Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

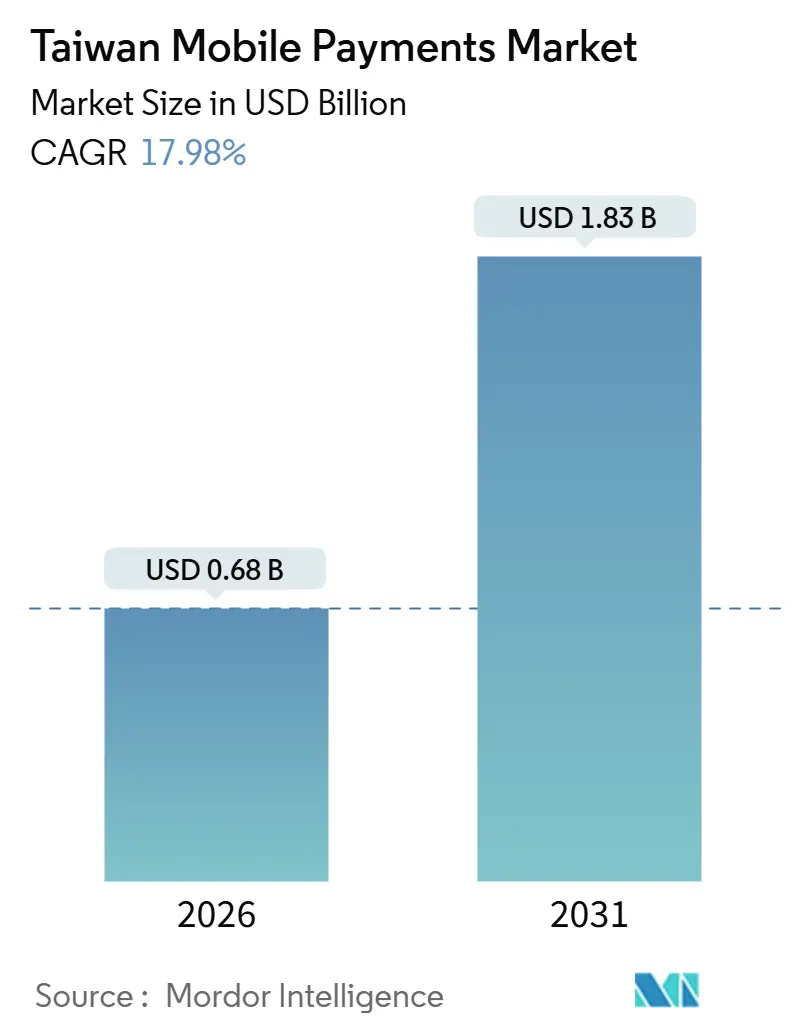

| Market Size (2026) | USD 0.68 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 17.98% CAGR |

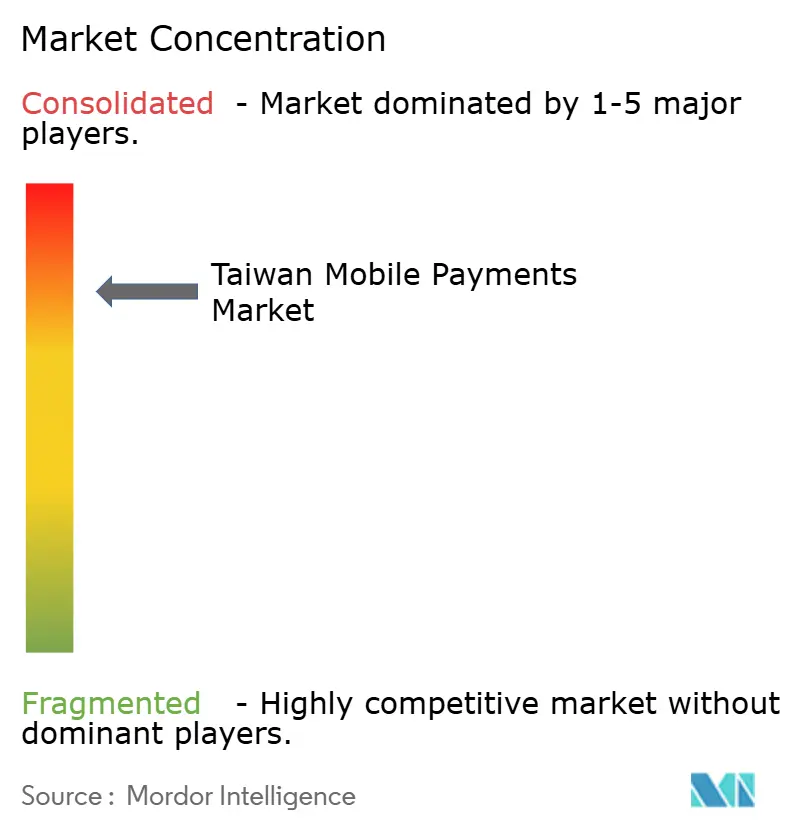

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Mobile Payments Market Analysis by Mordor Intelligence

The Taiwan mobile payments market size reached USD 0.68 billion in 2026 and is projected to advance to USD 1.83 billion by 2031, reflecting a 17.98% CAGR over the forecast period. The surge is propelled by the Executive Yuan’s 90% penetration mandate, real-time settlement rails that slash clearing delays, and open‐API frameworks that let any consumer app trigger payments. Fast broadband coverage, near-universal smartphone ownership, and cross-wallet QR interoperability have broadened use cases beyond e-commerce into transit, bill pay, and peer transfers. Wallet operators are embedding loyalty programs to increase stickiness, while virtual banks and card networks are collapsing QR, NFC, and account-to-account modalities into single merchant endpoints. Competitive intensity remains high, yet the market’s structural tailwinds and supportive regulation continue to expand addressable volumes.

Key Report Takeaways

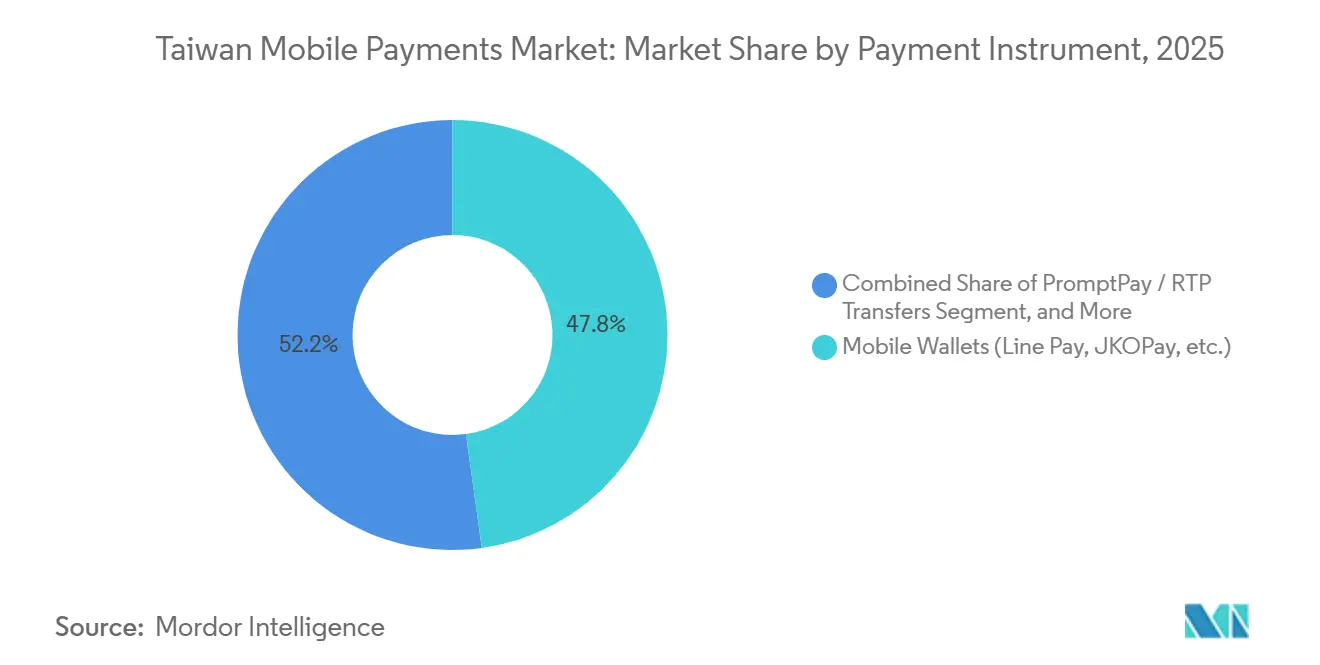

- By payment instrument, mobile wallets held a 47.83% Taiwan mobile payments market share in 2025, whereas instant account-to-account transfers are poised to grow at an 18.73% CAGR through 2031.

- By transaction channel, e-commerce accounted for a 47.83% share of the Taiwan mobile payments market size in 2025, while cross-border and tourist payments are forecast to post an 18.63% CAGR to 2031.

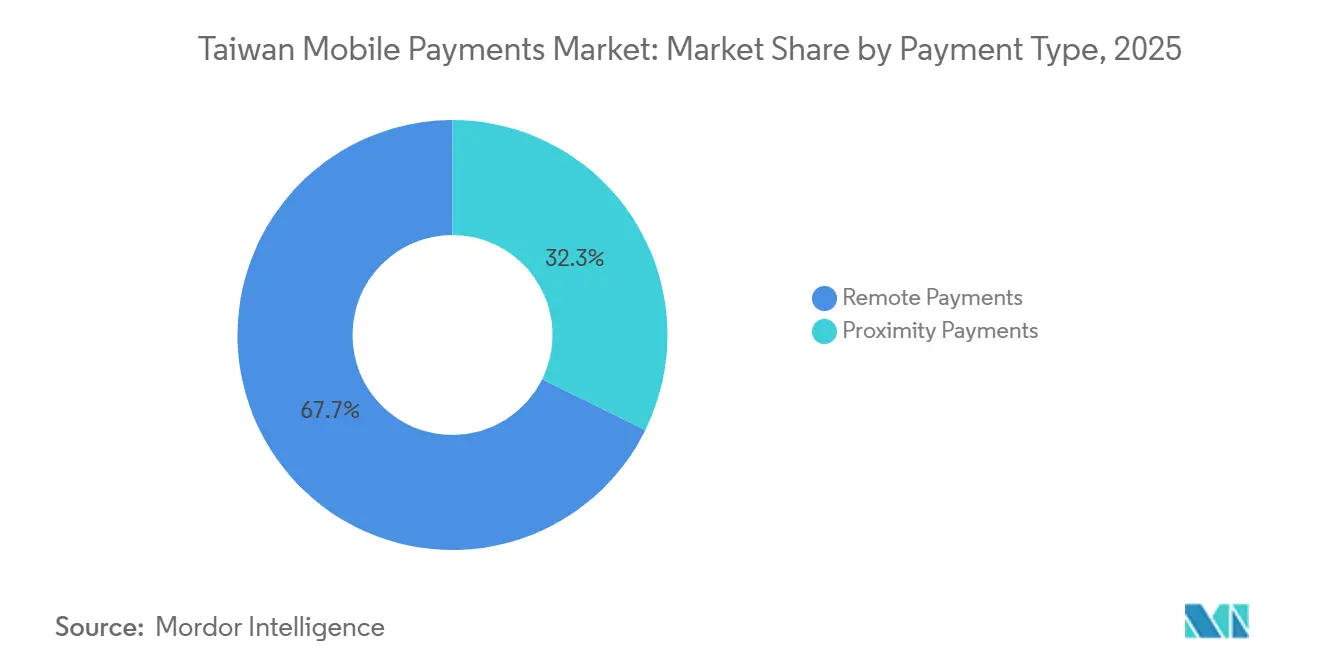

- By payment type, remote payments captured 67.72% of the Taiwan mobile payments market size in 2025 and will continue expanding at an 18.73% CAGR as mobile-first checkout flows reduce cart abandonment.

- By end-user industry, retail and fast-moving consumer goods led with 34.72% revenue share in 2025, whereas hospitality and tourism are projected to register the fastest 18.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government target of 90% mobile-payment penetration by 2025 | +3.2% | National, with early gains in Taipei, New Taipei, Taichung, Tainan, Kaohsiung, Taoyuan | Short term (≤ 2 years) |

| Growing QR-code acceptance for public transport and utilities | +2.8% | National, accelerated rollout in Taipei Metro, Kaohsiung MRT, intercity bus networks | Medium term (2-4 years) |

| Integration of e-wallets with loyalty ecosystems (e.g., "mo coins") | +2.4% | National, strongest in urban retail clusters and convenience-store chains | Medium term (2-4 years) |

| Booming e-commerce and omnichannel retail incentives | +3.5% | National, concentrated in Taipei, New Taipei, Taichung metropolitan areas | Short term (≤ 2 years) |

| Cross-border TWQR and real-time RTP rollout boosting tourist spend | +2.1% | National, with spillover to Hualien, Taitung, Kenting tourist corridors | Medium term (2-4 years) |

| Rise of virtual banks and open-API rails enabling embedded payments | +2.9% | National, led by LINE Bank, Rakuten Bank, NEXT Bank digital-native user bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Target of 90% Mobile-Payment Penetration by 2025

Continuous policy pressure accelerated wallet onboarding, pushing electronic-payment accounts to 34.81 million in October 2025, a 15.8% year-on-year rise.[1]Financial Supervisory Commission, “Electronic Payment Statistics October 2025,” fsc.gov.tw Ministries digitized tax, utilities, and transit fees, while the National Credit Card Center introduced unified TWQR acceptance standards that let night-market stalls and rural cooperatives process multiple wallets on one terminal. The initiative boosted account openings but not all registrants transact regularly, signaling a second-wave challenge of fostering habitual use.

Growing QR-Code Acceptance for Public Transport and Utilities

Taipei Metro’s January 2026 launch of QR ticketing allows commuters to scan wallets at turnstiles, eliminating physical stored-value cards.[2]Taipei Rapid Transit Corporation, “QR Ticketing Deployment Press Release,” metro.taipei iPASS Corporation had already extended TWQR to Kaohsiung MRT and inter-city buses in March 2025. Utilities quickly followed, with Taiwan Power and Taiwan Water integrating LINE Pay and JKOPay bill settlement portals. Daily essential use cases reinforce wallet frequency and shrink cash reliance.

Integration of E-Wallets with Loyalty Ecosystems

Retailers now let shoppers earn and redeem points, such as momo “mo coins”, inside wallet apps, creating a closed loop that merges physical and digital shopping. Convenience-store chains leverage large footprints to funnel traffic into their proprietary wallets, increasing visit frequency and retention. The model strengthens network effects but sustains subsidy costs, pressuring operating margins for pure-play fintechs.

Booming E-Commerce and Omnichannel Retail Incentives

Online retail hit NTD 313.9 billion (USD 9.6 billion) in H1 2024, with mobile accounting for 60% of orders. Merchants promote buy-online-pick-up-in-store discounts and wallet-linked cashback to boost conversion rates, while livestream sellers embed one-click payment links that keep viewers in social media feeds. Aggregated API gateways simplify integration, enabling smaller merchants to accept wallets, cards, and bank transfers through a single contract.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent cash preference in rural/elderly cohorts | -2.1% | Non-municipal regions, rural townships, elderly-concentrated districts | Long term (≥ 4 years) |

| Tight profitability and high subsidy burn among wallet operators | -1.8% | National, affecting all licensed electronic-payment institutions | Medium term (2-4 years) |

| Fragmented QR standards - merchant integration complexity | -1.4% | National, acute in small and medium enterprises, traditional markets | Medium term (2-4 years) |

| Heightened regulatory scrutiny on wallet diversification (e.g., JKO funds) | -1.2% | National, concentrated among operators seeking wealth-management licenses | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Cash Preference in Rural and Elderly Cohorts

Only 7% of September 2025 credit-card volume occurred outside the six largest municipalities, underscoring lagging rural adoption. Infrastructure gaps, limited digital literacy, and trust issues keep cash dominant among citizens over 65. Government programs such as the 2025 NTD 10,000 cash handout nudged many seniors online, yet converting dormant accounts into active payment users requires ongoing education, larger font interfaces, and merchant subsidies.

Tight Profitability and High Subsidy Burn Among Wallet Operators

Taiwan hosts 29 licensed electronic-payment institutions, all battling for share in a low-fee environment regulated by the Financial Supervisory Commission. Heavy cashback and discount campaigns acquire users but erode margins, prompting some wallets to pursue higher-yield services. Regulatory blocks on unapproved wealth-management products, evidenced by JKOPay’s 2025 equity restructuring, limit diversification pathways and may catalyze sector consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Instrument: Instant Settlement Reshapes Wallet Dynamics

Mobile wallets controlled 47.83% of the Taiwan mobile payments market in 2025, yet bank-initiated real-time transfers are forecast to expand at an 18.73% CAGR through 2031 as CIFS infrastructure processes more than 260 million TWQR transactions each year.[3]Central Bank of the Republic of China, “TWQR Transaction Volume Report 2025,” cbc.gov.tw The convergence of QR, NFC, and account-to-account rails lets merchants run a single terminal across multiple schemes, reducing hardware costs.

PromptPay-style RTP hooks embedded in everyday banking apps remove the need to pre-fund stored-value accounts, improving float economics. Card-token solutions such as Apple Pay and Google Pay remain attractive to users unwilling to spread balances across multiple wallets; their growth is largely additive rather than cannibalistic. As LINE Pay’s December 2025 overhaul enables direct bank debit, wallet operators increasingly resemble payment-initiation service providers rather than float-holding institutions, easing capital requirements while boosting transaction ceilings.

By Transaction Channel: Cross-Border Corridors Unlock Tourist Spend

E-commerce garnered 47.83% share in 2025, but cross-border and tourist transactions are expected to climb at an 18.63% CAGR to 2031 as TWQR gains interoperability with South Korea’s BC Card and Visa Cloud-Based Payments. Inbound tourism receipts recovered to USD 10.028 billion in 2024, and real-time settlement ensures merchants receive funds instantly, making QR code acceptance attractive for small hotels and restaurants.

Unified QR gateways, such as Alipay+, enable retailers to reach 1.8 billion potential visitors using their home-country wallets. Domestic commuters reinforce daily volume: Taipei Metro’s January 2026 QR rollout and SoftPOS smartphone terminals in traditional markets broaden acceptance without costly hardware, closing rural gaps and deepening everyday usage.

By Payment Type: Remote Dominance Mirrors Mobile-First Commerce

Remote payments accounted for 67.72% of the Taiwan mobile payments market in 2025, and they are forecast to expand at an 18.73% CAGR through 2031 as one-click authentication in shopping, social, and messaging apps removes friction. Smartphone access is significant across the population, ensuring near-ubiquitous reach.

Proximity payments will remain vital for transit, grocery, and quick-service retail, especially once Taipei Metro activates credit card tap-and-go in 2026. Yet the structural tilt toward mobile-commerce and peer-to-peer transfers secures enduring dominance for remote flows, with proximity usage serving as a high-frequency complement rather than the primary engine of transaction value.

By End-User Industry: Hospitality Surges as Travel Rebounds

Retail and FMCG supplied 34.72% of 2025 revenue, leveraging convenience-store ecosystems that funnel daily spend into proprietary wallets. President Chain Store’s icash Pay and PX Mart’s PXPay Plus illustrate how large retailers bind payments to loyalty, guaranteeing repeat traffic.

Hospitality and tourism, however, is projected to register an 18.62% CAGR to 2031 as QR interoperability lets visitors pay with their domestic wallets and local businesses receive instant local-currency settlement. The Central Bank’s real-time infrastructure decreases chargeback risk, accelerating adoption by smaller accommodation and dining operators. Transportation, utilities, and emerging sectors such as education inch forward on specialized use cases, but tourism-related categories set the briskest pace.

Geography Analysis

Taipei, New Taipei, Taichung, Tainan, Kaohsiung, and Taoyuan together accounted for 93.87% of credit card transaction value in September 2025, reflecting superior terminal density, higher disposable income, and younger demographics. Rural townships lack both QR hardware and merchant training, and older residents remain wary of digital payments. The National Credit Card Center began rolling out subsidized TWQR readers in traditional markets and fishing harbors in 2023, yet uptake is incremental.

Despite these disparities, nationwide internet coverage reaches 96.7%, and mobile subscriptions equal 127% of the population, meaning infrastructure constraints are more about last-mile merchant equipment than network availability. Government cash-rebate programs require online enrollment, nudging rural citizens to open e-payment accounts even if daily activity lags.

Cross-border linkages enhance regional clout; for example, TWQR’s tie-up with BC Card allows Korean tourists to pay in won, while Visa’s November 2024 LINE Pay integration extends acceptance across Southeast Asia. Reciprocal arrangements with Japan’s Bank of the Ryukyus let EasyWallet users tap Okinawa terminals and Japanese visitors scan TWQR. Immediate settlement cushions foreign-exchange exposure for merchants and positions Taiwan as a cash-light tourism hub.

Competitive Landscape

Taiwan has 29 licensed e-payment institutions under the oversight of the Financial Supervisory Commission. LINE Pay, JKOPay, PXPay Plus, and iPASS Money jointly retained most of wallet users in 2025, yet none secured sustainable profit because consumer acquisition still hinges on cashback and fee waivers. LINE Pay leverages 12 million chat users for in-app commerce, PXPay Plus taps PX Mart’s 1,100 supermarkets for loyalty-tethered grocery spend, and iPASS Money rides Kaohsiung MRT’s rider base.

Global card networks are embedding QR code functionality atop existing NFC infrastructure, so one countertop reader can capture tap or scan, a boon for smaller retailers with limited hardware budgets. Virtual banks offer open APIs that let ride-hailing or food-delivery platforms trigger payment directly from customer accounts, raising competitive stakes for traditional issuers.

Regulatory firmness shapes strategy. JKOPay’s July 2025 equity restructuring underscored the need for vigilance in governance and fund diversification. New fraud-prevention statutes require stronger identity verification, raising compliance costs but elevating entry barriers. As subsidy fatigue mounts, mid-tier wallets may merge or exit, while larger ecosystems deepen vertical integrations around retail, social media, and transportation.

Taiwan Mobile Payments Industry Leaders

LINE Pay Corporation

Apple Inc. (Apple Pay)

JKOPay Co., Ltd.

Taiwan Mobile Payment Co., Ltd. (Taiwan Pay)

Alphabet Inc. (Google Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Taipei Metro and city buses activated QR ticketing on January 3, extending wallet payments to daily commuters.

- December 2025: LINE Pay launched a standalone e-payment app with direct bank-linking capability.

- July 2025: JKOPay underwent a court-ordered NTD 3.6 billion equity restructuring that temporarily delisted the app from marketplaces.

- March 2025: The Digital Identity Wallet prototype entered regulatory sandbox testing, targeting selective-disclosure credentials by year-end.

Taiwan Mobile Payments Market Report Scope

The Japan Mobile Payments Market Report is Segmented by Payment Instrument (PromptPay/RTP Transfers, Mobile Wallets, Card-based Mobile Payments, Carrier Billing/Others), Transaction Channel (In-store POS, E-commerce, P2P Transfers, Bill and Government Payments, Cross-border/Tourist), Payment Type (Proximity Payments, Remote Payments), and End-User Industry (Retail and FMCG, Transportation and Mobility, Hospitality and Tourism, Utilities and Telecom, Healthcare and Education, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Payment Instrument

| PromptPay / RTP Transfers |

| Mobile Wallets (Line Pay, JKOPay, etc.) |

| Card-based Mobile Payments |

| Carrier Billing / Others |

By Transaction Channel

| In-store POS |

| E-commerce |

| P2P Transfers |

| Bill and Government Payments |

| Cross-border / Tourist |

By Payment Type

| Proximity Payments |

| Remote Payments |

By End-User Industry

| Retail and FMCG |

| Transportation and Mobility |

| Hospitality and Tourism |

| Utilities and Telecom |

| Healthcare and Education |

| Other End-User Industries |

| By Payment Instrument | PromptPay / RTP Transfers |

| Mobile Wallets (Line Pay, JKOPay, etc.) | |

| Card-based Mobile Payments | |

| Carrier Billing / Others | |

| By Transaction Channel | In-store POS |

| E-commerce | |

| P2P Transfers | |

| Bill and Government Payments | |

| Cross-border / Tourist | |

| By Payment Type | Proximity Payments |

| Remote Payments | |

| By End-User Industry | Retail and FMCG |

| Transportation and Mobility | |

| Hospitality and Tourism | |

| Utilities and Telecom | |

| Healthcare and Education | |

| Other End-User Industries |

Key Questions Answered in the Report

How big is the Taiwan mobile payments market today and how fast is it expanding?

The Taiwan mobile payments market size reached USD 0.68 billion in 2026 and is forecast to rise to USD 1.83 billion by 2031, reflecting a robust 17.98% CAGR.

Which payment instruments are growing the quickest in Taiwan?

Real-time account-to-account transfers inside banking apps are projected to grow at an 18.73% CAGR through 2031, gradually closing the gap with mobile wallets.

What drives everyday use of mobile wallets among Taiwanese consumers?

QR ticketing for metro and bus rides, utility bill pay integrations, and loyalty-point redemption at convenience stores embed wallets into daily routines and lift transaction frequency.

Why is cross-border QR acceptance important for Taiwan?

Partnerships with South Korea’s BC Card and Visa Cloud-Based Payments let tourists pay with their home wallets, instantly settling funds for local merchants and boosting visitor spend.

What challenges limit mobile payment uptake outside major cities?

Rural areas face fewer QR terminals and an older population still prefers cash, so penetration lags despite nationwide internet coverage and government incentives.

Page last updated on: