Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

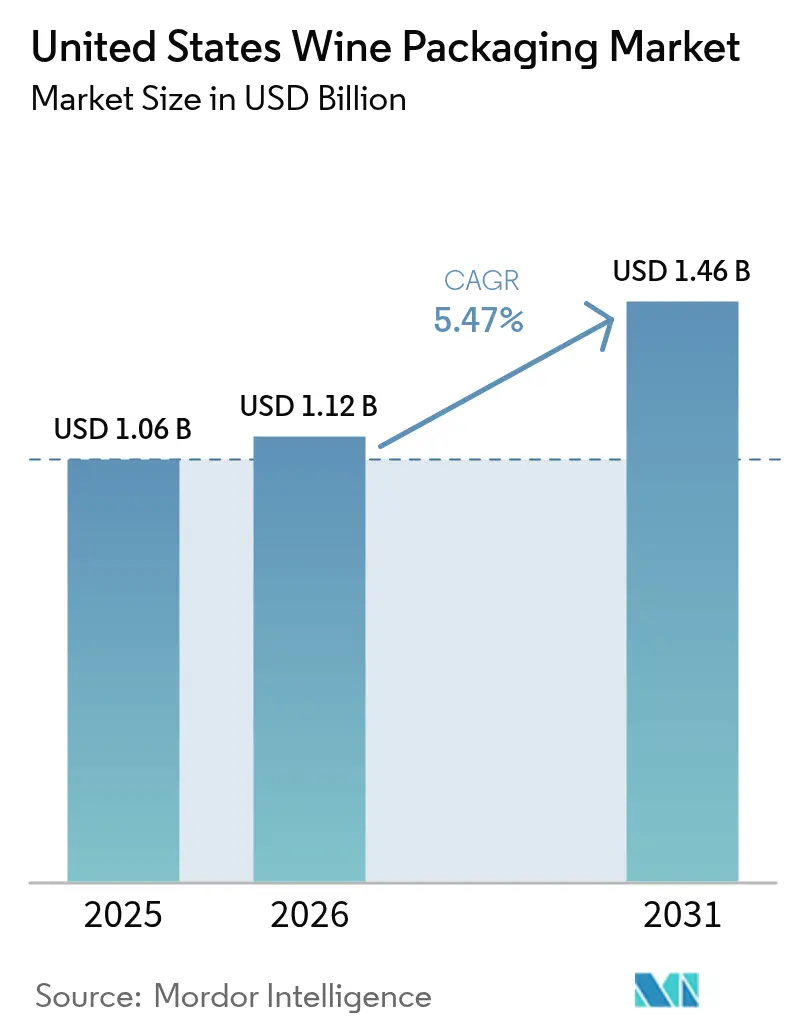

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

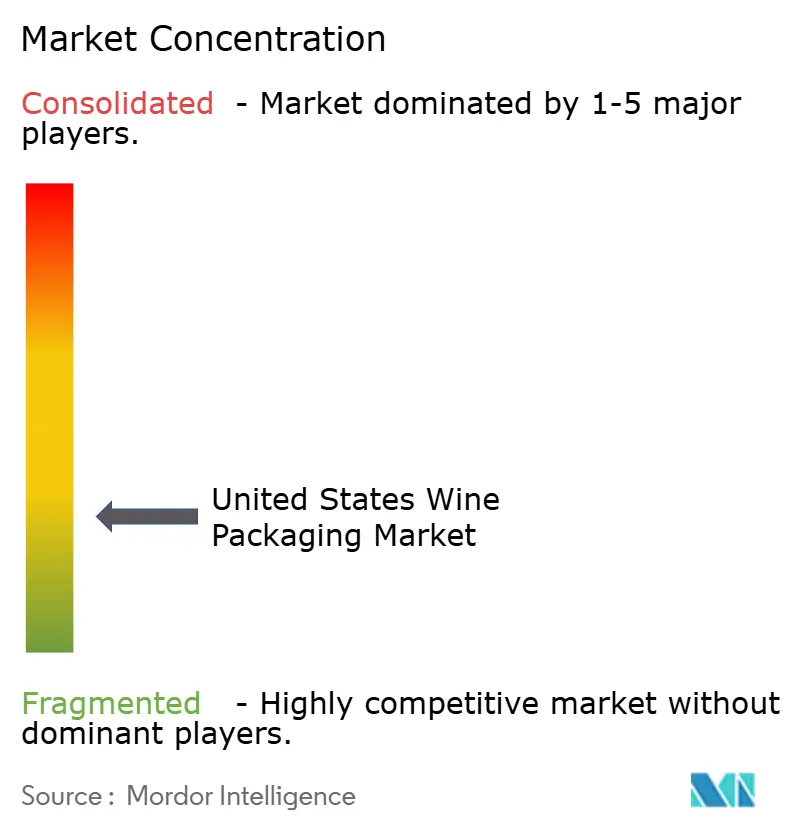

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Wine Packaging Market Analysis by Mordor Intelligence

The United States wine packaging market size was valued at USD 1.06 billion in 2025 and estimated to grow from USD 1.12 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). Regulatory expansion, stricter sustainability mandates, and omnichannel purchasing habits are reshaping material choices, forcing suppliers to balance premium cues with carbon-reduction goals. Deposit-return rules in California and Oregon, along with direct-to-consumer (DtC) shipping access in 47 states, are accelerating demand for lighter, more easily recycled containers that travel safely through parcel networks. Labor shortages in major wine regions are also nudging producers toward bulk-friendly formats that reduce manual handling requirements. Meanwhile, competitive dynamics are shifting as aluminum, paper, and refillable-glass specialists gain visibility at the expense of traditional heavy-glass suppliers that face margin pressure from volatile energy costs.

Key Report Takeaways

- By material type, glass held 66.65% of United States wine packaging market share in 2025, while metal is on track for the fastest 8.31% CAGR to 2031.

- By product type, glass bottles led with 56.12% revenue share in 2025; cans are projected to expand at a 7.74% CAGR through 2031.

- By closure type, natural cork accounted for 43.95% share in 2025 as screw caps record the top 7.98% CAGR to 2031.

- By wine type, still-wine formats commanded 67.55% of United States wine packaging market size in 2025, yet low and no-alcohol packaging is advancing at a 9.02% CAGR to 2031.

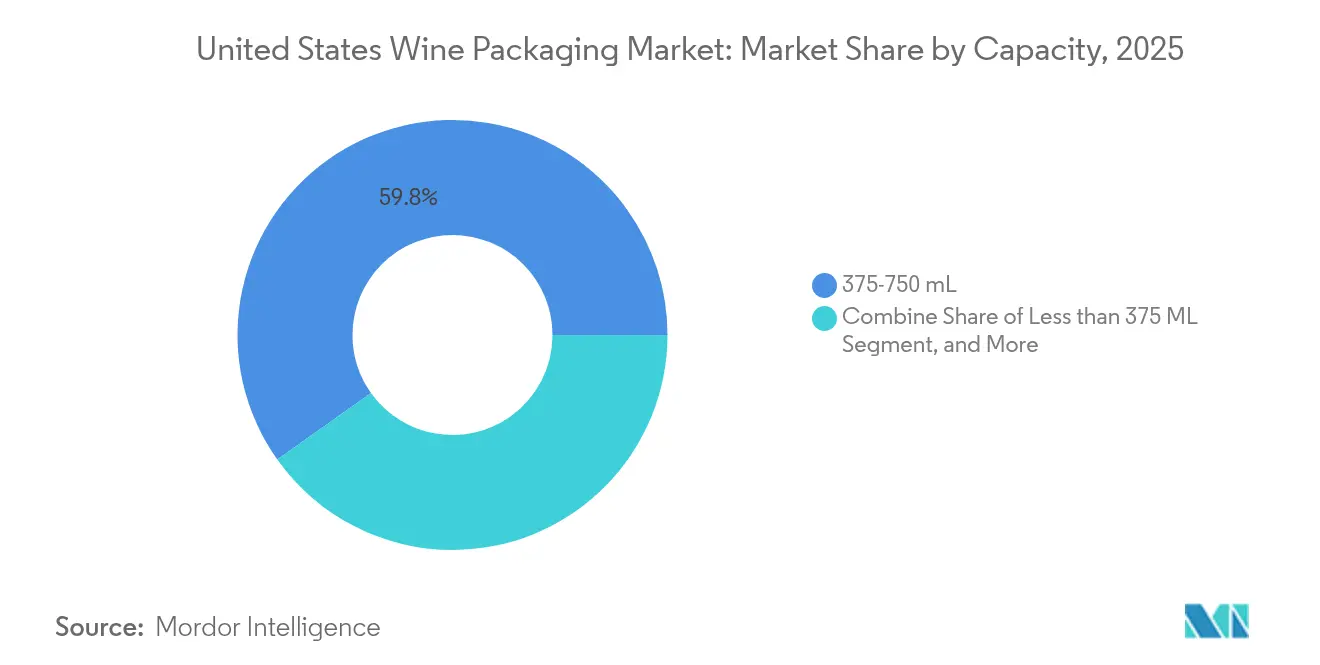

- By capacity, 375-750 mL units controlled 59.84% share in 2025; containers below 375 mL are expected to rise at a 7.41% CAGR to 2031.

- By distribution channel, direct sales represented 57.92% share in 2025, whereas indirect retail outlets are forecast to post a 6.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Wine Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight eco-glass | +1.2% | National, concentrated in California, Oregon, Washington | Medium term (2-4 years) |

| Booming canned-wine sales in off-premise channels | +1.8% | National, strongest in urban markets and venues with glass restrictions | Short term (≤ 2 years) |

| DtC shipping liberalisation across 47 states spurring e-commerce-ready packs | +0.9% | National, excluding Delaware, Mississippi, Utah with restrictions | Medium term (2-4 years) |

| Bottle-deposit laws (OR, MI) increasing recycled-content requirements | +0.7% | Oregon, Michigan, with potential expansion to other states | Long term (≥ 4 years) |

| Vineyard labour shortages shifting bulk formats toward bag-in-box | +0.6% | California Central Coast, Willamette Valley, other labor-intensive regions | Short term (≤ 2 years) |

| Private-label retailers scaling cost-efficient PET/BIB volumes | +0.5% | National, concentrated in major retail chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight Eco-Glass

Glass suppliers are cutting bottle weight to curb freight emissions and control surging input costs. O-I’s Estampe bottle dropped to 390 g while pushing recycled content to 82%, lowering its carbon impact by 25% relative to legacy 500 g designs. [1]O-I Glass, “Estampe Eco-Designed Wine Bottle Launch,” Glass International, glass-international.com Napa and Sonoma wineries saw glass-container price indexes jump 16% in 2024, reinforcing the economic case for lighter stock. Verallia’s new all-electric furnace cut process CO₂ by 60%, signaling long-term commitment to decarbonized glass supply. As freight makes up roughly 35% of delivered glass-package emissions, each 10% weight reduction can trim shipping emissions by nearly 3%, a compelling trade-off for premium wineries that must now publish Scope 3 footprints.

Booming Canned-Wine Sales in Off-Premise Channels

Aluminum’s 100% recyclability, low mass, and venue acceptance have lifted the format from novelty to mainstream. Ball shipped 48 billion aluminum beverage containers across North America in 2024, crossing the 30% penetration mark for the first time. Consumer trials show younger drinkers value portability over tradition, and venues from stadiums to beaches prefer non-breakable packages. Quality hurdles linked to hydrogen-sulfide formation are being mitigated by improved liners that vary by manufacturer. Brands such as Bogle’s Element[AL] have launched 90 g aluminum bottles that ship at one-fifth the mass of glass while retailing at premium price points.

DtC Shipping Liberalisation Across 47 States

Mississippi’s 2025 decision to allow DtC shipments leaves only three states with full bans, expanding the addressable e-commerce base and intensifying the need for parcel-resilient packs. Brands are investing in shock-absorbing cartons and gift-ready designs that elevate the unboxing moment. Frugalpac’s 83 g paper bottle, made from 94% recycled board, debuted at Target, highlighting how feather-weight formats reduce freight and damage risk. Premium houses such as Ruinart rolled out 99% paper “Second Skin” gift cases that are nine times lighter than previous boxes, improving carbon scores by 60%.

Bottle-Deposit Laws Increasing Recycled-Content Requirements

Oregon’s Senate Bill 1520 added canned wine to the state’s 10-cent redemption program in July 2025, compelling wineries to register with the Oregon Beverage Recycling Cooperative and adjust labels. [2]Oregon Liquor and Cannabis Commission, “Wine in a Can – Bottle Bill Expansion,” oregon.gov California’s CRV expansion similarly applies fees up to 25 cents for boxed formats, aiming to lift recycling from under 30% toward 75%. For glass makers, every additional 10% of cullet can save 2-3% energy and trim CO₂ by as much as 10%, a decisive edge in the face of volatile utility costs. [3]International Journal of Applied Glass Science, “Reducing the Environmental Footprint of Glass Manufacturing,” doi.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas costs inflating domestic glass production | -1.4% | National, concentrated in glass manufacturing regions | Short term (≤ 2 years) |

| Community resistance to new glass plants on emissions grounds | -0.6% | Regional, particularly in environmentally sensitive areas | Medium term (2-4 years) |

| Premium-segment scepticism toward PET quality perception | -0.8% | National, strongest in premium wine regions like Napa, Sonoma | Long term (≥ 4 years) |

| Plateauing food-grade RPET supply bottlenecks | -0.5% | National, with supply chain concentration in recycling hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Costs Inflating Domestic Glass Production

Energy expenses account for roughly 20% of glass plant overhead, and spikes in natural-gas prices have prompted closures such as Ardagh’s Houston facility, which idled 220 workers in 2024. O-I disclosed a 4.5% drop in 2024 sales volume as buyers shifted toward cheaper or lighter alternatives. While companies are retrofitting furnaces with oxy-fuel or electric systems, capital requirements slow fleet turnover, keeping price volatility in play for the near term.

Premium-Segment Scepticism Toward PET Quality Perception

Barrier advances have improved PET wine-bottle oxygen performance, yet many premium wineries fear negative consumer cues. University of Florida researchers note oxygen ingress can shorten shelf life unless multilayer structures are used. ALPLA’s 30%-recycled PET format yields a 42% smaller carbon footprint, but adoption remains limited to entry or casual wines. Overcoming entrenched perceptions requires gradual exposure and education, tempering near-term PET growth among high-priced labels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum’s Rise Challenges Glass Leadership

Glass accounted for 66.65% of the United States wine packaging market share in 2025, equal to about USD 706.5 million within the United States wine packaging market size. Metal, led by aluminum, is projected to post an 8.31% CAGR through 2031 as brands prioritize lighter weights and closed-loop recycling credentials. Glass suppliers are countering with 390 g eco-bottle launches and higher cullet ratios that lower furnace energy use while preserving premium shelf presence. Paper composites and refillable-glass systems remain niche but signal the next wave of low-carbon formats that could erode glass share if supply chains scale.

Aluminum’s ascent hinges on reduced freight cost, 100% recyclability, and venue acceptance where breakage is a concern, while glass retains an authenticity advantage for premium cues. Ball’s plan to reach 85% recycled content by 2030 exemplifies the aggressive sustainability targets that drive material substitution. Glass makers are investing in electric furnaces and oxy-fuel burners to shield margins from natural-gas volatility, yet capital intensity slows fleet turnover. Ultimately, wineries are weighing carbon disclosures against brand heritage, prompting a gradual mix shift rather than an abrupt material handoff.

By Product Type: Cans Accelerate Amid Bottle Dominance

Glass bottles captured 56.12% of the 2025 value, but cans are expanding at a 7.74% CAGR as portability, recyclability, and event-venue policies favor unbreakable formats. Hydrogen-sulfide risks linked to can liner chemistry are being mitigated through improved internal coatings, opening the door for broader varietal adoption. Bag-in-box remains entrenched for bulk and value wines because vineyard labor shortages push producers toward formats that minimize handling. Plastic bottles and pouches serve price-sensitive or single-serve occasions but face premium-image headwinds.

Canned presentations align with younger demographics that prioritize environmental responsibility over tradition, evidenced by Bogle’s 90 g aluminum bottle introduction at USD 16.99 retail. Bottlers are also experimenting with resealable ends and secondary paper wraps to upgrade shelf visibility. For glass, lightweighting and emboss-free silhouettes are helping retain relevance by trimming freight emissions without compromising perceived quality. The result is a diversified product mix that lets wineries match pack type to channel, price tier, and consumption occasion.

By Closure Type: Screw Caps, Chip Away at Cork Tradition

Natural cork maintained 43.95% share in 2025, yet screw caps are advancing 7.98% annually as consumers favor convenience and wineries seek consistent oxygen ingress. Studies show screw caps can foster reductive conditions, but liner options now allow tuned permeability that protects aromatics for wines designed for near-term drinking. Technical cork and synthetics fill middle-price niches, blending cork aesthetics with lower cost and taint risk. Specialty closures such as crown caps and T-stoppers meet sparkling or fortified requirements but remain small in volume.

Cork suppliers are marketing forest-stewardship credentials and carbon sequestration claims, while aluminum-cap makers tout 35% emission cuts via recycled stock in launches like Amcor’s STELVIN Goes Greener. Premium estates are gradually adopting screw caps for white and rosé labels aimed at immediate consumption, reserving cork for cellar-worthy reds. As sensory studies continue to narrow performance gaps, closure choice is becoming a deliberate branding lever rather than a default tradition.

By Wine Type: Low-Alcohol Surge Within Still-Wine Stronghold

Still-wine formats represented 67.55% of United States wine packaging market size in 2025, translating to roughly USD 716 million of spend. Low and no-alcohol wines, though less than 5% of volume, are forecast to grow 9.02% per year through 2031 on wellness and moderation trends. These products demand barrier properties that preserve volatile aroma compounds despite lowered ethanol, prompting interest in multilayer bottles and cans with specialized liners. Sparkling and fortified wines maintain niche status, each with rigid closure and pressure-tolerance needs.

Dealcoholized offerings often target socially active consumers who seek premium cues without alcohol, driving brands to replicate traditional bottle shapes and label aesthetics. Packaging must also navigate differing labelling regulations on alcohol content, sugar, and nutritional disclosures. As producers diversify SKUs, suppliers see opportunities for custom portion sizes and interactive labels that guide pairing and serving tips. The segment’s rapid rise is pressuring legacy pack lines to handle lower fill temperatures and varying carbonation levels.

By Capacity: Single-Serve Growth Pressures Standard Bottles

Standard 375-750 mL bottles delivered 59.84% of 2025 revenue, yet sub-375 mL formats are climbing 7.41% yearly as portion control and convenience drive trial. Smaller sizes support premium pricing per ounce, enable sampler flights, and reduce waste for moderate drinkers. They also fit into stadium and airline settings where volume caps exist, favoring aluminum or PET to save weight. Large 1.5 L and 3 L sizes persist in family and food-service channels but face weaker growth.

Shrink-sleeve decoration and augmented-reality label initiatives help compact bottles retain shelf impact despite reduced billboard space. For wineries, higher bottling line changeover costs are offset by diversified revenue streams and inventory agility. Supply-chain planners note that small formats improve pallet utilization and lower DtC shipping costs, vital as carriers enforce stricter dimensional weight rules. Consequently, capacity choice is evolving from a passive tradition to a strategic marketing lever tied to channel economics.

By Distribution Channel: Retail Momentum Challenges Direct Sales Supremacy

Direct sales delivered 57.92% of 2025 volume as tasting-room and wine-club programs preserve high margins and data access. However, retail and on-premise outlets are set to expand at a 6.33% CAGR, boosted by private-label pushes from grocers and convenience chains. Retailers demand cost-efficient packs that maximize shelf density often cans, bag-in-box, or lightweight glass while DtC shipments prioritize protective secondary packaging and gift-ready aesthetics.

Mississippi’s 2025 D2C legalization widened e-commerce reach, yet varied state laws force pack differentiation to accommodate tax stamps and volume caps. Rising freight surcharges make feather-weight bottles and recycled-paper shippers attractive for subscription clubs. In stores, eye-catching sustainability claims and NFC tags that unlock provenance data are increasingly influential. The evolving channel mix compels wineries to adopt a portfolio approach, aligning packaging SKUs with margin structure, shopper journey, and regulatory overhead.

Geography Analysis

California generates the bulk of United States wine packaging market demand but grapples with a 20-year-low red-grape crop and a new CRV fee structure that increases compliance costs for small wineries. Oregon serves as a circular-economy testbed, where roughly 60 wineries are expected to refill 720,000 Revino bottles in 2024, cutting lifecycle emissions by 85%. Washington benefits from nearby aluminum smelters and tech-savvy consumers who reward sustainable packaging.

The Pacific Northwest’s weather-related labour tightness has accelerated bag-in-box usage to ease handling, especially along California’s Central Coast where 2024 grape tonnage fell 35%. Eastern states, though smaller wine producers, are leveraging proximity to dense population centres to build DtC programs that rely on damage-resistant parcel packs. State-by-state shipping restrictions continue to demand nuanced labelling and fulfilment strategies, creating service niches for specialised contract packagers.

Competitive Landscape

The United States wine packaging market is moderately fragmented. Owens-Illinois leads in glass but saw volumes dip after natural-gas spikes raised furnace costs, prompting a strategic pivot toward leaner furnaces and recycled-content targets. Ardagh’s 2024 Houston shutdown illustrates exposure to demand swings in adjacent beer glass, handing share to nimble rivals.

Aluminum specialist Ball is scaling capacity with a new Oregon plant to harness fast-growing canned-wine demand while advancing toward 85% recycled content. Paper-bottle pioneer Frugalpac struck US production deals that could exceed 2.5 million units annually, signalling competitive threats from disruptive substrates.

Amcor closed a USD 650 million merger with Berry Global, blending film, cap, and closure expertise and signalling aggressive synergy extraction goals. Patent filings around self-aerating glass further show how incumbents chase differentiation beyond raw material battles. Across the United States cost structures, M&A ambitions, and technology races are redefining supplier hierarchies.

United States Wine Packaging Industry Leaders

AMCOR PLC

Ball Corporation

Owens–Illinois Inc.

Ardagh Group

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Oregon’s Senate Bill 1520 took effect, adding canned wine to the Bottle Bill at a 10-cent redemption fee.

- June 2025: Amcor completed its merger with Berry Global, targeting USD 650 million in annual cost synergies and 12% adjusted EPS growth by 2026.

- June 2025: Revino refillable bottles hit 720,000 fills across 60 Oregon wineries, extending bottle life up to 50 cycles.

- February 2025: ProMach formed a Wine & Spirits Solutions Group to integrate filling and packaging lines for alcoholic beverages.

United States Wine Packaging Market Report Scope

The wine packaging market uses various materials and product types for the packaging of wines. Segmentation is done the basis of material (glass, metal, paper, etc.) and product type (Glass bottles, Plastic bottles, Bag in Box, etc). The report offers market forecasts and size in value (USD) for all the above segments.

By Material Type

| Glass |

| Plastic |

| Metal |

| Paper |

By Product Type

| Glass Bottles |

| Plastic Bottles |

| Bag-in-Box |

| Cans |

| Pouches |

By Closure Type

| Natural Cork |

| Technical/Synthetic Cork |

| Screw Caps |

| Crown Caps |

| Other Closure Types (T-stoppers, Vino-Lok) |

By Wine Type

| Still Wine |

| Sparkling Wine |

| Fortified and Dessert Wine |

| Low and No-Alcohol Wine |

By Capacity

| Less than 375 mL |

| 375-750 mL |

| 750-1,500 mL |

| More than 1,500 mL |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

| By Material Type | Glass |

| Plastic | |

| Metal | |

| Paper | |

| By Product Type | Glass Bottles |

| Plastic Bottles | |

| Bag-in-Box | |

| Cans | |

| Pouches | |

| By Closure Type | Natural Cork |

| Technical/Synthetic Cork | |

| Screw Caps | |

| Crown Caps | |

| Other Closure Types (T-stoppers, Vino-Lok) | |

| By Wine Type | Still Wine |

| Sparkling Wine | |

| Fortified and Dessert Wine | |

| Low and No-Alcohol Wine | |

| By Capacity | Less than 375 mL |

| 375-750 mL | |

| 750-1,500 mL | |

| More than 1,500 mL | |

| By Distribution Channel | Direct Sales |

| Indirect Sales |

Key Questions Answered in the Report

What is the current value of the United States wine packaging market?

The market stands at USD 1.12 billion in 2026 and is projected to reach USD 1.46 billion by 2031.

Which packaging material is growing fastest?

Aluminum and other metal formats are expanding at an 8.31% CAGR thanks to recyclability and light weight.

How are deposit-return laws affecting packaging choices?

New 10-cent fees on canned wine in Oregon and expanded CRV rules in California are pushing suppliers toward high-recycled-content designs that meet circular-economy targets.

Why are smaller wine formats gaining traction?

Sub-375 mL containers are rising 7.41% annually as consumers seek portion control and brands leverage premium single-serve pricing.

What role does direct-to-consumer shipping play in design decisions?

DtC liberalisation across 47 states is driving demand for lightweight, protective, and gift-ready packs that can survive parcel networks while elevating the unboxing experience.

Which closure type is winning share from cork?

Screw caps are capturing volume at an 7.98% CAGR due to consistent seal quality and consumer convenience, especially for wines intended for early consumption.

Page last updated on: