Unsaturated Polyester Resin (UPR) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

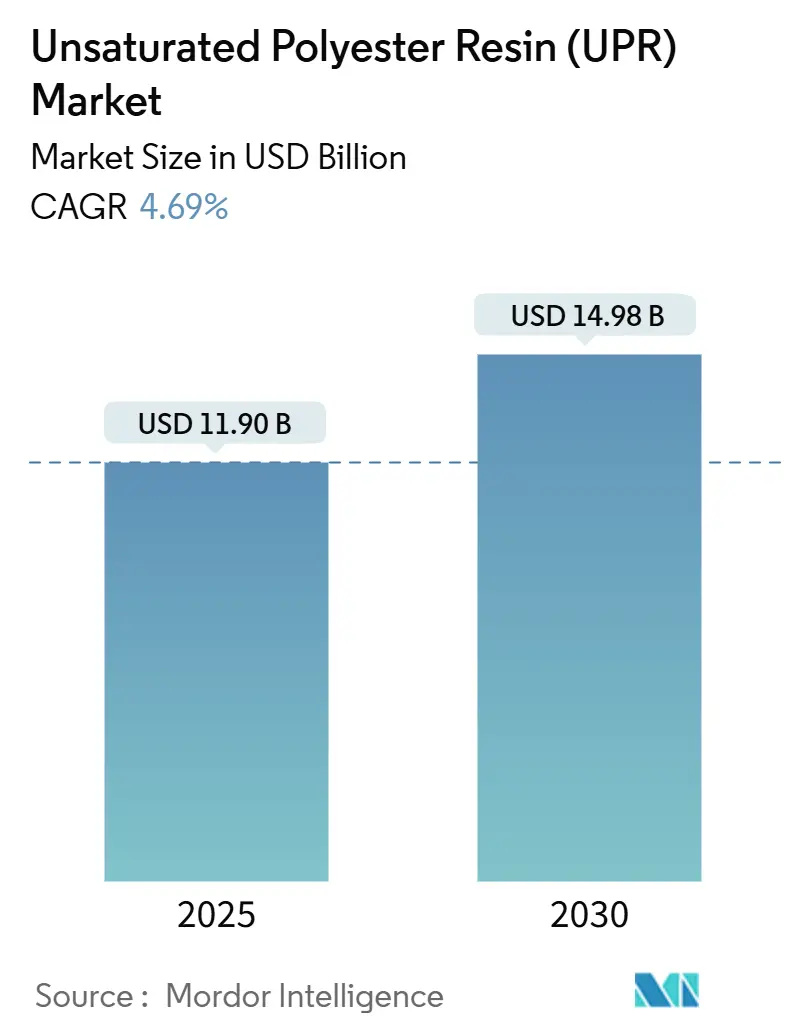

| Market Size (2025) | USD 11.90 Billion |

| Market Size (2030) | USD 14.98 Billion |

| Growth Rate (2025 - 2030) | 4.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Unsaturated Polyester Resin (UPR) Market Analysis by Mordor Intelligence

The Unsaturated Polyester Resin Market size is estimated at USD 11.90 billion in 2025, and is expected to reach USD 14.98 billion by 2030, at a CAGR of 4.69% during the forecast period (2025-2030). Demand keeps rising as manufacturers in construction, wind energy, automotive, and electronics turn to these resins for their strength-to-weight advantages, chemical resistance, and competitive pricing. Producers are widening their portfolios to serve both commodity volumes and specialized high-performance niches. Asia-Pacific anchors global consumption thanks to large-scale infrastructure programs, while ongoing product innovation, especially low-styrene, bio-based, and recyclable grades, supports growth in developed regions. Despite raw-material price swings and tighter environmental rules, the unsaturated polyester resin market continues to attract capacity expansions and strategic investments.

Key Report Takeaways

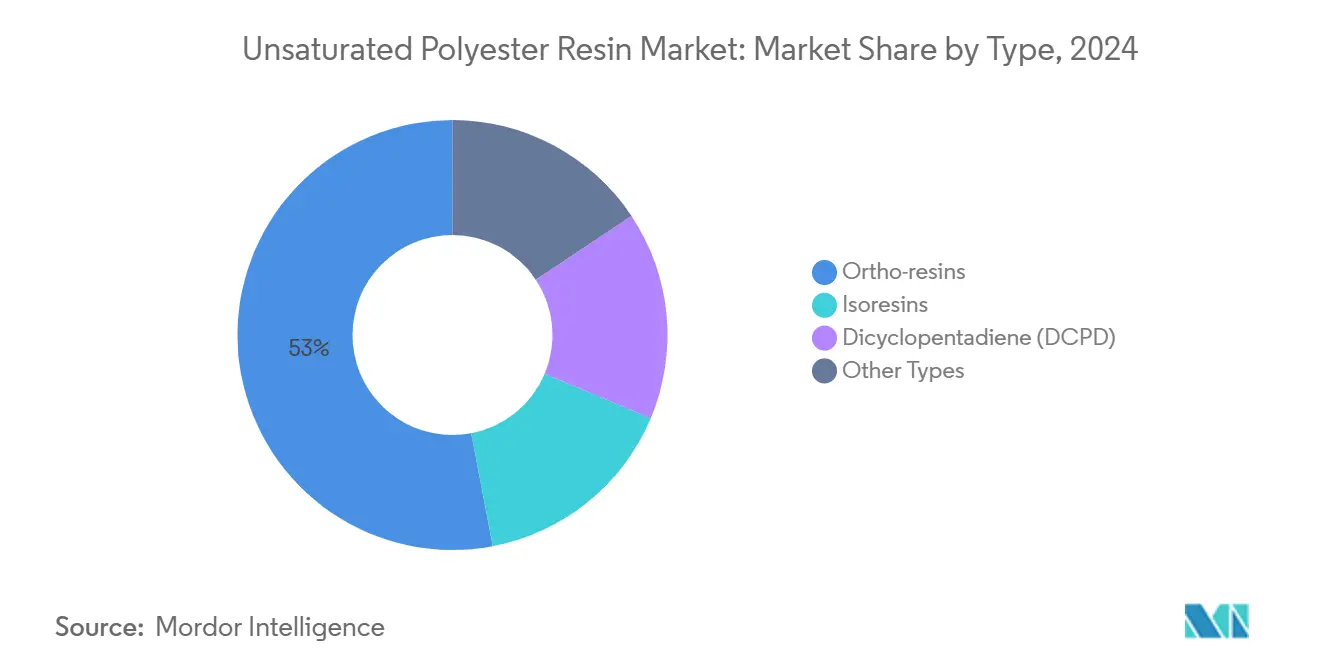

- By product type, ortho-resins held 53% of the unsaturated polyester resin market size in 2024, while isoresins are set to grow at a 6.51% CAGR through 2030.

- By raw material, maleic anhydride accounted for 51% of the unsaturated polyester resin market size in 2024; propylene glycol is poised for the quickest 5.61% CAGR.

- By form, liquid grades captured 85% of the unsaturated polyester resin market share in 2024, whereas powder formulations are forecast to expand at 6.12% CAGR.

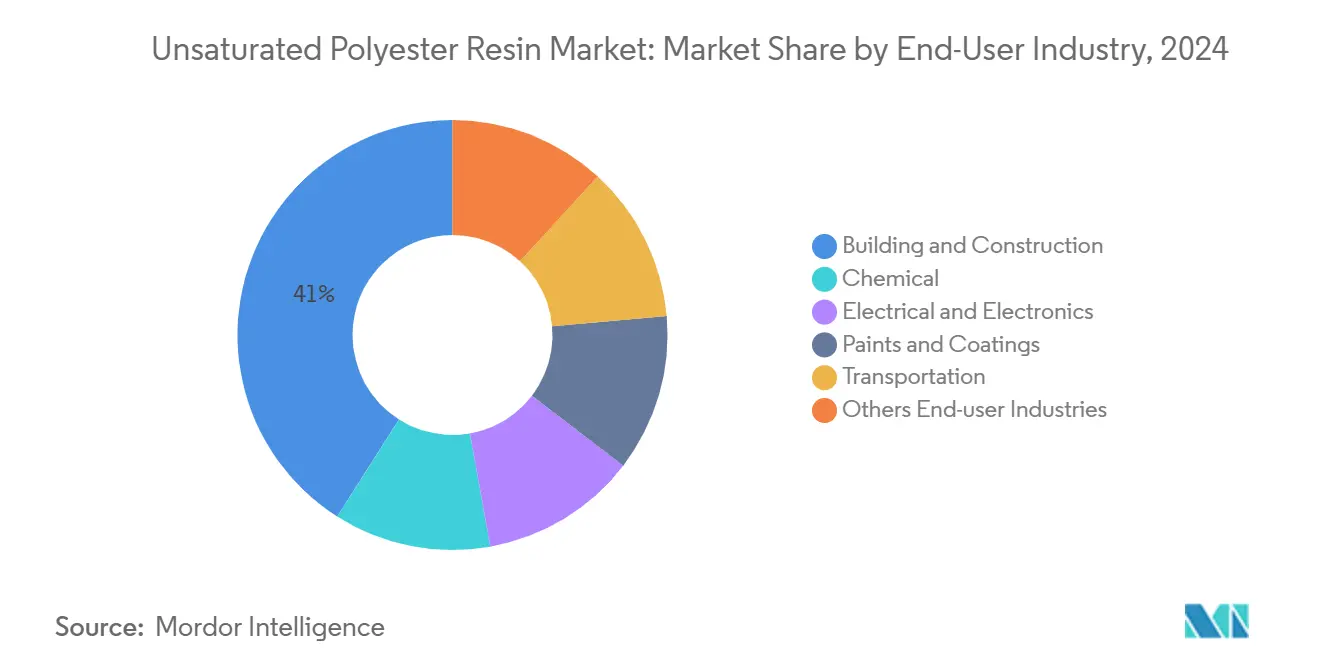

- By end-use, building & construction commanded 41% share of the unsaturated polyester resin market size in 2024, while electrical & electronics advances at a 6.13% CAGR to 2030.

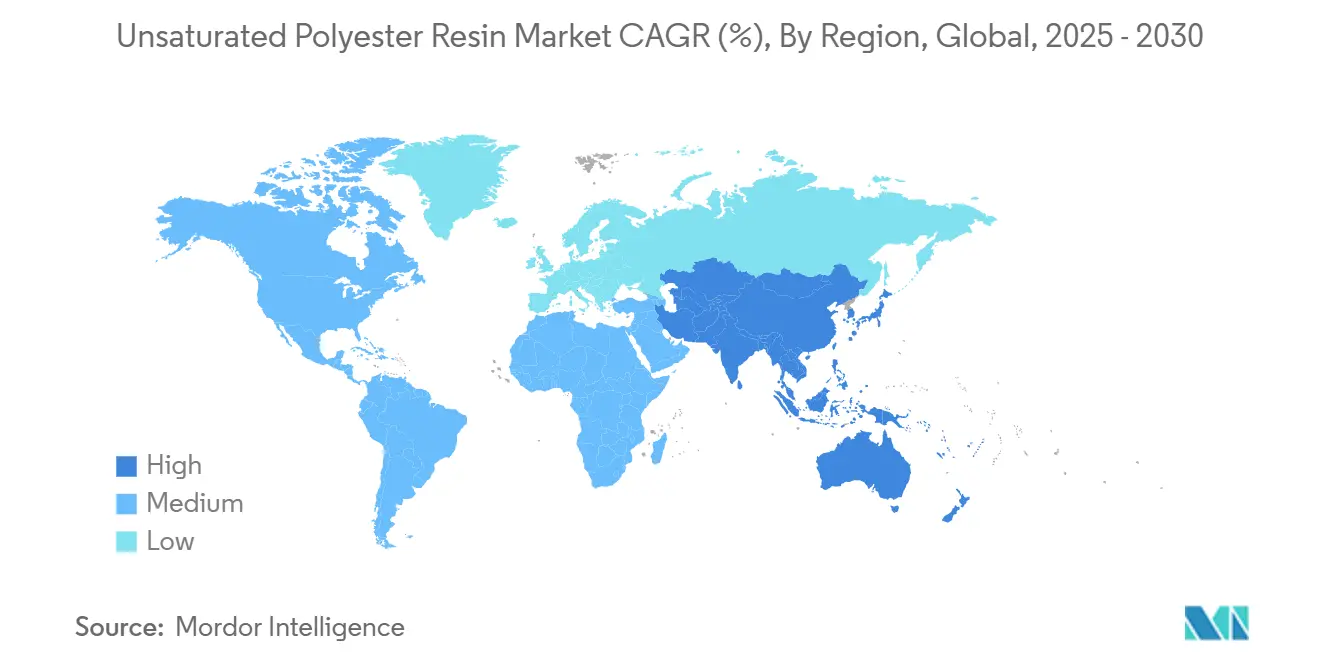

- By region, Asia-Pacific led with 43% of the unsaturated polyester resin market share in 2024; North Asia is projected to post the fastest 5.66% CAGR to 2030.

Global Unsaturated Polyester Resin (UPR) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of UPR in Wind-Turbine Blade Manufacturing | +1.2% | Europe, North America, China | Medium term (2-4 years) |

| Growth in Automotive and Transportation Sectors | +0.9% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Shift toward Lightweight Composite Materials in Global Rail Transportation Fleets | +0.7% | Europe, Asia Pacific (Japan, China, India) | Medium term (2-4 years) |

| Expansion in Construction and Infrastructure | +1.1% | Asia-Pacific, Middle East, North America | Short term (≤ 2 years) |

| Preference for Low-Styrene-Emission Resins under EU REACH Pressure | +0.5% | Europe with global spill-over | Long term (≥ 4 years) |

Source: Mordor Intelligence

Surging adoption of UPR in wind-turbine blade manufacturing

Record onshore and offshore wind installations kept blade demand high in 2024, and designers now favor longer blades built from glass-fiber UPR laminates. A 15% jump in average turbine capacity combined with a 7% cut in blade weight has boosted energy capture and lowered levelized costs. Policy targets such as the EU’s 42.5% renewable share by 2030 and China’s 1,200 GW wind-plus-solar aim for rapid scale-up. These ambitions sustain resin orders for blade shells, shear webs, and root sections. Manufacturers are, however, examining end-of-life recycling for the estimated 200,000 tons of composite blade waste expected each year by 2033[1]Source: Y. Chen et al., “Recycling of Wind Turbine Blades,” sciencedirect.com .

Expansion in construction and infrastructure

Megaproject pipelines in Asia, the Middle East, and North America keep the consumption of corrosion-resistant pipes, panels, and tanks robust. China’s 14th Five-Year Plan earmarks USD 2.3 trillion for infrastructure, while UPR’s fire-retardant and weather-resistant grades win specifications for bridges and coastal defenses. Renovation work in mature economies favors lightweight decorative panels that cut installation time. New low-VOC formulations also allow contractors to meet stricter indoor-air standards.

Growth of automotive and transportation sectors

Automakers substitute metal with fiber-reinforced UPR to shave 10-60% component weight, improving fuel economy by 6-8% per 10% mass saved[2]Source: M. Shiferaw & A. Tegegne, “Lightweight Automotive Body Parts,” researchgate.net . Electric-vehicle builders balance battery weight using composite exterior panels, under-body shields, and structural inserts. Recent alliances, such as BASF with NIO, accelerate tailored resin chemistries for fast-cycle molding. Rail-car makers also integrate UPR interiors and skins to cut traction energy and meet fire-safety codes.

Preference for low-styrene-emission resins under EU REACH pressure

Open-mold processing can release 28-70 ppm styrene, whereas closed-mold shifts cut levels to near 0.30 ppm, an improvement of 98%. European rules propel closed vac-infusion, pultrusion, and specialty diluents. Producers market premium resins that match mechanical targets while easing workplace exposure. Adoption now spreads to North America and Asia as multinationals harmonize health-and-safety standards.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Maleic Anhydride Feedstock Prices Linked to Crude-Oil Fluctuations | -0.8% | Global, higher in import-dependent regions | Medium term (2-4 years) |

| Environmental and Regulatory Challenges | -0.6% | Europe, North America with global expansion | Long term (≥ 4 years) |

| Competition from Alternative Materials | -0.5% | Global, with concentration in high-performance applications | Medium term (2-4 years) |

Source: Mordor Intelligence

Volatility in maleic anhydride feedstock prices linked to crude-oil fluctuations

Maleic anhydride forms roughly half the raw-material cost for standard UPR, so its price spikes erode margins quickly. Geopolitical events that move crude prices are transmitted to benzene and n-butane chains, tightening supply. Producers hedge and sign longer-term offtake contracts, yet the cost pass-through to converters faces resistance during demand lulls. Integrated resin makers that own upstream capacity sustain steadier economics.

Environmental and regulatory challenges

EU landfill bans on composite waste from 2025 oblige recyclers to scale chemical and mechanical recovery. Microplastic restrictions and extended-producer-responsibility fees raise compliance costs for electronics and paint users. North America considers similar rules. While these measures temper short-term demand, they also spur R&D into recyclable thermosets and bio-based resins with reduced carbon footprints.

Segment Analysis

By Type: Isoresins Accelerate Performance Adoption

Ortho-resins retained 53% of the unsaturated polyester resin market size in 2024 because of their balanced price and versatility in pipes, panels, and general laminates. Commodity users value reliable cure profiles and abundant supply. Isoresins, though costlier, register a 6.51% CAGR as formulators prioritize higher tensile strength, heat distortion, and chemical resistance for marine structures, scrubbers, and automotive under-hood parts. Evolving specifications in wind-blade shear webs and battery casings highlight this migration toward higher-performance chemistries.

Rising demand for recyclable solutions has prompted research into glycerol- and FDCA-derived bio-isoresins that reach 173 °C glass-transition temperature while cutting fossil content[3]Source: S. Akbari et al., “Bio-Based Branched Unsaturated Polyester Resins,” doi.org. Developers now pilot plant-scale production to validate processing parity with petroleum grades. DCPD resins, though small in volume, gain attention for low shrinkage and reduced styrene output, making them suitable for aesthetic panels and electrical housings. Specialty chlorendic and bisphenol-fumarate grades continue to satisfy flame-retardant or high-temperature niches in defense and industrial equipment.

Note: Segment Share of all individual segments available upon report purchase

By Raw Material: Propylene Glycol Broadens Sustainable Options

Maleic anhydride captured 51% share of the unsaturated polyester resin market size in 2024 as the key acid component used across ortho and iso chemistries. Procurement teams monitor any disruption in maleic supply because substitution flexibility remains limited. Propylene glycol, however, is the fastest-growing raw material at 5.61% CAGR as bio-routes from glycerin or sorbitol improve cost and carbon profiles. Producers leverage glycol variation to fine-tune viscosity, reactivity, and end-use durability, particularly in powder SMC.

Phthalic anhydride remains essential for classic ortho recipes, while styrene acts as the reactive diluent needed for cross-linking during cure. Formulators also add triethyl phosphate or diphenyl cresyl phosphate to raise limiting-oxygen indices without sacrificing mechanical balance. Growing additive complexity underlines the shift from bulk commodity toward engineered formulations that answer customer-specific performance targets.

By Form: Powder Resins Carve Value in Precision Molding

Liquid grades dominated 85% of the unsaturated polyester resin market share in 2024 since they wet fibers readily, adapt to infusion, and suit large surface parts. Continuous process investments in high-pressure RTM and filament winding reinforce this preference. Powder resins, expanding at 6.12% CAGR, bring longer shelf life, low VOC, and safer handling for compact factories. The segment’s momentum stems from sheet and bulk molding compounds used in headlamp housings, appliance parts, and small motor casings.

New powder chemistries demonstrate improved flow, uniform filler dispersion, and compatibility with glass mats, enabling cycle times comparable to liquids. Equipment suppliers now market turnkey lines that bag, convey, and meter powder automatically, lowering plant solvent emissions and satisfying ISO 14001 audits.

By End-use Industry: Electronics Outpaces Traditional Demand

Building & construction accounted for 41% of the unsaturated polyester resin market size in 2024 on the strength of tanks, roofing sheets, and decorative columns that withstand moisture and corrosive atmospheres. Infrastructure booms in South and Southeast Asia alongside retrofits in North America sustain baseline volume. Electrical & electronics, by contrast, is the fastest-moving segment at 6.13% CAGR. Manufacturers rely on UPR encapsulants, insulating varnishes, and PCB substrates for thermal stability, dielectric integrity, and weight savings.

Researchers recently created low-VOC UPR coatings that raise the comparative tracking index and long-term heat aging, opening prospects in high-power converters. Transportation applications keep leveraging 10-60% weight cuts for EV battery enclosures and rail interiors, while chemical-process industries specify vinyl ester-modified UPR blends for scrubbers and pipes where moderate corrosion resistance suffices over epoxy price premiums.

Note: Segment Share of all individual segments available upon report purchase

Geography Analysis

Unsaturated Polyester Resin Market in Asia-Pacific

Asia-Pacific remained the epicenter of the unsaturated polyester resin market in 2024, contributing 43% of global volume and advancing at a 5.66% CAGR through 2030. China dominates output with integrated maleic anhydride and downstream composite plants serving wind, construction, and electronics clusters. India records double-digit demand growth under “Make in India” initiatives that add domestic blade and SMC facilities. Japan and South Korea focus on premium electrical and automotive sectors, adopting low-styrene and high-strength recipes to meet advanced quality norms.

North America sustains high-value applications across aerospace interiors, specialty pipes, and infrastructure renewal. Government incentives for reshored manufacturing encourage new composite lines, while strict VOC rules push adopters toward closed-molding and powder forms. Ongoing blade-repowering projects in the United States also underpin stable resin offtake.

Europe enforces the toughest environmental standards, accelerating the shift toward low-styrene and bio-based grades. The region’s rail, marine, and wind industries demand reliable high-performance systems, justifying price premiums. Simultaneously, composite-waste landfill bans hike interest in chemical recycling platforms, with pilot trials in Germany and Denmark scheduled before 2027. Growth pockets in the Middle East, Africa, and South America rely on construction sprees, desalination projects, and emerging auto supply bases. Though their combined tonnage is small, improving local fabrication capabilities create long-term volume upside for the unsaturated polyester resin market.

Competitive Landscape

Top Companies in Unsaturated Polyester Resin Market

The global unsaturated polyester resin market is characterized by a combination of vertically integrated multinationals and dynamic regional players. Major companies leverage control over raw material supply chains, including styrene and maleic anhydride, to maintain cost advantages, while smaller firms focus on niche chemistries, local customization, and timely deliveries to stay competitive. Sustainability has become a key driver of competition, with leading producers investing in bio-based feedstocks, low-VOC formulations, and recycling technologies to recover monomers from cured composites. Molders increasingly prefer suppliers offering technical support for faster cure cycles and process automation, giving integrated resin and catalyst solutions a competitive edge.

Consolidation continues to shape the market. KPS Capital Partners completed its acquisition of INEOS Composites in March 2025, expanding its global resin production network. Similarly, Nippon Paint Holdings announced a USD 4.35 billion acquisition of AOC in October 2024, enhancing its presence in construction and marine applications. Meanwhile, emerging disruptors are advancing solvent-free resin technologies and recyclers capable of recovering styrene and glycols from composite waste.

Unsaturated Polyester Resin (UPR) Industry Leaders

-

Polynt S.p.A.

-

AOC

-

INEOS

-

ZheJiang TianHe Resin Co.,Ltd.

-

Scott Bader Company Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: KPS Capital Partners, LP has acquired the composites business from INEOS Enterprises. INEOS Composites is recognized as one of the leading global manufacturers of unsaturated polyester resins. This acquisition is anticipated to strengthen the market's dynamics.

- October 2024: Nippon Paint Holdings Co., Ltd. has signed a purchase agreement to acquire all equity interests in AOC, a manufacturer of unsaturated polyester resin with operations primarily in the United States and Europe. Upon completion, AOC will become a Nippon Paint Holdings Co., Ltd subsidiary.

Global Unsaturated Polyester Resin (UPR) Market Report Scope

Unsaturated polyester resins are available in many forms and offer several desirable properties, making them an ideal matrix material for several composites. Their properties include low shrinkage, corrosion resistance, low water absorption, and low volatility. The unsaturated polyester resins (UPR) market is segmented by type, end-user industry, and geography. The market is segmented by type: ortho-resins, iso-resins, dicyclopentadiene, and other types. By end-user industry, the market is segmented into building and construction, chemical, electrical and electronics, paints and coatings, transportation, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| By Type | Ortho-resins | ||

| Isoresins | |||

| Dicyclopentadiene (DCPD) | |||

| Other Types | |||

| By Raw Material | Maleic Anhydride | ||

| Phthalic Anhydride | |||

| Propylene Glycol | |||

| Styrene Monomer | |||

| Others (Additives, Initiators) | |||

| By Form | Liquid | ||

| Powder | |||

| By End-use Industry | Building and Construction | ||

| Chemical | |||

| Electrical and Electronics | |||

| Paints and Coatings | |||

| Transportation | |||

| Others End-user Industries | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Ortho-resins |

| Isoresins |

| Dicyclopentadiene (DCPD) |

| Other Types |

| Maleic Anhydride |

| Phthalic Anhydride |

| Propylene Glycol |

| Styrene Monomer |

| Others (Additives, Initiators) |

| Liquid |

| Powder |

| Building and Construction |

| Chemical |

| Electrical and Electronics |

| Paints and Coatings |

| Transportation |

| Others End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is driving the fastest growth within the unsaturated polyester resin market?

Electrical & electronics applications are expanding at a 6.13% CAGR through 2030 as manufacturers need insulating, low-VOC resins for components.

Why is Asia-Pacific the largest regional consumer of unsaturated polyester resins?

The region houses extensive construction activity, large wind-blade factories, and a broad electronics supply chain, giving it 43% of 2024 global volume.

How are environmental regulations influencing product development?

EU REACH and landfill bans push producers to launch low-styrene, bio-based, and recyclable grades that reduce emissions and support circularity.

Which raw material shows the strongest future demand growth?

Propylene glycol leads with a projected 5.61% CAGR as bio-based production routes scale and enable more sustainable formulations.

What strategies help resin makers manage maleic anhydride price volatility?

Vertical integration, hedging contracts, and dual-sourcing allow suppliers to smooth cost swings and protect margins.

Are powder resins likely to displace liquid grades in high-volume applications?

Powder formulations grow quickly where low VOC and precise dosing matter, yet liquid resins will remain dominant for large, complex composite parts.

Page last updated on: June 19, 2025