Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The Thailand Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

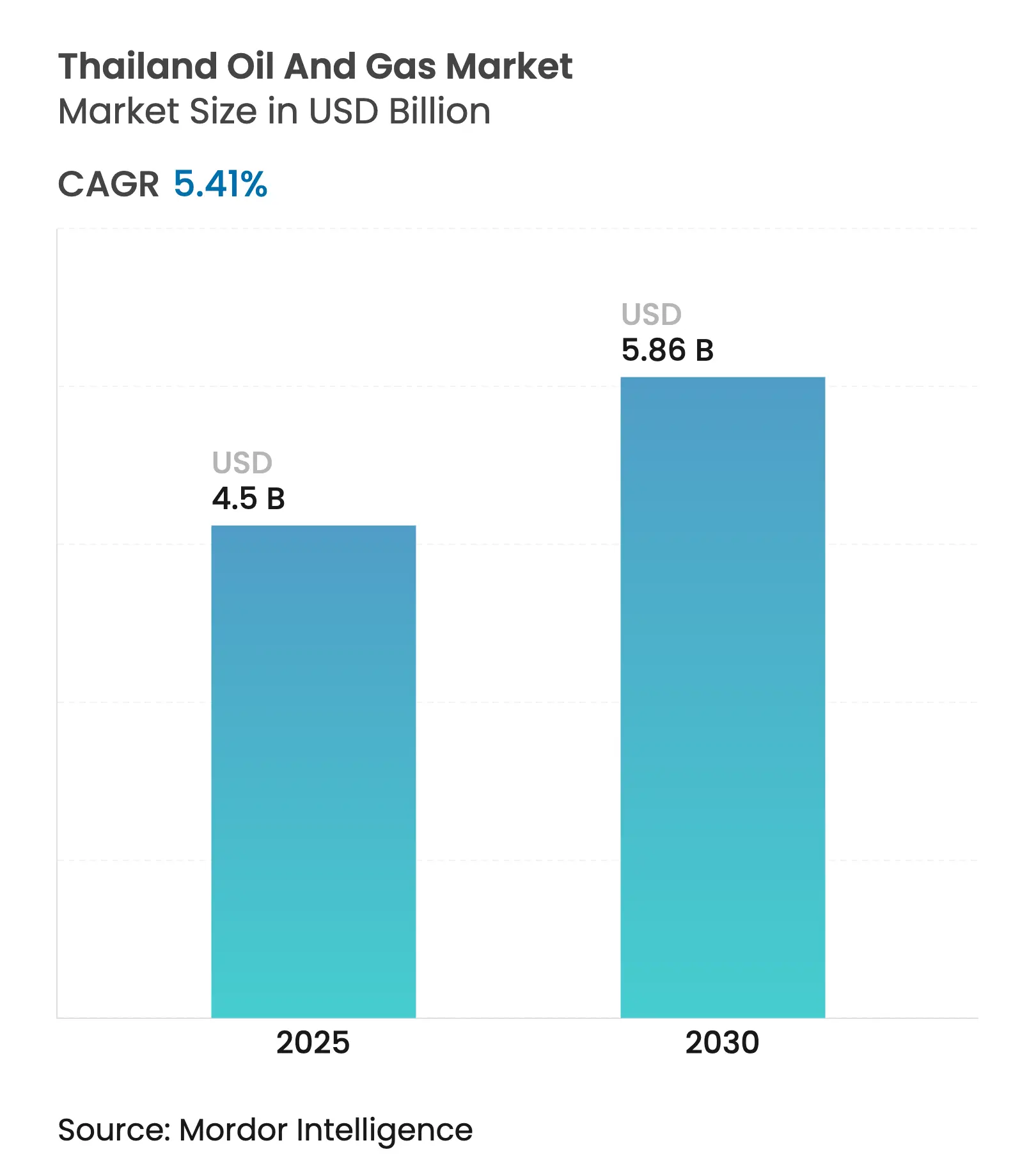

| Market Size (2025) | USD 4.5 Billion |

| Market Size (2030) | USD 5.86 Billion |

| Growth Rate (2025 - 2030) | 5.41 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

This growth stems from resilient domestic gas demand for power generation, rising petrochemical feedstock needs in the Eastern Economic Corridor, and continuous capital allocation to sustain production from mature offshore fields. The 25th petroleum bidding round further buoys robust upstream spending, accelerates LNG terminal development, and offers supportive fiscal terms that enhance project economics. Decommissioning activity and digital‐enabled maintenance remain bright spots, while fuel-price caps and emissions-related trade rules temper downstream profitability. Operators are therefore balancing cost discipline, carbon-reduction initiatives, and selective frontier exploration to safeguard energy security and corporate returns. Collectively, these dynamics keep the Thailand oil and gas market firmly on a mid-single-digit growth trajectory through the decade.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Robust

gas-fired power build-out boosting domestic demand

Robust

gas-fired power build-out boosting domestic demand

| +1.2% | National, with concentration in Central and Eastern regions | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:

+1.2%

|

Geographic

Relevance

:

National,

with concentration in Central and Eastern regions

|

Impact

Timeline

:

Medium

term (2-4 years)

|

New

Gulf of Thailand PSC licensing rounds opening acreage

New

Gulf of Thailand PSC licensing rounds opening acreage

| +1.0% | Gulf of Thailand offshore blocks, spill-over to adjacent maritime zones | Long term (≥ 4 years) | |||

Ongoing

downstream expansions at Map Ta Phut petro-complex

Ongoing

downstream expansions at Map Ta Phut petro-complex

| +0.8% | Rayong Province, with supply-chain effects across Thailand | Short term (≤ 2 years) | |||

LNG

regas capacity additions improving supply security

LNG

regas capacity additions improving supply security

| +0.6% | National distribution, anchored by Map Ta Phut and planned terminals | Medium term (2-4 years) | |||

Cross-border

OCA framework unlocking untapped reserves

Cross-border

OCA framework unlocking untapped reserves

| +0.4% | Thailand-Malaysia and Thailand-Cambodia border areas | Long term (≥ 4 years) | |||

CCS

retrofits extending life of mature offshore fields

CCS

retrofits extending life of mature offshore fields

| +0.3% | Gulf of Thailand mature fields, primarily Erawan and Bongkot complexes | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Robust Gas-Fired Power Build-Out Boosting Domestic Demand

EGAT’s current Power Development Plan calls for 15 GW of additional gas-fired capacity by 2030, a 40% step-up from 2024 levels.[1]EGAT, “Power Development Plan (PDP2024),” egat.co.th Long-term supply contracts between independent power producers and PTTEP underpin a stable offtake for new upstream projects. Demand is concentrated in the Eastern Economic Corridor, where power and petrochemical requirements overlap, ensuring minimum load factors for new plants. Pipeline expansions from the Gulf of Thailand to Chonburi and Rayong have therefore gained priority approvals. Consequently, upstream investors view the Thailand oil and gas market as insulated from near-term demand volatility, encouraging a healthy drilling program pipeline.

New Gulf of Thailand PSC Licensing Rounds Opening Acreage

The 25th bidding round, with nine onshore blocks and improved fiscal terms, marks the first licensing window since 2018. Royalty rates have been lowered by one percentage point for exploration phases, while local-content rules are relaxed until field development commences. This fiscal reset arrives as Brent prices hover above USD 80/bbl, lifting netbacks for frontier drilling. International majors have pre-qualified teams focusing on shallow-water gas prospects that could enter production before 2030. Successful awards would counterbalance a 5% annual decline in legacy fields and reinforce the Thailand oil and gas market’s upstream-led growth narrative.

Ongoing Downstream Expansions at Map Ta Phut Petro-Complex

PTTGC’s USD 1.2 billion ethane cracker expansion adds 1 million tpa of ethylene capacity by 2026, while Dow Chemical’s USD 800 million polyethylene unit strengthens value-chain integration.[2]PTT Global Chemical, “Ethane Cracker Expansion Fact Sheet,” pttgcgroup.com These projects increase domestic demand for NGL and lean gas, providing a back-of-the-envelope level of offtake security for Gulf of Thailand gas producers. The complex’s adjacency to deep-water berths lowers export logistics costs, enhancing Thailand’s regional competitiveness. New storage, such as Vopak’s 60,000 m³ ethane tank, improves feedstock optionality and supports turn-key contract opportunities for midstream players. Collectively, these assets anchor downstream profitability despite national pump-price controls.

LNG Regas Capacity Additions Improving Supply Security

The 7.5 mtpa Nong Fab terminal entered service in 2024, granting Thailand access to global spot LNG and mitigating pipeline supply risks from Myanmar. A 5 mtpa third terminal in Chonburi is undergoing FEED review, with a target FID by late 2025. Regas capacity raises system flexibility, enabling seasonal import arbitrage and safeguarding power plants during upstream maintenance shutdowns. Thailand also eyes re-export opportunities via interconnected pipelines to Laos and Cambodia, potentially creating an ASEAN trading hub. These moves enhance the resilience of the Thailand oil and gas market while widening revenue pools along the gas value chain.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid

decline of legacy fields (Erawan, Bongkot)

Rapid

decline of legacy fields (Erawan, Bongkot)

| -1.1% | Gulf of Thailand offshore, particularly central and southern blocks | Short term (≤ 2 years) | (~) %

Impact on CAGR Forecast:

-1.1%

|

Geographic

Relevance

:

Gulf of

Thailand offshore, particularly central and southern blocks

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Domestic

fuel-price caps squeezing refinery margins

Domestic

fuel-price caps squeezing refinery margins

| -0.4% | National, with acute impact on major refineries in Rayong and Chonburi | Short term (≤ 2 years) | |||

Carbon-intensity

scrutiny under EU CBAM on refined exports

Carbon-intensity

scrutiny under EU CBAM on refined exports

| -0.3% | Export-oriented refineries, primarily affecting EU trade routes | Medium term (2-4 years) | |||

Environmental

activism delaying pipeline right-of-way

Environmental

activism delaying pipeline right-of-way

| -0.2% | Rural and coastal areas, particularly sensitive ecological zones | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Decline of Legacy Fields (Erawan, Bongkot)

Output from Erawan, once 25% of the national gas supply, is declining 15% per year due to a drop in reservoir pressure and rising water cut.[3]PTTEP, “Field Decline Management Report,” pttep.com Bongkot shows parallel exhaustion trends, despite secondary recovery schemes. Chevron has allocated USD 2 billion for infill drilling, but geological limits cap incremental gains. The shortfall forces higher LNG imports, which squeeze the balance of payments and elevate power tariffs. Urgent replacement barrels and molecules therefore dominate operator capital budgets in the Thailand oil and gas market, crowding out discretionary exploration spend elsewhere.

Carbon-Intensity Scrutiny Under EU CBAM on Refined Exports

The EU’s Carbon Border Adjustment Mechanism enters its monitoring phase in 2026, exposing Thai refiners shipping diesel and jet fuel to Europe to prospective carbon tariffs. Bangchak has begun ISO 14001 deployments, yet full Scope-1 emission cuts require multi-year furnace upgrades and renewable power PPAs. Added compliance costs could erode netbacks by USD 1/bbl for European-bound cargoes, thereby challenging the expansion economics of export-oriented capacity. This policy headwind nudges refiners toward higher-value petrochemicals and Asian demand centers, reshaping downstream flow patterns within the Thailand oil and gas market.

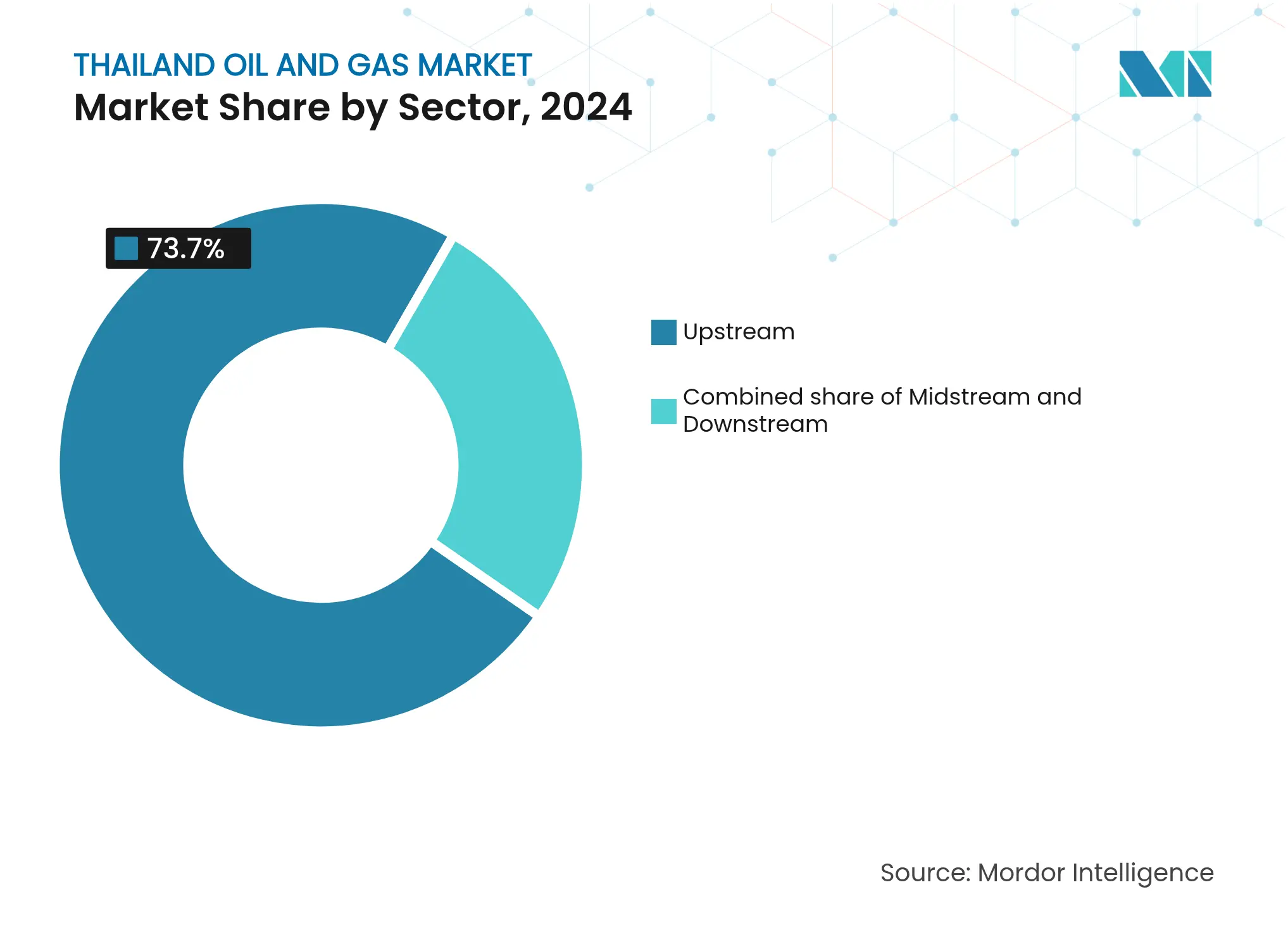

By Sector: Upstream Dominance Drives Market Growth

Upstream activities captured 73.7% of the Thai oil and gas market share in 2024, reflecting heavy capital expenditure (capex) to offset natural decline and bring discoveries onstream.[4]PTTME, “Offshore Maintenance Portfolio,” pttme.co.th The segment is projected to post a 5.7% CAGR to 2030, outpacing midstream and downstream segments due to multi-well drilling campaigns, platform refurbishments, and early CCS pilots. The Thailand oil and gas market size attributed to the upstream sector stood at USD 3.3 billion in 2025, with PTTEP, Chevron, and TotalEnergies leading the investment. DigitalX workflow adoption has reduced unplanned downtime by 85%, resulting in higher asset uptime and lower lifting costs.

Midstream, while smaller, benefits from LNG terminal build-outs, new gas processing trains, and cross-border pipelines. Processing capacity additions at onshore gas plants preserve condensate quality, enabling premium pricing. Downstream faces margin compression due to regulated pump prices, yet receives structural support from the Eastern Economic Corridor’s petrochemical boom. As fuel subsidies unwind after 2026, refining utilization is expected to recover modestly, aided by increased export demand to Cambodia and Laos.

Note: Segment shares of all individual segments available upon report purchase

By Service: Maintenance Leadership Amid Decommissioning Surge

Maintenance and turnaround accounted for 48.3% of 2024 service revenue, as 450 offshore platforms require periodic inspections, valve overhauls, and topsides integrity checks. Aging jackets in the Gulf necessitate high scaffolding hours and subsea cathodic protection, validating the need for long-term framework contracts with providers such as PTTEP Energy Service. Decommissioning, though only 7% of 2024 revenue, is set for a 7.5 % CAGR, driven by Chevron’s 49-platform retirement campaign and Centurion’s 250 km pipeline plug-and-abandon scope. The Thailand oil and gas market size for decommissioning is forecast to touch USD 420 million by 2030, with high engineering barriers offering attractive margins.

Construction services occupy the middle ground, buoyed by LNG jetty builds and onshore compressor station upgrades. EPC contractors are embedding digital twin models to compress schedule risk and improve safety compliance. Service providers that combine asset integrity expertise with end-of-life removal solutions are well-positioned to secure bundled contracts as operators seek one-stop solutions for mature assets.

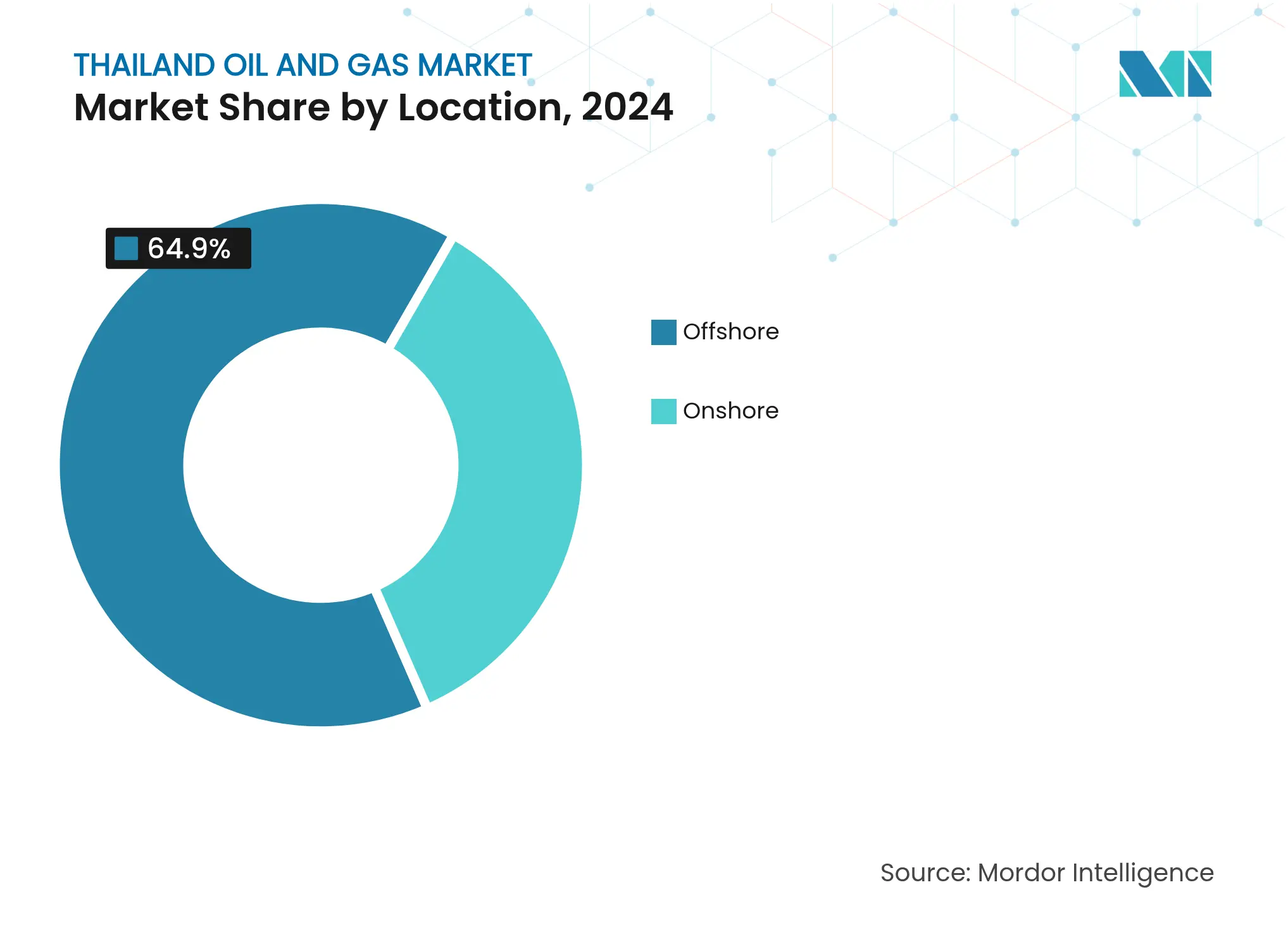

By Location: Offshore Concentration Reflects Resource Geography

Offshore output represented 64.9% of Thailand's oil and gas market size in 2024 and is forecast to grow 6.2% annually amid the intensive redevelopment of shallow-water blocks. Fixed-platform economics remain viable for water depths of 20–80 m and short tieback distances to onshore gas plants. Erawan, Arthit, and Bongkot alone host over 200 wellhead platforms, generating steady demand for marine logistics, drilling, and brownfield modifications.

Onshore, while holding a modest share, still appeals to independents, thanks to lower OPEX and easier land access. The current bidding round's nine blocks could surface small but quick-to-market finds that complement the national supply mix. Frontier areas in the Northern basins are being remapped using high-resolution 3D seismic data that was previously unavailable. Nonetheless, offshore will likely retain dominance given its remaining prospective resource base and existing infrastructure grid.

Note: Segment shares of all individual segments available upon report purchase

Thailand’s oil and gas activities are concentrated in the Gulf of Thailand and the Eastern Economic Corridor, where 80% of proven reserves and 60% of refining capacity are located. Rayong Province hosts Map Ta Phut, the hub for LNG imports, ethane cracking, and bulk chemical exports. Chonburi complements with tank farms and a forthcoming 5 mtpa regas terminal, reinforcing coastal supply resilience.

Power and industrial demand concentrate around Bangkok and Pathum Thani, creating a steady sink for pipeline gas delivered via the onshore trunk grid. Northern provinces, although resource-light, serve as distribution nodes for refined products transported by pipeline and road to Laos and Myanmar. In the south, Songkhla supports offshore logistics, while pipeline links to Malaysia facilitate cross-border swap arrangements.

Joint development of overlapping claims with Cambodia and Malaysia may unlock 11 trillion cubic feet (tcf) of gas and 300 million barrels (bbl) of liquids, although diplomatic negotiations extend the timelines beyond 2028. Successful framework agreements would diversify supply and defer LNG import dependence. The Thailand oil and gas market, therefore, benefits from both domestic clustering efficiencies and emerging regional integration pathways.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

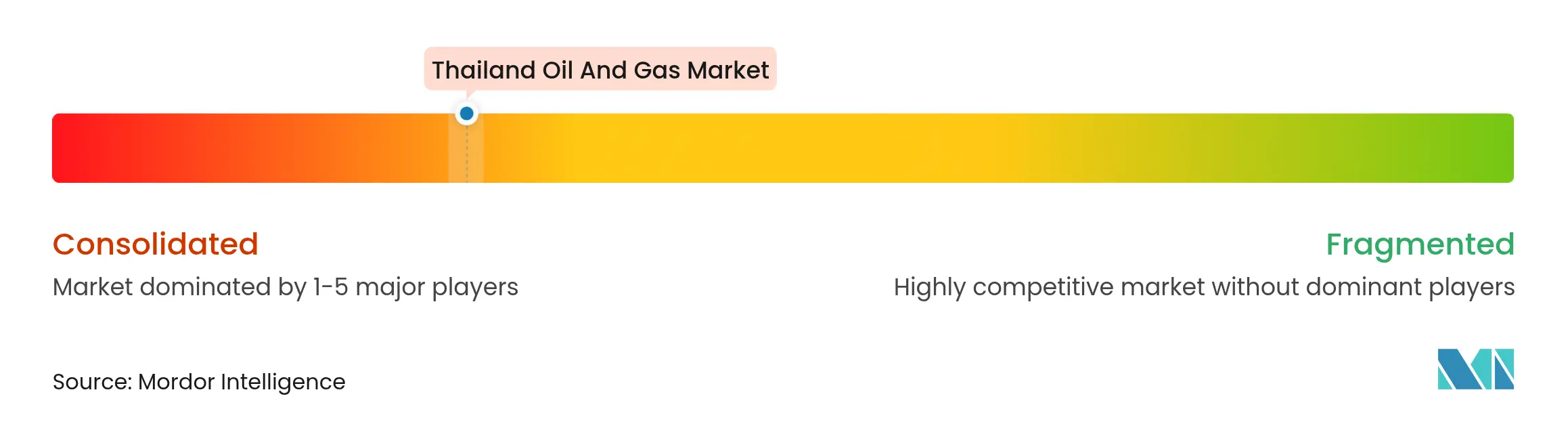

Market Concentration

The Thai oil and gas market features moderate concentration. PTTEP controls roughly 35 % of upstream volumes, leveraging state backing and extensive acreage. Chevron, TotalEnergies, and ExxonMobil combine their global deepwater expertise with local partnerships to maintain sizable market shares. The top five operators collectively own approximately 72% of production, indicating a moderately consolidated structure.

Competitive focus areas include cost-effective redevelopment of mature fields, digital field enablement, and low-carbon solutions. PTTEP’s DigitalX program cut bid-cycle times by 92%, improving supplier engagement. Chevron’s pending CCS tie-in trial at Bongkot signals early adoption of decarbonization levers that could shape license extensions. In services, James Fisher, Centurion, and local players such as PTTME compete on engineering depth and safety track records for complex decommissioning scopes. Niche digital analytics firms enter the market with AI-based reservoir models, offering operators incremental recovery at sub-$2/boe unit costs.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

The oil and natural gas market is a major industry in the energy market and plays an influential role in the global economy as the world's primary fuel source. The processes and systems involved in producing and distributing oil and gas are highly complex, capital-intensive, and require state-of-the-art technology.

The Thailand oil and gas market is segmented by sector. The market is segmented by sector into upstream, midstream, and downstream. The market sizing and forecasts have been done based on volume.

Unlocking Market Potential for Solid-State Transformers

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.