UV Stabilizers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV Stabilizers Market Analysis by Mordor Intelligence

The UV Stabilizers Market size was valued at USD 1.39 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 1.99 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). The growth is fueled by automotive original-equipment manufacturers who now require exterior plastics to retain gloss and mechanical strength for 10 years or more, e-commerce logistics in Asia that expose polyolefin films to high solar loads, and increasingly strict volatile-organic-compound caps on European wood coatings. Formulators are responding with next-generation hindered amine light stabilizers (HALS), triazine-based UV absorbers, and bead or granule grades that minimize contamination during compounding. Capacity additions by leading suppliers in Italy, Germany, Mexico, and China are designed to serve both regulatory-driven specialty niches and volume demand in packaging and agriculture. Feedstock volatility and supply-chain friction for HALS intermediates introduce cost pressure, yet premium additives that lower warranty risk and extend film life deliver a compelling value proposition, sustaining pricing power for market leaders.

Key Report Takeaways

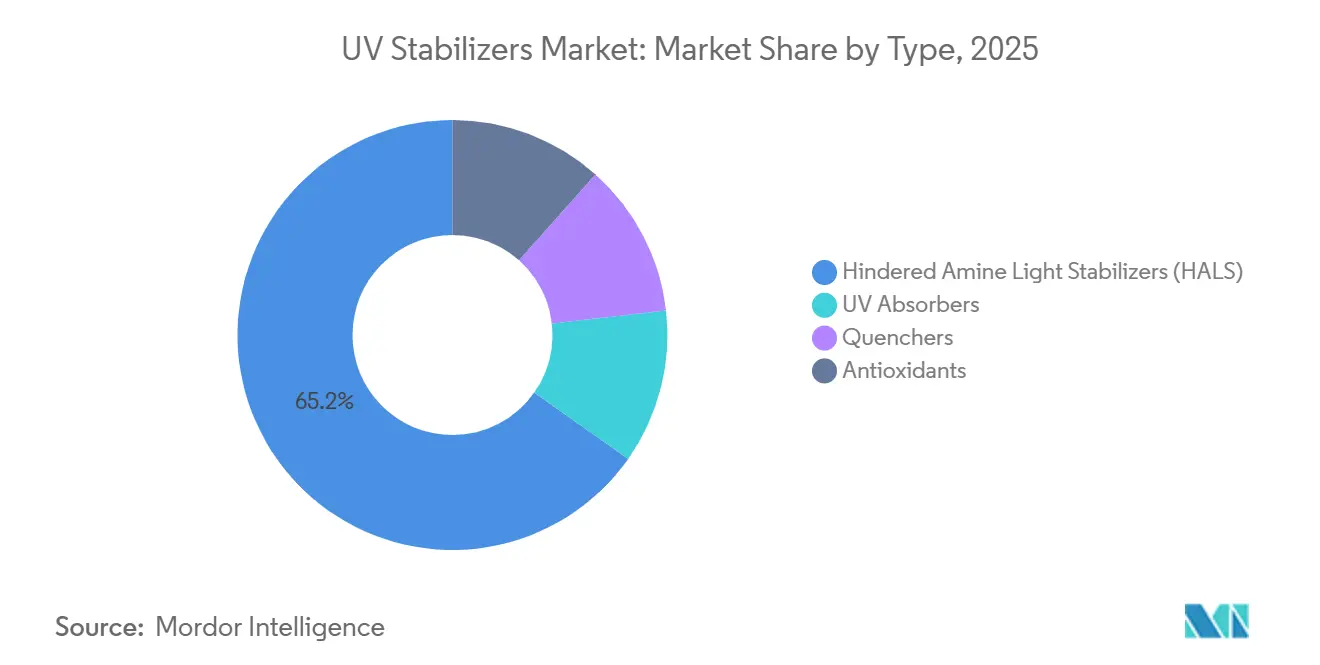

- By type, Hindered Amine Light Stabilizers led with 65.22% of UV stabilizers market share in 2025; the segment is forecast to expand at a 6.35% CAGR through 2031.

- By polymer type, polyolefins accounted for 52.13% of the UV stabilizers market size in 2025, while polyurethanes are projected to grow at a 6.48% CAGR to 2031.

- By end-use industry, automotive applications captured 41.16% of demand in 2025 and are advancing at a 6.89% CAGR over the forecast period.

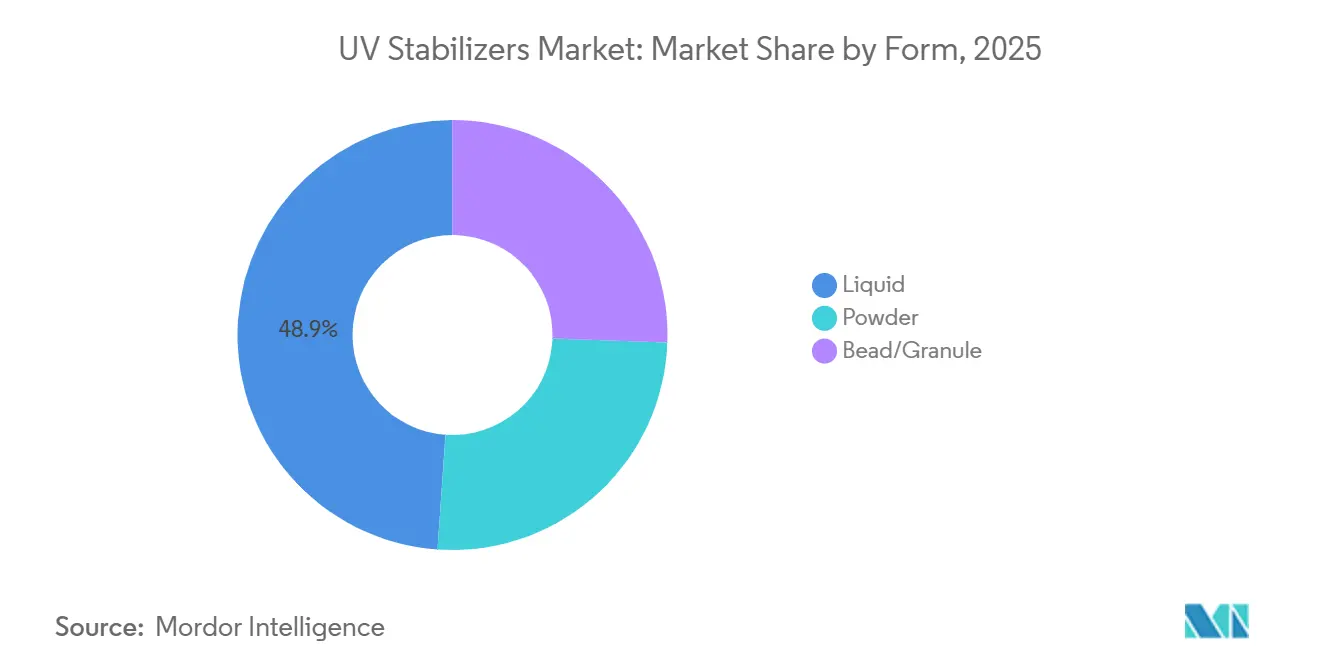

- By form, bead and granule grades are the fastest rising format, recording a 6.92% CAGR to 2031, compared with liquids that held 48.89% revenue share in 2025.

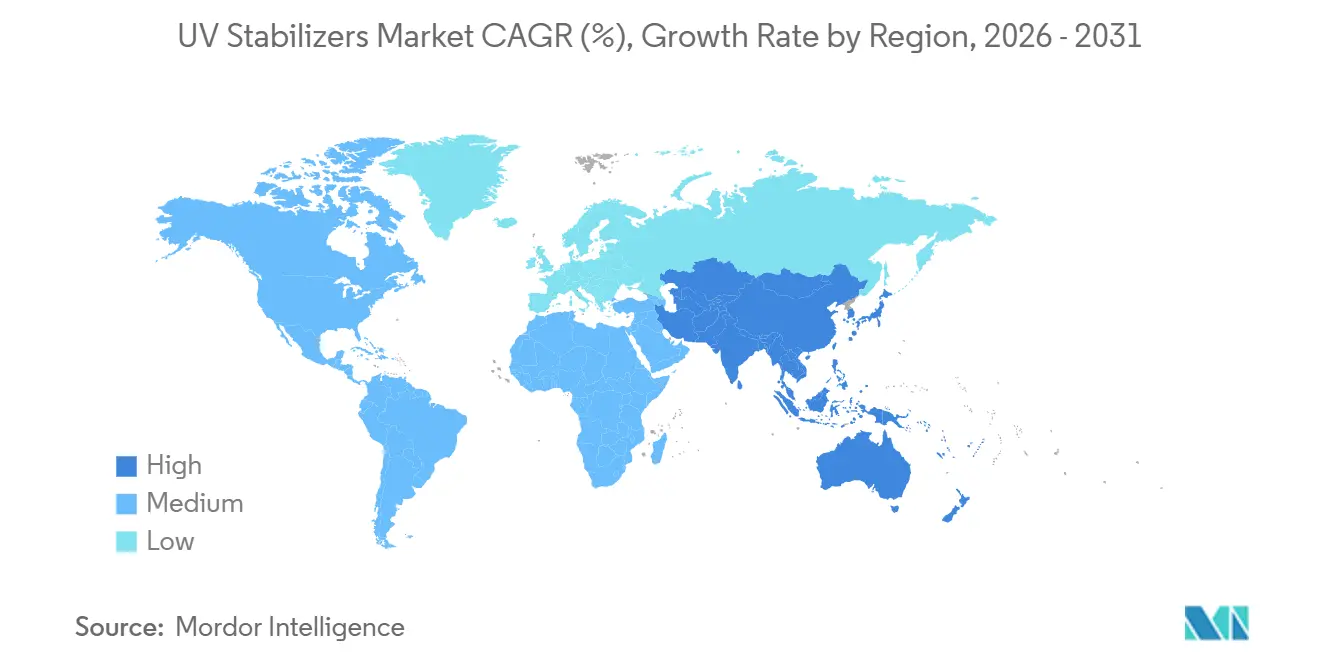

- By geography, Asia-Pacific dominated with 54.34% revenue share in 2025 and is projected to expand at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UV Stabilizers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of UV-stable polyolefin films in Asian industrial packaging | +1.4% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Shift toward low-VOC, water-borne wood coatings in Europe | +1.1% | Europe, with early adoption in Germany, France, Nordics | Short term (≤ 2 years) |

| Growing adoption of weather-resistant 3D-printed plastics in North America | +0.9% | North America, selective uptake in Western Europe | Medium term (2-4 years) |

| Surge in UV-stabilized greenhouse films across the Middle East | +1.2% | Middle East (Saudi Arabia, UAE), North Africa | Long term (≥ 4 years) |

| OEM mandates for long-life exterior automotive plastics | +1.5% | Global, led by North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of UV-Stable Polyolefin Films in Asian Industrial Packaging

In China and India, e-commerce hubs are increasingly demanding stretch-hood and shrink-wrap films that can endure outdoor storage without compromising tensile strength. To combat photo-oxidation and ensure printed graphics remain legible during multimodal transport, compounders are increasing HALS loading. India's flexible-packaging market is pivoting towards UV-stable films. These films are particularly sought after for agricultural-input bags that face extended exposure during the monsoon. Meanwhile, in China, converters are pre-qualifying HALS-rich films for export. This move caters to customers who demand stringent recycling-stream purity standards, thereby boosting regional demand. Southeast Asian warehouse operators are now storing palletized goods outdoors. This shift has hastened the adoption of weatherable polyolefin films. Consequently, while there's a notable increase in overall additive consumption, it's happening alongside a trend of film gauge reductions.

Shift Toward Low-VOC, Water-Borne Wood Coatings in Europe

Implementation of EU Directive 2004/42/EC lowered permissible VOC content, steering formulators away from solvent-borne systems toward water-based coatings that require hydrolytically stable UV absorbers[1]European Commission, “Directive 2004/42/EC,” EUROPA.EU. Benzotriazole chemistries leach out of aqueous media, so producers have migrated to triazine UV absorbers and polymeric HALS that resist extraction. Germany and Nordic countries pioneered adoption in 2025, but Southern Europe is closing the gap as building codes tighten. Suppliers must reformulate legacy lines and validate compatibility with new resin platforms, embedding UV protection, biocides, and rheology modifiers into single masterbatches. While reformulation incurs short-term cost, it opens premium pricing opportunities for turnkey additive packages that guarantee color stability on exterior wood façades for at least five years.

Growing Adoption of Weather-Resistant 3D-Printed Plastics in North America

Industrial additive manufacturing has transitioned from mere prototyping to producing functional components, now catering to automotive tooling, drone housings, and outdoor recreational gear. Given that polycarbonate and polyamide 12 filaments are prone to rapid degradation under sunlight, there's a growing trend to adopt HALS and UV absorbers. These additives help maintain the filaments' impact strength throughout their multi-year service life. In a significant move, U.S. automotive OEMs have begun qualifying UV-stabilized printed brackets for under-hood applications, achieving a remarkable reduction in tooling lead time. Meanwhile, aerospace suppliers are making strides by embedding weatherable filaments into ground-support fixtures, opting for these over traditional machined aluminum due to the weight savings. These applications are establishing new qualification pathways, placing a premium on accelerated-weathering testing as opposed to the conventional legacy resin approvals.

Surge in UV-Stabilized Greenhouse Films Across the Middle East

Saudi Arabia's Vision 2030 and the UAE's Food-Security Initiative are driving the establishment of large-scale greenhouses in the region. These greenhouses utilize polyethylene films, engineered to endure the harsh desert sunlight. Growers have observed that extending film replacement intervals reduces payback periods. Suppliers of these films are now emphasizing the use of HALS concentrations in the outer layer. They're also incorporating infrared blockers to reduce cooling loads. Manufacturers from Asia and Europe have set up local converting lines, targeting projects, thereby securing a steady demand for additives. Furthermore, neighboring markets in North Africa are adopting these specifications, leading to a swift regional uptake of premium stabilizer packages.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in feedstock prices | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Supply-chain disruptions in HALS intermediates | -0.6% | North America and Europe, sourcing from Asia | Medium term (2-4 years) |

| Uptake of high-barrier monolayer films reducing stabilizer demand | -0.4% | Europe and North America, selective in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Feedstock Prices

During 2024–2025, costs for benzene and phthalic anhydride fluctuated, tightening margins for formulators lacking long-term petrochemical contracts. Spot buyers in the Asia-Pacific experienced the most pronounced price swings, while producers in Europe contended with high energy tariffs, driving up costs for aromatic intermediates. As a result, smaller firms are postponing capacity expansions and cutting back on research and development budgets, which is hindering the commercialization of advanced UV stabilizers. While integrated major companies are mitigating risks through derivatives trading and backward integration, the entire sector remains susceptible to geopolitical upheavals and impending carbon-pricing initiatives that threaten to escalate feedstock costs.

Supply-Chain Disruptions in HALS Intermediates

In 2024, China tightened its grip on the export of certain amine derivatives, pushing back lead times for HALS precursors[2]Chemical & Engineering News, “China Export Controls on Amine Derivatives,” CEN.ACS.ORG. In response, compounders in Europe and North America either bolstered their safety stocks or pivoted to suppliers in Japan and India, incurring a cost premium. Automotive clear coats and engineering plastics, particularly specialty grades, are under heightened threat due to qualification cycles stretching up to 18 months. While multinationals have unveiled plans for regional production investments, the new capacities won't be operational until 2027. This delay creates a medium-term supply gap, potentially stunting the growth of the UV stabilizers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: HALS Dominance Anchored in Polyolefin Synergies

Hindered amine light stabilizers controlled 65.22% of the UV stabilizers market share in 2025, and the segment will post a 6.35% CAGR to 2031 as NOR-HALS grades extend exterior plastic life beyond 10 years. UV absorbers face slower growth due to their limited efficacy in thin films, a challenge posed by volatility and migration. Nonetheless, UV absorbers remain crucial for clear coatings and polycarbonate glazing. Meanwhile, quenchers and antioxidants play niche roles, balancing the equation in synergistic blends. BASF's 2025 introduction of Tinuvin NOR 600 underscores the industry's trend: formulators are willing to pay a premium for NOR-HALS, especially those that minimize haze in dark automotive components.

There's a growing demand for packages tailored to specific polymers. For instance, polyurethane dispersions are now opting for secondary HALS that can endure alkaline settings. Similarly, filaments used in 3D printing are turning to hydroxyphenyltriazines, which are compatible with polyamide 12. In Europe, nickel-based quenchers are under heightened scrutiny due to REACH regulations, leading to a gradual pivot towards organic substitutes. Furthermore, integrated additive packages that merge HALS, UV absorbers, and antioxidants not only streamline the formulation process but also mitigate antagonistic interactions. This trend positions suppliers with diverse portfolios for growth that outpaces the market average.

By Polymer Type: Polyurethanes Outpace Polyolefins on Foam and Coating Growth

Polyolefins represented 52.13% of 2025 demand, supported by packaging films, agricultural covers, and automotive parts, yet their growth moderates as thinner films and monolayer barriers reduce stabilizer intensity. Polyurethanes will post a 6.48% CAGR through 2031 as spray-foam insulation and automotive seating foams demand additives that prevent yellowing and maintain flexibility. PVC is witnessing slower growth due to competition from alternative materials in window profiles and siding. In contrast, engineering plastics like polycarbonate and polyamide are expanding, driven by trends in automotive lightweighting and the rise of 3D printing.

Gains in polyurethane are fueled by mandates for energy-efficient insulation and lightweight seating solutions, which can reduce a vehicle's mass. During installation, spray-foam installers opt for HALS, known for their UV resistance, while seating suppliers choose absorbers that align with isocyanate chemistries. Although styrenics and elastomers occupy a niche space, BASF is making strategic moves. Their 2026 expansion in Puebla, Mexico, is set to cater specifically to customers in polyurethane and engineering plastics, focusing on antioxidants and UV stabilizers.

By End-Use Industry: Automotive Leadership Driven by Warranty Economics

Automotive applications commanded 41.16% of 2025 volume and will grow at a 6.89% CAGR, reflecting OEM requirements for long-life exterior plastics. Packaging experiences slower growth due to the adoption of lightweight materials and monolayers, which reduce the need for stabilizers. Agriculture enjoys growth, spurred by greenhouse initiatives in the Middle East and India. The building and construction sector sees an uptick, driven by demand for UV-stable PVC profiles and polycarbonate roofing. While other sectors, such as electrical and electronics, remain modest, they exhibit stability.

In the automotive realm, warranty considerations fuel the adoption of additives. An investment in additives can prevent potential claims for faded parts, highlighting the financial advantage of adopting HALS. While sustainability efforts temper growth in packaging, agriculture reaps rewards from government-backed subsidies promoting protected cultivation. The construction sector benefits from energy codes in Europe that prioritize insulated window profiles and resilient glazing.

By Form: Bead and Granule Grades Gain on Masterbatch Precision

Liquid formulations secured 48.89% of revenue in 2025 because they integrate seamlessly into high-throughput polyolefin compounding. Bead and granule grades, however, will log a 6.92% CAGR thanks to dust-free handling and accurate gravimetric dosing, attributes prized by automotive and engineering-plastic processors. Powders lose ground due to occupational-health costs and dust-collection requirements.

Bead and granule grades match resin bulk density, enabling precise dosing without airborne particulates. Their price premium is offset by reduced clean-up time and minimized contamination risk. BASF added bead and granule capacity in Italy and Germany in 2025 to serve European automotive clients. Liquids remain dominant in commodity films, but by 2031, bead and granule formats could increase their share as regulators tighten worker-exposure limits.

Geography Analysis

Asia-Pacific held 54.34% of global revenue in 2025 and will expand at a 6.61% CAGR through 2031. In 2025, China's flexible-packaging sector accounted for a significant portion of the regional stabilizer volume. This surge was driven by exporters' demand for UV-resistant films that align with European recycling standards. Meanwhile, in 2025, India subsidized greenhouses, fueling a spike in demand for polyethylene films infused with HALS loading. Japan and South Korea outpaced the market, supplying engineering-plastic components pivotal for automotive and electronics exports. In response to the burgeoning local and export demand, BASF expanded its HALS capacity at the Nanjing plant.

In 2025, North America claimed a notable share of the global market value and is projected to grow steadily through 2031. The region's growth is bolstered by automotive reshoring and a surge in additive manufacturing, driving up demand for weatherable thermoplastic olefins and UV-stabilized filaments. In Canada, the construction sector is turning to UV-stable polycarbonate roofing to withstand snow loads. Simultaneously, Mexico's Puebla expansion is ensuring a steady regional supply of additives. Europe is on a growth trajectory, attributed to mature construction markets balancing out the robust, regulation-driven demand for coatings. Notably, Germany, France, the UK, and Italy collectively account for a significant portion of Europe's revenue, largely due to adherence to Directive 2004/42/EC.

South America is set to rise, thanks to Brazil's tropical agriculture and Argentina's focus on PVC construction. The Middle East and Africa, while currently representing a smaller share, are expanding rapidly. This growth is spurred by Saudi Arabia and the UAE's investments in protected agriculture. Additionally, South Africa's ambitions in automotive exports are driving up the demand for UV-stable thermoplastic olefins. Thus, regional opportunities are diverse, spanning from Asia-Pacific's volume growth and North America's lucrative automotive upgrades to the Middle East's burgeoning greenhouse industry.

Value Chain Analysis

The UV stabilizers value chain begins with petrochemical and fine-chemical feedstocks (notably benzene-linked aromatics and amine derivatives used in HALS intermediates), then moves into synthesis of UV absorbers, HALS/NOR-HALS, quenchers, and tailored blends. Additive producers convert these materials into liquid, powder, or bead/granule grades and supply to resin producers and compounders directly or through masterbatchers, with demand ultimately pulled by automotive plastics, packaging films, agricultural films, coatings, and construction polymers.

Midstream conversion and qualification are a recurring bottleneck, particularly when end users ask for multi-year outdoor durability and low migration in thin films and exterior parts. Supply-chain resilience has become more visible after disruptions in amine-derivative availability and lead times, including 3V Sigma USA launching domestic production of its Uvasorb HA44 HALS at a South Carolina facility in March 2025 to improve regional supply security. Distribution generally follows direct contracting for large automotive and film accounts, while specialty chemical distributors support smaller converters. Technical service, including dispersion support, accelerated weathering data, and polymer-specific packages, helps differentiate suppliers across these channels.

Competitive Landscape

The UV stabilizers market is moderately fragmented. Strategic priorities cluster around regional capacity expansion, premium chemistry development, and integration into masterbatch production. White-space opportunities involve bio-based stabilizers, nano-dispersed additives that cut loading rates, and combined UV-antimicrobial-flame retardant packages. Patent filings from 2024–2025 show activity in polymer-bound HALS that survive mechanical recycling, addressing circular-economy mandates. Suppliers offering technical services such as in-line spectroscopy for additive dispersion can command premiums and deepen ties with tier-one customers. Regional regulatory divergence, notably China’s GB food-contact norms, creates niches that agile local players exploit faster than global incumbents.

UV Stabilizers Industry Leaders

BASF SE

Clariant

Songwon

ADEKA Corporation

Solvay

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Most opportunities center on higher-performance, lower-migration stabilization packages for long-life exterior plastics and films, where additive selection is tied to warranty economics and extended qualification cycles. BASF’s continued investment in premium NOR-HALS and related portfolios, including Tinuvin NOR 600 positioned for roofing and artificial turf at K 2025, aligns with demand for outdoor applications beyond traditional packaging. In parallel, compliance-driven reformulation in coatings and plastics is supporting triazine-based UV absorbers and polymeric HALS that better tolerate water-borne systems and resist extraction, which supports the broader shift away from legacy benzotriazole chemistries in regulated environments.

Localization and capacity adds also create whitespace for suppliers that can secure intermediates and shorten lead times for converters. Clariant commissioned a second production line for Nylostab S-EED in Cangzhou, China, in August 2025, indicating targeted investment around engineering plastics and application-specific stabilizers. Outside established use cases, floating solar platforms and weather-resistant additive-manufactured components are raising demand for stabilizers that can be validated for extreme UV exposure and long service life, favoring suppliers that can pair products with application testing and material certification support.

Recent Industry Developments

- April 2026: BASF announced an expansion of its HALS and NOR-HALS manufacturing capacities. This increases supply availability for high-performance light stabilizers used in long-life plastics such as agricultural films and durable outdoor applications, where qualification and continuity of supply are important for converters.

- October 2025: BASF launched Tinuvin NOR 600, a next-generation NOR-HALS light stabilizer for PVC and polyolefin applications, at K 2025. The product positioning in roofing and artificial turf points to supplier focus on higher-durability outdoor end uses that can support premium formulations.

- July 2024: BASF launched Tinuvin NOR 211 AR, a heat and light stabilizer system for agricultural plastics in intensive horticulture under its VALERAS portfolio. This broadened the toolkit for plasticulture films exposed to high UV radiation and agrochemical conditions, pushing more application-specific stabilizer packages into mainstream film specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of UV stabilizer additives used to protect plastics, coatings, and other polymer-based materials from sunlight-driven degradation during use outdoors and under strong lighting.

Scope exclusions: We exclude sunscreen active ingredients and internal transfers inside vertically integrated masterbatch operations when there is no external sale.

Segmentation Overview

- By Type

- Hindered Amine Light Stabilizers (HALS)

- UV Absorbers

- Quenchers

- Antioxidants

- By End-Use Industry

- Packaging

- Automotive

- Agriculture

- Building and Construction

- Adhesives and Sealants

- Other End-user Industries (Electrical and Electronics, etc.)

- By Polymer Type

- Polyolefins (PE, PP)

- PVC

- Polyurethane

- Engineering Plastics (PC, PA, PET)

- Others (Styrenics and Rubber and Elastomers)

- By Form

- Liquid

- Powder

- Bead/Granule

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries, build the first demand map, and anchor the model to observable indicators. We reviewed public sources including UN Comtrade trade data, USITC trade statistics, Eurostat manufacturing indicators, and industry safety and usage notes from agencies such as the US EPA. For plastics and coatings context, we also used sources such as the American Chemistry Council and peer-reviewed polymer degradation and additive-performance papers.

To translate demand signals into value, we cross-checked historical price direction and feedstock-linked movements using public chemical price commentary, plus company annual reports and investor presentations that discuss additive portfolios and end-market exposure. Where needed, we used paid subscription data for company financials and intelligence, a patent database, and an import-export shipment-level database to support consistency checks on supplier footprints and application focus. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done to pressure-test the desk model and close gaps that public data does not explain well, including typical loading rates and how pricing differs by stabilizer family and performance grade. We spoke with participants across the value chain, including additive suppliers, compounders, and downstream users in plastics and coatings, and we covered major demand regions so the assumptions did not reflect one geography only.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 43% | EMEA: 36% |

| Smaller Players: 14% | Managers: 45% | Americas: 19% |

Market-Sizing & Forecasting

For sizing, we used a top-down and bottom-up blended approach. We started with polymer and coatings demand pools and then reconstructed UV stabilizer consumption through penetration and additive loading rates by major end uses. The top-down path was anchored to visible indicators such as plastics processing activity, coatings production trends, and trade flows for relevant chemical additive categories, which we converted to value using price ranges validated in interviews.

We also used a selective bottom-up approximation to corroborate totals, where supplier and channel checks helped confirm whether implied volumes and average selling prices were realistic. Key inputs included the mix shift between HALS and UV absorbers, typical dosage ranges in packaging versus durable outdoor parts, regional manufacturing intensity (especially in Asia), replacement cycles tied to weathering performance, and the pace of lightweighting and plastic substitution in end uses. Where gaps remained, we filled assumptions using nearest-application proxies and then rechecked with respondents before finalizing.

For forecasting, scenario analysis was used so the outlook could reflect different paths for construction activity, automotive build rates, packaging growth, and regulatory or sustainability-driven material changes. Growth rates were not carried forward mechanically, and they were adjusted using expert consensus on pricing progression, substitution between stabilizer chemistries, and expected capacity additions or constraints.

Data Validation & Update Cycle

Model outputs were validated through several checks, and the goal was to ensure totals stayed consistent with independent signals. We compared implied consumption and value against external markers such as plastics and coatings production trends, import-export movements, and disclosed business commentary from additive suppliers.

When large variances showed up by region or application, assumptions were revisited and respondents were re-contacted to confirm what changed, such as a pricing step-up, a demand slowdown, or a material shift. Each report goes through multi-step analyst review before sign-off, and it is refreshed annually with interim updates when material events occur. Before delivery, a final pass is completed so the output reflects the latest available information.

Mordor Intelligence's Uv Stabilizers Market Estimate Compared With Other Published Estimates

Published market numbers for UV stabilizers can differ even when the topic looks similar, because each publisher may count a different set of additive chemistries, price points, and end-use routes. Differences also appear when one model leans more on supplier revenue disclosures while another starts from polymer demand and dosage assumptions.

The largest gap drivers in this market usually come from whether the estimate blends in adjacent light stabilizer categories, how masterbatch value versus active ingredient value is treated, and whether internal transfers are counted as sales. Currency timing and the chosen base year also matter, since additive prices can move with feedstocks and contract cycles, and a model that updates ASPs only once can drift away from current market reality. Excluding non-market transactions and keeping the scope to external sales is one reason the 2026 value lands at USD 1.48 B for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.48 B (2026) | |

| Industry Publisher A | USD 1.78 B (2025) | Uses a different base year and may capture a broader value definition, which can pull in more of the formulated masterbatch value instead of the stabilizer-active value only. |

| Industry Publisher B | USD 1.64 B (2025) | Relies on 2025 as the base year and applies a longer forecast window, and the included type buckets can be wider, which can change how blends and adjacent stabilizer families are counted. |

The spread in these figures is mainly explained by what is being priced (active additive versus formulated form), the treatment of internal versus external sales, and the base-year and currency timing choices. By keeping the model tied to demand indicators like polymer use and realistic loading rates, and then cross-checking against supplier and channel feedback, the final number stays traceable to repeatable inputs rather than broad category rollups.

Key Questions Answered in the Report

What is the current value of the UV stabilizers market?

The UV stabilizers market is valued at USD 1.48 billion in 2026.

How fast will the market grow over the next five years?

It is forecast to climb to USD 1.99 billion by 2031, advancing at a 6.12% CAGR.

Which polymer type is growing fastest in stabilizer consumption?

Polyurethanes are projected to expand at a 6.48% CAGR, driven by spray-foam insulation and automotive seating.

Why are bead and granule stabilizers gaining popularity?

They offer dust-free handling and precise dosing, supporting masterbatch producers and high-spec automotive applications.

Which region contributes most to global demand?

Asia-Pacific accounts for 54.34% of revenue in 2025, supported by China’s packaging sector and India’s greenhouse-film adoption.

What is driving automotive demand for UV stabilizers?

OEM warranty extensions on exterior plastics require additives that maintain color and gloss for up to 15 years, boosting premium HALS uptake.

Page last updated on: