Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.99 Billion |

| Market Size (2031) | USD 10.36 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

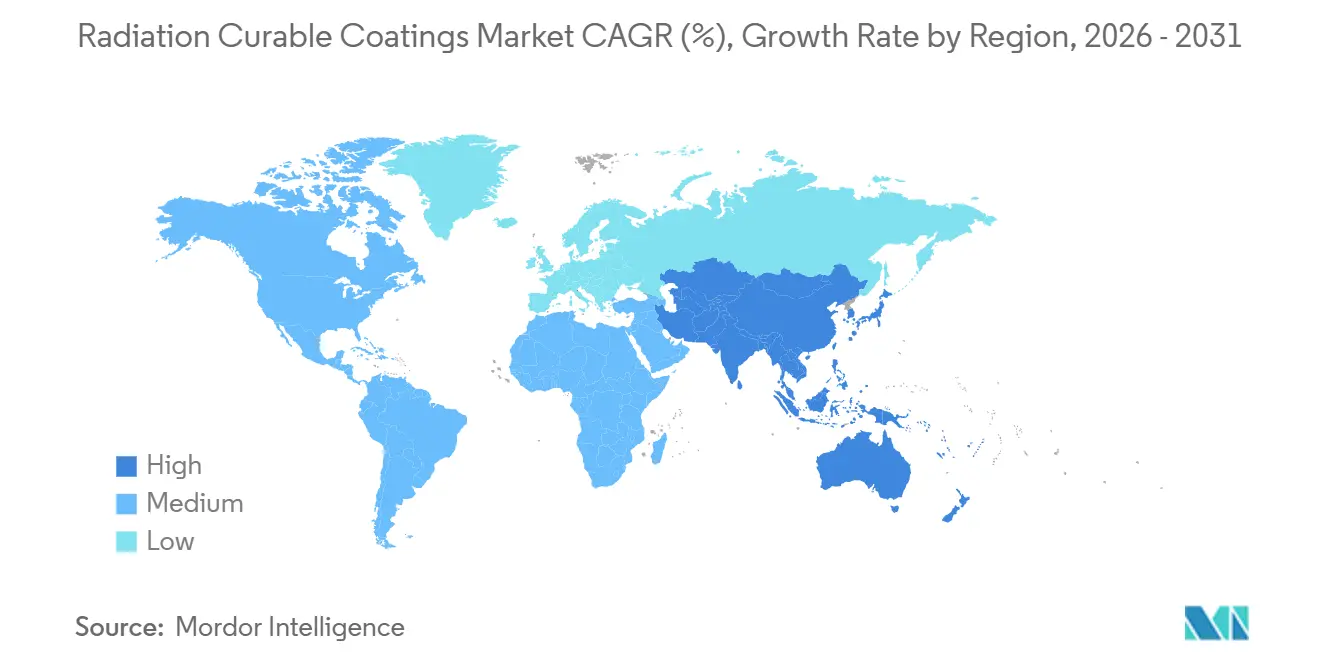

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

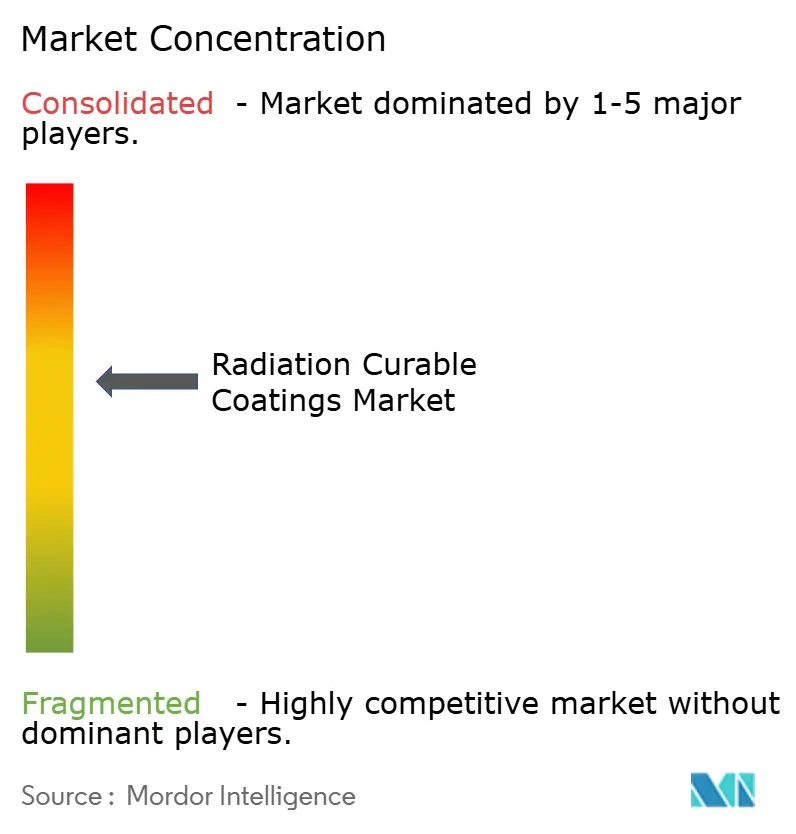

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiation Curable Coatings Market Analysis by Mordor Intelligence

The Radiation Curable Coatings Market size is projected to expand from USD 7.60 billion in 2025 and USD 7.99 billion in 2026 to USD 10.36 billion by 2031, registering a CAGR of 5.34% between 2026 to 2031. Mounting regulatory pressure on volatile-organic-compound (VOC) emissions, accelerating replacement of mercury lamps with LED arrays, and continuous advances in oligomer and photoinitiator chemistries underpin this growth. Rising capital investments in high-throughput packaging, furniture, and automotive lines reinforce demand, while energy savings from LED-UV systems compared with mercury lamps bolster cost competitiveness. Asia-Pacific dominates capacity additions because China, India, and Vietnam are scaling export-oriented furniture and flooring output, whereas North American and European growth depends on automotive original-equipment-manufacturer (OEM) adoption of in-line LED curing.

Key Report Takeaways

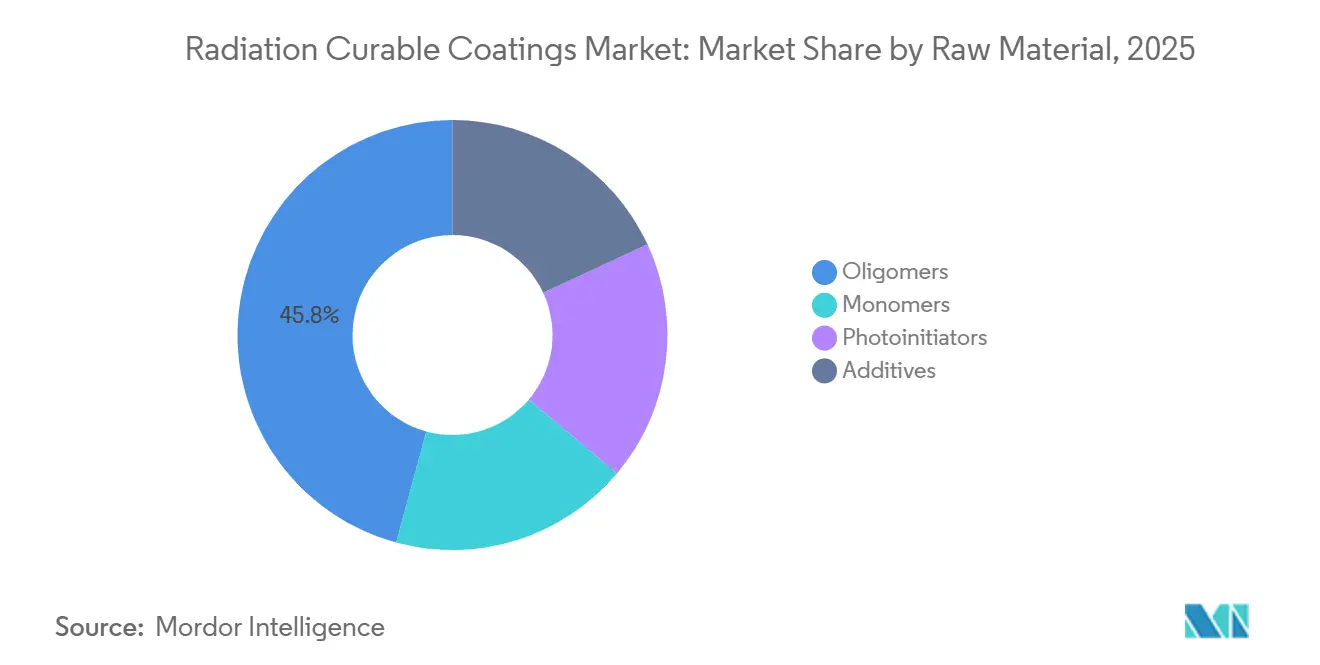

- By raw material, oligomers controlled 45.79% of the radiation-curable coatings market share in 2025, while photoinitiators are poised to grow at a 6.89% CAGR to 2031.

- By curing technology, UV lamp systems delivered 69.71% of the radiation-curable coatings market size in 2025; electron-beam curing is expected to expand at a 7.12% CAGR through 2031.

- By resin chemistry, epoxy acrylates captured 30.50% share of the radiation-curable coatings market size in 2025, whereas urethane acrylates will outpace others at 6.35% CAGR up to 2031.

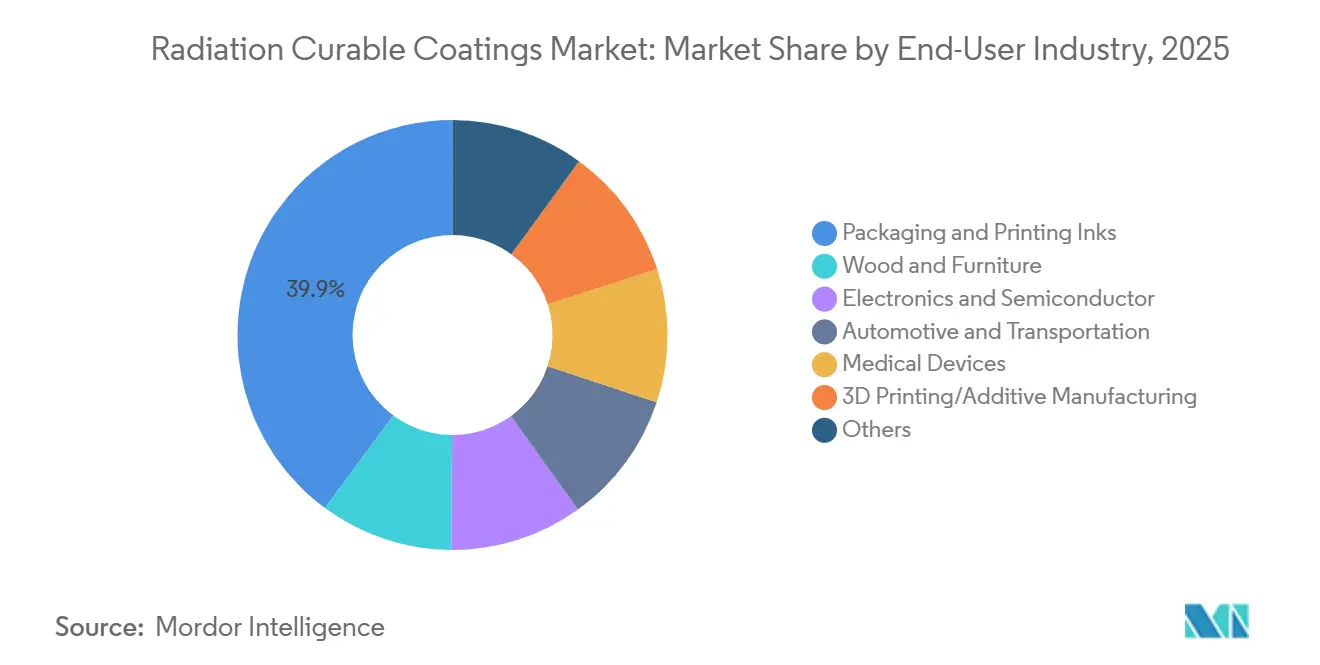

- By end-user industry, printing and packaging inks led with 39.90% share in 2025; 3D printing and additive manufacturing should accelerate at 6.25% CAGR to 2031.

- By geography, the Asia-Pacific held 41.26% of 2025 revenue and is forecast to register a 6.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radiation Curable Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC and carbon-neutrality regulations accelerate solvent-free UV/EB adoption | +1.8% | Global, with peak enforcement in EU, China, and select US states (California, New York) | Medium term (2-4 years) |

| Demand for high-throughput packaging and digital printing lines | +1.5% | Global, concentrated in Asia-Pacific flexible packaging hubs and North America label printing | Short term (≤ 2 years) |

| Growth in ultra-thin electronic and wearable device conformal coatings | +0.9% | APAC core (China, South Korea, Taiwan), spill-over to North America automotive electronics | Medium term (2-4 years) |

| Rapid expansion of Asia-Pacific furniture and flooring manufacturing capacity | +1.2% | China, India, Vietnam, Indonesia; secondary impact in Southeast Asia export corridors | Long term (≥ 4 years) |

| OEM shift to in-line LED-UV curing for automotive interior parts | +0.7% | North America, Europe, China (EV production clusters in Shanghai, Guangzhou, Stuttgart, Detroit) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC and Carbon-Neutrality Regulations Accelerate Solvent-Free UV/EB Adoption

Starting June 2026, China's GB 30981 standards will limit coating VOCs to specific levels. These standards will also phase out solvent-borne polyurethane and alkyd systems in the industrial wood and metal sectors. At the same time, the European Union, under REACH Annex XVII, is placing restrictions on dimethylacetamide and N-ethyl-2-pyrrolidone[1]“REACH Annex XVII Solvent Restrictions,” European Chemicals Agency, echa.europa.eu. This move is steering industries towards 100%-solids UV and electron-beam (EB) chemistries, with a compliance deadline set for December 2026. Meanwhile, California’s South Coast Air Quality Management District has already implemented stricter limits than the upcoming U.S. federal regulations, pushing converters to consider radiation-curable alternatives. Additionally, LED-UV installations are proving to be a game-changer, offering significant energy savings compared to traditional mercury lamps. This not only allows for a return on investment in a short period but also aids coaters in reducing Scope 2 emissions as part of broader corporate decarbonization efforts.

Demand for High-Throughput Packaging and Digital Printing Lines

Flexible-packaging web speeds now exceed 300 m/min with UV-LED laminating adhesives such as Henkel’s 2025 Loctite series, scrapping thermal-oven dwell time and enabling 24-hour order-to-ship cycles. Digital presses like HP’s Indigo 25K integrate instant-cure UV inks, shrinking production windows for personalized campaigns and small batches. Food-contact compliance remains crucial: the European Printing Ink Association revised its photoinitiator positive list in 2025, steering formulators toward high-molecular-weight polymeric initiators that remain immobilized in cured films[2]“Photoinitiator Suitability List,” EuPIA, eupia.org . Converters mastering low-migration systems secure premium dairy and confectionery contracts governed by Swiss Ordinance SR 817.023.21 and U.S. FDA 21 CFR 175.300.

Growth in Ultra-Thin Electronic and Wearable Device Conformal Coatings

IPC-CC-830C now covers UV-curable acrylics qualified for sub-25-µm coatings that pass salt-spray and dielectric tests on high-density printed-circuit boards. Dow introduced UV-curable silicone-acrylate hybrids in 2025 that maintain flexibility across −40 °C to 125 °C thermal cycles demanded by electric-vehicle inverters. Zero-VOC formulations avoid outgassing that can degrade OLED displays and lithium-polymer cells, an imperative for wearables that undergo ISO 10993 biocompatibility evaluation.

Rapid Expansion of Asia-Pacific Furniture and Flooring Manufacturing Capacity

In 2024, China rolled out a significant number of wood-furniture units. Notably, a majority of its laminate-flooring lines have adopted UV coatings, ensuring compliance with GB 18580 formaldehyde standards. Meanwhile, in India, manufacturers from Gujarat and Maharashtra are retrofitting solvent lines with UV technology. This move caters to European retailers prioritizing REACH compliance. Such initiatives bolster India's domestic furniture market, projected to reach a substantial valuation by 2030. Over in Vietnam, the nation exported a considerable amount of furniture in 2024. To cater to the U.S. market's demand for high-gloss aesthetics, Vietnam is harnessing UV technology. This ensures adherence to the California Air Resources Board's VOC caps.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialized oligomers and photoinitiators | -0.8% | Global, acute in price-sensitive segments (furniture, general industrial) and emerging markets | Short term (≤ 2 years) |

| Supply tightness after EU REACH reclassification of acyl-phosphine oxides | -0.6% | Europe, North America; secondary impact in Asia-Pacific via multinational supply chains | Medium term (2-4 years) |

| Thermal sensitivity of emerging bio-based packaging substrates | -0.3% | Europe, North America (sustainable packaging mandates); limited impact in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialized Oligomers and Photoinitiators

Urethane-acrylate oligomers command a higher price compared to commodity alkyds. Meanwhile, bis-acyl-phosphine-oxide photoinitiators are priced higher, and low-migration polymeric grades are the most expensive. In Q2 2025, acrylic-acid feedstock prices surged due to outages in China, putting pressure on converters who couldn't hedge against raw-material risks. Suppliers like BASF and Allnex, being vertically integrated, mitigate this volatility by owning precursors like acrylic acid or isocyanate. In contrast, independent formulators frequently grapple with margin erosion.

Supply Tightness after EU REACH Reclassification of Acyl-Phosphine Oxides

In 2023, Triphenylphosphine oxide was elevated to Reproductive Toxicity 1B status, mandating authorization under REACH Annex XIV by 2026 and tightening its availability in Europe. LED-UV systems, which depend on TPO or TPO-L for absorption in the 385–405-nm range, now face challenges: formulators can either up the dosage of alternatives, endure slower line speeds, or pivot to EB processes that completely eliminate photoinitiators. Between 2024 and 2025, patent activity spiked for polymerizable photoinitiators exceeding 1,000 Da, aiming to curb migration. Yet, with scale-up timelines stretching 12 to 18 months, supply gaps remain extended.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Photoinitiator Innovation Outpaces Oligomer Dominance

Oligomers contributed 45.79% of 2025 revenue. These oligomers, with their polymer backbones, play a pivotal role in defining mechanical performance. Urethane-acrylate and epoxy-acrylate variants lead the market, driven by the need for abrasion resistance in furniture and chemical adhesion in electronics. Monomers, responsible for diluting viscosity and adjusting cure speed, constituted a significant portion of the expenditure. Meanwhile, additives, including wetting and slip agents, carved out a small yet crucial niche.

Photoinitiators will grow at a 6.89% CAGR to 2031, driven by REACH classifications necessitating reformulation. Polymerizable initiators enable food-contact and medical applications without migration risks. Converters are investing in proprietary blends, customizing photoinitiator triplet energies to align with specific LED wavelengths, ensuring a competitive edge. As a result, the market size for photoinitiators in radiation-curable coatings is projected to grow, enhancing supply-chain leverage for specialized producers.

By Curing Technology: Electron Beam Accelerates in Metal and Battery Lines

UV-lamp platforms supplied 69.71% of 2025 revenue, yet electron-beam systems will crest 7.12% CAGR through 2031 thanks to photoinitiator-free metal-coil and battery-electrode applications. This growth is driven by their applications in photoinitiator-free metal-coil and battery-electrode sectors. AkzoNobel's collaboration with Wuxi El Pont on a 2026 coil-coating pilot is noteworthy. They are utilizing 100%-solids EB chemistries at speeds exceeding commercial thresholds, validating the commercial viability and justifying the capital premium. By 2024, LED-UV modules reached significant irradiance levels. They secured over half of the new UV installations, successfully displacing mercury units. This transition bolsters the global movement to phase out mercury, aligning with the Minamata Convention.

While hybrid dual-cure systems cater to niche applications, they play a crucial role in areas like headlamp housings and thick black pigmented layers, where UV penetration is limited. Microwave and infrared technologies, though occupying a smaller segment, find their primary use in release coatings. These advancements underscore the market's momentum in radiation-curable coatings, driven by the dual imperatives of sustainability and speed.

By Resin Chemistry: Urethane Acrylate Gains on Epoxy Stronghold

Epoxy acrylate commanded 30.50% of 2025 revenue, thanks to its superior adhesion and chemical resistance, making it ideal for beverage-can interiors and electronics assemblies. Yet, its inherent brittleness gives way to urethane acrylate, projected to grow at a 6.35% through 2031. Flooring producers in China are turning to urethane systems, achieving Taber abrasion losses below 100 mg per 1,000 cycles—a feat unachievable with epoxies unless softened by plasticizers, which compromise hardness.

Covestro is set to debut bio-attributed polyols in 2025, boasting renewable carbon content. This move not only underscores Covestro's commitment to sustainability but also helps furniture manufacturers earn coveted sustainability points. While polyester acrylate dominates graphic-arts coatings due to its cost-effectiveness and gloss retention, silicone-acrylate hybrids carve out a niche in the release-liner and optical-fiber sectors. As a result, urethane systems are on track to match epoxies in market share within the radiation-curable coatings segment by the end of the forecast period.

By End-User Industry: 3D Printing Emerges as the Fastest-Growing Vertical

Printing and packaging inks led the 2025 demand at 39.90%. This surge was largely driven by flexible-packaging converters transitioning to UV-LED inkjet platforms for their variable-data runs. Meanwhile, wood and furniture applications saw Asia-Pacific factories adopting UV lines to meet formaldehyde and VOC regulations.

Electronics coatings catered to ADAS modules and 5G boards, both of which necessitate sub-25-µm UV acrylic films. The automotive sector contributed to sales, with OEMs favoring LED curing over traditional thermal ovens for interior trims. Although 3D printing held a modest share in 2025, it is projected to grow at a 6.25% CAGR through 2031, driven by the adoption of SLA and DLP photopolymers in dental labs and automotive jigs. This trend underscores the significant growth potential of radiation-curable coatings in additive manufacturing, especially when juxtaposed with the more mature packaging volumes.

Geography Analysis

Asia-Pacific held 41.26% of global 2025 revenue and is set for a 6.10% CAGR through 2031. China's dominance is evident, with substantial wood-furniture production and laminate flooring output in 2024, both heavily reliant on UV lines to meet VOC and formaldehyde standards. In India, urban housing starts are propelling the furniture sector, especially in retrofit-heavy states like Gujarat and Maharashtra. Meanwhile, Vietnam solidifies its regional standing with notable furniture exports and an expanding coil-coating capacity.

North America, contributing a considerable portion of the 2025 market value, anticipates steady growth. Tesla's adoption of LED-UV for interior trims underscores the pull from OEMs. Concurrently, U.S. flexible-packaging converters are racing to meet the demands of e-commerce brands, utilizing UV-inkjet presses for same-day shipping. Canada is capitalizing on UV lines for engineered wood cabinetry destined for the U.S. market, while Mexico's Tier-1 suppliers are aligning their strategies with the decarbonization roadmaps of the Detroit Three through UV technology adoption.

Europe commands a significant share of the radiation-curable coatings market. In Germany, stringent REACH and VOC Solvents Directive regulations are driving heightened UV investments, especially within the automotive and furniture sectors. Post-Brexit, the U.K. is pushing for packaging self-sufficiency, bolstered by UV-LED digital capabilities. France and Italy are merging artisanal designs with solvent-free chemistries, ensuring compliance with urban air-quality standards. Together, South America and the Middle-East-Africa region contribute additional momentum, buoyed by Brazil's furniture exports and a construction surge in Saudi Arabia.

Regulatory Landscape

Regulation is tightening around both VOC emissions and specific additives used in radiation-curable systems, which is accelerating substitution toward 100% solids UV and electron-beam (EB) chemistries. In China, GB 30981 VOC limits take effect starting June 2026 for coatings, reinforcing the shift away from solvent-borne systems in industrial wood and metal applications. In the United States, VOC compliance remains a major pull for energy-curable alternatives: the US EPA moved the compliance deadline for National VOC Emission Standards for Aerosol Coatings to 17 January 2027 (via its 2025 interim final action), while South Coast AQMD provided Q1 2026 guidance for thin-film energy-curable materials that allows use of ASTM D7767-11 for VOC determination where test methods are unclear.

In Europe, chemicals restrictions are a key driver of photoinitiator and additive reformulation. Commission Delegated Regulation (EU) 2025/843 (under the EU POPs framework) restricts UV-328 with a 100 mg/kg limit from 4 August 2025 and progressively lower limits through 2027 and 2029, with time-limited exemptions for certain automotive and heavy-duty coatings until 4 August 2030. Alongside this, ECHA activity on authorisation (Annex XIV) continues to increase the compliance burden for specific UV absorbers and related substances, and REACH Annex XVII solvent restrictions with a December 2026 compliance timeline further favor low-VOC, solvent-free curing routes.

Value Chain Analysis

The value chain begins with upstream petrochemical and specialty-chemical feedstocks, which are converted into oligomers and monomers (epoxy acrylates, urethane acrylates, polyester acrylates) and specialty additives (wetting, slip, dispersing agents) alongside photoinitiators. These inputs are then formulated into coatings, inks, and adhesives for packaging, wood, electronics, automotive, and industrial uses. Formulators and large integrated producers (for example, BASF and Allnex) balance performance targets (cure speed, migration control, abrasion resistance) against evolving restrictions on specific photoinitiators and UV absorbers, while OEMs and converters qualify systems on production lines using UV lamp, UV-LED, or EB curing equipment. Industry bodies such as RadTech support adoption by coordinating technical guidance, user resources, and engagement on chemical registration and VOC policy.

Downstream, performance depends strongly on curing hardware and application engineering, which makes equipment suppliers and integrators important for commercialization (lamp-to-LED retrofits, web-handling upgrades, and EB shielding and controls). Supply risk is most concentrated in specialty photoinitiators and high-purity monomers, where compliance-driven reformulation and REACH-driven classification changes can tighten availability. As a result, buyers increasingly favor multi-sourcing, higher-molecular-weight or polymeric initiators, and EB pathways that remove photoinitiators altogether. On costs, outages and feedstock volatility (for example, acrylic-acid-linked disruptions referenced in 2025) flow through to monomer pricing, and capacity additions by Asian suppliers can pressure global pricing and raise competitive intensity across standardized UV-curing material grades.

Competitive Landscape

The radiation-curable coatings market is moderately consolidated. IGM Resins and Lambson specialize in photoinitiators, advising converters on LED wavelength matching amid REACH disruptions. EB equipment suppliers promote modular units, opening photoinitiator-free curing to mid-size converters. Start-ups harness machine-learning algorithms to optimize cure kinetics, pointing to future service-based revenue models.

Radiation Curable Coatings Industry Leaders

Allnex Netherlands B.V.

BASF

Covestro AG

PPG Industries, Inc.

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reformulation and qualification programs around restricted additives and low-migration requirements are creating near-term whitespace in photoinitiator-reduced or photoinitiator-free systems, as well as in application-specific packages tuned for UV-LED wavelengths and fast web speeds. This direction is supported by iGM Resins launching Photomer SC91 in June 2026, a self-curable acrylate resin chemistry with built-in photoactivity that reduces reliance on external photoinitiators. EuPIA updates to photoinitiator suitability guidance (2025) also support a shift toward safer, immobilized options for food-contact compliant packaging ink and coating designs.

EB curing benefits in parallel in metal-coil and battery-related lines where removing photoinitiators helps address both regulatory and performance constraints. Investment is also focusing on regional testing and scale-up infrastructure to shorten qualification cycles across UV (LED, excimer, arc), IR, and EB, which improves the ability to transfer lab formulations into customer production conditions. In April 2026, PPG announced an advanced radiation-curable coatings testing line at its Marly, France R&D Center of Excellence, and in June 2026 Evonik upgraded radiation-curable coating testing capability at its Shanghai Innovation Park, aligning with demand from high-throughput packaging, furniture, and industrial lines that require reproducible curing windows. BASF presenting Efka PX 4720 in May 2026 for ultra-matte UV formulations provides additional room for solvent-free, ultra-matte aesthetics and durability in premium furniture finishes and brand-driven packaging.

Recent Industry Developments

- July 2026: BASF introduced a new performance dispersing agent targeted at solvent-free radiation-curing coating applications. The launch expands BASF Performance and Formulation Additives options for formulators working on high-solids UV systems where dispersion quality and viscosity control directly affect throughput and finish consistency.

- May 2026: BASF debuted Efka PX 4720 at the American Coatings Show 2026 as a dispersing agent designed for ultra-matte UV coating formulations. This adds a formulation lever for converters pursuing low-gloss aesthetics in solvent-free systems while maintaining processing stability on UV and UV-LED lines.

- April 2025: Evonik Industries AG launched TEGO Wet 288, a wetting additive positioned for waterborne and radiation-curable inks to improve substrate wetting while preserving reprintability and glueability. The product supports converters running high-speed packaging and label applications where ink laydown quality and downstream converting compatibility are critical.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from radiation curable coatings used to form and cure a protective or functional layer through UV or electron beam energy, across major industrial and specialty end uses.

Scope exclusions: We exclude curing equipment, UV lamps/LED units, and service revenues for installation or maintenance.

Segmentation Overview

- By Raw Material

- Oligomers

- Monomers

- Photoinitiators

- Additives

- By Curing Technology

- UV Lamp

- Electron Beam

- Hybrid/Dual-Cure

- Microwave/Infra-red

- By Resin Chemistry

- Epoxy Acrylate

- Urethane Acrylate

- Polyester Acrylate

- Acrylic Ester

- Others (Silicone, Vinyl Ether)

- By End-User Industry

- Wood and Furniture

- Packaging and Printing Inks

- Electronics and Semiconductor

- Automotive and Transportation

- Medical Devices

- 3D Printing / Additive Manufacturing

- Others (Optical, Construction)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context around where radiation curing is actually used, and how fast it is being adopted in production lines. We reviewed public sources such as US EPA materials on VOC control, Eurostat and UN Comtrade trade series for relevant chemicals and coating inputs, and industry safety and handling documentation that clarifies typical formulations and use conditions.

To keep the model grounded, we also pulled patterns from sources such as the US International Trade Commission, patent databases for UV and EB chemistry activity, and peer reviewed journals that discuss cure performance, photoinitiator loading, and substrate compatibility. Company annual reports, investor presentations, and credible press coverage helped us cross-check capacity additions, product launches, and regional demand commentary. In a few cases we used paid subscriptions for company financials and intelligence, shipment-level trade checks, and patent lookups to reduce guesswork. The sources listed here are illustrative, and many other public and paid references were also used to collect, validate, and clarify the data.

Primary Interviews and Surveys

Primary work was used to pressure-test adoption rates, pricing direction, and mix shifts between UV, UV-LED, and EB systems across the big consuming industries. We spoke with a balanced set of participants from the supply side and the demand side, and then validated the same assumptions across APAC, EMEA, and the Americas so regional skews did not get over-modeled.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 21% | APAC: 44% |

| Mid tier: 50% | Functional/Unit leaders: 22% | EMEA: 29% |

| Smaller Players: 21% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

The core sizing uses a top-down build that starts from coated substrate demand pools and then applies penetration rates for radiation curing across wood finishes, packaging and print-related uses, electronics, and other relevant end uses. To keep the totals grounded, the output was corroborated with selective bottom-up checks, such as sampled supplier revenue splits, channel feedback on application volumes, and simple ASP times volume sanity checks for a few high-visibility use cases.

Key inputs that moved the numbers included: regional manufacturing output trends for packaging and durable goods, adoption of UV-LED lines versus conventional UV, photoinitiator and oligomer usage intensity by formulation family, typical coating weight per square meter for common substrates, and observed price movement tied to raw material availability. Where bottom-up signals were incomplete (for example, privately held supplier exposure), we filled gaps using peer sets and then re-tested the implied shares in interviews.

For forecasting, we leaned on scenario analysis supported by short time-series smoothing on stable indicators, and then adjusted the outlook with expert views on regulatory pressure for low-VOC coatings, equipment conversion cycles, and end-market growth. The forecast was kept repeatable by keeping the variables explicit and by documenting every major assumption that changes the curve.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including trade flows for key inputs, public capacity announcements, and the implied coating consumption per end-use, so outliers could be spotted early. When large variances showed up by region or technology, we re-opened assumptions, checked currency timing, and re-contacted relevant interviewees to confirm what changed in the market.

Before sign-off, the work goes through step-by-step analyst reviews that focus on unit consistency, mix logic, and year-over-year reasonableness. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory moves or large capacity changes. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Radiation Curable Coatings Market Size Compared With Other Published Estimates

Published market values for radiation curable coatings can look far apart because the underlying scope is not always the same, and the assumptions behind pricing and adoption are often not shared. Differences usually come from what is counted as a coating versus adjacent ink and printing chemistry, how UV-LED conversion is treated, and how currency timing is handled for global rollups.

Some public estimates fold in a wider printing value chain and count broader ink and substrate coating uses together, which can lift the reported number. In the Mordor Intelligence framework, the total is limited to radiation curable coatings revenues and is then checked using penetration and application-level demand signals so adjacent materials are not double counted.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.60 B (2025) | |

| Industry Publisher A | USD 8.80 B (2025) | Uses a broader application definition that includes printing inks and several substrate coating uses together, which can pull adjacent radiation-curable material revenues into the same total. |

| Global Publisher B | USD 8.90 B (2025) | Applies higher assumed adoption and pricing progression across multiple functions and end uses, with fewer visible cross-checks against end-market demand pools and regional conversion cycles. |

The spread in the table is mainly explained by scope expansion into ink-heavy applications and by different adoption and price assumptions that are harder to reproduce. By keeping the inputs tied to penetration, end-use demand, and repeatable checks, the estimate stays traceable and easier to update as real market signals change.

Key Questions Answered in the Report

How large will the radiation-curable coatings market be by 2031?

It is forecast to reach USD 10.36 billion by 2031, reflecting a 5.34% CAGR from USD 7.99 billion in 2026.

Which raw material category is growing the fastest?

Photoinitiators post a 6.89% CAGR to 2031 as converters reformulate around LED-optimized and low-migration chemistries.

Which region leads demand?

Asia-Pacific accounts for 41.26% of 2025 revenue and grows the quickest at 6.10% CAGR, thanks to Chinese, Indian, and Vietnamese furniture expansions.

What is the main regulatory tailwind?

VOC and solvent restrictions in China, the EU, and select U.S. states compel a shift from solvent-borne to radiation-curable systems.

How does electron-beam technology differ from UV?

EB curing forgoes photoinitiators, achieves higher throughput, and excels on metal-coil and battery-electrode lines, albeit with higher capital cost.

Page last updated on: