and reduced long-term foreign-body presence. Calcium-phosphate fillers and ceramic hybrids provide intermediate mechanical performance and resorb naturally, while enhanced PMMA variants integrate nano-tantalum carbide for higher radiopacity and osteogenic potential.

Three-year follow-up on calcium-phosphate cement shows volume reduction without loss of stability. Hydroxyapatite/collagen composites deliver fusion rates comparable to iliac crest grafts but with less surgical trauma, hinting at broader spinal application. Material R&D will be a decisive lever for differentiation across the vertebral compression fracture devices industry, especially as payers scrutinize long-term outcomes.

By Surgery: Minimally Invasive Dominance Accelerates

Minimally invasive percutaneous procedures captured 64.78% of the vertebral compression fracture devices market size in 2025 and are forecast to compound at 12.54% CAGR. Open spine surgery remains essential for multi-level deformities but is ceding routine fracture care to percutaneous techniques. Single-session multilevel kyphoplasty cut pain scores from 8.38 to 2.15 with minimal complications, confirming efficacy in broader indications.

Navigation-guided methods reduce radiation exposure while sharpening screw accuracy. Balloon-assisted endplate reduction now treats severe thoracolumbar fractures that once required open fixation. Such procedural expansion cements minimally invasive care as the default within the vertebral compression fracture devices market.

By End User: ASCs Reshape Care Delivery

Hospitals retained a 52.45% revenue share in 2025, yet ASCs are scaling at 11.03% CAGR as payers capitalize on lower procedural costs. Trauma centers remain vital for acute fracture stabilization, whereas specialty spine clinics attract elective vertebral augmentation cases, building high-volume expertise that reinforces outcomes.

Medicare’s 2024 policy expanded ASC-eligible primary codes and simplified prior authorization. Comparative studies confirm equivalent safety between ASCs and hospital outpatient departments, strengthening payer confidence. The COVID-19 experience underscored ASC adaptability, further accelerating the vertebral compression fracture devices market shift toward decentralized care.

Geography Analysis

North America led with 38.90% share in 2025, leveraging mature reimbursement systems and sophisticated spine-care infrastructure. Medicare compares vertebral augmentation at USD 4,737 against USD 7,250 for conservative therapy, validating cost-effectiveness. ASC reimbursement reform shortened approval timelines, encouraging providers to transfer cases out of hospital outpatient departments. Canada’s universal model and Mexico’s episodic payment pilots also expand demand, each supported by regional training and NIH-sponsored clinical trials that power innovation in the vertebral compression fracture devices market.

Asia-Pacific is the fastest-growing theater at 10.31% CAGR through 2031, propelled by demographic shifts and healthcare modernization. Japan’s osteoporosis screening deficit—only 25.7% of elderly fusion patients receive pre-operative scans—underscores latent demand. China speeds device approvals through its National Medical Products Administration fast-track, while India’s elder cohorts benefit from proven post-surgical functional gains. Australia and South Korea pioneer early adoption of AI navigation, and Southeast Asian nations introduce bundled payments for minimally invasive spine surgery, collectively widening the vertebral compression fracture devices market footprint.

Europe advances steadily on the back of evidence-based medicine and pan-EU regulatory harmonization. Economic modeling projects EUR 2.8 billion in potential savings by 2040 if osteoporosis diagnosis rates improve. Germany, the United Kingdom, and France spearhead multicenter trials, while Southern Europe accelerates adoption through public-private partnership initiatives. Russia modernizes rural spine centers, tapping into EU research networks to upgrade procedural standards. South America and the Middle East & Africa lag but display growing interest in cost-optimized percutaneous approaches, indicating long-term contribution to the vertebral compression fracture devices market.

Competitive Landscape

The vertebral compression fracture devices market is moderately concentrated. Medtronic posted a 7.1% neuroscience revenue upturn anchored by the AiBLE ecosystem and expandable implant launches. Stryker divested U.S. spinal implants to VB Spine LLC so it can channel resources into interventional spine and robotics. Johnson & Johnson, via DePuy Synthes, leverages double-digit R&D investment, while Globus Medical’s USD 250 million Nevro acquisition integrates spinal cord stimulation with fracture repair.

Market rivalry pivots on evidence generation and digital workflow integration. Companies couple implants, bio-active cement and AI navigation systems into turnkey packages that match value-based reimbursement criteria. Regulatory heft is a differentiator: larger firms absorb the cost of FDA’s ISO-aligned Quality System Regulation, whereas smaller entrants may prioritize CE-first strategies to maintain burn rates. White-space fosters innovation in biodegradable cements and low-radiation imaging, creating opportunities for nimble players aiming at the vertebral compression fracture devices industry.

Strategic collaborations also proliferate. Medtronic joined forces with Merit Medical in 2024 to co-develop next-generation augmentation technology that combines the former’s spine heritage with the latter’s interventional toolkit. Elsewhere, regional OEMs in Asia-Pacific partner with academic centers to localize implant designs, addressing unique anthropometric requirements and improving penetration of the vertebral compression fracture devices market.

Vertebral Compression Fracture Devices Industry Leaders

IZI Medical Products

Stryker Corporation

Merit Medical Systems Inc.

Globus Medical, Inc.

Johnson & Johnson (DePuy Synthes)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Globus Medical agreed to acquire Nevro Corp for USD 250 million to integrate spinal-cord stimulation with fracture-repair offerings.

- January 2025: Stryker finalized the sale of its U.S. spinal implants portfolio to Viscogliosi Brothers, forming VB Spine LLC

- June 2024: Medtronic partnered with Merit Medical to co-develop a next-generation vertebral compression fracture treatment device.

Global Vertebral Compression Fracture Devices Market Report Scope

As per the scope of this report, vertebral compression fractures (VCFs) are caused by the collapse of the bone block or vertebral body in the spine, resulting in severe pain, deformity, and loss of height. These fractures are more prevalent in the thoracic spine (the middle section of the spine), particularly in the lower section. The vertebroplasty procedure involves placing medical cement in the damaged vertebral body to provide immediate pain relief and stability. Kyphoplasty, on the other hand, involves the equipment for creating a cavity underneath the broken vertebral body and injecting medical-grade bone cement into the cavity. The Vertebral Compression Fracture Devices Market is segmented by Product Type (Balloon Kyphoplasty and Vertebroplasty), Surgery (Open Spine Surgery and Minimally Invasive Spine Surgery), End-User (Hospitals, Ambulatory Surgical Centers, Trauma Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Balloon Kyphoplasty Devices |

| Vertebroplasty Devices |

| Expandable Intravertebral Implants |

| Radio-frequency Augmentation Systems |

| Vesselplasty & Mesh-containment Systems |

| Bone-cement Delivery Systems & Accessories |

| PMMA Bone Cement |

| Bio-active / Bioresorbable Cement |

| Calcium-phosphate & Ceramic Fillers |

| Others |

| Open Spine Surgery |

| Minimally-Invasive (Percutaneous) Surgery |

| Hospitals |

| Ambulatory Surgical Centers |

| Trauma Centers |

| Specialty Spine Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Balloon Kyphoplasty Devices | |

| Vertebroplasty Devices | ||

| Expandable Intravertebral Implants | ||

| Radio-frequency Augmentation Systems | ||

| Vesselplasty & Mesh-containment Systems | ||

| Bone-cement Delivery Systems & Accessories | ||

| By Material | PMMA Bone Cement | |

| Bio-active / Bioresorbable Cement | ||

| Calcium-phosphate & Ceramic Fillers | ||

| Others | ||

| By Surgery | Open Spine Surgery | |

| Minimally-Invasive (Percutaneous) Surgery | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Trauma Centers | ||

| Specialty Spine Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the vertebral compression fracture devices market?

The market generated USD 1.44 billion in 2026 and is projected to hit USD 2.11 billion by 2031 at a 7.99% CAGR.

Which product segment leads the vertebral compression fracture devices market?

Balloon kyphoplasty devices held 44.02% market share in 2025, supported by strong reimbursement and mature clinical evidence.

Why are ambulatory surgical centers important for market growth?

ASC procedures cost less than hospital outpatient equivalents and now qualify for broader Medicare coverage, driving faster 11.03% CAGR growth for this venue.

Which region is expanding fastest?

Asia-Pacific is expected to grow at a 10.31% CAGR to 2031, propelled by rapidly aging populations and expanding healthcare coverage.

What technologies are companies investing in to stay competitive?

Firms focus on AI-enabled navigation, expandable intravertebral implants, and bio-active cements that improve safety and long-term outcomes.

Page last updated on: