Terrain Awareness And Warning System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

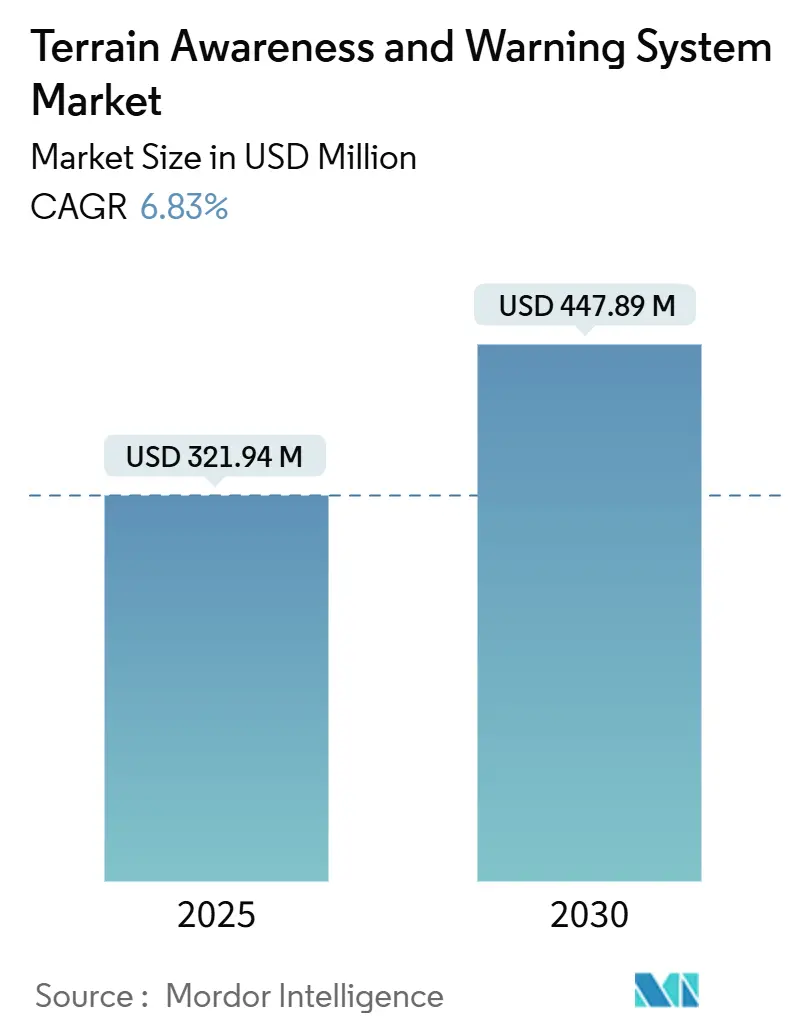

| Market Size (2025) | USD 321.94 Million |

| Market Size (2030) | USD 447.89 Million |

| Growth Rate (2025 - 2030) | 6.83% CAGR |

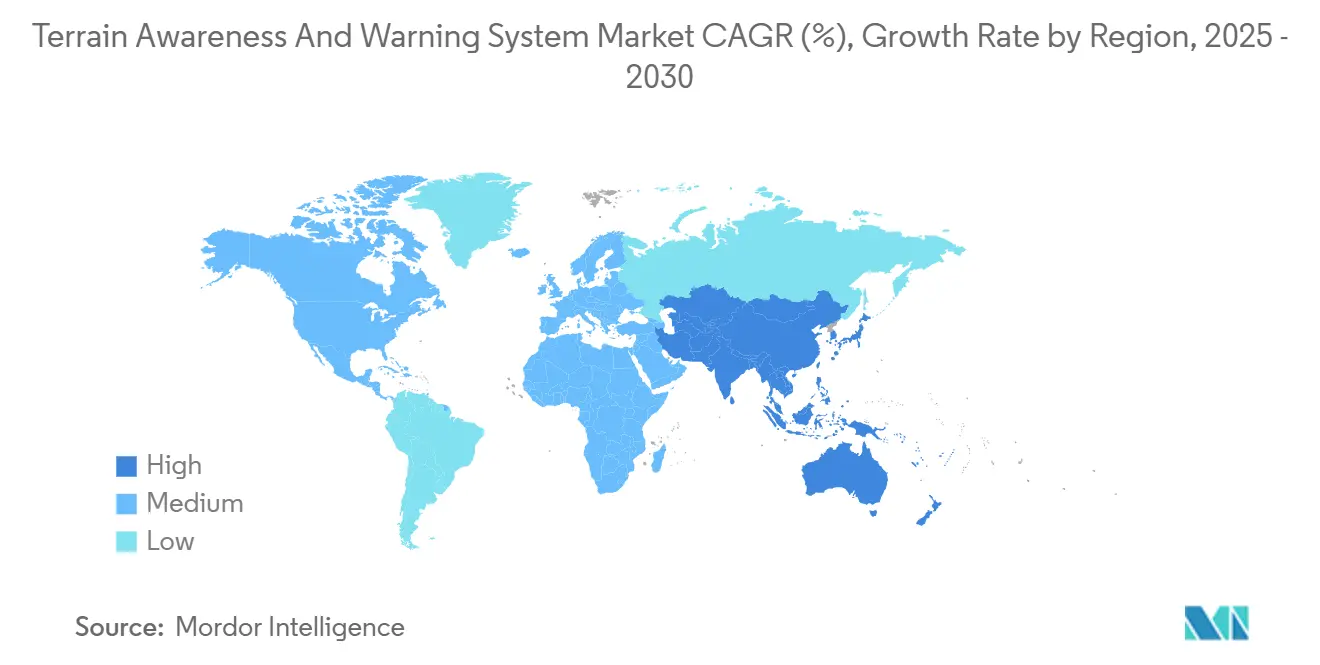

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Terrain Awareness And Warning System Market Analysis by Mordor Intelligence

The terrain awareness and warning system (TAWS) market size reached USD 321.94 million in 2025 and is forecasted to touch USD 447.89 million by 2030 at a 6.83% CAGR, underscoring the aviation sector’s sustained commitment to controlled-flight-into-terrain (CFIT) prevention and broader flight-safety mandates. Mandatory equipment rules for turbine aircraft, integration of radar-based predictive alerting, and steady fleet expansion anchor demand, while increasing helicopter sorties in offshore and emergency missions extend the customer base. Operators favor OEM fitment to minimize certification burdens. Yet, a large installed base of older jets and rotorcraft ensures continued retrofit opportunities, especially as avionics modernization dovetails with synthetic-vision rollouts. North America benefits from stringent FAA standards and concentrated airline traffic, but Asia-Pacific now leads incremental growth as domestic carriers scale capacity and regulators tighten performance requirements. Heightened cybersecurity scrutiny has also elevated the value proposition of next-generation TAWS solutions that authenticate GPS signals and cross-check multiple sensors for spoof-resilient operation.

Key Report Takeaways

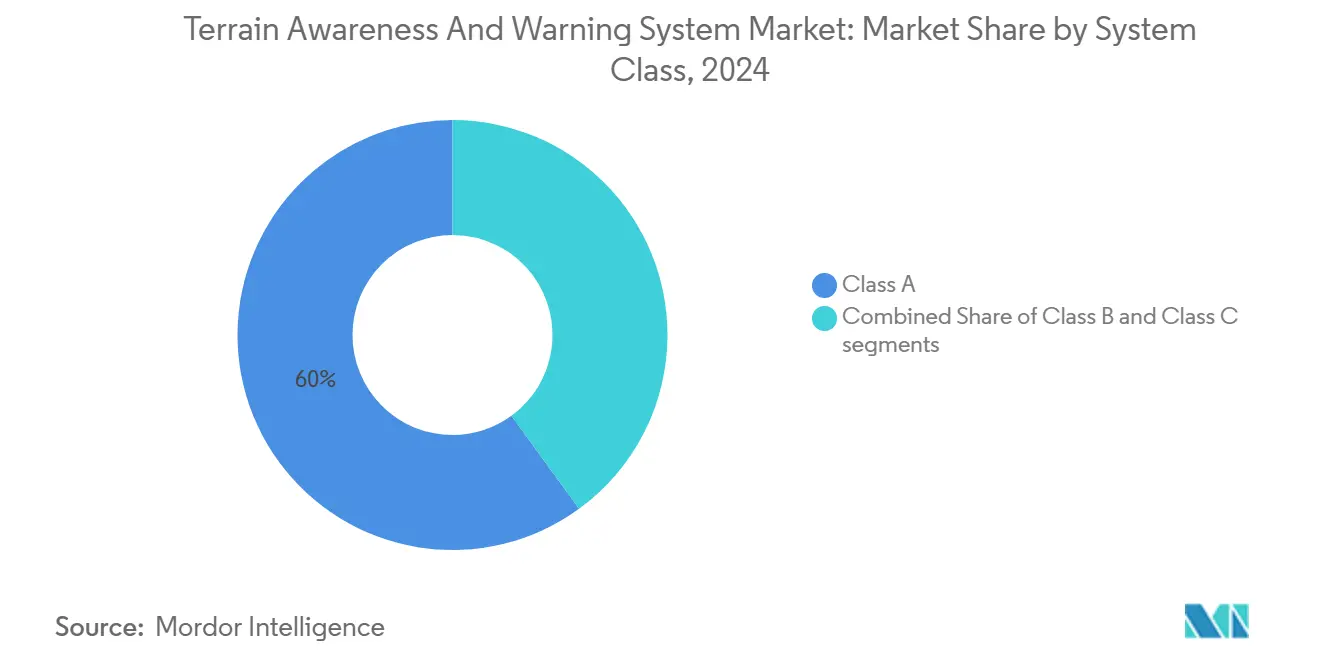

- By system class, Class A captured 60.02% of the terrain awareness and warning system market share in 2024; Class C is projected to expand at a 9.10% CAGR through 2030.

- By platform type, commercial aviation held 52.45% revenue share in 2024, while military aviation is set to post the fastest 7.68% CAGR to 2030.

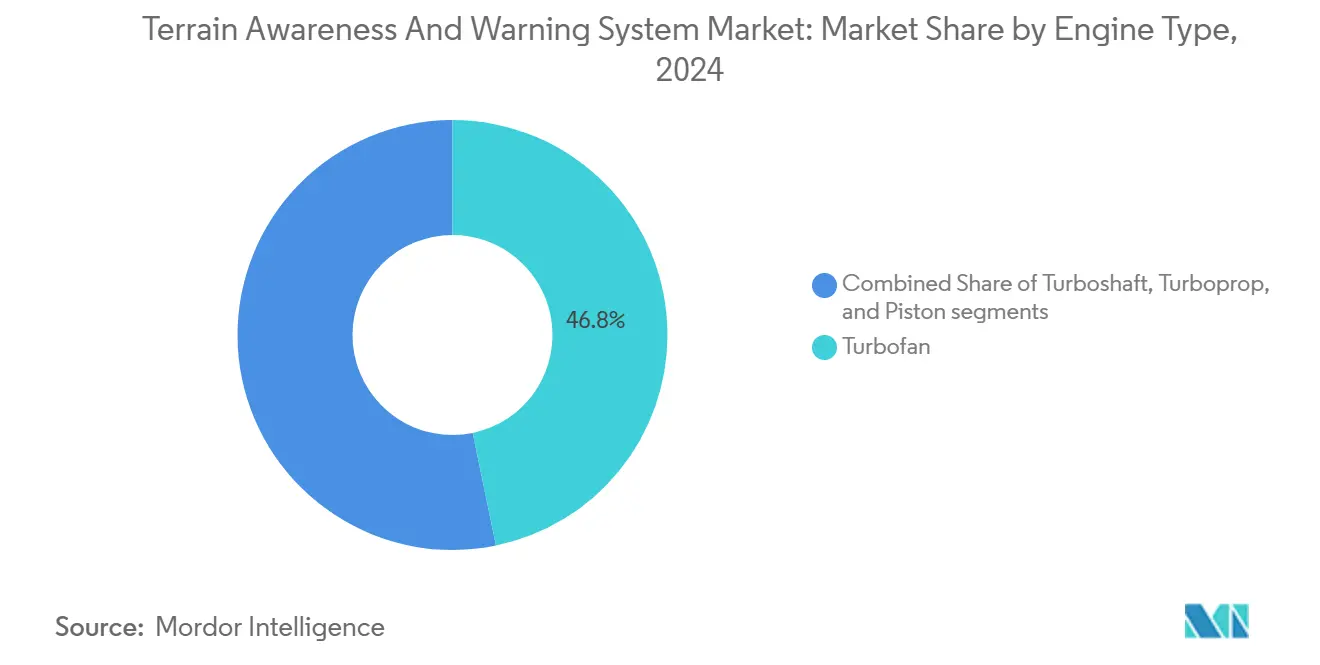

- By engine type, turbofan equipment accounted for 46.76% of the terrain awareness and warning system market size in 2024, and turboshaft installations are advancing at a 7.42% CAGR to 2030.

- By end user, OEM fitment commanded 64.76% share of the terrain awareness and warning system market in 2024 and also leads projected growth at 7.21% CAGR through 2030.

- By geography, North America led with a 37.89% share in 2024, whereas Asia-Pacific is forecast to deliver the highest 7.92% CAGR over the same horizon.

Global Terrain Awareness And Warning System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory installation requirements across commercial aviation regulations | +1.8% | Global; strongest in North America and Europe | Long term (≥ 4 years) |

| Growth in global air passenger traffic and commercial aircraft deliveries | +1.2% | Asia-Pacific core; spill-over to Middle East and South America | Medium term (2–4 years) |

| Rising helicopter operations in complex terrain and offshore environments | +0.9% | North America, Europe, Middle East offshore | Medium term (2–4 years) |

| Technological advancements in radar and sensor-based terrain alerting systems | +0.7% | Global; innovation led by North America and Europe | Long term (≥ 4 years) |

| Emphasis on proactive safety measures by aviation authorities and operators | +0.6% | Global | Long term (≥ 4 years) |

| Growing demand for autonomy and flight safety in military transport aircraft | +0.5% | North America, Europe, Asia-Pacific defense programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Installation Requirements Drive Market Expansion

Stringent rules such as 14 CFR 135.154 and TSO-C151d obligate turbine aircraft to carry certified TAWS, prompting continuous fleet-wide deployments.[1]Federal Aviation Administration, “AC 23-18 – Installation of TAWS Approved for Part 23 Airplanes,” faa.gov Comparable mandates from Transport Canada and EASA ensure regulatory harmonization that simplifies cross-border operations and stabilizes long-term demand. Airlines value compliance certainty, leading manufacturers to integrate terrain awareness and warning system market offerings directly into production lines for new jets. The framework also spurs upgrades of cockpit procedures and recurrent crew training, embedding TAWS into the broader safety culture. These factors make rule-driven adoption the most significant contributor to revenue visibility during the forecast window.

Commercial Aviation Growth Fuels TAWS Demand

Airbus plans 820 deliveries in 2025, and Boeing has restarted momentum after clearing quality bottlenecks, keeping single-aisle assembly lines near capacity. Each rollout ships with factory-installed TAWS to satisfy air-transport category regulations, guaranteeing baseline volume for suppliers. In parallel, carriers are extending the service life of 15-plus-year-old aircraft while waiting for new slots, which enlarges the retrofit pool. Intense network expansion across India, Indonesia, and mainland China has shifted a meaningful portion of terrain awareness and warning system market orders to Asia-Pacific carriers, underpinning the region’s leadership in incremental growth.

Helicopter Operations Expansion in Complex Environments

Search and rescue (SAR), offshore energy logistics, and air-ambulance providers increasingly treat TAWS—or HTAWS—as indispensable life-safety equipment. Operators such as Offshore Helicopter Services UK have added AW139 airframes with integrated warning suites for North Sea missions.[2]Offshore Helicopter Services UK, “Two Leonardo helicopters added to North Sea search and rescue fleet,” offshore-mag.com US accident analyses identified degraded situational awareness as a recurring factor in rotorcraft mishaps, reinforcing uptake of predictive terrain displays in the terrain awareness and warning system market. The trend is mirrored in the Gulf of Mexico, Arabian Gulf, and Asian offshore blocks, where low-level flight over water and variable weather amplify CFIT risk.

Technological Integration with Synthetic Vision Systems

Suppliers now pair digital elevation models, radar altimetry, and vision-computing chips to create fully fused displays that look beyond traditional audio alerts. Honeywell’s Mark XXII EGPWS and AI-enabled pipelines built with NXP Semiconductors exemplify the shift toward predictive analytics and lower false-alarm rates. Saab’s 0.5-meter-resolution terrain databases and Thales’ two-minute advisory line further shrink pilot reaction time, positioning TAWS as a hub within connected flight decks. Airlines gain additive value through crew-resource management improvements and reduced controlled-flight-into-terrain events.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of retrofit for aging general aviation and regional aircraft fleets | -0.8% | Global; pronounced in North America and EU | Medium term (2–4 years) |

| Integration challenges with legacy avionics and platform compatibility | -0.6% | Mature aviation markets worldwide | Short term (≤ 2 years) |

| Cybersecurity risks including GPS spoofing and terrain data breaches | -0.5% | Global, with recent incidents in Asia-Pacific and Europe | Medium term (2–4 years) |

| Lack of comprehensive global terrain mapping in emerging airspaces | -0.4% | Global; deepest impact on North American and European MROs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs Constrain General Aviation Adoption

Installing a Class A system can exceed USD 50,000 per airframe, discouraging many owners of piston singles and regional turboprops from voluntary upgrades. Supply-chain snags have also prolonged parts procurement, pushing maintenance labor beyond 80 hours per installation for some shops. The expense-to-aircraft-value ratio remains especially acute for 30-year-old platforms, slowing penetration in price-sensitive sub-segments of the terrain awareness and warning system market.

Legacy Avionics Integration Complexity

Retrofits in early-2000s jets require bespoke engineering to marry TAWS computers with analog ground-proximity sensors, mode-S transponders, and older EFIS displays. Collins Aerospace’s Pro Line modernization kits illustrate the level of supplemental type certification (STC) work needed per variant. Mis-wired connectors or improper software loads have triggered service difficulty reports, mandating repeat inspections and driving up downtime. These hurdles prolong decision cycles and temper short-term conversion volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Class: Regulatory Compliance Sustains Class A Leadership

Class A equipment held 60.02% of the terrain awareness and warning system market in 2024, cementing its role as the benchmark for commercial air-transport categories. This dominance originates from mandates that turbine aircraft with 10+ passenger seats carry full-featured TAWS, creating a structural demand floor. Parallel adoption in widebody freighters further enlarges the installed base. Class C offerings' terrain awareness and warning system market size is projected to climb at a 9.10% CAGR as price-efficient solutions penetrate light twins and high-performance singles. Lower size-weight-and-power (SWaP) footprints and GPS-centric architectures give Class C vendors entry leverage without compromising core warning logic.

Manufacturers have responded by launching scalable product families: Honeywell's BendixKing suite now embeds TAWS logic within integrated flight displays, while Garmin autoloads HTAWS functions in its G1000 NXi glass-cockpit line.[3]Honeywell Aerospace, “Mark XXII EGPWS,” honeywell.com That convergence simplifies pilot training and raises the perceived safety utility, supporting robust unit growth well into the forecast.

By Platform Type: Commercial Dominance Meets Military Modernization

Commercial operators, driven by narrowbody and widebody volume, represented 52.45% of the terrain awareness and warning system market revenue in 2024 and will remain the largest customers through 2030. Fleet utilization close to 12-hour daily averages makes CFIT safeguards indispensable. However, a 7.68% CAGR is forecast for military aviation, driven by programs like the US Army’s UH-60V digital cockpit upgrade and NATO transport modernization agendas.

Defense buyers increasingly pair TAWS with autonomous navigators and mission-computer stacks, accelerating order value per aircraft. Meanwhile, general aviation adoption continues but at a gentler trajectory, chiefly influenced by regulatory grace periods and owner economics. This mix of steady commercial volume and emerging defense momentum keeps the overall terrain awareness and warning system market balanced across civil–military lines.

By Engine Type: Turbofan Fleet Dominates While Turboshaft Gains Altitude

Turbofan-powered jets accounted for 46.76% of the terrain awareness and warning system market share in 2024, reflecting the ubiquity of single-aisle workhorses such as the A320, 737, and Embraer E-Jet families. Each new delivery automatically ships with Class A TAWS, locking in baseline unit shipments. By contrast, turboshaft helicopter applications are poised for a 7.42% CAGR, mirroring increased medevac and offshore commitments where HTAWS provides low-level terrain-avoidance envelopes.

Turboprops occupy a middle tier, serving short-haul regional and cargo routes that still traverse mountainous terrain. Piston aircraft remain the smallest addressable segment, yet offer upside as entry-level class-C prices drop and insurers reward equipage with lower premiums. These dynamics underscore propulsion diversity as a driver of differentiated growth pockets within the terrain awareness and warning system market.

By End User: OEM Fitment Delivers Scale and Speed

Factory installations captured 64.76% of the terrain awareness and warning system market revenue in 2024 and will outpace aftermarket conversions at 7.21% CAGR through 2030. Airframers integrate TAWS alongside autopilot, ADS-B, and flight-management bundles, leveraging single certification flows and eliminating post-delivery downtime. Airbus and Boeing specify terrain databases and alert-logic certification inside original Type Certificates, assuring global operability from day one.

The retrofit channel, while smaller, remains strategic. Thousands of pre-2010 aircraft operate daily without modern TAWS or with first-generation ground proximity warning system (GPWS) units; avionics refresh cycles tied to ADS-B mandates often trigger TAWS upgrades as incremental line-items. Specialized MROs, notably AMETEK MRO Asia, are scaling their capabilities to trim installation timelines, preserving aftermarket relevance for the terrain awareness and warning system market.

Geography Analysis

Asia-Pacific airlines collectively ordered more than 1,800 single-aisle jets scheduled for delivery between 2025 and 2030, ensuring a robust pipeline of factory-installed TAWS units. Low-cost carriers (LCCs) in Indonesia and Vietnam lead the wave, often negotiating bundled terrain-awareness options with more expansive avionics suites to streamline training across burgeoning pilot cohorts. Parallel policy moves by the Civil Aviation Administration of China, which targets 780 million passengers in 2025, compel domestic carriers to equip new and in-service fleets with current-generation terrain-warning logic, reinforcing regional baseline demand.[4]Civil Aviation Administration of China, “Passenger Forecast 2025,” aviationweek.com

North America nonetheless remains the single largest market by revenue, sustained by stringent oversight, a vast business-jet community, and Department of Defense upgrade programs. FAA Airworthiness Directives covering TAWS software updates ensure recurring aftermarket activity, while US rotorcraft EMS providers continue large-scale HTAWS retrofits in response to human-factors accident findings. Canada’s mirrored regulatory environment brings additional volume, particularly among regional turboprop carriers traversing the Rocky Mountains and sub-Arctic routes.

Europe exhibits mature yet steady demand. EASA certification pathways emphasize harmonized training and maintenance, prompting full-life-cycle support contracts that embed database subscription revenues within the terrain awareness and warning system market. Given challenging topography, operators in Norway, the Alps, and the Iberian Peninsula prioritize terrain-database granularity. Across the Middle East, national carriers’ widebody growth obliges Class A equipage, while emerging MRO clusters in the Gulf provide installation know-how for African and South Asian customers. South America’s mountainous geographies, notably the Andes, present clear safety imperatives, although budget constraints and older fleet profiles slow immediate adoption, suggesting longer-tail upside as financing schemes mature.

Competitive Landscape

Honeywell International Inc., Collins Aerospace, and Thales Group anchor the competitive core, jointly controlling a significant share through broad portfolios ranging from Class A to helicopter-specific solutions. Honeywell’s Mark XXII EGPWS introduces AI-assisted threat prioritization, while Collins leverages Pro Line Fusion to embed TAWS logic into larger flight-management ecosystems. Thales differentiates with its patented Terrain Advisory Line that extends predictive windows to two minutes.

Garmin Ltd. and Universal Avionics focus on light- and mid-cabin business aircraft, exploiting quicker software-release cycles and modular certification approaches. L3Harris Technologies, Inc., and Saab AB supply enabling databases and algorithm libraries that other OEMs license, broadening the value chain. Barriers to entry remain high because each new product must meet TSO-C151d and EASA ETSO-2C151 conformity-assessment requirements, including hazard-level analyses and flight-test evidence.

Cyber-resilience has emerged as the latest battleground. Incidents of GPS spoofing against civil transports in Southeast Asia have forced avionics vendors to incorporate multi-sensor cross-checking, encrypted integrity beacons, and ground-segment validation. Suppliers investing early in these countermeasures are securing long-term sole-source positions with defense departments and premium airlines, adding strategic heft. Overall, the market displays moderate concentration: the top five suppliers hold roughly 65% of 2024 revenue, leaving meaningful room for niche specialists but limiting the probability of disruptive new entrants.

Terrain Awareness And Warning System Industry Leaders

Honeywell International Inc.

Garmin Ltd.

Elbit Systems Ltd.

Thales Group

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Aero Asahi Corporation ordered its sixth H145/BK117 D-3 helicopter from Kawasaki Heavy Industries, enhancing its air ambulance fleet. The D-3 helicopter features advanced avionics, such as an autopilot, GPS map display, and terrain awareness and warning system, ensuring safe and efficient operations in challenging conditions.

- May 2021: The US Air Force announced a contract with Honeywell International, Inc., for bi-annual software updates for the Terrain Awareness and Warning System (TAWS) on 431 Lockheed Martin C-130J Super Hercules aircraft.

Global Terrain Awareness And Warning System Market Report Scope

| Class A |

| Class B |

| Class C |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Military Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| Turbofan |

| Turboshaft |

| Turboprop |

| Piston |

| OEM Fitment |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Class | Class A | ||

| Class B | |||

| Class C | |||

| By Platform Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Military Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By Engine Type | Turbofan | ||

| Turboshaft | |||

| Turboprop | |||

| Piston | |||

| By End User | OEM Fitment | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the terrain awareness and warning system market?

The TAWS market was valued at USD 321.94 million in 2025 and is projected to grow to USD 447.89 million by 2030.

Which region is expanding fastest in deploying TAWS?

Asia-Pacific is forecasted to register a 7.92% CAGR through 2030, outpacing all other regions.

Why do airlines prefer OEM fitment for TAWS?

Factory installations streamline certification, reduce downtime, and embed TAWS within broader avionics suites.

Which system class shows the highest growth potential?

Class C systems are expected to rise at a 9.10% CAGR as lightweight, cost-efficient options penetrate general aviation.

How does helicopter growth affect TAWS demand?

Expanding SAR, offshore, and medevac missions boost HTAWS uptake, driving a 7.42% CAGR in turboshaft applications.

Page last updated on: