Timing Belt Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

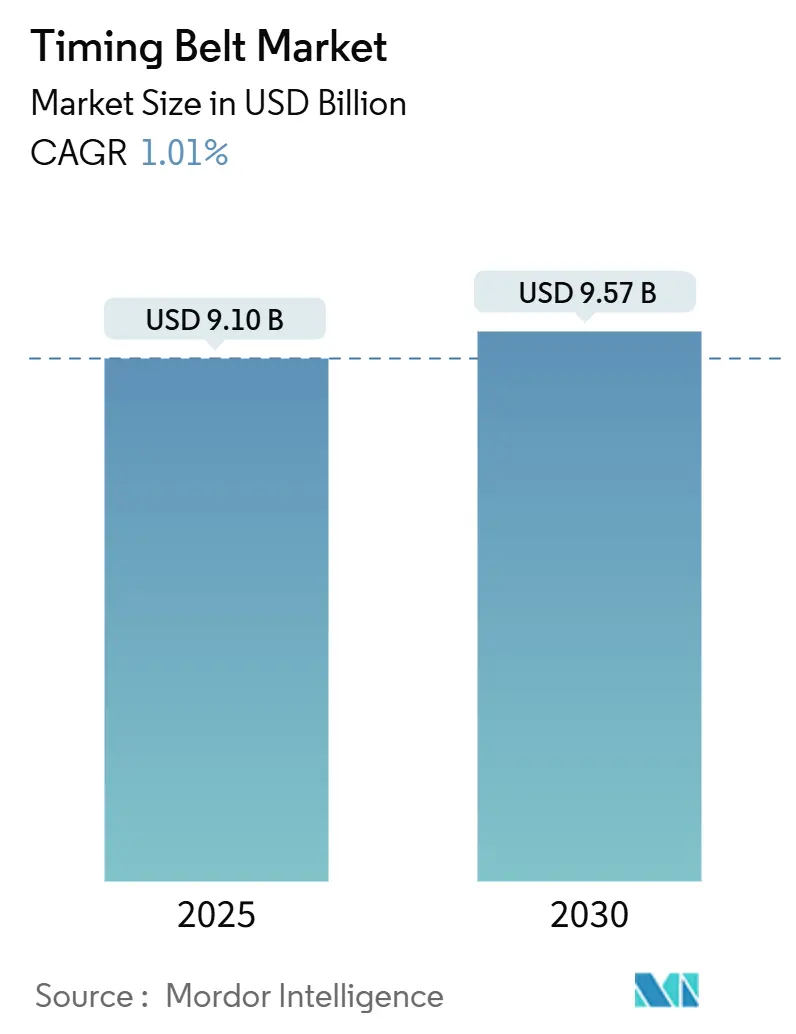

| Market Size (2025) | USD 9.10 Billion |

| Market Size (2030) | USD 9.57 Billion |

| Growth Rate (2025 - 2030) | 1.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Timing Belt Market Analysis by Mordor Intelligence

The timing belt market size stands at USD 9.10 billion in 2025 and is projected to reach USD 9.57 billion by 2030, translating into a 1.01% CAGR during the forecast period (2025-2030). As internal combustion volumes decline and hybrids, still reliant on mechanical valvetrain drives, gain traction, the timing belt market navigates a transitional phase, a nuance often overshadowed by the headline figures. Demand is shifting toward aramid- and carbon-cord constructions that permit 200,000-km service intervals, helping suppliers defend value even as unit volumes plateau. Asia-Pacific remains the anchor region thanks to high vehicle output in China and India, while Europe leans on premium belt-in-oil programs to meet Euro 7 durability rules. Medium and heavy commercial vehicles, which electrify more slowly than passenger cars, underpin replacement demand through the decade.

Key Report Takeaways

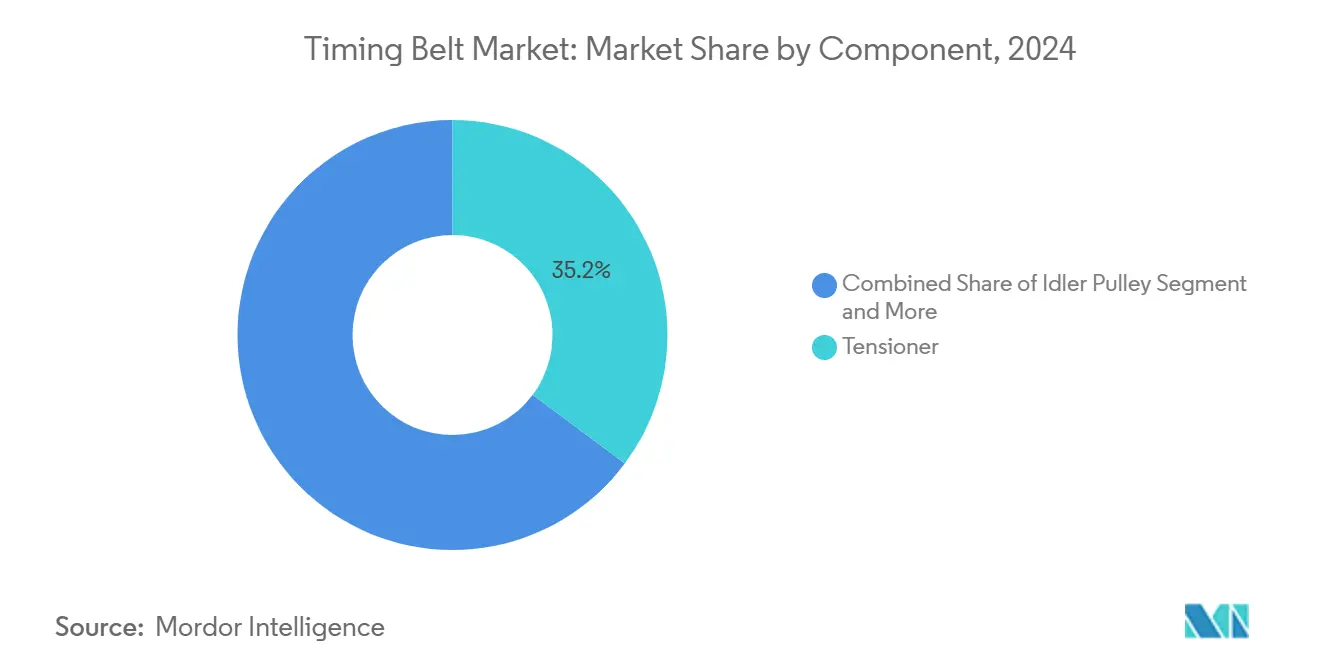

- By component, tensioners held a 35.18% share of the timing belt market in 2024, whereas timing shields and covers are expected to rise at a 1.46% CAGR during the forecast period (2025-2030).

- By drive type, dry belts accounted for a 62.11% share of the timing belt market in 2024, but belt-in-oil systems are expected to expanding at a 2.04% CAGR during the forecast period (2025-2030).

- By fuel type, gasoline applications commanded a 72.45% share of the timing belt market in 2024, while LPG/CNG installations are forecast to grow at a 2.33% CAGR during the forecast period (2025-2030).

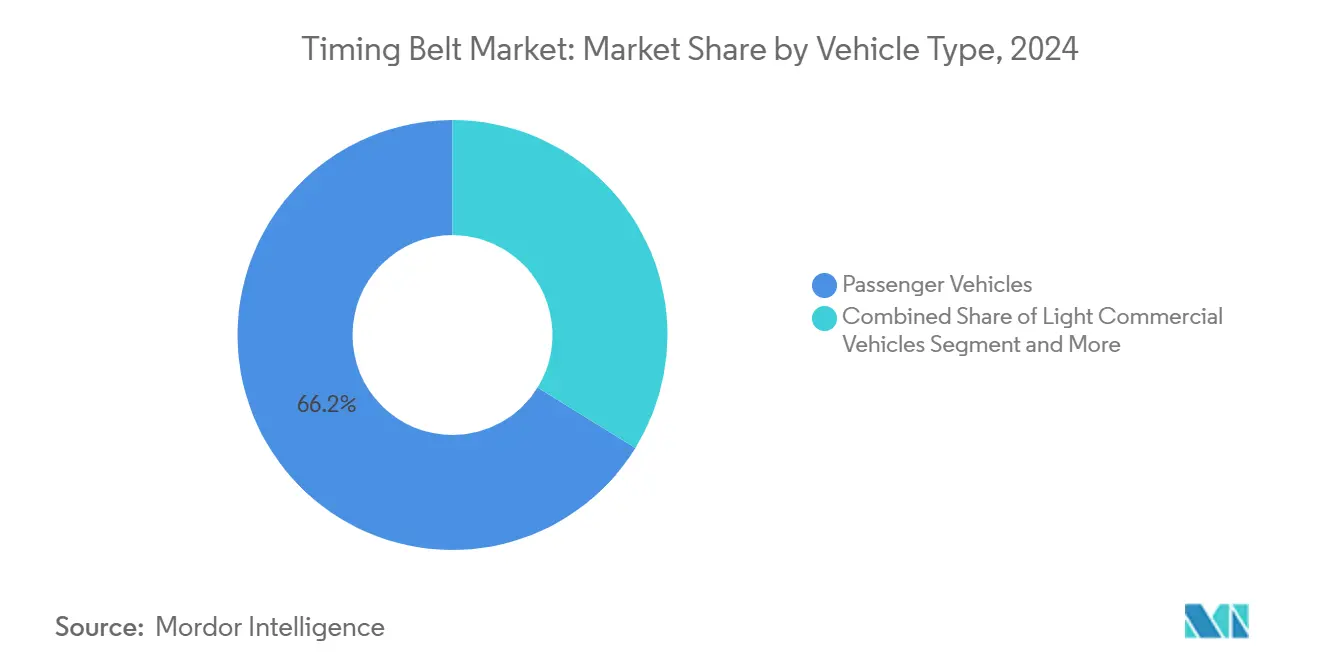

- By vehicle type, passenger vehicles contributed a 66.19% share of the timing belt market in 2024, medium and heavy commercial vehicles is forecat to grow at a 3.75% CAGR during the forecast period (2025-2030).

- By distribution channel, OEM supply streams captured a 57.05% share of the timing belt market in 2024, the aftermarket is expected to grow at a 3.12% CAGR during the forecast period (2025-2030), as vehicle age lengthens.

- By geography, Asia-Pacific contributed a 47.31% share of the timing belt market in 2024, Asia-Pacific is expected to rise with a 1.71% CAGR during the forecast period (2025-2030).

Global Timing Belt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Vehicle Parc | +0.3% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Rising Passenger-Car Production | +0.2% | China, India, Europe | Medium term (2-4 years) |

| Shift Toward Belt-In-Oil Systems | +0.1% | North America & EU premium brands | Medium term (2-4 years) |

| OEM Lightweighting for Stricter Norms | +0.1% | Global, led by EU Euro 7 rollout | Short term (≤ 2 years) |

| Adoption of Advanced Timing Belts | +0.1% | Global, premium and commercial segments | Medium term (2-4 years) |

| Timing Belts Retained in Hybrids | +0.1% | North America and EU during electrification transition | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Vehicle Parc

An expanding worldwide fleet sustains aftermarket demand even as new-car electrification gathers pace. Vehicle age in major markets now averages 12.2 years and is projected to exceed 14 years in the coming years, stretching replacement cycles that favor premium timing belts with extended life. Continental projects flat new-vehicle builds globally for 2025, yet Chinese output is still edging up, channeling more units into the long-run parc[1]“Automotive Outlook 2025,” Continental AG, continental.com. Older cars require multiple belt renewals across their lifetime, cushioning suppliers from ICE phase-out pressures. Asia-based producers with short lead times and export reach gain from this structural aftermarket uptick. The dynamic keeps the timing belt market resilient in revenue terms, even when pure-electric penetration accelerates.

Rising Passenger-Car Production in APAC and Europe

Production volumes in China, India, and Southeast Asia continue to support large-scale synchronous belt programs for both OEM and replacement lines. Local firms have broadened export coverage to Europe and the Americas, reinforcing supply-chain fluidity. In Europe, Euro 7 regulations extend mandated durability from five to eight years, compelling automakers to specify stronger, longer-life belts capable of 160,000 km duty cycles. Suppliers that can certify aramid or carbon reinforcement compliant with the new standard attract higher-margin orders. The twin-continent production trend, therefore, injects incremental volume and value into the timing belt market.

Shift Toward Belt-in-Oil Systems for NVH and Fuel-Efficiency Gains

Belt-in-oil drives, first proven on Ford’s 1.0-L EcoBoost, immerse the belt in engine oil to cut friction and noise. Gates offers PowerGrip Belt-in-Oil kits rated beyond 150,000 miles and formulated for oil compatibility [2]“PowerGrip Belt-in-Oil Technology,” Gates Corporation, gates.com. PSA, Volkswagen, and several Japanese brands now deploy similar architectures, widening the addressable base. Wet belts enable tighter engine packaging and can reduce CO₂ by around 1 g/km, supporting fleet-average targets without costly redesigns. Service complexity rises, but trained dealerships capture revenue from specialized oil and belt change kits. This switch boosts the premium mix inside the timing belt market.

OEM Lightweighting to Meet Stricter Emission Norms

Automakers face next-round emission caps that push every component toward lower mass. Suppliers respond with thinner tooth profiles, high-modulus cords, and abrasion-resistant elastomers such as PA46, lowering belt preload and friction. The European Commission’s Euro 7 protocol requires on-board monitoring over longer lifespans, so belts must hold tension under wider temperature cycles [3]“Euro 7 Proposal,” European Commission, ec.europa.eu. Weight-optimized synchronous belts support this agenda by shaving grams from the engine front end while also resisting elongation. Lightweighting, therefore, adds incremental but meaningful lift to the timing belt market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Powertrains Eliminate Timing Belts | -0.4% | EU and China lead, global spill-over | Long term (≥ 4 years) |

| EPDM/Neoprene Price Volatility | -0.2% | Global, rubber supply chain | Short term (≤ 2 years) |

| Return to Timing Chains | -0.1% | Global, performance and commercial | Medium term (2-4 years) |

| Lifetime Belts and Maintenance | -0.1% | North America and EU premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BEV Powertrains Eliminate ICE Timing Belts

Pure battery-electric vehicles remove cam-drive components entirely, erasing timing belt demand on those platforms. European BEV registrations reached a 14% share in 2024, and could rise further by 2030, displacing considerable aftermarket revenue. The effect is most acute in Western Europe and coastal China, where aggressive zero-emission mandates advance. Yet extended-range hybrids keep ICE generators on board, preserving belts in specific models until at least mid-decade. Suppliers hedge risk by investing in e-drive belts for two-wheeler micromobility and industrial applications, partially offsetting ICE attrition.

EPDM / Neoprene Price Volatility Squeezing Margins

Synthetic-rubber feedstock prices have swung wildly, pushing material costs up by double-digit percentages at times. Large suppliers can hedge or forward-buy, but smaller firms absorb margin compression. Continental’s rubber-based ContiTech unit cited raw-material inflation among reasons its 2024 EBIT margin slipped. Volatility also spills into reinforcement fibers such as aramid, tethering profit visibility and curbing cap-ex for new belt lines. Currency swings compound the challenge for exporters trading in multiple currencies, creating a persistent profitability headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Tensioners Anchor System Reliability

Tensioners commanded a 35.18% share of the timing belt market in 2024, underscoring their role in safeguarding precise belt tracking under thermal expansion. The sub-segment’s outlook stays positive because electrified hybrids still employ mechanical tensioners to cushion start-stop torque spikes. Suppliers are integrating damping and predictive-sensor modules, lifting average selling prices.

Timing Shield/Cover segment are expected to be the fastest mover at a 1.46% CAGR during the forecast period (2025-2030), as OEMs increasingly embrace the drive to bar contaminants and simplify acoustics validation. This shift also aligns with digital inspection tools that rely on transparent or easily removable covers for optical belt condition checks. Sprockets and idlers mature more slowly, yet they benefit from metallurgical upgrades that match the 200,000-km target life of premium belts. Collectively, these developments keep the timing belt market vibrant despite unit stagnation.

By Drive Type: Wet Belts Accelerate from Niche to Necessity

Dry synchronous belts still represented 62.11% share of the timing belt market in 2024,because they cost less and fit legacy engine designs. Even so, wet belt programs are widening beyond Ford to PSA’s PureTech and Volkswagen’s 1.5 TSI engines,expected to propels at a 2.04% CAGR during the forecast period (2025-2030). Wet configurations help cut oil-pump drag and suppress integer-order harmonics, key for premium cabin acoustics.

OEMs favor integrated packages that bundle oil pump and water-pump drives, lifting content per vehicle. Timing chains, though durable, add mass and friction, so compact three-cylinder engines continue the migration toward belt solutions. In emerging markets, maintaining familiarity with dry belts prevents a wholesale pivot, ensuring a blended portfolio for the timing belt industry.

By Fuel Type: Gasoline Retains Primacy, Alternative Fuels Gain

Gasoline engines delivered 72.45% share of the timing belt market in 2024, aided by stable demand in North America and Asia. Hybrids further embed gasoline ICEs, extending relevance through 2030. The timing belt market size linked to LPG and CNG vehicles is the smallest today, yet it expected to grow with a 2.33% CAGR during the forecast period (2025-2030), on the back of municipal fleet incentives in India and parts of South America.

Diesel declines in passenger cars, but remains critical for medium-duty trucks where duty cycles justify belt-driven camshafts over chains, thanks to lower NVH and weight benefits. Suppliers tailor tooth profiles and rubber blends to withstand higher combustion pressures in modern lean-burn gasoline engines, accentuating differentiation across fuel segments.

By Vehicle Type: Commercial Vehicles Lift Volume Growth

Passenger cars still occupied a 66.19% share of the timing belt market in 2024, reflecting sheer build numbers. However, the 3.75% CAGR during the forecast period (2025-2030), expected to booked by medium and heavy commercial vehicles outpaces every other vehicle class. Fleet operators appreciate longer service intervals and total-cost-of-ownership gains from premium belts that limit downtime.

Gates, for instance, has designed robust EPDM-based synchronous belts that can endure harsh conditions, including oil exposure and cold starts. The rise of e-commerce and its push for last-mile delivery have bolstered the durability and efficiency of light commercial vans. These vans frequently pair compact diesel engines with sophisticated belt-driven starter-generator systems, amplifying torque demands on the primary belt. Together, these advancements ensure timing belts maintain a diverse and stable presence across a range of vehicle types.

By Distribution Channel: Aftermarket Becomes Share Gainer

OEM supply routes captured a 57.05% share of the timing belt market in 2024, because belts are engineered alongside the engine’s cam phasing and NVH targets. Yet the aftermarket is projected to advance at a 3.12% CAGR during the forecast period (2025-2030), as vehicle age stretches and workshops adopt digital inspection routines. Modern EPDM constructions exhibit fewer visible cracks, compelling the use of laser wear gauges now offered in Gates service kits.

Independent repairers lean on kit bundles that include tensioners and seals, lifting invoice values. Regional discrepancies persist: Europe’s Block Exemption Rule secures independent access to repair data, while North America’s evolving right-to-repair legislation could unlock new growth for aftermarket specialists. Collectively, channel diversification supports overall timing belt market resilience.

Geography Analysis

Asia-Pacific held 47.31% share of the timing belt market in 2024, and is forecast to expand at a 1.71% CAGR during the forecast period (2025-2030). China remains the production epicenter, harnessing economies of scale and vertically integrated rubber supply chains that reduce cost volatility. India adds momentum through its BS VI-aligned gasoline and CNG car programs, each retaining mechanical belts for cam and balance-shaft drives. Local content mandates encourage belt makers to site factories near OEM hubs, insulating the region from freight disruptions.

Europe represents a mature yet technologically intense arena. The Euro 7 framework raises durability verification to 160,000 km, motivating automakers to adopt aramid-cord designs that maintain tension for longer intervals. Belt-in-oil conversions help luxury marques lower drivetrain noise, crucial amid the near-silent BEV driving experience they aim to emulate. BEV adoption nonetheless caps volume upside; several Western European assembly plants moved to chain-free electric platforms, trimming timing belt demand in first-fit but leaving a sizeable installed parc for replacement.

North America displays a mixed trajectory. Light-truck popularity sustains gasoline and hybrid V-6 engines that still rely on belts for auxiliary drives, even as federal incentives channel new investment toward EV manufacturing. Commercial trucking adheres to diesel for high-torque requirements, preserving meaningful belt content in medium-duty vocational vehicles. Canada’s harsh winters highlight belts capable of cold-start flexibility, an attribute chains lack without costly pre-heaters. Consequently, the region anchors a balanced share of the timing belt market, with the aftermarket capturing incremental growth on a mature vehicle base.

Competitive Landscape

The timing belt market shows moderate concentration. Continental’s decision to divest the ContiTech industrial unit refocuses its automotive portfolio on high-margin smart belt systems. Gates leverages proprietary rubber compounding and a global logistics network to retain leadership in both OE and replacement lines, expanding premium kits for wet-belt Ford Ecoboost variants. BorgWarner signed an agreement in February 2025 to supply variable cam-timing modules to an East Asian automaker, a deal that indirectly secures synchronous belt pull-through for hybrid engines starting in 2026.

Asian challengers use cost advantages and rising quality certifications to penetrate export markets, particularly in service parts. Compliance with ISO 21342:2019 and China’s GB/T 24619-2021 standards accelerates their accreditation pathway. Western incumbents defend territory through material science, such as carbon-cord belts rated for 245°C peak-under-bonnet exposure. Across all continents, suppliers invest in digital engineering twins and predictive wear diagnostics, responding to OEM requests for over-the-air maintenance alerts that can bundle replacement parts with dealer appointments.

Looking forward, strategic partnerships between belt producers and lubricant companies aim to co-develop oil-immersed formulations that minimize elastomer swelling. Collectively, these tactics signal a pivot from price to performance differentiation inside the timing belt industry.

Timing Belt Industry Leaders

Continental AG

Gates Corporation

Dayco LLC

Bando Chemical Industries, Ltd.

Mitsuboshi Belting Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: GSF Car Parts, the UK's fastest-growing motor factor, has bolstered its collaboration with BGA by introducing a new lineup of timing belt kits. GSF's inventory will encompass a broad selection, catering to 90% of the vehicle parc. Notably, nearly 50% of these kits come with a water pump, a component typically advised for simultaneous replacement to enhance reliability.

- February 2025: BorgWarner, bolstering its enduring alliance with a prominent East Asian OEM, is set to provide its cutting-edge Variable Cam Timing (VCT) technology. This VCT will be integrated into the automaker's newest hybrid and gasoline engines, with production slated to kick off in Q1 2026.

Global Timing Belt Market Report Scope

| Tensioner |

| Idler Pulley |

| Timing Shield / Cover |

| Sprocket |

| Dry Belts |

| Belt-in-Oil |

| Timing Chains |

| Gasoline |

| Diesel |

| LPG / CNG |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Tensioner | |

| Idler Pulley | ||

| Timing Shield / Cover | ||

| Sprocket | ||

| By Drive Type | Dry Belts | |

| Belt-in-Oil | ||

| Timing Chains | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| LPG / CNG | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the timing belt market in 2030?

The timing belt market is forecast to reach USD 9.57 billion by 2030 at a 1.01% CAGR.

Which component currently holds the largest share of global timing-belt revenue?

Tensioners lead with 35.18% of revenue due to their critical role in maintaining belt tension.

Why are belt-in-oil systems gaining popularity among automakers?

They reduce friction and noise, aiding fuel-efficiency targets; adoption drives a 2.04% CAGR within drive-type segmentation.

Which region is expected to post the fastest growth through 2030?

Asia-Pacific leads with a 1.71% CAGR, powered by robust vehicle production in China and India.

Page last updated on: