Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

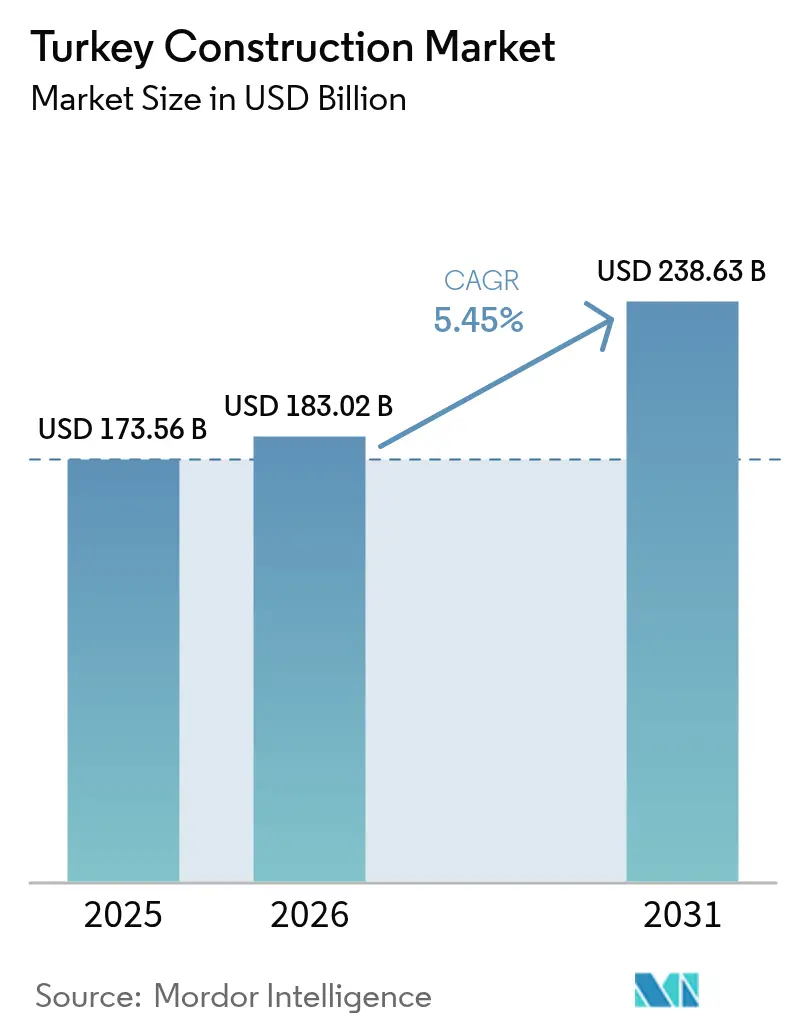

| Base Year Market Size (2025) | USD 173.56 Billion |

| Market Size (2026) | USD 183.02 Billion |

| Market Size (2031) | USD 238.63 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Construction Market Analysis by Mordor Intelligence

The Turkey construction market size was valued at USD 173.56 billion in 2025 and estimated to grow from USD 183.02 billion in 2026 to reach USD 238.63 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031). Multiple tailwinds interact to sustain this trajectory: a USD 46.2 billion public-investment program, record-scale post-earthquake reconstruction, and a widening pipeline of public-private partnerships that already total 270 completed projects worth USD 204 billion. Sector leaders also capitalize on Turkey’s Belt and Road positioning, giving the Turkey construction market unique access to trans-Eurasian trade flows and concessional finance. New seismic codes introduced in 2025 add compliance costs yet simultaneously spur demand for retrofit engineering, while green-cement mandates and ESG-linked loans accelerate uptake of low-carbon building solutions. Further momentum comes from industrial free-zone expansion that compresses permitting time by up to 40%, and a digital-construction push that channels prefabrication to offset skilled-labor shortages.

Key Report Takeaways

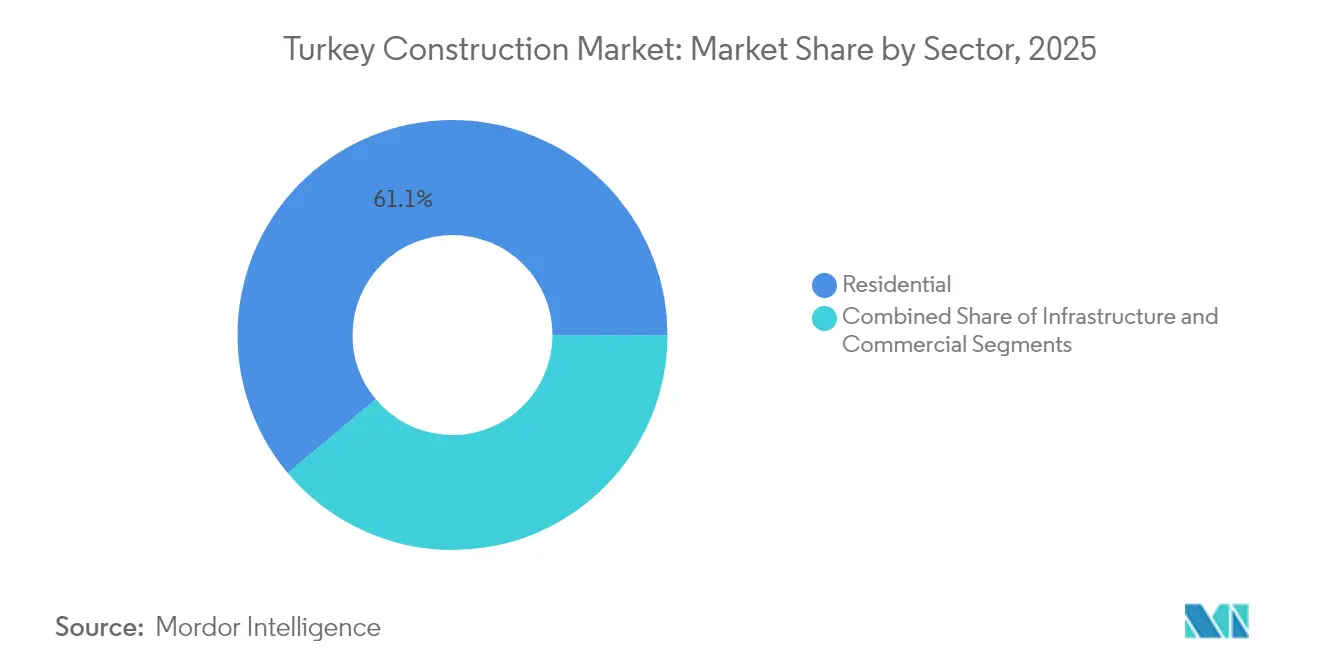

- By sector, residential construction led with 61.10% of Turkey construction market share in 2025; infrastructure is set to expand at a 6.92% CAGR to 2031.

- By construction type, new-build activity accounted for 76.35% share of the Turkey construction market size in 2025, while renovation is forecast to progress at a 5.96% CAGR through 2031.

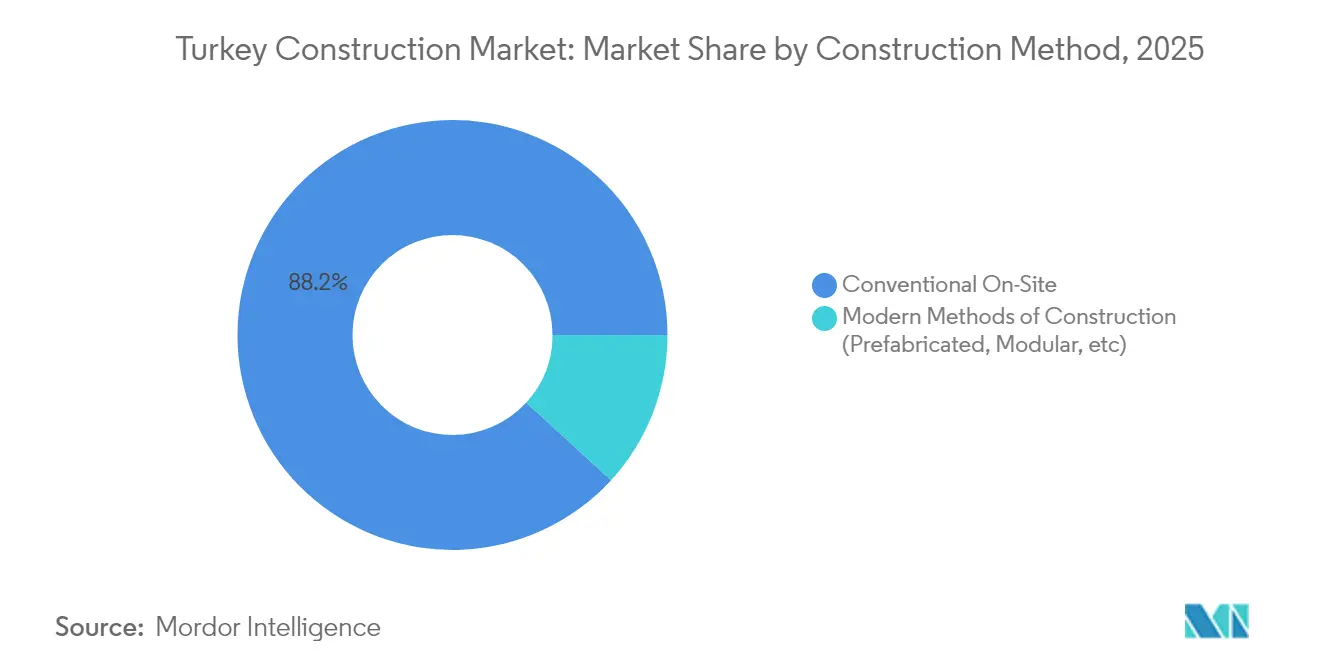

- By construction method, conventional on-site practices held 88.20% of the Turkey construction market size in 2025; prefabricated and modular systems are poised for a 7.64% CAGR over the outlook period.

- By investment source, public funding captured 65.40% of the Turkey construction market share in 2025, whereas private-sector outlays are projected to climb at a 7.41% CAGR to 2031.

- By region, Istanbul commanded 25.80% of the Turkey construction market share in 2025, while the Rest of Turkey region is projected to advance at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing industrial free-zone expansion | +1.2% | Ceyhan, Istanbul, Izmir | Medium term (2-4 years) |

| Surge in green-certified projects & ESG financing | +0.9% | Major metros | Medium term (2-4 years) |

| Rising urban-renewal & earthquake-resilient demand | +0.8% | Istanbul, Ankara, the southeast | Short term (≤ 2 years) |

| Government mega-infrastructure spending pipeline | +0.6% | National corridors | Long term (≥ 4 years) |

| Affordable-housing programs & mortgage subsidies | +0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Industrial Free-Zone Expansion

Industrial free-zones intensify Turkey’s manufacturing appeal by bundling tax incentives, streamlined permits, and logistics connectivity, all of which expand the Turkey construction market. The Ceyhan Energy Specialized Industrial Zone anchors hydrocarbons processing and trims the nation’s USD 60 billion intermediate-goods import bill. Accelerated approvals that cut development cycles by up to 40% stimulate a continuous flow of factory, warehouse, and utility projects. Foreign investors co-locate suppliers inside zones, magnifying spillover construction demand along the value chain. These clusters dovetail with the 2024-2028 International Direct Investment Strategy, which prioritizes green transformation and supply-chain diversification, ensuring sustained project inflows over the medium term.

Surge in Green-Certified Projects & ESG Financing

Turkey’s 2053 net-zero pledge pushes developers to seek ESG-linked loans that lower borrowing costs in exchange for certified energy performance. The World Bank’s USD 3.2 billion climate framework funds decarbonization measures, while a new Building Sector Decarbonization Roadmap sets zero-carbon standards for all public projects. Cement and steel suppliers confront the EU Carbon Border Adjustment Mechanism, giving rise to green-hydrogen installations targeting 2 GW electrolyzer capacity by 2030. Concurrently, public tenders now require reduced-clinker cement beginning January 2025, channeling R&D toward alternative binders. These converging forces embed sustainability as a core selection criterion across the Turkey construction market[1]Ministry of Environment, Urbanization and Climate Change, “Yarısı Bizden Program,” csb.gov.tr.

Rising Urban-Renewal & Earthquake-Resilient Demand

Turkey has launched the world’s largest seismic retrofit program, targeting 6.7 million vulnerable structures after the 2023 quakes. Istanbul’s ‘Yarısı Bizden’ campaign offers grants up to USD 54,000 per dwelling, sparking 21,000 active construction sites and 41,000 pipeline projects. Updated performance-based codes elevate building costs by 15-25% but open premium niches for specialized structural engineers. World Bank financing of EUR 219.4 million links resilience with energy efficiency, so upgrades now encompass insulation, HVAC, and renewable integration, broadening revenue layers for contractors. These combined policies turn urban renewal into a multi-decade construction growth engine.

Government Mega-Infrastructure Spending Pipeline

An explicit state objective is to lift motorway stock to 4,728 km by 2028 while devoting 49% of infrastructure outlays to rail in 2024. Flagship projects such as the USD 594 million Orient Express high-speed rail line, co-funded by the EU, embed EU-grade standards in local contracts. Strategic road-bridge packages have already delivered 488 km of bridges since 2003, a 157% surge, reinforcing regional connectivity. The Twelfth Development Plan aligns these ventures to green and digital mandates, ensuring that future bids stipulate low-carbon materials, BIM coordination, and smart-asset management. Continuous mega-project flow sustains multi-year backlog visibility for tier-one contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile lira driving material-import inflation | –0.7% | Import-dependent areas | Short term (≤ 2 years) |

| Tight monetary policy is dampening housing demand | –0.5% | Istanbul & Ankara | Short term (≤ 2 years) |

| Contractor insolvency & payment-delay risks | –0.4% | Small-contractor clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Lira Driving Material-Import Inflation

Turkey sources nearly 40% of its construction inputs abroad, making projects sensitive to currency swings. Lira depreciation amplifies steel, aluminum, and mechanical-equipment costs, compressing margins on fixed-price contracts. Hedging and escalation clauses offer partial relief yet can erode competitiveness in public tenders. Elevated inflation forecast at 43% for 2024 adds further strain by lifting domestic logistics and labor expenses. Some contractors localize supply or invest in domestic plants, but these capital-intensive moves dilute balance-sheet flexibility in the near term.

Tight Monetary Policy Dampening Housing Demand

Aggressive interest-rate hikes reduce mortgage affordability, causing a 6% decline in national home sales during Q2 2024. Developers counter by extending installment plans and partnering with banks to offer below-market loan packages, but overall absorption rates remain below pre-tightening levels. Istanbul is disproportionately affected, holding 40.6% of the national housing surplus, whereas interior provinces fare better due to reconstruction demand. Prolonged credit constraints could delay new residential starts, although retrofit activity partially compensates by targeting existing stock rather than new units. Market sentiment hinges on inflation moderation and eventual monetary easing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Outpaces Residential Dominance

Infrastructure construction accounted for 31.05% of Turkey construction market size in 2025, whereas residential commanded a larger 61.10% share. Yet infrastructure is projected to be the fastest-growing with a 6.92% CAGR through 2031, powered by highway extensions, high-speed rail lines, and energy corridors. Government outlays of USD 16.3 billion for transport alone in the 2025 investment program validate sustained work pipelines. Contractors active in road, rail, and bridge packages gain from multi-year contracts that shield workflows against cyclical housing soft patches.

Rapid scale-up of energy infrastructure adds further depth. The Akkuyu nuclear project’s four 1,200 MW reactors, slated for phased commissioning in 2025, anchor a multi-billion-dollar construction scope. Renewable expansion complements baseload capacity, with utility-scale solar parks and wind clusters embedding smart-grid interfaces. Logistics construction inside industrial free-zones rounds out the opportunity set, while commercial offices in Istanbul gradually pivot toward green-certified retrofits anchored by LEED and BREEAM protocols. Together, these sub-sectors inject diversified volume, reinforcing the upward trajectory of the Turkey construction market.

By Construction Type: Renovation Becomes a Strategic Priority

New-build projects held 76.35% of Turkey construction market share in 2025, but renovation is forecast to post a 5.96% CAGR to 2031, mirroring mandated seismic upgrades. The Turkish Building Earthquake Code of 2018 and the 2025 enforcement directive make retrofit compliance obligatory for structures erected before 2000. Istanbul’s ‘Yarısı Bizden’ program alone has catalyzed 106,000 funding applications that translate into USD 69 million in committed works. Shorter permitting cycles for retrofit approvals are now down to six months, accelerating cash conversion for contractors specializing in structural reinforcement.

Retrofit complexity, encompassing base isolation, carbon-fiber wrapping, and HVAC re-specification, commands higher margins than standard shell-and-core construction. World Bank-co-financed energy-efficiency upgrades piggyback on seismic scopes, bundling insulation, glazing, and rooftop solar into single contracts. Although material input inflation challenges cost control, renovation timescales are typically shorter than ground-up builds, limiting exposure to exchange-rate volatility. As a result, renovation forms a counter-cyclical buffer, stabilizing the Turkey construction market during housing-credit slowdowns.

By Construction Method: Prefabrication Edges into Mainstream

Conventional on-site techniques represented 88.20% of Turkey construction market size in 2025; nonetheless, prefabricated and modular systems are poised for a 7.64% CAGR through 2031. Labor shortages and the need for stricter quality control make factory-assembled components attractive, especially in seismic-risk zones where uniform structural integrity is critical. Modular housing can cut schedule duration by 40% while meeting code-mandated performance criteria, a crucial benefit for post-quakes rapid rehousing.

Digitalization is the keystone of modern methods. Building Information Modeling facilitates clash detection before factory production, curbing rework rates. Early movers such as ENKA have piloted hybrid steel-modular units on both domestic and export contracts, signaling an industry shift toward design-for-manufacture. Regulatory bodies have updated approvals to recognize modular standards, reducing certification bottlenecks. Long term, rising adoption of robotics and AI-driven quality inspection across precast yards will narrow the cost differential with conventional builds, increasing the penetration of modern methods in the Turkey construction market.

By Investment Source: Private Capital Accelerates Under ESG Lens

Public funding controlled 65.40% of the 2025 Turkey construction market share, but private investment is forecast to expand at a 7.41% CAGR to 2031. ESG-linked instruments unlock lower interest coupons for green-certified schemes, stimulating commercial developers to exceed baseline sustainability thresholds. World Bank blended-finance mechanisms crowd in private lenders by offering first-loss guarantees tied to carbon-reduction metrics. High-yield prospects in premium residential and office assets, where rent premiums of 15-20% are achievable for certified buildings, further incentivize private allocation.

Public-private partnership (PPP) structures remain a mainstay, covering hospitals, transport corridors, and renewable plants. Turkey’s 270 completed PPPs valued at USD 204 billion showcase mature risk-sharing templates. Equity sponsors increasingly blend mezzanine tranches to optimize capital structures, while construction contractors take minority stakes to secure EPC backlogs. As green-taxonomy rules tighten in Europe, Turkish developers aim to future-proof assets through design alignment, ensuring continued access to cross-border capital pools.

Geography Analysis

Istanbul captured 25.80% of the Turkey construction market in 2025, underpinned by its role as the nation’s finance and logistics nucleus. Its skyline continues to densify through high-rise residential and Grade-A office towers, yet the city also leads retrofitting volume with 21,000 active seismic-upgrade sites. Housing oversupply has eased rents, prompting developers to pivot toward mixed-use and hospitality conversions, while the new mandatory green-cement rule raises material compliance costs that premium projects can absorb.

Ankara and Izmir follow as secondary hubs, benefiting from decentralization incentives that steer government ministries and corporate back offices away from Istanbul. Metro extensions and ring-road upgrades expand urban footprints, spurring suburban housing and retail plazas. Izmir, with its coastal tourism focus, registers higher hotel occupancy conversions, whereas Ankara’s knowledge-economy tilt drives demand for technology parks and research facilities. Both cities leverage smart-city pilots that integrate IoT sensors for traffic and energy management.

Provinces in the southeast represent the fastest-growing geography at a 6.78% CAGR through 2031, driven by massive reconstruction grants and industrial-zone rollouts. Free-zone policy spreads to Gaziantep and Şanlıurfa, triggering demand for logistics sheds and supplier campuses. Rural-urban migration across Anatolia supports incremental residential starts, and donor-funded educational and healthcare facilities round out social infrastructure needs. Collectively, these regional flows balance the Turkey construction market, mitigating reliance on Istanbul while accelerating convergence between core and periphery.

Competitive Landscape

Turkey's construction market displays moderate fragmentation: the top five firms collectively hold a moderate percentage of the revenue share, leaving ample space for specialized mid-tier players. Leading contractor ENKA leverages strong balance-sheet liquidity to secure EPC contracts in power and petrochemicals domestically and overseas, recently lifting its order book to USD 5.8 billion. Rönesans pursues a design-build-operate model across healthcare PPPs, streamlining lifecycle costs that appeal to government sponsors. Domestic alloy-steel supplier Tosyalı invests in green hydrogen to align with low-carbon mandates, locking in material demand from public projects.

International diversification is a hallmark competitive move. Turkish firms completed 1,800 African projects worth USD 85 billion in 2023, exporting turnkey know-how while buffering lira volatility. Experience with FIDIC contracts and multilateral lenders allows these companies to pivot among markets as currency or demand shifts occur. Conversely, smaller local builders struggle with rising performance-bond premiums and payment delays, occasionally resorting to joint ventures with larger peers to access financing[3]Global Arbitration Review, “Turkish Contractors Expand in Africa,” globalarbitrationreview.com.

Digital capabilities emerge as a new battleground. Early adopters deploy BIM-enabled quantity takeoffs and drone-based site analytics that shorten procurement lead times. Prefabrication entrants partner with machinery manufacturers to improve line automation and reduce cycle times. Meanwhile, legal reforms targeting time-bound permit issuance compress competitive advantage windows, rewarding firms that can mobilize quickly. Overall, rivalry favors players able to harmonize cross-border pipeline, technology investment, and sustainability credentials.

Turkey Construction Industry Leaders

Rönesans Holding (Renaissance Construction)

Limak İnşaat

ENKA İnşaat ve Sanayi A.Ş.

TAV Construction

Alarko Contracting Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ENKA İnşaat reported USD 3.1 billion in 2024 revenue and expanded its backlog to USD 5.8 billion, highlighting resilience in the Turkey construction market.

- February 2025: Government earmarked USD 46.2 billion for 3,783 projects in its Public Investment Program, with USD 16.3 billion for transportation.

- January 2025: Mandatory green-cement procurement took effect, phasing in lower-clinker formulations for public projects.

- August 2024: Foster + Partners unveiled a 30 km² master plan for Hatay province quake reconstruction.

Turkey Construction Market Report Scope

The construction market includes a wide range of activities that cover upcoming, ongoing, and growing construction projects in different sectors, which include but are not limited to geotechnical (underground structures) and superstructures in residential, commercial, and industrial structures as well as infrastructure construction (like roads, railways, and airports) and power generation (transmission-related infrastructure). Construction is an industry that includes the erection, maintenance, and repair of buildings and other immobile structures and the building of roads and service facilities that become integral parts of structures and are essential to their use.

This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation and its impact, Porter's five forces analysis, and the impact of the COVID-19 pandemic on the market. In addition, the report also provides company profiles to understand the competitive landscape of the market.

The Turkish construction market is segmented by sector (residential, commercial, industrial, infrastructure (transportation), and energy and utilities). The report offers market size and forecasts for the Turkish construction market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Region

| Istanbul |

| Ankara |

| Izmir |

| Rest of Turkey |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Region | Istanbul | |

| Ankara | ||

| Izmir | ||

| Rest of Turkey | ||

Key Questions Answered in the Report

What is the 2026 value of the Turkey construction market?

The sector is valued at USD 183.02 billion in 2026, reflecting its post-earthquake reconstruction momentum.

How fast will Turkey’s construction sector grow through 2031?

It is forecast to post a 5.45% CAGR, climbing to USD 238.63 billion by 2031.

Which segment grows fastest within Turkish construction?

Infrastructure shows the steepest outlook with a projected 6.92% CAGR to 2031, fueled by highways and rail corridors.

Why is renovation gaining importance in Turkey?

Mandatory seismic retrofitting for 6.7 million buildings and energy-efficiency funding from the World Bank make renovation a rising strategic priority.

How do green-cement rules affect contractors?

Starting 2025 public tenders require low-clinker cement, compelling suppliers to invest in alternative binders and contractors to adjust mix designs.

What keeps Istanbul dominant despite regional diversification?

The city’s role as the financial and logistics hub, coupled with premium commercial and residential projects, sustains its 25.80% market share despite policy moves to spread growth.

Page last updated on: