Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

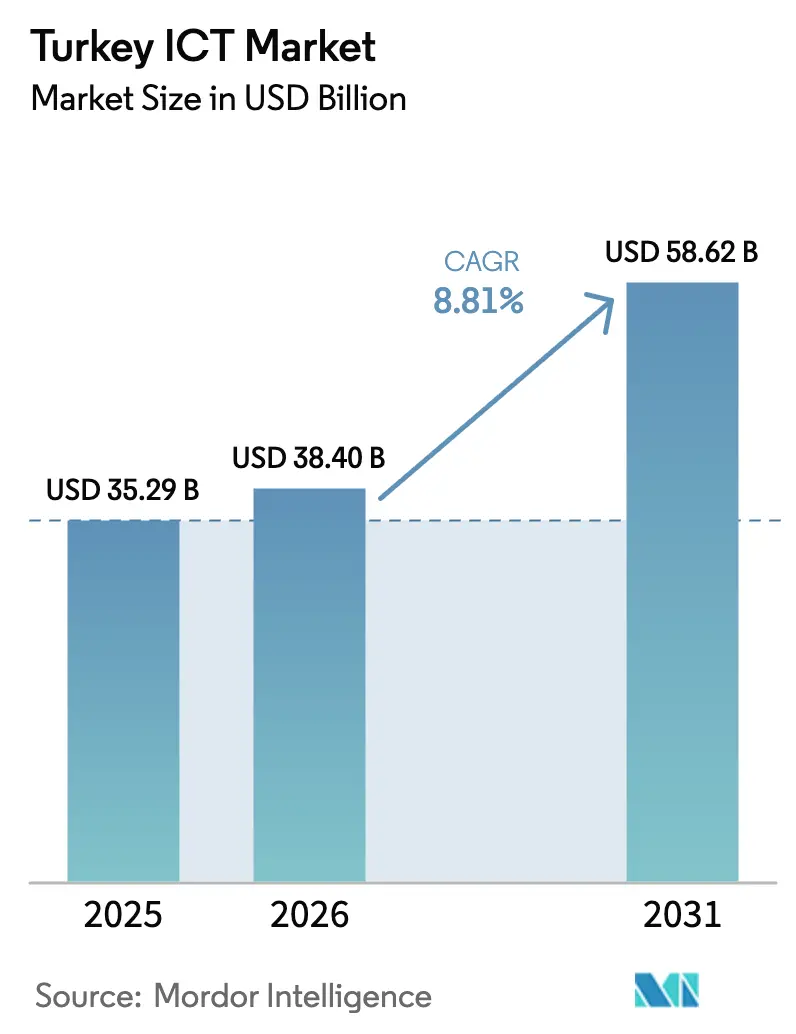

| Base Year Market Size (2025) | USD 35.29 Billion |

| Market Size (2026) | USD 38.4 Billion |

| Market Size (2031) | USD 58.62 Billion |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey ICT Market Analysis by Mordor Intelligence

The Turkey ICT market size was valued at USD 35.29 billion in 2025 and estimated to grow from USD 38.4 billion in 2026 to reach USD 58.62 billion by 2031, at a CAGR of 8.81% during the forecast period (2026-2031). A young digital-native population, aggressive government digitalization programs and sustained private-sector investment create a stable demand baseline despite macroeconomic volatility. Cloud-first adoption among small and medium enterprises accelerates infrastructure modernization, while the country’s position between Europe and Asia attracts regional data-hub investments. Telecommunications incumbents reinforce competitive intensity by pairing 5G rollouts with content-delivery partnerships. Currency fluctuations and energy-price swings constrain hardware imports and data-center operating margins, yet ongoing submarine-cable and edge-facility projects mitigate long-term risks through diversified connectivity routes.

Key Report Takeaways

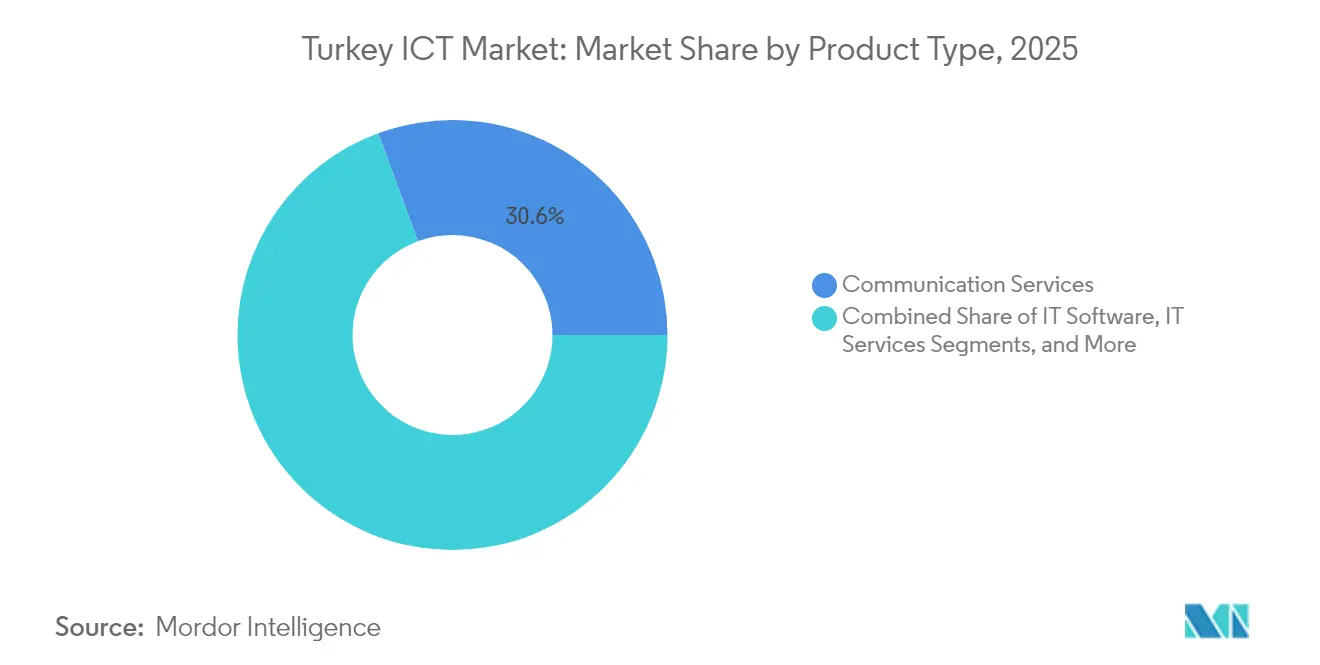

- By product type, Communication Services led with 30.62% revenue share in 2025; Cloud Services is forecast to expand at a 9.04% CAGR through 2031.

- By enterprise size, SMEs held 52.74% of the Turkey ICT market share in 2025, while the segment posts the fastest 8.98% CAGR through 2031.

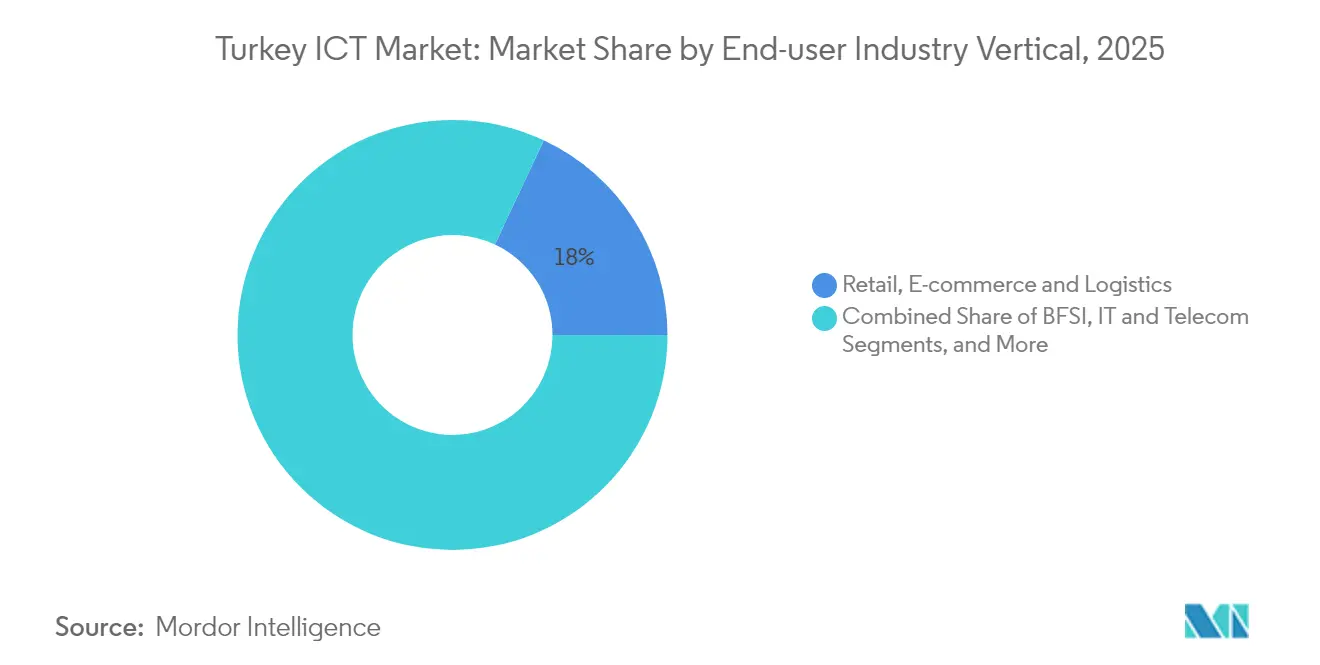

- By end-user vertical, Gaming and Esports recorded the highest 10.12% CAGR to 2031, whereas Retail, E-commerce, and Logistics retained the largest share at 18.02% in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led "Digital Türkiye" and 5G investment push | +2.1% | National, with priority focus on Istanbul, Ankara, Izmir | Medium term (2-4 years) |

| Rapid e-commerce and digital payments expansion | +1.8% | National, strongest in urban centers and western regions | Short term (≤ 2 years) |

| High mobile-broadband penetration and young population | +1.4% | National, with rural acceleration through 5G rollout | Long term (≥ 4 years) |

| Cloud adoption surge among SMEs | +1.3% | National, concentrated in industrial clusters | Medium term (2-4 years) |

| Regional disaster-recovery data-center hub emergence | +0.9% | National hub strategy, serving MENA and Eastern Europe | Long term (≥ 4 years) |

| New submarine-cable corridors boosting wholesale traffic | +0.8% | National infrastructure, regional connectivity benefits | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-led “Digital Türkiye” and 5G investment push

The Digital Türkiye roadmap prioritizes nationwide gigabit connectivity and secure critical ICT infrastructure. The administration channels public-private funds into 5G spectrum auctions, fiber backbones and cybersecurity frameworks that set common technical standards. A single-window permit system shortens rollout timelines for base-station upgrades, increasing investor confidence. Preferential financing for locally-sourced equipment stimulates domestic vendors such as HAVELSAN and ASELSAN, which in turn retain intellectual property within national borders. The regulatory clarity provided by the Information and Communication Technologies Authority encourages global cloud providers to deploy edge nodes and form joint ventures with Turkish operators.[1]Presidency Investment Office, “ICT – Invest in Türkiye,” invest.gov.tr

Rapid e-commerce and digital payments expansion

Transaction volumes on digital marketplaces surge as merchants integrate frictionless checkout, embedded finance and buy-now-pay-later options. The acquisition of Paynet by iyzico for USD 87 million demonstrates healthy domestic consolidation that raises service-quality thresholds. Banks digitize credit-origination workflows, extending payment terms for small suppliers and deepening financial inclusion. Interoperability between fintech APIs and legacy core-banking platforms accelerates adoption of instant-payment rails. Retailers leverage omnichannel inventory systems to synchronize physical outlets with online storefronts, which enlarges addressable cloud-services demand.

High mobile-broadband penetration and young population

Smartphone adoption exceeds four-fifths of the population, fueling rich-media consumption and gaming revenue. Operators monetize data packages through value-added services, and IoT subscriptions climb steadily in logistics, energy and agriculture. The workforce skews under 35 years of age, aligning skill sets with software development, DevOps and game design. Success stories such as Paxie Games’ 28-million-download casual title spark venture-capital inflows and reinforce Turkey’s image as a creative-content incubator. Demographic momentum sustains long-run demand for high-capacity mobile-edge compute nodes.

Cloud adoption surge among SMEs

Cost-elastic subscription models resonate with firms exposed to currency risk, enabling them to convert capital expenditure into predictable operating costs. Domestic providers bundle SaaS, managed security and compliance audit services that meet local data-protection laws, removing entry barriers for first-time adopters. Manufacturing SMEs pilot predictive-maintenance applications using cloud-hosted analytics, achieving measurable downtime reductions. Financial institutions co-design industry clouds that support sandbox testing for regulatory reporting. Year-over-year cloud revenue growth for leading telcos underscores the shift from proof-of-concept to production workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and high hardware import costs | -1.90% | Nationwide, import-heavy verticals | Short term (≤ 2 years) |

| Digital-services tax and data-localization uncertainty | -1.10% | Nationwide, multinational cloud providers | Medium term (2-4 years) |

| Scarcity of bilingual AI/ML training datasets | -0.80% | Nationwide, AI-focused startups | Long term (≥ 4 years) |

| Electricity-price swings hurting data-center margins | -0.70% | Concentrated in Istanbul-Ankara hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency volatility and high hardware import costs

Elevated policy rates increase working-capital expenses for distributors that rely on dollar-denominated credit lines. Lira depreciation inflates unit prices for servers, routers and storage arrays, compelling enterprises to extend refresh cycles. Some manufacturers relocate final assembly to free-trade zones to capture tariff exemptions, yet scale remains insufficient to counterbalance exchange-rate exposure. Widening bid-ask spreads in foreign-exchange markets create procurement timing risks, which distorts budgeting for public-sector tenders. These pressures collectively defer on-premise infrastructure projects and shift demand toward subscription-based alternatives.

Digital-services tax and data-localization uncertainty

A 7.5% levy on digital revenue complicates forecasting for global platform providers. Overlapping obligations under upcoming OECD Pillar Two reforms demand dual compliance frameworks, raising legal and accounting overhead. Some providers accelerate build-out of in-country availability zones to minimize cross-border data transfers and related penalties. Smaller SaaS vendors without local entities pass incremental costs to customers, tempering price competitiveness. Ongoing consultations on AI governance prolong investment decision cycles for high-computing projects that depend on international datasets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Communication Services Lead Infrastructure Modernization

Communication Services captured the largest revenue slice at 30.62% in 2025. Operators allocate spectrum-auction proceeds toward massive-MIMO upgrades and low-latency backhaul, which embeds long-term annuity streams into the Turkey ICT market. Meanwhile Cloud Services registers the fastest 9.04% CAGR, indicating structural migration of compute workloads from enterprise data rooms to hosted platforms. IT Hardware demand slows under currency-linked cost pressures, but localized assembly initiatives cushion decline. Software vendors localize user interfaces and compliance modules, lifting addressable spend from government contracts. IT Infrastructure growth concentrates in high-density urban corridors that interconnect carrier-neutral facilities. Security-solution uptake responds to escalating breach incidents across public agencies, and managed-service providers bundle threat-intelligence feeds to strengthen customer retention.

A surge in video-streaming subscriptions elevates backbone traffic, requiring continual capacity investments that reinforce the primacy of Communication Services. Interoperator network-sharing arrangements reduce capital duplication, releasing funds for edge-content caches that improve user experience in secondary cities. The Turkey ICT market size attached to Cloud Services benefits from tiered-storage offerings that suit cost-sensitive SMEs. Hybrid-cloud orchestration tools gain momentum among regulated entities aiming to retain sensitive databases on-premise while running analytics in public clouds. Hardware distributors hedge currency exposure through consignment stock that shortens delivery cycles during tariff repricing windows. Domestic software houses leverage low-code platforms to accelerate e-government portal development, and security integrators earn premium margins by embedding zero-trust architectures into DevOps pipelines.

By Enterprise Size: SME Digital Transformation Accelerates

SMEs hold more than half of overall 2025 revenue, underscoring their central role in the Turkey ICT market. Their swift procurement processes compress sales cycles for SaaS and IaaS vendors, producing recurring revenues that are less sensitive to macro swings. Cloud-based point-of-sale and enterprise-resource-planning systems dominate first-time IT purchases, closing the digital gap between small merchants and urban franchises. Government grants covering up to 60% of software expenses further propel uptake, particularly in export-oriented manufacturing clusters. The segment also fuels cybersecurity demand because managed service bundles offer compliance tools that meet personal-data regulations without in-house expertise.

Large Enterprises pursue modernization through multi-year programs that weave existing mainframes into containerized microservices. Their spending shapes the upper tier of the Turkey ICT market size as they procure private cloud nodes, disaster-recovery seats and unified-communications licenses. Vendor selection emphasizes sovereign-cloud assurance to satisfy data-localization statutes. Integration-service providers win contracts by orchestrating identity-access management across hybrid estates. Rising volumes of proprietary data encourage corporations to deploy analytics lakes that feed digital-twin use cases in oil, steel and automotive plants. As venture funding crosses USD 2.6 billion in 2024, a growing pool of scale-ups graduates into the large-enterprise bracket, further blurring traditional size definitions.

By End-user Industry Vertical: Gaming Leads Growth Acceleration

Gaming and Esports advance at a 10.12% CAGR, propelled by mobile first engagement and international studio acquisitions. Cloud-rendering services lower hardware barriers for mid-range devices, while localized payment gateways support micro-transactions in local currency. Competitive leagues hosted in Istanbul arenas stimulate peripheral spending on streaming infrastructure and content-delivery networks. Meanwhile Retail, E-commerce and Logistics continues to dominate revenue thanks to its 18.02% share, reflecting entrenched omnichannel habits among urban consumers. Fulfillment centers integrate AI-driven stock-placement engines that compress last-mile delivery times to under two hours in major cities.

The government sector scales e-procurement and citizen-service portals, driving demand for secure ID verification, workflow automation and analytics dashboards. Financial institutions integrate spatial-computing interfaces such as Apple Vision Pro within mobile apps, setting precedent for immersive banking experiences. Manufacturers adopt predictive-maintenance analytics and autonomous-guided vehicles on factory floors to raise productivity in line with Digital Anatolia objectives. Healthcare providers embed telemedicine modules within national e-health records, widening specialist reach to rural districts. Energy utilities install IoT sensors across pipeline networks, linking data streams to AI-driven anomaly-detection platforms that avert supply disruptions.

Geography Analysis

Istanbul, Ankara and Izmir constitute the primary nexus for research, talent and venture capital that fuels the Turkey ICT market. These metropolitan clusters host interconnected carrier hotels that enable sub-2 millisecond round-trip latency between cloud availability zones and financial trading venues. Provincial cities in the Marmara and Aegean regions leverage improved fiber rings to participate in nationwide e-commerce and remote-work patterns. Eastern Anatolia benefits from universal-service fund projects that extend 4G and pilot 5G coverage to mountainous districts, facilitating telehealth and distance-learning adoption.

Regional data-center capacity concentrates along seismic-resilient corridors outside Ankara, where Türksat’s planned 21-megawatt facility will triple sovereign cloud capacity and backstop government workloads. Submarine-cable landing points in Çanakkale and Mersin diversify routes toward southern Europe, the Maghreb and the Gulf, positioning Turkey as a neutral peering location. Energy-corridor synergies allow hyperscalers to co-locate fiber conduits with oil-pipeline rights-of-way, lowering trenching costs.

Digital inclusion programs deploy mobile base stations aboard buses and ferries servicing sparsely populated areas, ensuring that e-government push notifications reach residents in real time. Clustered industrial zones in Bursa and Kocaeli adopt smart-factory standards, driving localized demand for edge AI gateways. Universities in Eskisehir and Gaziantep contribute bilingual AI datasets that mitigate the national shortage, creating specialized research enclaves. Turkey’s location across two time zones allows managed-service centers to provide near-shore support to Western Europe in the morning and to the Gulf in the afternoon, raising utilization rates of telecom backbones.

Competitive Landscape

Telecommunications incumbents Turkcell, Türk Telekom, and Vodafone Türkiye operate under revenue-share regimes that emphasize network-quality differentiation. The trio collectively owns fiber routes exceeding 400,000 kilometers, which form the basic transport layer for many smaller cloud and content providers. In cloud services, hyperscalers such as Microsoft, Google, and Amazon establish local regions in partnership with telcos to satisfy data sovereignty demands. Domestic vendors like GlassHouse extend hybrid-cloud management and disaster-recovery solutions, strengthened by e& Enterprise’s USD 60 million stake that injects capital and Gulf market access.[2]GlassHouse, “A New Era Begins: GlassHouse Joins the e& Enterprise Family,” glasshouse.com.tr

Gaming studio exits to international buyers signal a maturing creative ecosystem. The USD 67 million purchase of Paxie Games by DoubleU Games underscores valuation premiums attainable for titles with global reach.[3]Silicon UK via Businesswire, “DoubleU Games completes acquisition of Paxie Games,” silicon.co.uk Defense-electronics leaders HAVELSAN and ASELSAN diversify into civilian cybersecurity and cloud orchestration, leveraging domain expertise in secure systems. Fintech consolidation accelerates as iyzico’s Paynet deal scales transaction throughput to 350 billion liras, reinforcing network effects in payment processing.

Strategic positioning favors partnerships that blend localized compliance with global scale. Vodafone partners with IBM to deliver industry clouds targeting automotive suppliers, while Turkcell’s fiber backbone hosts Oracle’s interconnection nodes for low-latency database replication. Acquisition pipelines focus on AI-driven observability, low-code workflow engines and language-localization platforms. Competitive variables therefore extend beyond traditional price-bandwidth metrics into ecosystem depth, regulatory alignment and vertical specialization.

Turkey ICT Industry Leaders

Turkcell İletişim Hizmetleri A.S.

Turk Telekomunikasyon A.S.

Vodafone Telekomunikasyon A.S.

Amazon Web Services Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BtcTurk acquired VNGRS to create BtcTurk Teknoloji and deepen product-engineering capabilities.

- March 2025: HAVELSAN secured a four-year agreement to supply ADVENT Combat Management System to the Chilean Navy.

- March 2025: DoubleU Games finalized its USD 67 million purchase of Paxie Games after competition clearance.

- March 2025: DenizBank integrated Apple Vision Pro into its MobilDeniz app in collaboration with Intertech and Commencis.

Turkey ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Turkey ICT Market is segmented by Type (Hardware, Software, IT Services, and Telecommunication Services), the Size of the Enterprise (Small and Medium Enterprise and Large Enterprises), and Industry Vertical (BFSI, IT and Telecom, Government, Retail and E-commerce, Manufacturing, and Energy and Utilities). The report provides the market sizes and forecasts in terms of value in USD.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Gaming and Esports |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Gaming and Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large is the Turkey ICT market in 2026?

The sector is valued at USD 38.4 billion in 2026 and is set to surpass USD 58.62 billion by 2031.

Which segment grows fastest within Turkey’s technology ecosystem?

Cloud Services posts the highest 9.04% CAGR as enterprises migrate workloads from on-premise systems.

Why do SMEs invest heavily in digital tools in Turkey?

SMEs convert capital expenses into predictable cloud subscriptions, aided by government incentives that cover part of software costs.

What challenges hinder data-center profitability?

Volatile electricity pricing and currency depreciation elevate operating expenses, prompting operators to pursue renewable-energy contracts.

How is Turkey positioning itself as a regional tech hub?

Investments in submarine-cable corridors, 5G expansion and sovereign cloud facilities attract cross-border workloads from the Middle East and Eastern Europe.

Which emerging technology vertical shows the strongest momentum?

Gaming and Esports advances at a double-digit CAGR thanks to a youthful population and international studio acquisitions.

Page last updated on: