Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

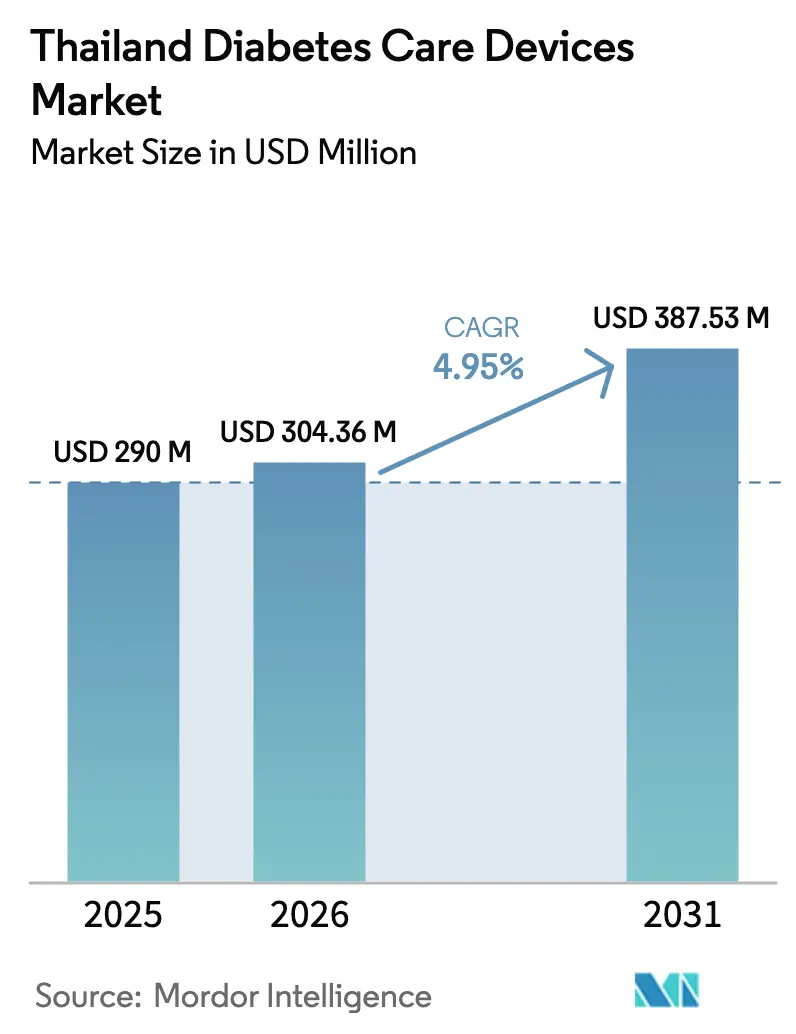

| Base Year Market Size (2025) | USD 290 Million |

| Market Size (2026) | USD 304.36 Million |

| Market Size (2031) | USD 387.53 Million |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Diabetes Care Devices Market Analysis by Mordor Intelligence

The Thailand diabetes care devices market size is expected to grow from USD 290 million in 2025 to USD 304.36 million in 2026 and is forecast to reach USD 387.53 million by 2031 at 4.95% CAGR over 2026-2031. The expansion is underpinned by widening public reimbursement, rising prevalence of Type 2 diabetes, and ongoing consumer migration from test-strip–based monitoring to continuous glucose monitoring (CGM). Multinational suppliers maintain a strong foothold in premium segments, yet Thailand 4.0 incentives are drawing domestic firms into mid-tier product niches, gradually reducing import reliance. Digital-health pilots inside the government’s “Digital Health Sandbox” are accelerating telemonitoring adoption, especially in urban centers where smartphone penetration is highest. Persistent urban–rural disparities, limited diabetes-education capacity outside Bangkok, and currency-driven pricing volatility temper the near-term growth outlook.

Key Report Takeaways

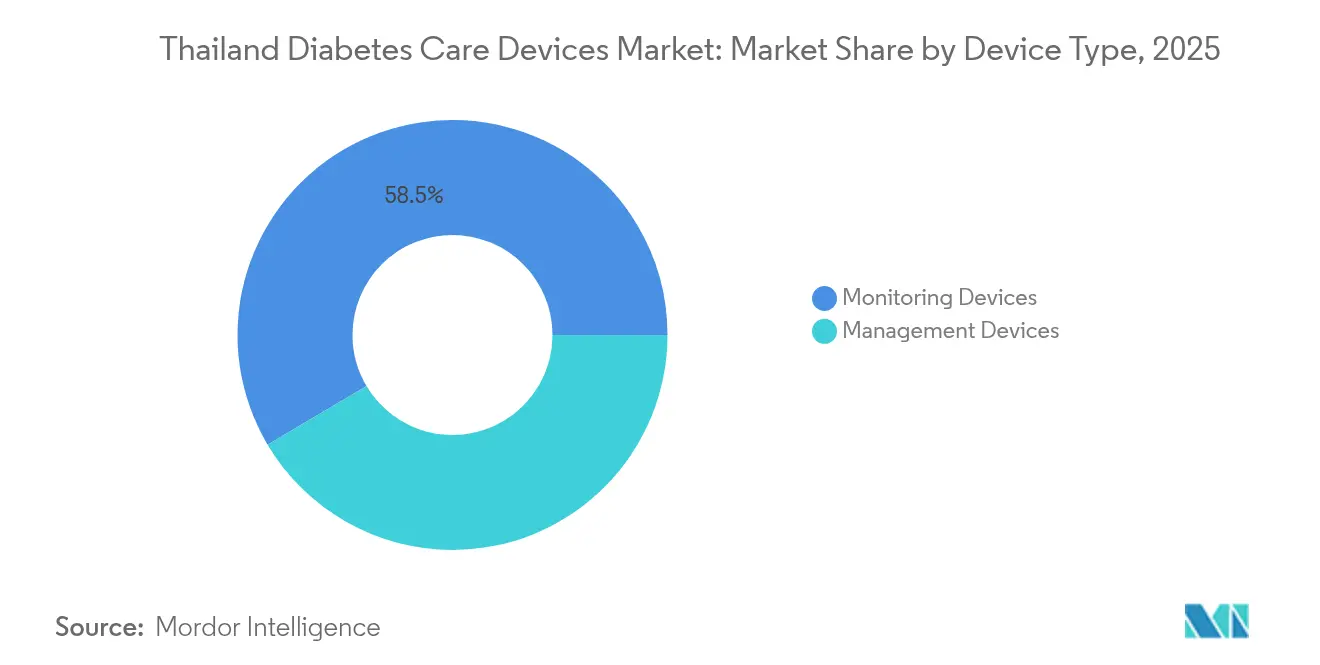

- By device type, monitoring devices led with 58.52% of Thailand diabetes care devices market share in 2025; management devices are projected to register the fastest 7.01% CAGR through 2031 .

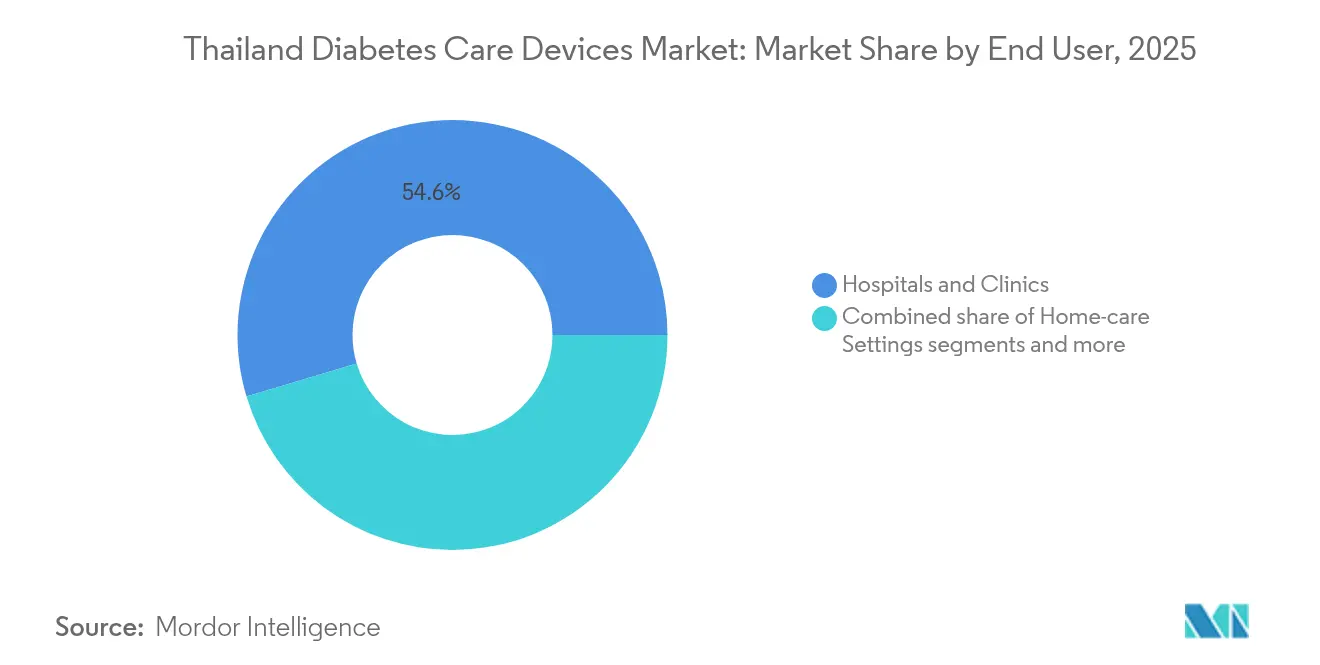

- By end-user setting, hospitals and clinics captured 54.62% of the Thailand diabetes care devices market size in 2025 while home-care settings are expanding at a 7.78% CAGR to 2031 .

- By diabetes type, Type 2 patients accounted for 87.05% of the Thailand diabetes care devices market size in 2025 and continue to underwrite long-run demand momentum.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Diabetes Care Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Diabetes and Pre-diabetes in Thailand's Working-age Population | +1.8% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Universal Coverage Scheme Expansion Increasing Device Reimbursement | +1.2% | National, with emphasis on rural areas | Medium term (2-4 years) |

| Rapid Uptake of CGM Sensors Among Tech-savvy Urban Consumers | +0.9% | Urban centers, particularly Bangkok | Short term (≤ 2 years) |

| Government-led "Digital Health Sandbox" Encouraging Remote Glucose Monitoring | +0.7% | National, with initial focus on urban centers | Medium term (2-4 years) |

| Local Manufacturing Incentives Under Thailand 4.0 Lowering Device Costs | +0.5% | Industrial zones near Bangkok | Medium term (2-4 years) |

| Private Hospital Chains' Chronic-care Programs Boosting Insulin Pump Demand | +0.4% | Urban centers and medical tourism hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Diabetes and Pre-diabetes in Thailand

Roughly 11.6% of Thai adults—nearly 5 million people—live with Type 2 diabetes, and annual incident cases exceed 300,000, creating a sizable pipeline of patients who require long-term device-based management. Demand spans both monitoring and insulin-delivery categories as complications tied to poor glycemic control place new pressure on Thailand’s Universal Coverage Scheme (UCS). Government-backed screening campaigns are gaining traction among seniors, but working-age adults now account for an increasingly high share of new diagnoses, pushing employers to include CGM as an employee-benefit add-on. Urbanization, ultra-processed diets, and sedentary lifestyles remain primary disease drivers. As prevalence rises, device makers are tailoring educational programs to improve self-management and extend sensor usage life, thereby strengthening patient retention. These trends collectively support steady expansion of the Thailand diabetes care devices market across all price tiers.

Universal Coverage Scheme Expansion Increasing Device Reimbursement

The UCS now insures 47.2 million residents, including 4.27 million individuals with diabetes, and its benefits package has recently been expanded to cover CGM sensors, smart glucometers, and select insulin pens. Reimbursement lowers out-of-pocket costs for middle-income Thais, driving unit sales volume even in price-sensitive provinces. Funding flexibility—stemming from Thailand’s tax-based healthcare financing—allows timely inclusion of new diabetes technologies judged cost-effective in preventing expensive complications. Device suppliers are aligning product-registration schedules with the National List of Essential Medicines review cycle to secure faster market access. As more patients transition to reimbursed home-monitoring regimens, refill purchases of test strips, sensors, and lancets rise, reinforcing recurring-revenue streams. This policy evolution is therefore a structural demand catalyst for the Thailand diabetes care devices market.

Rapid Uptake of CGM Sensors Among Urban Consumers

CGM systems are moving from niche to mainstream in Bangkok, Chiang Mai, and Pattaya, propelled by tech-savvy consumers seeking real-time glucose insights. Clinical studies in Thailand show mean HbA1c improvements of 0.87% when CGM is embedded in digital-coaching programs versus standard self-monitoring. Manufacturers have responded by debuting 14-day sensors with smartphone pairing and subscription models that bundle data analytics. Pharmacies have begun stocking starter kits, and insurers now market CGM-linked wellness packages to office workers. Teleconsult platforms integrate CGM dashboards, allowing endocrinologists to adjust insulin doses remotely, which fits the congested urban-clinic environment. Continued price erosion—enabled by local assembly of consumables—should broaden adoption into middle-income cohorts, supporting a higher-than-average growth arc inside the Thailand diabetes care devices market.

Government-Led “Digital Health Sandbox” Encouraging Remote Glucose Monitoring

Thailand’s Digital Health Sandbox fast-tracks pilot rollout of connected diabetes solutions by granting conditional approvals before full Thai FDA certification. This regulatory predictability shortens time-to-market for startups integrating CGM, artificial-intelligence algorithms, and medication-tracking apps. Sandbox status also unlocks corporate-income-tax incentives and dedicated 5G testing zones in major hospitals. Pilot data feed directly into update cycles for the national eHealth strategy (2017-2026), ensuring reimbursement pathways evolve in parallel with technological progress. Early successes—such as the Steno Detektor telemonitoring platform—demonstrate improved glycemic metrics and reduced clinic visits, reinforcing policy momentum. As more solutions graduate from the sandbox, the Thailand diabetes care devices market gains a broader portfolio of locally tailored offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Costs for Advanced Insulin Pumps | -0.8% | National, with higher impact in rural areas | Medium term (2-4 years) |

| Limited Trained Diabetes Educators Outside Bangkok | -0.6% | Rural areas and provincial cities | Medium term (2-4 years) |

| Import Dependency Causing Supply Vulnerability During Baht Volatility | -0.4% | National | Short term (≤ 2 years) |

| Cultural Resistance to Needle-based Self-Injection in Elderly Patients | -0.3% | Rural areas and traditional communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Trained Diabetes Educators Outside Bangkok

Only 26.7% of Thai Type 2 diabetes patients achieve adequate glycemic control, well below the Ministry of Public Health’s 40% target, with inadequate self-management education identified as a major gap. Provincial and rural hospitals contend with a shortage of certified diabetes educators, leading to inconsistent training on device usage and suboptimal treatment adherence. The Northeast records an unmet-need rate of 78% versus 58.4% in the South, reflecting stark regional disparities. Patients who do obtain advanced devices often lack follow-up counseling, reducing long-run sensor and pump retention rates. Manufacturers are piloting hybrid tele-education programs, yet bandwidth limitations outside major cities slow roll-out. Unless educator capacity broadens, the Thailand diabetes care devices market will struggle to unlock its full growth potential beyond Bangkok.

Import Dependency Causing Supply Vulnerability During Baht Volatility

Advanced devices such as CGM transmitters, insulin pumps, and automated dosing algorithms depend on imported electronics and pharmaceutical-grade polymers. A sudden 5% Baht depreciation against the USD can raise landed costs enough to trigger unplanned retail price hikes and procurement delays. Distributors hedge by carrying extra inventory, yet this ties up working capital and raises obsolescence risk when next-generation models arrive. Hospitals reliant on capped public-procurement budgets occasionally postpone tenders, forcing patients back to older self-monitoring techniques. Domestic production capabilities remain concentrated in basic consumables, so the supply chain for sophisticated hardware will remain exposed for several years. This currency sensitivity moderates the headline growth trajectory of the Thailand diabetes care devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Devices Maintain Leadership While Management Devices Accelerate

Monitoring devices generated USD 0.17 billion in 2025, equal to 58.52% of the Thailand diabetes care devices market size, as finger-stick glucometers and CGM sensors form the backbone of daily diabetes care . Hospitals standardize procurement around trusted monitoring brands, and home users appreciate the familiarity of portable readers. However, a noticeable shift toward sensor-based systems is compressing test-strip margins, encouraging incumbents to bundle analytics subscriptions with hardware to stabilize revenue.

Management devices, chiefly insulin pumps and smart pens, accounted for USD 0.12 billion in 2025 and are projected to grow at 7.01% CAGR. The double-digit adoption of hybrid closed-loop systems in Bangkok’s tertiary centers demonstrates strong latent demand for automation. Price declines, fueled by Thailand 4.0 import-duty waivers on components, are narrowing the affordability gap. Leading global players have begun local algorithm customization to reflect Thai dietary glycemic loads, positioning management devices as the fastest-growing segment in the Thailand diabetes care devices market.

By Diabetes Type: Type 2 Segment Drives Long-Term Demand

Type 2 diabetes represents 87.05% of total diagnosed cases and underpins the bulk of recurrent device consumption. The segment’s high prevalence among working-age adults ensures continuous annual inflows of first-time device users. CGM adoption resonates with Type 2 patients managing diet and exercise regimens, elevating sensor turnover.

Type 1 patients, though numerically smaller, exhibit higher per-capita device spend due to pump therapy and frequent sensor replacement. Many Bangkok specialists now initiate Type 1 adolescents directly on hybrid closed-loop systems, pushing management-device revenue density well above the Type 2 peer group. The combined dynamics keep the Thailand diabetes care devices market diversified across patient profiles.

By End-User Setting: Hospitals Dominate but Home-Care Uptake Outpaces

Hospitals and clinics absorbed 54.62% of Thailand diabetes care devices market share in 2025 due to centralized procurement under the UCS and private insurance networks . In-clinic monitoring remains essential for newly diagnosed cases and for complications screening. Public hospitals leverage bulk-purchase agreements that include training modules, ensuring steady device throughput even in budget-tight quarters.

Home-care settings, though smaller in absolute terms, are advancing at 7.78% CAGR. Sensor-phone pairing technologies and rising smartphone ownership make self-monitoring increasingly convenient, reducing travel burdens for rural patients. The “30 Baht Treat Anywhere” extension allows device refills at any contracted pharmacy, further incentivizing home-based management. As remote-consult platforms embed AI triage, home-care is expected to claim a larger slice of the Thailand diabetes care devices market size by decade-end.

Geography Analysis

Bangkok accounts for an about half of national device sales value, driven by high household incomes, tertiary care institutions, and medical-tourism inflows. Urban patients readily adopt CGM subscriptions, and private insurers subsidize advanced pumps to differentiate benefit packages. Chiang Mai and Chonburi together add a further 17.60% share, reflecting their roles as regional referral hubs. In these provinces, wholesalers maintain cold-chain logistics enabling same-day fulfillment of sensor orders.

The Northeast, despite hosting the highest patient population, captures only 11.40% of Thailand diabetes care devices market size because of lower purchasing power and limited endocrinology coverage. However, the Ministry of Public Health’s THB 275 billion Diabetes Digital Care Initiative is earmarking funds to equip provincial hospitals with cloud-linked glucometers, potentially narrowing the access gap. Southern provinces such as Phuket and Songkhla show above-average penetration of home-care devices thanks to expatriate and medical-tourist demand. Pharmacies in these coastal cities stock imported CGM brands that appeal to visitors seeking short-term monitoring solutions. Collectively, geographic variances imply that successful suppliers tailor channel strategies by province, reinforcing the heterogeneous landscape of the Thailand diabetes care devices market.

Competitive Landscape

Abbott, Medtronic, and Roche collectively account for an estimated half of device revenue, anchoring premium CGM and insulin-delivery niches. Abbott’s 2025 Bangkok launch of FreeStyle Libre 3, featuring a 14-day sensor, accelerates the firm’s penetration in self-funded urban segments. Medtronic’s MiniMed 780G system integrates Meal Detection algorithms tailored for Thai cuisine, illustrating product-localization as a competitive lever. Roche’s acquisition of Carmot Therapeutics expands its pipeline of glucose-responsive therapies, foreshadowing device-drug combination offerings that could fortify brand stickiness.

Domestic entrants—backed by Thailand 4.0 fiscal incentives—are scaling assembly lines for mid-range glucometers and consumables. Thai Otsuka’s Ayutthaya plant already manufactures strips and lancets at 30% lower landed cost than imports, allowing aggressive retail pricing in rural pharmacies [BOI.GO.TH]. Start-ups such as SIBIONICS leverage partnerships with nationwide pharmacy chains to distribute CGM kits, signalling a pivot toward mass-market retail channels.

Strategic alliances round out competition. Pacific Prime’s telerehab tie-up with HelpDeliver embeds device-sourced data into virtual consults, differentiating insurer offerings. Meanwhile, Danish-Thai collaborations introduce community-based screening models that bundle government funding with private technology, broadening market access. The net effect is intensifying rivalry across both high- and mid-value tiers of the Thailand diabetes care devices market.

Thailand Diabetes Care Devices Industry Leaders

Medtronic

F. Hoffmann-La Roche AG

Novo Nordisk

Abbott Diabetes Care

Dexcom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The NHSO expanded the “30 Baht Treat Anywhere” program to include additional diabetes monitoring devices.

- January 2025: The Thai Ministry of Public Health launched the Diabetes Digital Care Initiative, allocating THB 275 billion (USD 7.8 billion) to expand chronic-disease technology access nationwide

Thailand Diabetes Care Devices Market Report Scope

The tools used in diabetes care are used to measure the body's blood sugar levels resulting from insulin synthesis. Patients with diabetes are given these care tools to monitor their blood glucose levels and better manage their chronic illnesses. Thailand Diabetes Care Devices Market is segmented into devices and Monitoring Devices. The report offers the value (in USD) and volume (in Units) for the above segments.

By Device Type

| Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring | Sensors | |

| Durables | ||

| Management Devices | Insulin Pumps | Insulin Pump Device |

| Insulin Pump Reservoir | ||

| Infusion Set | ||

| Insulin Syringes | ||

| Insulin Pens | ||

| Jet Injectors | ||

By Patient Type

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational & Others |

By End-user

| Hospitals & Clinics |

| Home-care Settings |

| Ambulatory Surgical Centres |

| Pharmacies & Retail Chains |

| By Device Type | Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | |||

| Lancets | |||

| Continuous Glucose Monitoring | Sensors | ||

| Durables | |||

| Management Devices | Insulin Pumps | Insulin Pump Device | |

| Insulin Pump Reservoir | |||

| Infusion Set | |||

| Insulin Syringes | |||

| Insulin Pens | |||

| Jet Injectors | |||

| By Patient Type | Type-1 Diabetes | ||

| Type-2 Diabetes | |||

| Gestational & Others | |||

| By End-user | Hospitals & Clinics | ||

| Home-care Settings | |||

| Ambulatory Surgical Centres | |||

| Pharmacies & Retail Chains | |||

Key Questions Answered in the Report

How big is the Thailand Diabetes Care Devices Market?

The Thailand Diabetes Care Devices Market size is expected to reach USD 304.36 million in 2026 and grow at a CAGR of 4.95% to reach USD 387.53 million by 2031.

What is the current Thailand Diabetes Care Devices Market size?

In 2026, the Thailand Diabetes Care Devices Market size is expected to reach USD 304.36 million.

Who are the key players in Thailand Diabetes Care Devices Market?

Medtronic, F. Hoffmann-La Roche AG, Novo Nordisk, Abbott Diabetes Care and Dexcom are the major companies operating in the Thailand Diabetes Care Devices Market.

What years does this Thailand Diabetes Care Devices Market cover, and what was the market size in 2025?

In 2025, the Thailand Diabetes Care Devices Market size was estimated at USD 290 million. The report covers the Thailand Diabetes Care Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Thailand Diabetes Care Devices Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: