Market Overview

| Study Period | 2021 - 2031 |

|---|---|

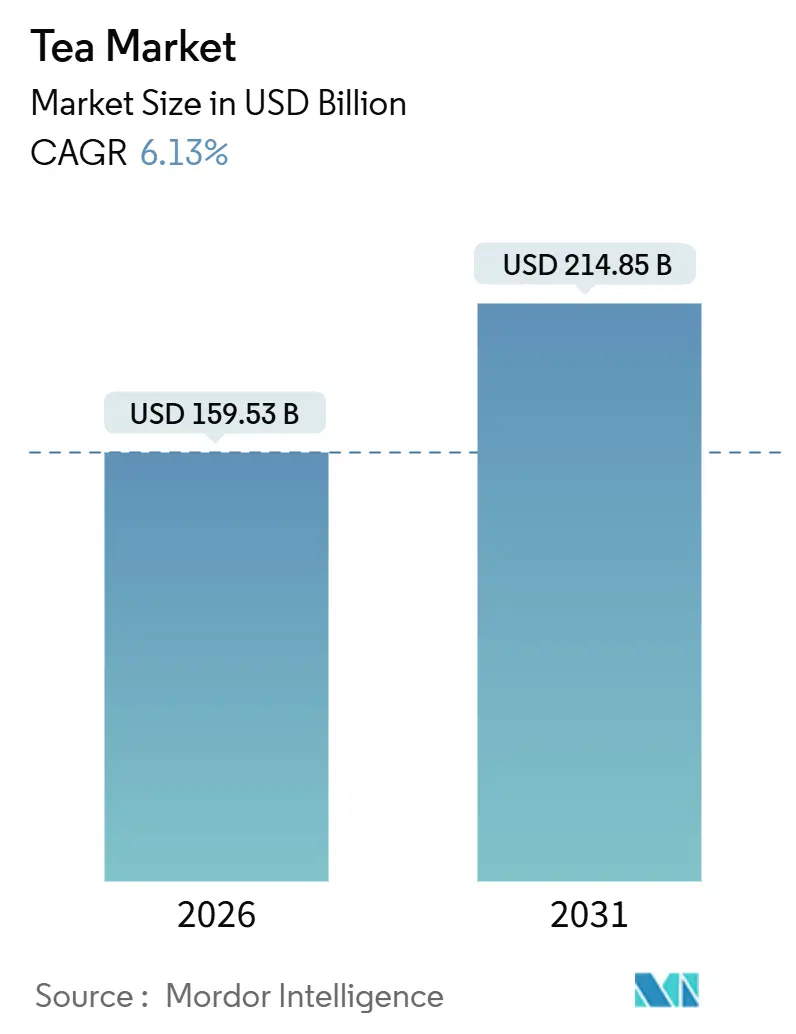

| Market Size (2026) | USD 159.53 Billion |

| Market Size (2031) | USD 214.85 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tea Market Analysis by Mordor Intelligence

The tea market is expected to grow from USD 159.53 billion in 2026 to USD 214.85 billion by 2031, with a compound annual growth rate (CAGR) of 6.13% during the forecast period. This growth is driven by increasing consumer demand for healthier and premium tea options, as well as a focus on sustainability and certified production practices. Younger consumers, particularly those from the Gen Z demographic, are showing a preference for teas that are low in caffeine, organic, and ethically sourced. These consumers are prioritizing quality and value over quantity, which is influencing how companies approach their sales and distribution strategies. Brands are innovating by introducing new products, such as collagen-infused teas and environmentally friendly packaging, including mono-material pouches, which are attracting a broader range of consumers. Overall, the tea market remains moderately fragmented, with numerous players competing to meet evolving consumer preferences and regulatory requirements.

Key Report Takeaways

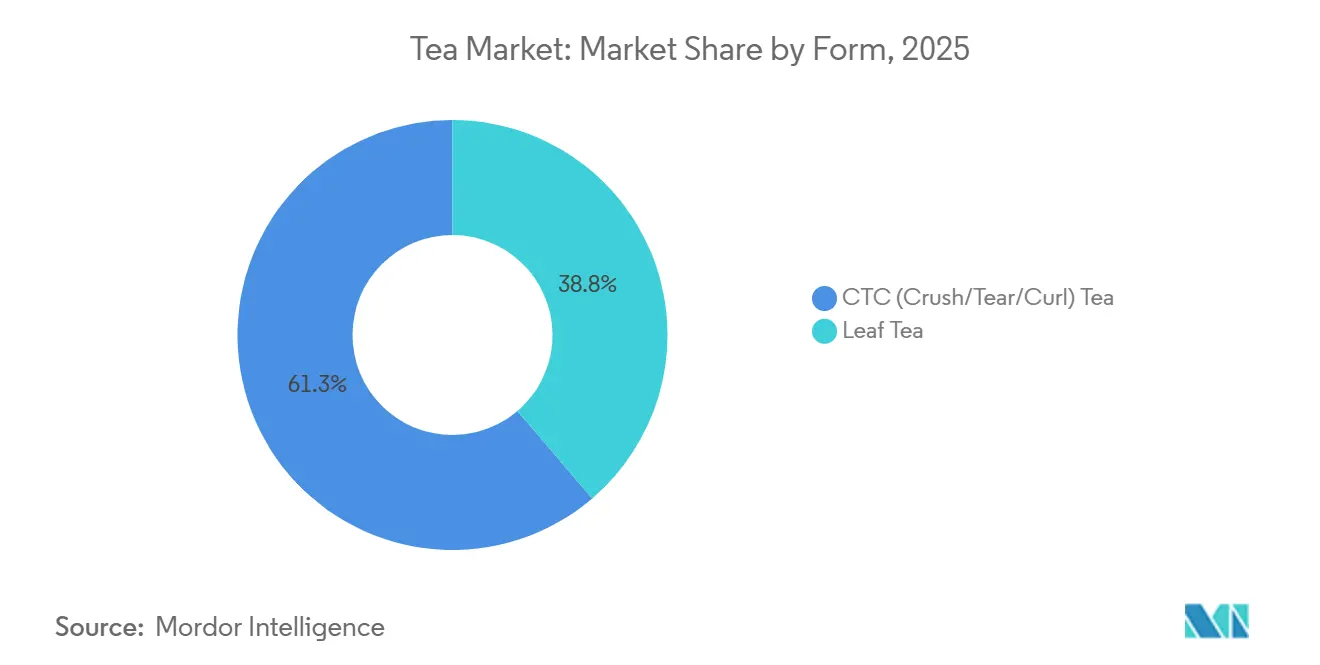

- By form, CTC (crush/tear/curl) tea commanded 61.25% of the tea market share in 2025, while leaf tea is projected to grow at a 6.45% CAGR through 2031.

- By product type, black tea accounted for 41.57% of the tea market size in 2025; herbal and fruit infusions are expected to expand at a 7.52% CAGR through 2031.

- By category, conventional tea held an 86.43% revenue share in 2025, whereas organic tea is forecasted to record the highest CAGR at 9.49% through 2031.

- By flavoring, unflavored tea accounted for 75.71% of sales in 2025, while flavored variants advanced at a 7.26% CAGR to 2031.

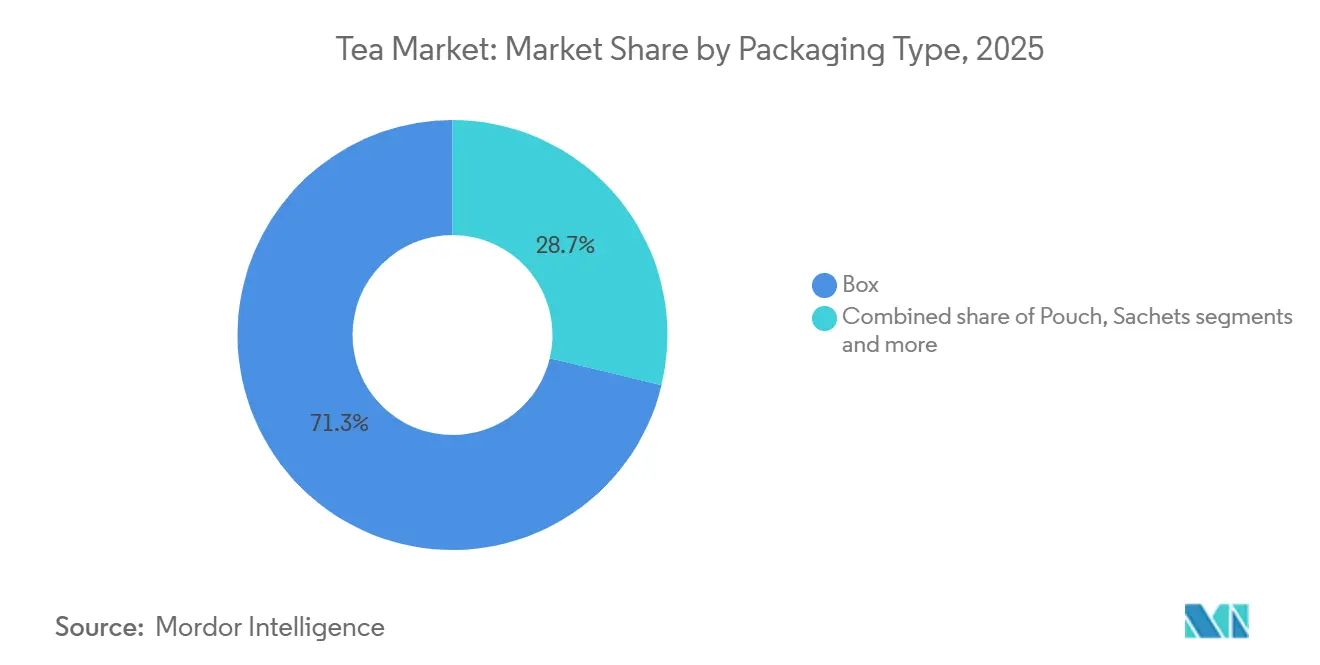

- By packaging type, box formats held a 71.25% share in 2025; pouches exhibited the fastest growth rate of 7.07% through 2031.

- By distribution channel, off-trade represented 69.05% share in 2025, yet on-trade is accelerating at 9.51% CAGR to 2031.

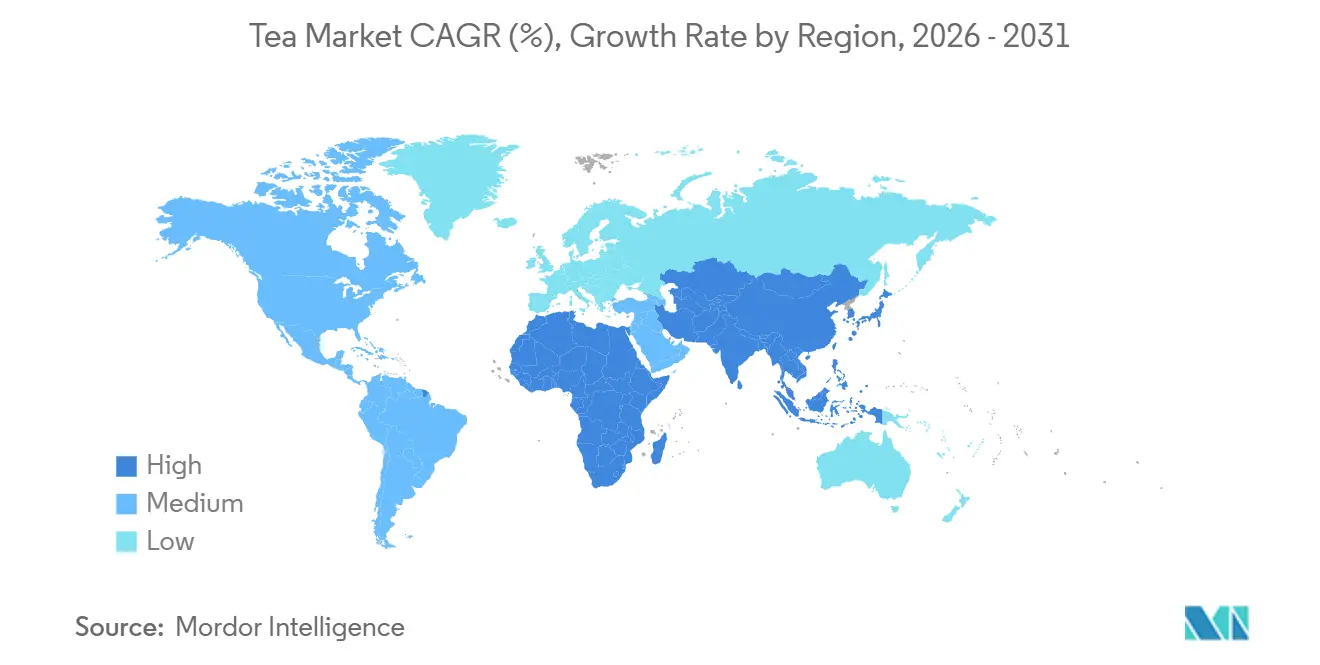

- By geography, Asia-Pacific led with 36.75% of tea market share in 2025; Middle East and Africa is the fastest-growing region at an expected 8.53% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased health consciousness boosting demand for green and herbal teas | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Consumer preference for sustainable and ethically sourced products | +0.9% | North America, Europe, Australia; emerging in Middle East premium segments | Long term (≥ 4 years) |

| Innovation in flavors, blends, and packaging | +1.5% | Global, led by Asia-Pacific (China, Japan) and North America | Short term (≤ 2 years) |

| Gen-Z preference for wellness teas with low caffeine or decaffeinated options | +0.8% | North America, Europe, urban Asia-Pacific (Singapore, South Korea) | Medium term (2-4 years) |

| Demand for single-origin tea driving premiumization | +0.6% | North America, Europe, Japan; niche growth in Middle East | Long term (≥ 4 years) |

| Tea consumption patterns and cultural importance | +0.7% | Asia-Pacific (China, India, Japan), Middle East, North Africa, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased health consciousness is boosting the demand for green and herbal teas

Growing health awareness is driving the demand for green and herbal teas, as more consumers opt for beverages that offer additional health benefits beyond basic hydration. According to an article published by the Cleveland Clinic Organization in September 2024, drinking 2 to 4 cups of green tea daily can lower the risk of stroke by up to 24%[1]Source: Cleveland Clinic Organization, "How Green Tea Can Benefit Your Health", health.clevelandclinic.org. Green tea contains compounds such as catechins and L-theanine, which are known to promote heart health, enhance cognitive function, and reduce stress levels. These proven health advantages are encouraging a shift, particularly among younger and health-conscious consumers, from sugary drinks to natural, low-calorie tea options. In response to this trend, brands are expanding their product offerings to include more functional teas for issues such as weight management. For instance, in June 2025, Tetley introduced Tetley Green Tea Slim Care, which is infused with L-Carnitine to cater to the growing interest in teas that support metabolism and weight management.

Gen-Z increasingly prefers wellness teas with low caffeine or decaffeinated options.

Gen Z's focus on wellness is driving a growing demand for low-caffeine and decaffeinated teas. Younger consumers are increasingly seeking beverages that support mental health, promote better sleep quality, and alleviate stress. This trend is supported by findings from Mental Health America’s 2024 Mind the Workplace report, which reveals that 71% of Gen Z employees and 59% of Millennials have poor workplace health scores[2]Source: Mental Health America, "MHA Releases 2024 Mind the Workplace Report, GenZ and Millennials Report the Poorerest Work Health Scores", mhanational.org. Three out of four employees in the United States report that work-related stress negatively affects their sleep. As a result, many Gen Z consumers are turning to teas that offer relaxation or calm energy without causing overstimulation. This has led to a rising interest in low-caffeine options, CO₂-extracted decaffeinated teas, and herbal blends that maintain flavor while minimizing stimulant content. Brands that clearly label caffeine levels and market tea as a beverage for stress relief or evening relaxation are successfully meeting this demand.

Tea consumption patterns and their cultural importance

Tea consumption habits and their cultural importance are significant factors driving the tea market. The daily tradition of drinking tea ensures a steady and reliable demand in both developed and developing markets. According to the Tea and Coffee Trade Journal in May 2025, China had the highest per capita tea consumption at 1.92 kg per person annually, followed by Morocco at 1.87 kg, Ireland at 1.52 kg, and the United Kingdom at 1.36 kg[3]Source: Tea and Coffee Trade Journal, "The 2025 Global Tea Report", teaandcoffee.net. These numbers demonstrate the profound impact of tea on the daily lives of people across various regions. In many countries, tea is a symbol of hospitality, a key part of social interactions, and a regular feature in workplace and home routines. This strong cultural connection drives frequent purchases, ensuring the market remains stable and resilient, even during periods of economic uncertainty. The growing popularity of specialty teas and health-conscious options has further strengthened tea's role in everyday life, contributing to the market's consistent growth.

Innovation in flavors, blends, and packaging

The tea market is evolving as companies are moving beyond traditional tea formats to attract younger audiences, health-conscious individuals, and environmentally aware buyers. Specialty teas, such as hojicha and oolong, which were once limited to niche cafés, are becoming widely available in mainstream retail stores. Sustainability in packaging has also emerged as a significant factor influencing consumer choices. For example, in July 2024, Esah Tea launched the world’s first microplastic-free tea bags made from biodegradable, chemical-free cotton. This innovation directly addresses increasing concerns about plastic contamination in tea bags. Functional and affordable tea formats are helping expand the market by reaching new consumer segments. In December 2025, Assam-based startup Oji introduced a ready-to-drink iced tea enriched with vitamin C, which positions tea as a strong competitor to juices and other functional beverages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from coffee and other beverages | -0.8% | Global, particularly North America and Europe where coffee culture dominates | Short term (≤ 2 years) |

| Climate change and agricultural risks | -1.1% | Asia-Pacific (India, China, Sri Lanka, Kenya), East Africa | Long term (≥ 4 years) |

| Consumer shift toward instant and functional beverages | -0.6% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory challenges and import/export barriers | -0.5% | Global, with acute impact on cross-border trade between Asia, Europe, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense competition from coffee and other beverages

Coffee and functional beverages are increasingly limiting the growth of the tea market by capturing frequent consumption occasions and a significant share of consumer spending. This trend is particularly evident in regions like North America and Europe, where coffee has become a staple in daily routines. For instance, the National Coffee Association’s Specialty Coffee Report from June 2025 revealed that 46 percent of American adults consumed specialty coffee in the past day. This highlights coffee’s stronghold on morning and on-the-go consumption occasions, areas where tea has traditionally competed. Innovations in coffee products, such as single-serve pods, nitro cans, and high-caffeine cold brews, have raised consumer expectations for convenience, flavor intensity, and functional benefits. At the same time, the rise of functional beverages, such as energy drinks and protein shakes, is further dividing consumer spending in the beverage market.

Regulatory challenges and import/export barriers hinder the smooth functioning of supply chains

Regulatory challenges and import and export barriers are slowing down the growth of the tea market by disrupting international trade and increasing costs across the supply chain. Tea producers must comply with stringent regulations, including limits on pesticide residues, food safety standards, and traceability requirements, particularly when exporting to major markets such as the European Union, the United States, and Japan. These regulations are often complex and subject to frequent changes, such as updates to maximum residue limits or new rules for packaging, labeling, and sustainability. As a result, producers face higher costs for testing, certification, and documentation, which can be particularly burdensome for small-scale growers and exporters. Import duties, port delays, and customs inspections further complicate the process. These issues slow down shipments, reduce the efficiency of supply chains, and increase the overall costs for tea brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Leaf Premiumization Challenges CTC Dominance

CTC (Crush, Tear, Curl) tea remains a dominant force in the tea market, primarily due to its widespread use in everyday consumption and mass-market channels. In 2025, it held a 61.25% global market share, reflecting its popularity in retail stores, foodservice outlets, and institutional catering. Its quick brewing process, strong flavor, and affordability make it a preferred choice for black tea blends, tea bags, and chai. This format is especially popular in high-demand regions, such as India, Africa, and parts of the Middle East, where it caters to large-scale consumption needs and remains a staple in the tea industry.

In contrast, leaf tea is emerging as the fastest-growing segment, driven by a shift toward premium and specialty products. This segment is projected to grow at a 6.45% CAGR through 2031, as consumers increasingly opt for whole-leaf, artisanal, and specialty teas. The growing interest in green, oolong, white, and high-quality black teas is supported by trends like café culture and home brewing. Leaf tea is often associated with better quality, authenticity, and health benefits, making it particularly appealing to urban and higher-income consumers who are willing to pay a premium for a superior tea experience.

By Product Type: Herbal Infusions Accelerate

Black tea continued to dominate the tea market in 2025, accounting for 41.57% of the total market share. Its popularity is driven by its strong cultural significance in regions such as India, the United Kingdom, and the Middle East, where it is an integral part of daily routines. The versatility of black tea, which pairs well with milk, sugar, and various spices, makes it a favorite for both home consumption and food service. Its availability in various formats, such as tea bags, instant tea, and ready-to-drink options, ensures its appeal across different consumer segments, from budget-friendly to premium categories.

On the other hand, herbal and fruit infusions are emerging as the fastest-growing segment in the tea market, with a projected CAGR of 7.52% through 2031. These teas are gaining traction among health-conscious consumers who prefer caffeine-free and wellness-focused beverages. Popular for their perceived benefits, such as aiding relaxation, digestion, immunity, and sleep, these infusions are particularly appealing to younger demographics. The growing demand for natural, plant-based, and clean-label products is driving their adoption in regions such as North America, Europe, and the Asia Pacific. As a result, herbal and fruit teas are transitioning from niche wellness products to mainstream retail offerings, shaping the future growth of the tea market.

By Category: Organic Certification Captures Value Growth

In 2025, conventional tea remained the leading segment in the tea market, accounting for 86.43% of the total market share. This dominance is attributed to its affordability, large-scale production, and widespread availability in retail outlets like supermarkets and convenience stores, as well as foodservice channels. It remains a popular choice for daily consumption, particularly in high-demand regions such as India, China, and Africa, where tea is a cultural staple. Additionally, its strong presence in formats such as tea bags, loose tea, and institutional catering ensures consistent demand and reinforces its position as the backbone of the tea industry.

Meanwhile, organic tea is emerging as the fastest-growing segment, with a projected CAGR of 9.49% through 2031, driven by increasing consumer focus on health and sustainability. Concerns over pesticide residues, a preference for eco-friendly farming practices, and the demand for clean-label products are key factors boosting its popularity. The availability of organic tea has improved significantly through modern retail stores and e-commerce platforms, while certifications for organic products have built consumer trust. Although organic tea currently holds a smaller market share, its rapid growth indicates a shift toward healthier and more environmentally conscious choices among consumers.

By Flavouring: Novelty Drives Flavoured Uptake

Unflavored tea continued to dominate the tea market in 2025, accounting for 75.71% of the total market share. This dominance is largely due to cultural traditions in key tea-consuming countries, such as China, India, and Japan, where tea is valued for its natural taste and purity. These regions often prefer unflavored tea in loose-leaf forms, which are commonly used in ceremonial practices and daily brewing. The strong demand for unflavored tea spans both premium and mass-market segments, making it a staple choice for consumers in these markets.

On the other hand, flavored tea is the fastest-growing segment, expected to grow at a CAGR of 7.26% through 2031. This growth is driven by increasing consumer interest in diverse flavors and functional benefits. Younger and urban consumers are particularly drawn to blends featuring fruits, spices, flowers, and botanicals, as they offer unique taste experiences. The rise of ready-to-drink teas, café culture, and gifting options has further boosted the popularity of flavored teas. These factors are helping flavored teas carve out a larger share in the market by appealing to evolving consumer preferences.

By Packaging Type: Pouches Reduce Environmental Footprint

Box packaging remains the most popular choice in the tea market, holding 71.25% of the market share in 2025. This is largely because consumers are familiar with it, and it is easy to store and display on retail shelves. Carton boxes are widely used for packaging both tea bags and loose-leaf tea, offering good protection for the product and helping brands stand out. Their strong presence in supermarkets and traditional stores, combined with their ability to support large-scale distribution, ensures their continued dominance in the tea packaging market.

Meanwhile, pouches are quickly becoming the fastest-growing packaging option, with an expected CAGR of 7.07% through 2031. The rising demand for eco-friendly and cost-efficient packaging solutions drives this growth. Regulations like the EU Regulation 2025/40 are encouraging brands to switch to recyclable and compostable materials, making flexible mono-material and paper-based pouches more attractive. Pouches also use less material, are lighter for transportation, and have a smaller environmental impact. As a result, many tea manufacturers are moving away from rigid boxes and adopting pouches to meet both regulatory requirements and consumer preferences for sustainable packaging.

By Distribution Channel: Experience-Led On-Trade Scales

Off-trade channels, including supermarkets, hypermarkets, convenience stores, and online platforms, held the largest share of the tea market in 2025, accounting for 69.05%. These channels are popular because they offer convenience, affordability, and easy access to a wide variety of tea products. Bulk purchasing options, promotional discounts, and strong shelf visibility make them the go-to choice for regular tea buyers. The growth of e-commerce and modern retail outlets has made it easier for consumers to explore and purchase different tea brands and formats from the comfort of their homes.

On the other hand, on-trade channels, including cafés, tea bars, and restaurants, are the fastest-growing segment, with a projected CAGR of 9.51% through 2031. The increasing popularity of café culture and premium tea experiences is driving this growth, as more people seek out specialty beverages like matcha lattes, bubble tea, and artisanal teas. Social dining, tourism, and the demand for unique, experiential retail experiences are also contributing to the rise of on-trade tea consumption. These venues are becoming important spaces for introducing premium tea products and enhancing brand visibility in the market.

Geography Analysis

Asia Pacific was the largest regional market for tea, accounting for 36.75% of the global market value by 2025. A robust production base and a long-standing tradition of tea consumption drive this dominance. China and India lead both production and demand, while Japan boosts exports of specialty teas. Southeast Asia is experiencing rapid growth in the ready-to-drink tea segment, with countries like South Korea and Australia contributing through premium imports and a thriving café culture. The region’s focus on high-quality and certified teas ensures its central role in the tea market.

The Middle East and Africa are the fastest-growing tea markets, with a CAGR of 8.53% through 2031. Urbanization, a young population, and increasing demand for imported packaged beverages are driving this growth. Gulf countries are expanding their retail and foodservice sectors, while East Africa remains a key supplier of black tea globally. In North Africa, traditional green tea and mint blends are popular, but premium and organic teas are gaining attention among urban consumers. However, the region faces challenges such as agricultural risks and climate-related issues that could impact supply.

Europe and North America are mature tea markets but continue to grow through innovation and sustainability efforts. In Europe, stricter regulations are pushing companies to adopt recyclable and compostable packaging, which is changing product designs and shelf displays. In the United States and Canada, there is rising demand for cold-brew, ready-to-drink, and wellness-focused teas, supported by cafés, specialty stores, and online platforms. South America, though smaller in market size, is seeing increased interest in herbal and wellness teas, particularly in countries like Brazil and Chile, where health awareness is growing.

Competitive Landscape

The tea market is moderately fragmented, which indicates a mix of large multinational companies and numerous regional or niche players. Major brands, such as Unilever, Tata Consumer Products, and Associated British Foods, dominate the market due to their strong distribution networks, brand recognition, and cost advantages resulting from large-scale operations. However, smaller brands are increasingly competing by focusing on unique selling points such as wellness benefits, premium quality, and authentic origin stories. This creates a competitive environment where both large-scale operations and niche branding strategies are essential for success.

Leading companies are actively investing in strategies to maintain their market positions and adapt to changing consumer preferences. For example, Tata Consumer Products is expanding its presence in cafés and out-of-home consumption through its partnership with Starbucks, targeting premium tea drinkers. Unilever has revamped its Lipton brand by introducing sustainable packaging and certifications, while Associated British Foods, through its Twinings brand, has focused on eco-friendly tea bags and compliance with environmental regulations. These efforts help established brands stay relevant as consumers increasingly prioritize sustainability, ethics, and quality in their purchasing decisions.

Meanwhile, smaller premium brands like Rishi Tea and Botanicals, Numi Organic Tea, and Dilmah are gaining traction by emphasizing organic ingredients, direct trade practices, and transparency in their supply chains. These brands are also leveraging technology, such as traceability tools and digital engagement, to connect with consumers and justify higher price points. Additionally, large beverage companies are entering the tea segment through partnerships and innovations in ready-to-drink products, such as PepsiCo’s collaborations in Asia and North America. As a result, the market is evolving into a structure where global giants dominate one end, while premium, craft-focused brands thrive on the other, creating a dynamic and competitive landscape.

Tea Industry Leaders

-

PepsiCo Inc.

-

Tata Consumer Products Ltd.

-

Associated British Foods PLC

-

ITO EN, Ltd.

-

Unilever plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Wagh Bakri Tea Group introduced its premium offering, Wagh Bakri Royale, during World Food India (WFI) 2025. This flagship global food and beverage event, organized by the Ministry of Food Processing Industries, served as a platform for the brand to showcase its finest tea blend to a diverse audience.

- September 2025: Brooke Bond Red Label introduced pre-mix tea sachets, expanding its product portfolio. The HUL brand launched its masala chai sachets through an advertisement set on a moving train, showcasing the convenience and flavor of the new offering.

- June 2024: Uncle Matt’s Organic introduced 3 new ready-to-drink, refrigerated, brewed black tea options. These teas, available in unsweetened, sweetened, and half-and-half black tea lemonade flavors, are packaged in convenient 52-oz bottles.

- March 2024: DAVIDsTEA introduced its “Tea-2-Go” initiative, now available at over 1,500 Couche-Tard and Circle K stores across Canada. This launch aimed to expand the brand's reach, offering convenient access to its premium tea products for on-the-go consumers.

Global Tea Market Report Scope

The tea market encompasses tea, a beverage produced by infusing dried leaves, buds, or herbs in hot or cold water to create a natural or flavored drink consumed for refreshment, taste, and wellness. The tea market is segmented by form, product type, category, flavouring, packaging type, distribution channels, and geography. Based on form, the market studied is segmented into leaf tea and CTC tea. Based on product type, the market is segmented into black tea, green tea, oolong tea, herbal and fruit tea infusions, and other product types. Based on category, the market is classified into conventional tea and organic tea. Based on the flavouring, the market is classified into unflavoured and flavoured. Based on the packaging type, the market is classified into boxes, bags, pouches, sachets, and other packaging types. Based on distribution channels, the market is segmented into off-trade and on-trade. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle-East, and Africa. The market forecasts are provided in terms of value (USD).

By Form

| Leaf Tea |

| CTC (Crush/Tear/Curl) Tea |

By Product Type

| Black Tea |

| Green Tea |

| Oolong Tea |

| Herbal and Fruit Tea Infusions |

| Other Product Types |

By Category

| Conventional Tea |

| Organic Tea |

By Flavouring

| Unflavoured |

| Flavoured |

By Packaging Type

| Box |

| Bag |

| Pouch |

| Sachets |

| Other Packaging Type |

By Distribution Channel

| Off-Trade | Supermarkets/Hypermarkets |

| Convinience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Leaf Tea | |

| CTC (Crush/Tear/Curl) Tea | ||

| By Product Type | Black Tea | |

| Green Tea | ||

| Oolong Tea | ||

| Herbal and Fruit Tea Infusions | ||

| Other Product Types | ||

| By Category | Conventional Tea | |

| Organic Tea | ||

| By Flavouring | Unflavoured | |

| Flavoured | ||

| By Packaging Type | Box | |

| Bag | ||

| Pouch | ||

| Sachets | ||

| Other Packaging Type | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convinience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the global tea market be by 2031?

It is forecast to reach USD 214.85 billion by 2031, growing at a 6.13% CAGR.

Which tea segment is expanding the quickest?

Organic certified products lead with a 9.49% CAGR as tighter enforcement boosts consumer trust.

Which distribution channel is growing fastest?

On-trade venues such as cafés and specialty bars register the highest 9.51% CAGR as consumers pay premiums for curated experiences.

Why is Gen Z important to tea growth?

Gen Z drives demand for low-caffeine, functional blends and amplifies product discovery on social media, influencing reformulation and labeling transparency.

Page last updated on: